- Industrial Machinery

- Elevator Maintenance Market

Elevator Maintenance Market Size, Share, and Growth Forecast, 2026 - 2033

Elevator Maintenance Market by Component Maintained (Traction Systems, Control Systems, Others), Service Type (Preventive Maintenance, Predictive Maintenance, Others), End-user, and Regional Analysis for 2026 - 2033

Elevator Maintenance Market Size and Trends Analysis

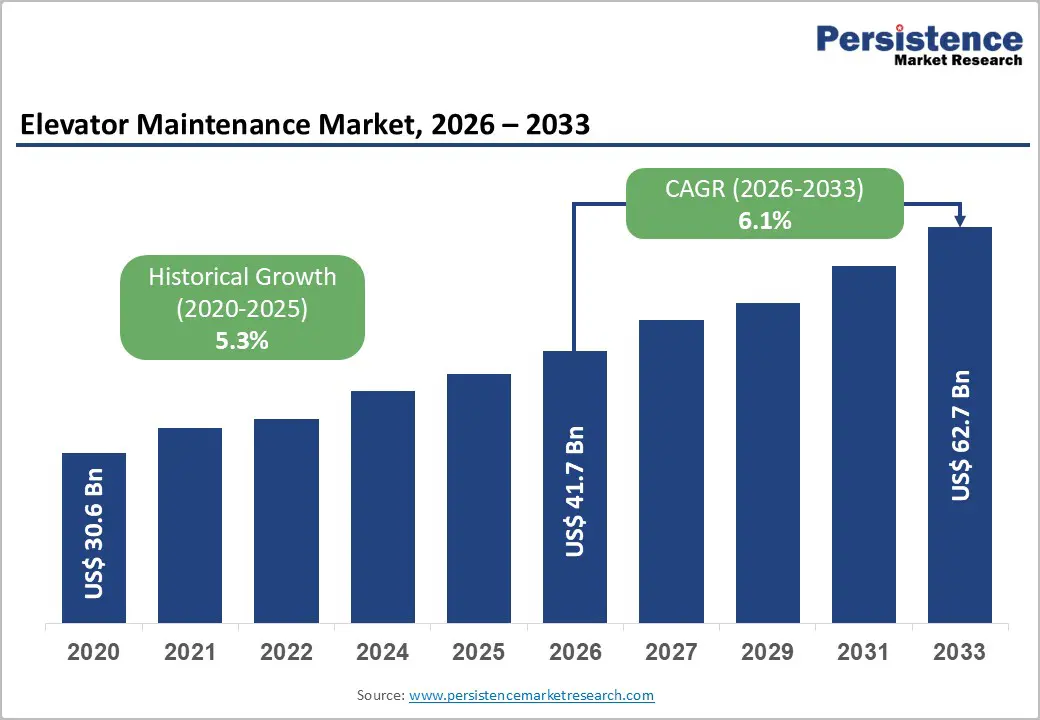

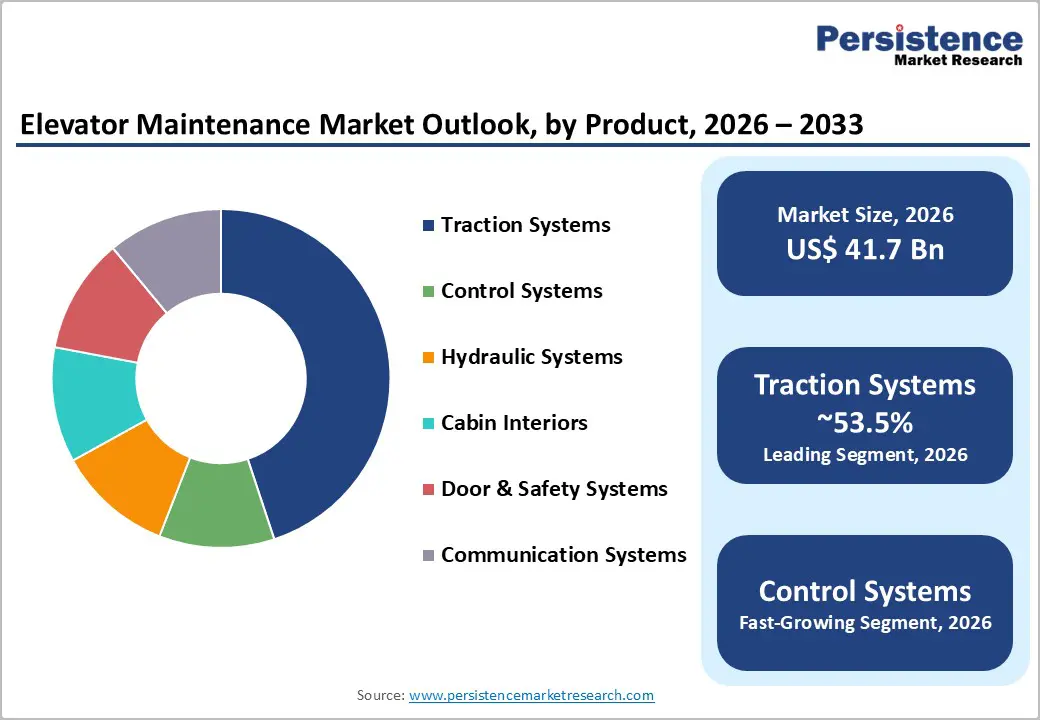

The global elevator maintenance market size is likely to be valued at US$41.7 billion in 2026 and is expected to reach US$62.7 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033, driven by urbanization, an aging global elevator installed base, and accelerating adoption of IoT-enabled predictive maintenance solutions.

Recurring service contracts and modernization activities represent the largest and most stable revenue streams, while predictive and remote maintenance services constitute the fastest-growing segments within the market. Growth is fueled by rising urban construction, aging elevators needing upgrades, and increased investment in digital service platforms for smarter, cost-efficient maintenance.

Key Industry Highlights

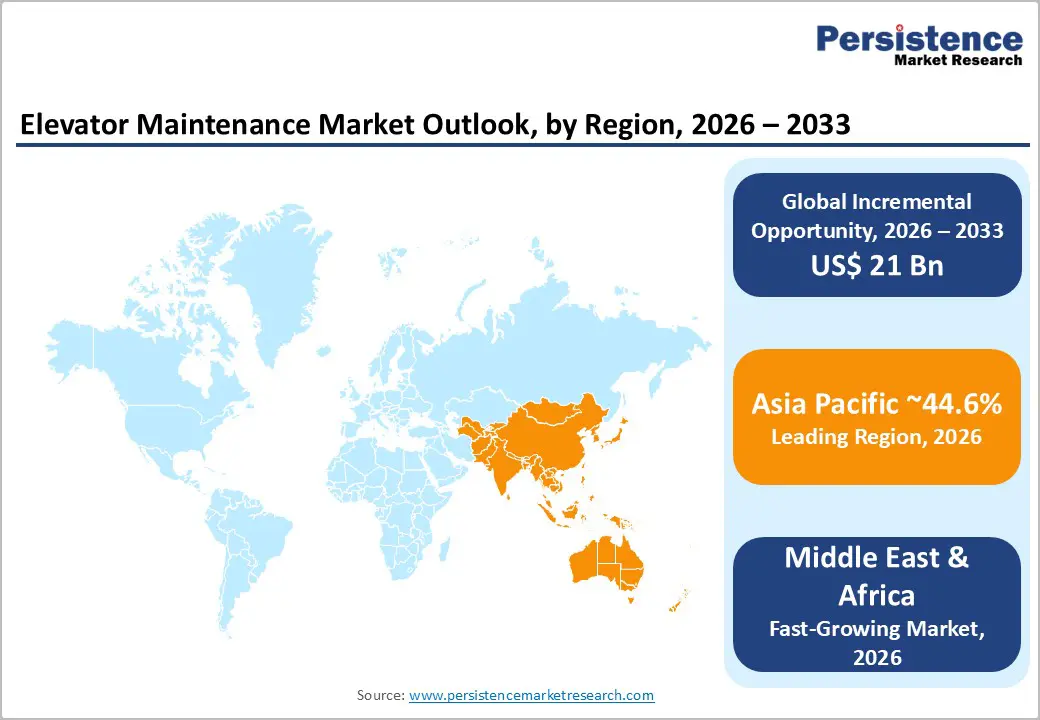

- Leading Region: Asia Pacific is projected to account for approximately 44.6% of the market share, driven by the world’s largest installed elevator base across China, Japan, India, and ASEAN economies, supported by urbanization and mandatory safety maintenance regimes.

- Fastest-growing Region: The Middle East & Africa, registering the highest growth rate globally due to large-scale infrastructure projects, high-rise construction, and tourism-led developments in GCC countries, alongside rising adoption of premium and digitally enabled maintenance contracts.

- Investment Plans: Market leaders are prioritizing digital service platforms, predictive maintenance technologies, technician upskilling, and regional service acquisitions, with capital deployment focused on IoT-enabled diagnostics, cloud-based monitoring systems, and consolidation of fragmented local service providers, particularly in North America and the Middle East.

- Dominant Component Maintained: Traction systems are anticipated to represent approximately 53.5% of the market share, reflecting their prevalence in high-rise buildings, higher safety risk exposure, and elevated regulatory scrutiny requiring frequent inspections and modernization.

- Leading Service Type: Preventive maintenance is estimated to hold roughly 40.8% of market share, supported by regulatory mandates, insurance compliance requirements, and long-term maintenance contracts that ensure predictable cash flows and asset lifecycle optimization.

| Key Insights | Details |

|---|---|

| Elevator Maintenance Market Size (2026E) | US$41.7 Bn |

| Market Value Forecast (2033F) | US$62.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Urbanization and New Installations

Global urbanization continues to drive sustained demand for elevators in residential, commercial, and mixed-use developments. The expansion of urban housing, office towers, transportation hubs, and retail complexes increases elevator density per square kilometer, directly enlarging the addressable maintenance market. Each new elevator installation generates a multi-decade maintenance requirement, creating long-term recurring revenue streams for service providers.

Building owners and property managers increasingly prioritize uptime, passenger safety, and digital tenant experience. As a result, maintenance contracts are evolving beyond basic servicing to include performance-based service-level agreements that integrate diagnostics, analytics, and uptime guarantees. Centralized maintenance platforms are increasingly adopted across large portfolios to reduce downtime and optimize the total cost of ownership.

Aging Installed Base and Modernization Cycle

A substantial portion of the global elevator fleet has surpassed 20 years of service life, significantly increasing demand for modernization and component replacement. Aging systems experience higher failure rates, lower energy efficiency, and increased safety risks, making modernization economically and regulatory necessary. Modernization projects typically include upgrades to drives, control systems, safety equipment, and cabin interiors. Modernization significantly increases the average contract value and introduces high-margin, one-time upgrade revenue alongside ongoing maintenance revenue. Regulatory requirements and energy-efficiency incentives further accelerate the adoption of modernization. Phased modernization programs enable service providers to convert low-margin corrective maintenance into structured, long-term lifecycle engagements.

Digitalization and Predictive Maintenance Adoption

The integration of sensors, edge computing, and cloud analytics is transforming elevator maintenance from time-based servicing to condition-based and predictive models. These systems continuously monitor elevator performance parameters, enabling early fault detection and optimized maintenance scheduling. Predictive maintenance delivers measurable reductions in downtime and spare parts costs. Service providers offering predictive maintenance achieve higher renewal rates, stronger customer retention, and increased revenue per unit. Tiered service offerings, ranging from basic preventive to premium predictive plans, enhance monetization while improving operational efficiency through data-driven field service optimization.

Barrier Analysis - High Upfront Modernization Costs and Budget Constraints

Modernization and IoT retrofits require substantial capital investment, which is often constrained by building owners’ budget cycles. In price-sensitive markets and smaller portfolios, high upfront costs delay modernization decisions, increasing reliance on reactive maintenance. When modernization costs exceed 3-6% of property value, owners frequently defer upgrades, increasing failure risk and service volatility.

Skilled Technician Shortage and Regulatory Complexity

The elevator maintenance industry faces persistent shortages of technicians with combined mechanical, electrical, and software expertise. Training and certification requirements vary widely across jurisdictions, increasing compliance costs. Stringent safety regulations, licensing requirements, and labor standards raise operational barriers, favoring large service providers with established training and compliance infrastructure while constraining smaller players.

Opportunity Analysis - Predictive Maintenance Platform Expansion

Predictive maintenance represents the highest-value growth opportunity within the market. As adoption expands from premium commercial portfolios to mid-scale residential and mixed-use buildings, this segment is expected to grow into a multi-billion-dollar addressable market by the early 2030s. Providers converting clients from preventive to predictive contracts benefit from recurring software fees, reduced churn, and higher lifetime customer value.

Modernization Financing and Phased Upgrade Models

Phased modernization approaches allow building owners to spread upgrade investments across multiple years while realizing immediate safety and energy-efficiency gains. Financing-backed modernization programs convert large upfront expenditures into manageable operating costs. This model expands the addressable market, particularly in cost-sensitive regions, and increases total spend per installed unit over the asset lifecycle.

Category-wise Analysis

Component Maintained Insights

Traction systems are anticipated to account for approximately 53.5% of total component maintenance expenditure, reflecting their structural dominance in high-rise residential towers, commercial office buildings, and mixed-use developments. These systems encompass traction motors, gearboxes, hoisting ropes, counterweights, and drive assemblies, all of which require frequent safety inspections, load testing, rope replacements, and certified technician intervention. Regulatory authorities in major markets mandate periodic audits for traction elevators due to their critical role in passenger safety and vertical mobility reliability.

From a cost perspective, traction systems command higher annual maintenance contracts (AMCs) and modernization budgets compared to hydraulic or cabin components. For example, global OEMs such as Otis, KONE, and Schindler allocate a substantial portion of their service revenues to traction motor retrofits and rope replacement programs in aging urban building stock. The high safety risk, energy intensity, and regulatory oversight associated with traction systems ensure sustained demand and pricing power for service providers over the forecast period.

Control systems represent the fastest-growing component maintenance segment, driven by the rapid digitalization of elevator infrastructure worldwide. Modern elevators increasingly rely on microprocessor-based controllers, destination dispatch systems, sensors, and cloud-connected electronics, all of which require continuous software updates, firmware upgrades, cybersecurity monitoring, and remote diagnostics.

This evolution shifts maintenance from purely mechanical servicing toward software-centric and data-driven service models. Leading players such as KONE (DX elevators) and Thyssenkrupp (MAX platform) have integrated IoT-enabled control systems that allow real-time fault detection and remote intervention. As a result, control system maintenance generates higher-margin recurring revenue, supports premium digital service tiers, and strengthens long-term customer lock-in. The growing penetration of smart buildings and intelligent transportation systems further accelerates demand for advanced control system maintenance.

Service Type Insights

Preventive maintenance is anticipated to retain the largest service share at approximately 40.8%, underpinned by strict safety regulations, insurance compliance requirements, and asset risk mitigation priorities. Scheduled inspections, lubrication cycles, mechanical adjustments, and component wear checks form the backbone of long-term maintenance contracts across residential, commercial, and public infrastructure segments.

In many jurisdictions, building codes explicitly require documented preventive maintenance programs to ensure elevator operating permits remain valid. For service providers, preventive maintenance delivers predictable recurring revenue streams and high contract renewal rates. Large portfolios managed by companies such as TK Elevator and Mitsubishi Electric rely heavily on standardized preventive programs to optimize technician utilization and reduce liability exposure. From a customer perspective, preventive maintenance enhances asset lifespan, stabilizes operating costs, and protects property valuation, making it a foundational element of the elevator maintenance market.

Predictive maintenance is emerging as the fastest-growing service category, as condition-based monitoring increasingly replaces traditional calendar-based servicing. Leveraging IoT sensors, machine learning algorithms, and real-time performance analytics, predictive models identify component degradation before failures occur.

This approach significantly reduces unplanned downtime, improves passenger safety, and optimizes spare-parts inventory management. Service providers are monetizing predictive maintenance through premium pricing structures and performance-based service-level agreements (SLAs). Platforms such as Otis ONE and Schindler Ahead enable remote diagnostics and proactive interventions, allowing operators to shift from reactive repairs to outcome-driven maintenance. As building owners prioritize uptime, energy efficiency, and lifecycle cost reduction, predictive maintenance is expected to play a central role in margin expansion and competitive differentiation within the service ecosystem.

Regional Insights

North America Elevator Maintenance Market Trends - High-Value, Regulation-Driven Market Focused on Modernization and Digital Service Platforms

North America remains a high-value and regulation-driven elevator maintenance market, with the U.S. accounting for the majority of regional revenue. The region’s large installed base of elevators, many exceeding 20-25 years of service life, creates sustained demand for maintenance, safety upgrades, and phased modernization. Higher labor costs, stringent safety codes (such as ASME A17.1/CSA B44), and insurance compliance requirements elevate service pricing and favor long-term maintenance contracts over ad-hoc repairs. As a result, North America generates among the highest revenue per unit (RPU) globally for elevator service providers. Aging urban infrastructure and accessibility mandates further reinforce market stability.

Compliance with the Americans with Disabilities Act (ADA) continues to drive upgrades to control panels, door systems, and cabin interfaces in residential and public buildings. In parallel, modernization programs across legacy office towers in cities such as New York, Chicago, and Toronto are increasing demand for control system retrofits and energy-efficient traction upgrades. For example, Otis Elevator Company has expanded adoption of its Otis ONE digital platform across U.S. commercial portfolios, enabling remote diagnostics and predictive maintenance to reduce downtime and labor inefficiencies.

Investment activity in North America is concentrated in digital service platforms, technician reskilling, and bolt-on acquisitions of independent service companies. Players such as TK Elevator and KONE have strengthened regional coverage through targeted acquisitions of local maintenance firms, allowing faster response times and deeper penetration into mid-rise residential segments. These strategies enhance customer retention while improving operating margins in a labor-intensive market. Overall, North America offers stable, cash-generative growth, with technology adoption acting as a key differentiator rather than new installations.

Middle East & Africa Elevator Maintenance Market Trends - Rapid Urban Expansion and Smart-Building Maintenance Fuel High-Growth Opportunities

The Middle East & Africa (MEA) region represents the fastest-growing elevator maintenance market, supported by large-scale urban development, infrastructure investment, and tourism-driven construction. Gulf Cooperation Council (GCC) countries, particularly Saudi Arabia, the UAE, and Qatar, are leading the demand for premium elevator systems and high-availability maintenance contracts aligned with international safety standards. Mega-projects such as mixed-use skyscrapers, transit hubs, and hospitality complexes significantly increase the installed base, creating long-term maintenance revenue pipelines.

Saudi Arabia’s Vision 2030 initiatives have accelerated vertical construction across cities such as Riyadh and Jeddah, driving demand for both new elevator installations and lifecycle maintenance services. Global OEMs such as Schindler, Mitsubishi Electric, and KONE have expanded regional service capabilities to support high-rise residential towers and commercial landmarks. In the UAE, smart building adoption in Dubai has increased demand for digitally enabled maintenance contracts, particularly for destination control systems and predictive analytics.

The MEA market remains highly fragmented, especially outside the GCC, with numerous local service providers operating alongside global OEMs. This fragmentation creates strong consolidation opportunities, as multinational players acquire or partner with regional firms to expand coverage and standardize service quality. Phased modernization models and flexible financing arrangements are gaining traction, enabling building owners to upgrade aging elevator systems without full replacements. Collectively, these dynamics position the MEA as a high-growth, margin-accretive region for elevator maintenance providers willing to invest in local presence and technical expertise.

Asia Pacific Elevator Maintenance Market Trends - Scale-Driven Market with Aging Inventory, Regulatory Oversight, and Predictive Maintenance Adoption

Asia Pacific dominates the market with an estimated 44.6% share, driven by the sheer scale of installed elevators across China, Japan, India, and ASEAN economies. Rapid urbanization, dense high-rise development, and government-led housing and transit programs have resulted in the world’s largest elevator base, particularly in China. Even marginal increases in maintenance revenue per unit translate into significant absolute market growth due to volume.

China remains the single largest national market, supported by a vast aging elevator stock installed during the 2000s construction boom. Regulatory focus on safety inspections and accident prevention has increased demand for mandatory maintenance contracts and modernization of control and door systems. Domestic players such as Hitachi China, Shanghai Mitsubishi, and Canny Elevator compete alongside global OEMs, intensifying price competition while accelerating digital adoption.

Japan represents a mature but technology-intensive market, with strong demand for predictive maintenance and seismic-resilient upgrades. Companies such as Mitsubishi Electric lead in advanced diagnostics and reliability-focused service offerings. India and Southeast Asia are emerging as high-growth maintenance markets, driven by rapid residential construction, metro rail projects, and smart city initiatives. Global brands such as Otis and KONE are expanding technician networks and localized service hubs to support growing mid-rise portfolios. Asia Pacific remains the largest and most strategically important region, combining scale, regulatory momentum, and long-term urban growth.

Competitive Landscape

The global elevator maintenance market is moderately consolidated, with global OEM service divisions controlling high-value contracts and modernization projects, while regional independents dominate smaller residential and local commercial accounts. This structure supports ongoing consolidation, particularly in fragmented emerging markets.

Market leaders emphasize predictive maintenance platforms, phased modernization, geographic expansion through acquisitions, and financing-enabled service models. Differentiation increasingly depends on digital capabilities, response speed, and outcome-based service agreements.

Key Industry Developments

- In April 2025, Schindler Elevator Corporation launched the Schindler-5000 machine-room-less (MRL) elevator in the U.S., designed for low- to mid-rise buildings with advanced connectivity, improving maintenance access and integration with digital service tools.

- In August 2025, KONE Corporation introduced its “24/7 Connected Services” global maintenance offering featuring enhanced IoT integration, real-time predictive analytics, and remote diagnostics, strengthening its predictive service capabilities.

Companies Covered in Elevator Maintenance Market

- Otis Elevator Company

- Schindler Group

- KONE Corporation

- TK Elevator

- Mitsubishi Electric Corporation

- Hitachi Ltd.

- Fujitec Co., Ltd.

- Hyundai Elevator Co., Ltd.

- Johnson Lifts Private Limited

- Sigma Elevator Company

- Canny Elevator Co., Ltd.

- Stannah Group

- Dover Elevator

- Orona Group

- Kleemann Hellas

- Express Lift Company

- AVT Beckett

- Escon Elevators Pvt. Ltd.

Frequently Asked Questions

The global elevator maintenance market is valued at US$41.7 billion in 2026.

By 2033, the elevator maintenance market is expected to reach US$62.7 billion, supported by recurring service contracts and modernization demand.

Key trends include the shift from preventive to predictive maintenance, increased adoption of IoT-enabled remote monitoring, rising modernization of aging elevator fleets, and growing use of phased upgrades and financing models to reduce upfront costs for building owners.

By component, traction systems are the leading segment, accounting for 53.5% of total maintenance spend, driven by their dominance in high-rise residential and commercial buildings.

The elevator maintenance market is projected to grow at a CAGR of 6.1% between 2026 and 2033.

Major players include Otis Elevator Company, KONE Corporation, Schindler Group, TK Elevator, and Mitsubishi Electric Corporation.