- Inks, Coatings, Adhesives & Sealants (ICAS)

- Elastomeric Coating Market

Elastomeric Coating Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Elastomeric Coating Market by Product Type (Acrylic, Silicone, Polyurea, Polyurethane, Epoxy, Others), Technology (Water-borne, Solvent-borne), Application (Building & Construction - Roof, Wall, Floor, Bridges, Others; Industrial; Automotive and Transportation; Others), by Regional Analysis, 2026 - 2033

Elastomeric Coating Market Size and Trend Analysis

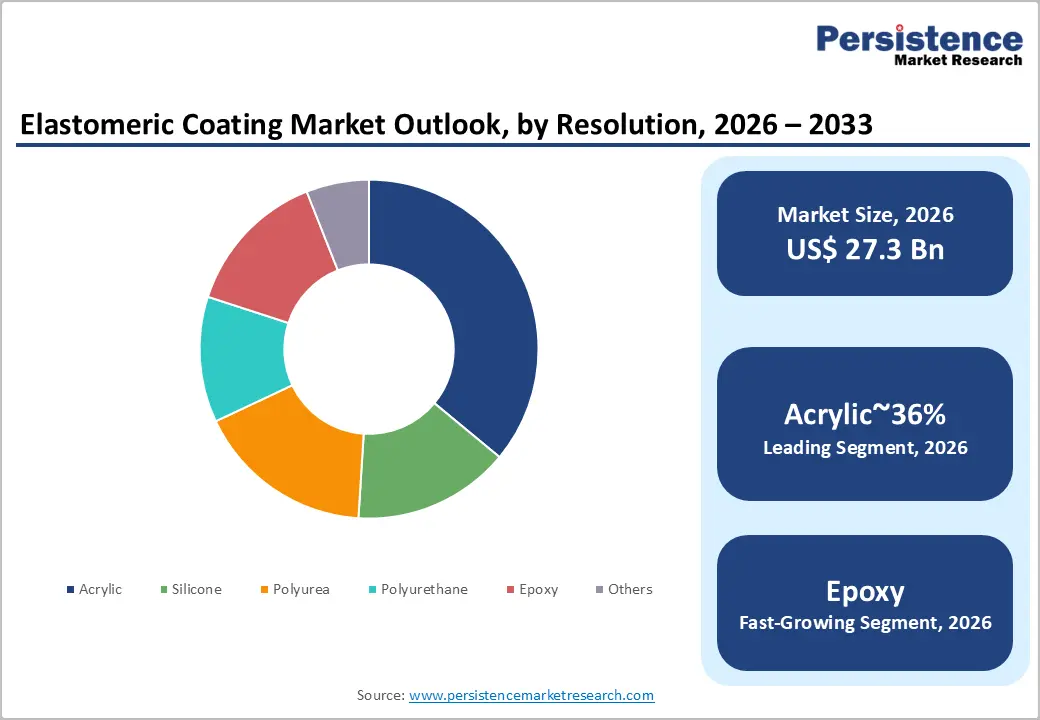

The global elastomeric coating market size is likely to be valued at US$ 27.3 billion in 2026 and is expected to reach US$ 47.1 billion by 2033, growing at a CAGR of 8.1% during the forecast period from 2026 to 2033.

This growth trajectory is primarily underpinned by the rising use of elastomeric coatings in building and construction for waterproofing, thermal insulation, and façade protection, alongside tightening VOC and energy-efficiency regulations in major economies that favor water-borne, low-emission formulations.

Key Industry Highlights:

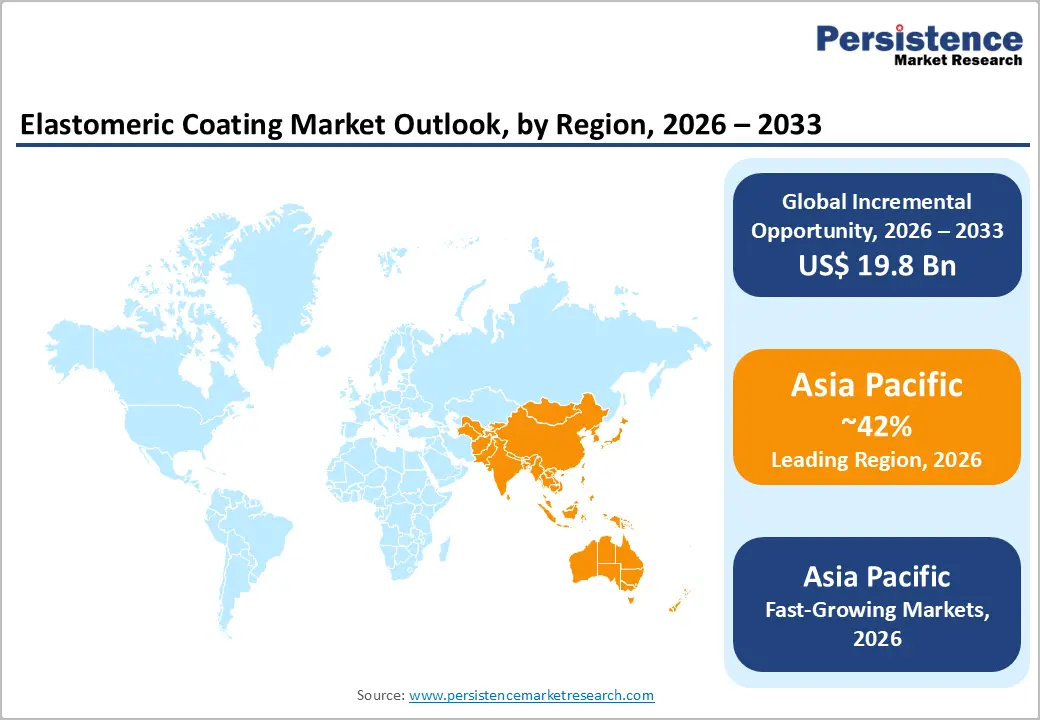

- Leading Region: Asia Pacific has emerged as a key demand center for elastomeric coatings, supported by rapid urbanization, large-scale residential and commercial construction, and aggressive infrastructure development programs across China, India, and ASEAN economies.

- Fastest growing region: Asia Pacific is also the fastest-growing regional market, with high growth in reflective roof and waterproofing applications driven by hot climates, energy efficiency initiatives, and increasing adoption of water-borne technologies amid tightening environmental regulations.

- Dominant segment: Within applications, building & construction, particularly roof and wall protection, commands the largest share of elastomeric coating demand, reflecting its critical role in waterproofing, crack-bridging, and extending the service life of concrete and masonry structures.

- Fastest growing segment: Water-borne acrylic elastomeric coatings are expected to be the fastest-growing segment, benefiting from global VOC reduction policies, improved performance of advanced polymer binders, and strong alignment with green building and occupant health priorities.

- Key market opportunity: The expansion of cool roof and reflective elastomeric systems for heat-island mitigation and building decarbonization represents a major opportunity, particularly as cities and policymakers incentivize high-albedo roofing solutions to cut cooling loads and peak power demand.

| Key Insights | Details |

|---|---|

| Elastomeric Coating Market Size (2026E) | US$ 27.3 Billion |

| Market Value Forecast (2033F) | US$ 47.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.1% |

| Historical Market Growth (2020 - 2025) | 7.3% |

Market Dynamics

Drivers - Global Shift Toward Energy-Efficient, Low-VOC Building Envelopes Accelerates Demand for Elastomeric Roof and Wall Coatings

One of the most powerful growth drivers for the elastomeric coating market is the global shift toward sustainable, energy-efficient buildings designed to reduce long-term operating costs and carbon emissions. Elastomeric roof and wall coatings, particularly water-borne acrylic systems, enhance thermal reflectance and significantly limit heat absorption, helping buildings stay cooler in hot climates. When applied as reflective “cool roof” solutions, these coatings can reduce cooling energy consumption by double-digit percentages, making them attractive to both new construction and retrofit projects.

Regulatory frameworks, such as the U.S. EPA’s VOC limits under 40 CFR Part 59, along with green building certifications like LEED, strongly favor low-VOC and high-reflectance materials, accelerating the replacement of traditional solvent-borne paints. Rapid urbanization and rising construction investments in Asia Pacific and the Middle East further strengthen adoption, as building owners prioritize durability, regulatory compliance, occupant comfort, and long-term asset value.

Rising Infrastructure Rehabilitation and Waterproofing Requirements Across Harsh Climatic Conditions Drive Elastomeric Coating Adoption

Another major driver of elastomeric coating demand is the growing need to rehabilitate and protect aging infrastructure exposed to harsh environmental conditions. Bridges, tunnels, highways, industrial plants, and transportation facilities face constant stress from moisture, UV exposure, temperature fluctuations, and chemical contact. Elastomeric coatings offer high elongation, crack-bridging capability, and strong adhesion, allowing them to seal hairline cracks and prevent water ingress that can lead to corrosion, freeze-thaw damage, and structural deterioration.

Governments across North America, Europe, and emerging economies are allocating significant budgets to infrastructure renewal programs, where durable waterproofing systems are specified to extend service life and reduce maintenance costs. In parallel, industrial facilities, including power generation, chemical processing, and water treatment plants, use elastomeric coatings for containment protection and exterior durability. These applications create steady, recurring demand even in mature construction markets.

Restraints - Raw Material Price Volatility and Supply Chain Instability Pressure Margins and Project Economics for Elastomeric Coating Manufacturers

The elastomeric coating market faces ongoing pressure from volatility in raw material prices, particularly for acrylic, polyurethane, and epoxy resins derived from petrochemical feedstocks. Fluctuations in crude oil and natural gas prices directly impact resin and monomer costs, creating margin uncertainty for manufacturers. Global supply chain disruptions, driven by geopolitical tensions, shipping delays, and logistics bottlenecks, further complicate procurement and inventory planning.

These challenges often result in price increases passed on to customers, which can delay projects or push buyers toward lower-cost alternatives, especially in price-sensitive regions. Smaller and regional manufacturers are particularly vulnerable, as they lack backward integration, long-term supply contracts, and hedging mechanisms available to large multinational players such as BASF and Dow. As a result, committing to fixed-price contracts becomes difficult, increasing commercial risk and reducing short-term market stability.

Performance Sensitivity and Application Challenges in Extreme Environments Limit Elastomeric Coating Use in Specialized Applications

Despite their many advantages, elastomeric coatings face certain performance and application limitations that can restrict adoption in specialized environments. Water-borne acrylic elastomeric systems may struggle with low-temperature curing, high humidity application windows, or continuous chemical immersion, leading engineers to specify alternatives such as polyurea or high-build epoxy coatings for extreme conditions. In addition, elastomeric coatings are highly sensitive to surface preparation and application thickness.

Poor substrate cleaning, inadequate priming, or incorrect film build can cause blistering, adhesion failure, or premature wear, particularly on aged or contaminated roofs. These failures can negatively affect customer perception and confidence in the technology. Successful performance often depends on trained applicators, strict quality control, and adherence to manufacturer guidelines. In regions with limited skilled labor or weak enforcement of application standards, these requirements act as a barrier to wider market penetration.

Opportunity - Growing Adoption of Cool Roof and Reflective Elastomeric Systems Creates Strong Opportunities in Urban Heat Mitigation Projects

A major growth opportunity lies in the rapid expansion of cool roof and high-reflectance elastomeric coatings aimed at addressing urban heat island effects and supporting climate-resilient cities. Advanced formulations, such as reflective acrylic binders and elastomeric white roof coatings, combine high solar reflectance and thermal emissivity with flexibility and crack-bridging performance. Governments and municipalities across the U.S., Europe, and Asia are increasingly promoting or mandating reflective roofing through building codes, incentive programs, and sustainability policies to reduce cooling demand and lower greenhouse gas emissions.

Elastomeric cool roof systems are especially attractive for retrofitting existing buildings, as they can be applied over aged membranes or metal roofs with minimal disruption. Their cost-effectiveness, ease of installation, and energy-saving benefits create strong demand potential. Manufacturers offering certified systems, proven performance data, and long-term warranties are well positioned to capture this expanding opportunity.

Advanced High-Performance Elastomeric Formulations Unlock Premium Opportunities in Industrial, Automotive, and Transportation Markets

Another high-value opportunity is the development of advanced elastomeric coatings designed for demanding industrial, automotive, and transportation applications. These sectors require coatings that combine flexibility with abrasion resistance, chemical durability, and long service life. Leading companies such as BASF, Covestro, and Huntsman continue to invest in polyurethane and polyurea technologies for heavy-duty linings, underbody protection, and protective membranes.

In railways, commercial vehicles, and transport infrastructure, elastomeric systems help reduce vibration, protect against stone-chip damage, and provide long-lasting waterproofing for decks and bridges. As asset owners increasingly focus on total cost of ownership and predictive maintenance, demand is rising for integrated coating systems supported by technical services, digital inspection tools, and extended warranties. Suppliers that can deliver high-performance formulations alongside value-added services stand to achieve premium pricing and stronger long-term customer relationships.

Category-wise Analysis

By Product Type Insights

Acrylic-based elastomeric coatings hold the largest share of the global market, accounting for approximately 36% of total demand due to their strong balance of cost, performance, and regulatory compliance. Their water-borne nature ensures low VOC emissions, making them suitable for projects that prioritize environmental standards and occupant health. Acrylic coatings also offer excellent UV resistance, color retention, and flexibility, making them ideal for exterior walls and roofing applications in residential and commercial buildings. Their ability to adhere well to diverse substrates, such as concrete, masonry, stucco, and asphalt, reduces the need for multiple coating systems and simplifies contractor operations.

Continuous innovation, including enhanced crack-bridging, dirt pickup resistance, and improved weatherability, further strengthens acrylic dominance. While silicone, polyurethane, and polyurea coatings continue to grow in specialized niches, acrylic elastomeric systems remain the preferred choice for high-volume architectural applications.

By Technology Insights

Water-borne technology dominates the elastomeric coating market, accounting for an estimated 60-65% of total consumption as environmental regulations and sustainability goals gain momentum. Strict VOC limits under U.S. EPA rules and evolving European ecolabel standards strongly favor low-emission, water-based formulations over solvent-borne alternatives. Advances in polymer chemistry, particularly in acrylic and styrene-acrylic binders, have significantly improved adhesion, flexibility, and weather resistance, narrowing the performance gap with solvent-based systems.

Water-borne elastomeric coatings also offer practical advantages, including reduced odor, easier cleanup, and safer on-site handling. As green procurement policies become more common in public and private projects, adoption of water-borne systems continues to rise. This trend is especially strong in urban regions and environmentally sensitive areas, where compliance, worker safety, and sustainability credentials play a critical role in product selection.

By Application Insights

The building and construction sector represents the largest application segment for elastomeric coatings, accounting for approximately 45% of global demand. Roofs and exterior walls in residential, commercial, and institutional buildings require flexible, durable membranes that can withstand water exposure, UV radiation, and thermal movement. Elastomeric coatings offer a cost-effective alternative to full roof replacement, enabling building owners to extend asset life with minimal disruption.

As cities focus on energy efficiency and climate resilience, elastomeric roof systems are increasingly combined with insulation upgrades and solar installations, reinforcing their role in refurbishment projects. The large installed base of buildings and the need for periodic maintenance ensure consistent recurring demand. Although industrial, automotive, and transportation applications are expanding, the construction segment’s scale, frequency of repairs, and regulatory support secure its continued leadership in overall elastomeric coating consumption.

Regional Insights

North America Elastomeric Coating Market Trends

In North America, elastomeric coating demand is supported by strict environmental regulations, aging infrastructure, and a strong culture of product innovation. Federal and state-level VOC regulations, along with green building programs such as LEED and Energy Star, encourage the use of low-VOC, high-reflectance coatings, particularly for commercial and institutional roofs. A large inventory of older buildings across the U.S. drives refurbishment activity, as property owners seek affordable solutions to extend roof life and improve energy efficiency without complete replacement.

Manufacturers continue to invest in advanced technologies, including reflective cool roof coatings, hybrid elastomeric systems, and formulations compatible with solar panels. In coastal and storm-prone regions, elastomeric coatings are increasingly specified for waterproofing and wind-driven rain resistance, supporting steady, long-term market growth.

Europe Elastomeric Coating Market Trends

Europe’s elastomeric coating market is shaped by strong regulatory alignment, ambitious climate goals, and a focus on building energy efficiency. EU VOC regulations, ecolabel standards, and energy-efficiency directives promote the adoption of water-borne elastomeric systems across residential and public infrastructure projects. Countries such as Germany, France, the U.K., and Spain emphasize façade insulation, waterproofing, and thermal performance, where elastomeric coatings complement ETICS and exterior renders.

In Southern Europe, high solar exposure and temperature variation increase demand for UV-resistant and crack-bridging coatings. Urban renewal programs and social housing investments further support market growth. European manufacturers are also advancing formulations aligned with circular-economy principles, including longer service life and reduced environmental impact, reinforcing the region’s role as a leader in sustainable coating technologies.

Asia Pacific Elastomeric Coating Market Trends

Asia Pacific is the fastest-growing region for elastomeric coatings, driven by rapid urbanization, infrastructure development, and industrial expansion across China, India, Japan, and Southeast Asia. Large-scale construction of residential towers, commercial buildings, and industrial facilities creates strong demand for waterproofing and protective solutions. In hot and humid climates, reflective elastomeric roof coatings help reduce indoor temperatures and energy consumption, supporting government energy-efficiency initiatives.

China’s renovation of older housing stock and Japan’s focus on high-performance, earthquake-resistant structures further boost the adoption of premium elastomeric systems. Tightening environmental regulations across major Asian economies are accelerating the shift toward water-borne technologies. Combined with competitive manufacturing costs and expanding production capacity, the region is becoming both a major consumption market and a global supply hub for elastomeric coatings.

Competitive Landscape

The elastomeric coating market is moderately fragmented, with competition among global chemical companies, major paint manufacturers, and specialized regional waterproofing players. Industry leaders such as BASF, Sherwin-Williams, Dow, Huntsman, and Covestro leverage strong R&D capabilities, integrated supply chains, and broad product portfolios to serve both high-volume architectural and specialized industrial segments. Competitive strategies focus on developing low-VOC water-borne formulations, reflective cool roof systems, and application-friendly products with faster curing and improved durability.

Companies are also expanding distribution networks through contractors, retailers, and specification-driven sales channels. Increasingly, suppliers differentiate through system warranties, technical training, digital specification tools, and after-sales support. These value-added services strengthen customer loyalty and enable manufacturers to compete beyond price in a market that prioritizes long-term performance and reliability.

Key Developments:

- In March 2023: Gaco™ (Holcim Building Envelope) launched GacoFlex A48, an acrylic elastomeric roofing coating enabling single-pass application up to 80 wet mils, significantly improving installation speed, seamless coverage, and long-term waterproofing durability for commercial roofing systems.

- In March 2023: BASF SE introduced Cool Roof Reflect 99, a high-performance elastomeric coating capable of reflecting up to 99% of solar radiation, helping reduce rooftop temperatures, lower cooling energy demand, and support compliance with global cool roof and energy-efficiency standards.

- In July 2024: BASF SE expanded its BRILLIANCE™ acrylics and additives portfolio, strengthening sustainable, low-VOC elastomeric reflective roof coatings with improved adhesion, enhanced UV resistance, and wider application temperature windows to extend seasonal construction and refurbishment activities.

Companies Covered in Elastomeric Coating Market

- BASF SE

- Sherwin-Williams Company

- DowDuPont Inc.

- Huntsman Corporation

- Covestro AG

- Versaflex Inc.

- Rhino Linings Corporation

- Nukote Coating Systems

- Marvel Industrial Coatings LLC

- Pidilite Industries Ltd.

- PPG Industries

- Akzo Nobel N.V.

- Holcim

- Asian Paints Limited

- Nippon Paint Holdings Co., Ltd.

Frequently Asked Questions

The global elastomeric coating market is projected to reach around US$ 47.1 Billion by 2033, up from US$ 27.3 Billion in 2026, reflecting a forecast CAGR of about 8.1% between 2026 and 2033.

Demand is primarily driven by sustainable construction trends, stricter VOC and energy-efficiency regulations, and increased infrastructure rehabilitation needs, where elastomeric coatings offer long-lasting waterproofing, crack-bridging, and reflective performance for roofs, walls, and civil structures.

The building & construction segment, particularly roof and wall applications, is the leading application area, accounting for an estimated 45% share due to widespread use in waterproofing, façade protection, and cool roof systems.

Asia Pacific leads the global market, supported by large-scale residential and commercial construction, rapid urbanization, and major infrastructure investments across China, India, and ASEAN countries.

A major opportunity lies in developing advanced cool roof and reflective elastomeric systems that help cities mitigate heat islands, reduce building cooling loads, and comply with decarbonization policies and green building programs.

Key players include BASF SE, Sherwin-Williams Company, DowDuPont Inc., Huntsman Corporation, Covestro AG, Versaflex Inc., Rhino Linings Corporation, Nukote Coating Systems, Marvel Industrial Coatings LLC, Pidilite Industries Ltd., PPG Industries, Inc., and Akzo Nobel N.V., among others.