- Sensors & Controls

- E-house Market

E-house Market Size, Share, and Growth Forecast 2025 - 2032

E-house Market by Installation Type (Fixed E-House, Mobile Substation), by Application (Utilities, Oil & Gas, Mining, Data Centers, Renewable Energy, Others), by Regional Analysis, 2025 - 2032

E-house Market Size and Trend Analysis

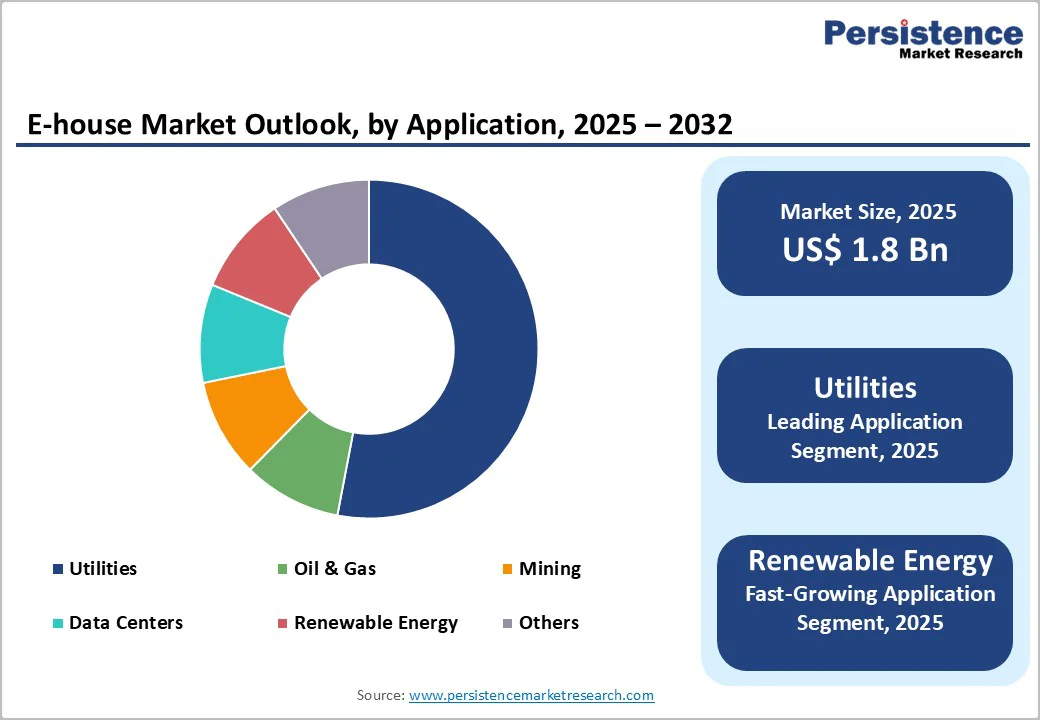

The global e-house market size is likely to be valued at US$1.8 billion in 2025 and projected to reach US$2.7 billion by 2032, growing at a CAGR of 6.2% between 2025 and 2032.

The rapid expansion of the e-house market is driven primarily by growing demand for modular, prefabricated power distribution solutions across the utilities, oil and gas, mining, and renewable energy sectors.

The increasing focus on grid modernization, integration of distributed energy resources, and the surge in data center developments worldwide are accelerating the adoption of E-house solutions as industries seek flexible and cost-effective alternatives to traditional brick-and-mortar substations.

Key Market Highlights:

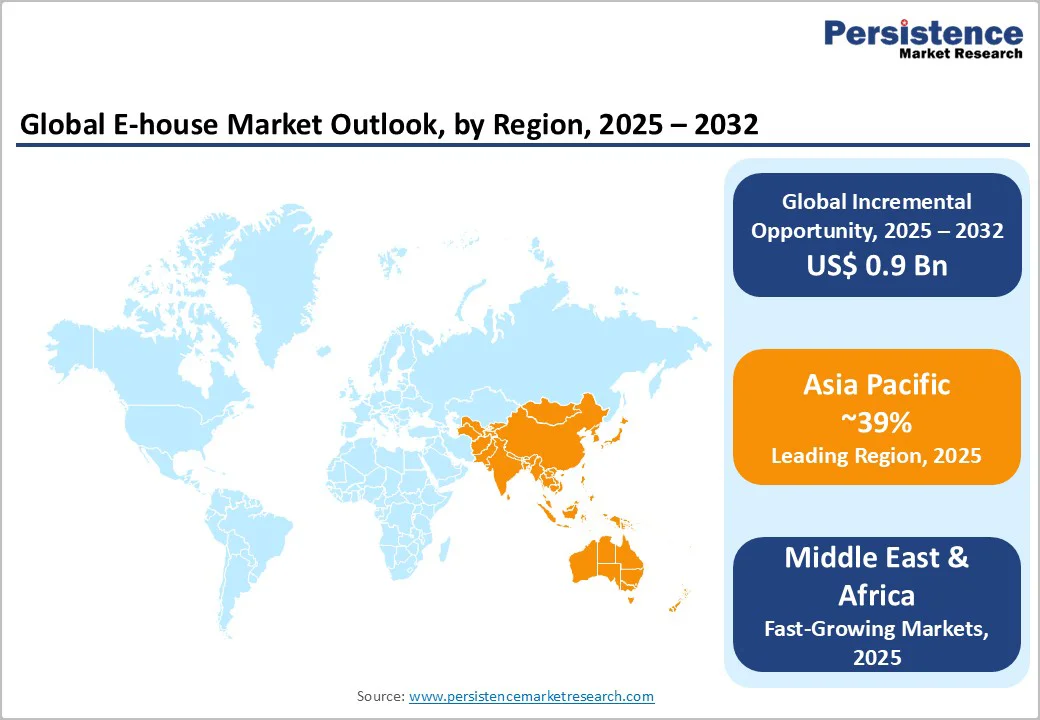

- Leading Region: Asia Pacific dominates the global E-house market with approximately 39% market share in 2025, driven by rapid industrialization, massive infrastructure investments, and aggressive renewable energy capacity additions across China, India, and Southeast Asian nations requiring flexible power distribution solutions.

- Fastest Growing Region: Middle East & Africa exhibits the highest regional growth trajectory with projected CAGR of 7% during 2025 - 2032, propelled by expanding oil and gas projects, mining sector development, and utility infrastructure investments addressing power shortage challenges across emerging economies.

- Dominant Segment: Utilities application segment commands approximately 53% market share in 2025, reflecting critical role of E-house substations in grid modernization initiatives, distributed energy resource integration, and provision of flexible power distribution capacity supporting transmission network expansion programs.

- Fastest Growing Segment: Renewable energy application segment demonstrates strongest growth momentum with projected CAGR of 8% during 2025 - 2032, driven by global acceleration of solar, wind, and hybrid power projects requiring flexible substations capable of managing variable generation patterns and energy storage integration.

- Key Market Opportunity: Expanding data center infrastructure expansion driven by artificial intelligence and cloud computing presents substantial E-house growth opportunity.

| Key Insights | Details |

|---|---|

| E-house Market Size (2025E) | US$ 1.8 Bn |

| Market Value Forecast (2032F) | US$ 2.7 Bn |

| Projected Growth CAGR (2025 - 2032) | 6.2% |

| Historical Market Growth (2019 - 2024) | 5.7% |

Market Dynamics

Market Growth Drivers

Accelerating Grid Modernization and Renewable Energy Integration

The worldwide transition toward modernized power grids and renewable energy integration is creating strong momentum for E-house deployment. In the United States, investor-owned utilities proposed approximately US$ 36.4 billion in grid modernization investments in 2023, reflecting a 71% increase over 2022.

The expansion of solar and wind capacity is accelerating across major economies, with renewable generation surpassing coal as the leading electricity source in the U.S. in 2024, accounting for nearly one-fourth of total output compared with only 9% in 2019.

This rapid shift toward intermittent and decentralized power generation requires compact, modular substations that can be installed quickly and withstand harsh environmental conditions. E-houses meet these requirements through factory-tested reliability, scalability, and fast commissioning, making them integral to renewable grid integration.

Explosive Growth in Data Center Infrastructure and AI Workloads

The explosive rise in data center infrastructure driven by artificial intelligence, cloud computing, and digital transformation is significantly boosting demand for E-houses. Global data centers consumed around 415 TWh of electricity in 2024, representing about 1.5% of total global demand, and consumption is projected to exceed 900 TWh by 2030.

The growing use of AI has increased power density requirements in server racks from conventional levels of 7-10 kW to as high as 100 kW per rack. This surge in power intensity demands robust, modular, and rapidly deployable electrical distribution systems.

E-house substations provide a flexible solution that reduces construction lead times by up to 50% while ensuring continuous power supply, driving widespread adoption among hyperscale data center developers worldwide.

Market Restraints

High Initial Capital Investment and Cost Barriers

The global E-House market continues to face adoption challenges due to the high initial capital investment required for procuring modular substations and electrical houses. While E-Houses deliver long-term savings and improved operational efficiency, their upfront costs can be 2% to 7% higher than traditional power distribution systems when only initial expenditures are considered.

This cost barrier is particularly restrictive for small and medium-sized enterprises and for infrastructure projects in developing economies, where financing costs are elevated. In many emerging markets, the weighted average cost of capital for energy infrastructure can be more than double that of developed regions.

Consequently, the capital-intensive nature of E-House projects limits their penetration in price-sensitive geographies and deters investors seeking faster returns on energy infrastructure projects.

Standardization Challenges and Interoperability Issues

Lack of standardization and interoperability across manufacturers remains a major restraint in the global E-House market. The absence of uniform design and communication standards makes it difficult to integrate modular substations with existing power infrastructure, smart grid systems, and automation platforms.

Manufacturers often use proprietary equipment configurations and protocols, leading to compatibility issues and increasing switching costs for end users. This fragmentation discourages potential buyers concerned about vendor lock-in and long-term flexibility.

Furthermore, the shortage of skilled professionals capable of handling high-voltage modular systems, along with the specialized installation and maintenance requirements of E-Houses, amplifies integration challenges. The combination of limited technical expertise and non-standardized system architectures continues to slow large-scale E-House adoption, especially in developing markets.

Market Opportunities

Expanding Renewable Energy Projects and Solar-Wind Hybrid Systems

The accelerating global shift toward renewable energy is creating major growth prospects for the E-house market as solar and wind power installations expand rapidly. According to IEA, global renewable capacity additions reached around 560 GW in 2024 and are expected to exceed 910 GW annually by 2029, driven by large-scale solar and wind deployments.

India’s solar capacity alone is projected to surge from 92 GW in 2024 to about 284 GW by 2033 at a CAGR of more than 13%. E-houses are increasingly preferred in hybrid renewable systems integrating solar photovoltaics, wind turbines, and battery storage, as they offer rapid deployment, compact design, and smart grid capabilities essential for managing fluctuating power sources efficiently.

Mining Industry Expansion and Remote Operations Electrification

The global mining industry’s expansion into remote, infrastructure-deficient regions is generating strong demand for E-house solutions that provide quick, reliable power distribution. Mining operations consume substantial electricity for extraction and processing, often in off-grid locations. Modular E-houses reduce installation time by up to 60% compared to traditional substations, enhancing efficiency and flexibility.

For example, Becker Mining Systems’ E-house deployment in an Arizona lithium mine improved energy efficiency by 15 percent and increased uptime by 40%. As the mining sector advances toward electrification and low-emission operations, and as mineral demand grows for batteries and renewable technologies, modular and relocatable E-houses are emerging as essential components for powering next-generation mining infrastructure.

Category-wise Analysis

Installation Type Insights

Fixed E-houses dominate the installation type segment in 2025, primarily due to their extensive deployment across utilities, manufacturing plants, and power generation facilities that require permanent or semi-permanent power infrastructure. Their popularity stems from superior safety, enhanced environmental protection, and the flexibility to be custom-engineered for specific operational requirements.

These units are ideal for stable, long-term operations such as industrial complexes and substations where reliability and protection from harsh conditions are paramount. In contrast, mobile E-houses are witnessing the fastest growth, supported by rising demand for modular, rapidly deployable power systems in mining, oil and gas, and emergency power restoration.

For instance, Iraq’s Ministry of Electricity’s adoption of mobile substations highlights the growing preference for flexible power solutions in developing regions.

Application Insights

The utilities sector remains the dominant application area in the global E-house market, driven by growing investments in grid modernization, transmission infrastructure upgrades, and distributed energy integration initiatives. Utilities are increasingly adopting prefabricated electrical houses to accelerate substation deployment, reduce downtime during maintenance or expansion, and improve overall operational efficiency.

According to the International Energy Agency (IEA), global grid investment surpassed US$ 330 billion in 2023, with the majority directed toward transmission and distribution network enhancement to support electrification and renewable integration. This sustained utility spending underpins strong demand for modular E-house solutions that ensure quick deployment and scalability.

Meanwhile, the renewable energy sector is the fastest-growing application, projected to record an 8% CAGR through 2032. The rising deployment of solar, wind, and hybrid systems requiring flexible, compact substations is accelerating E-house adoption, particularly for projects needing rapid commissioning and seamless integration of energy storage and smart grid technologies.

Regional Insights

North America E-house Market Trends

North America demonstrates strong E-house market dynamics driven by widespread infrastructure modernization initiatives, aging electrical grid replacement programs, and the region’s leadership in data center development.

The United States market is characterized by substantial utility investments in grid modernization, with approximately 75,000 substations requiring upgrades to accommodate distributed energy resources, bidirectional power flows, and integration of renewable generation capacity.

Average power transformer age in the U.S. now exceeds 40 years, well beyond the intended design life of 25-30 years, creating urgent replacement demand that E-house solutions can address more rapidly than traditional construction approaches.

The region’s regulatory framework strongly supports E-house adoption through initiatives including the Grid Modernization Initiative and Federal-State Modern Grid Deployment Initiative, which provide funding mechanisms and policy support for advanced electrical infrastructure technologies.

Major technology companies and hyperscale data center operators are increasingly specifying E-house substations to support their rapid facility expansions while meeting stringent uptime requirements and enabling future capacity additions through modular architecture.

Europe E-house Market Trends

Europe’s E-house market is shaped by the region’s ambitious renewable energy targets, stringent emissions reduction commitments, and comprehensive regulatory harmonization under the European Green Deal framework. The European Union aims to achieve 42.5% renewable energy share by 2030, requiring sustained wind deployment and rapid solar capacity additions that necessitate flexible substation infrastructure.

Germany led European wind capacity installations in 2024 with 4 GW of new capacity, followed by the United Kingdom at 1.9 GW and France at 1.7 GW, with all three countries deploying both onshore and offshore renewable projects that benefit from E-house solutions’ rapid deployment capabilities.

The Netherlands utility Enexis exemplifies European E-house adoption trends through its announced deployment of 11 E-house substations in the northern Netherlands, supported by approximately EUR 43 million investment to accelerate the energy transition and address limited grid capacity for large-scale clean energy projects.

Spain’s renewable energy expansion and the United Kingdom’s offshore wind development programs are generating substantial E-house demand as developers seek modular solutions that minimize environmental impact, reduce construction timelines, and provide the flexibility to scale capacity as renewable installations grow.

Asia Pacific E-house Market Trends

Asia Pacific emerges as the leading regional market, commanding approximately 39% market share in 2025, propelled by rapid industrialization, massive infrastructure development programs, and aggressive renewable energy capacity additions across China, India, and Southeast Asian nations.

China’s industrial sector expansion and India’s power infrastructure modernization initiatives are primary growth drivers, with India’s renewable energy capacity projected to increase from 135 GW in December 2023 to approximately 170 GW by March 2025.

India is pursuing an ambitious US$ 109.5 billion plan to expand power infrastructure and meet 458 GW demand by 2032, creating substantial opportunities for E-house deployment across transmission enhancement, renewable integration, and industrial electrification applications.

The region’s manufacturing advantages, including established supply chains, competitive production costs, and proximity to key component suppliers, strengthen Asia Pacific’s position as both a major E-house consumption market and manufacturing hub.

China maintains significant E-house production capacity serving domestic infrastructure projects and export markets, while countries including Japan, South Korea, and ASEAN nations are expanding E-house adoption to support their energy transition objectives.

Competitive Landscape

The global E-house market exhibits a moderately consolidated structure with established electrical equipment manufacturers maintaining dominant positions through comprehensive product portfolios, global service networks, and technological leadership in power distribution systems.

Leading market participants including ABB Ltd., Siemens AG, Schneider Electric SE, and Eaton leverage their extensive experience in electrical infrastructure, established relationships with utility and industrial customers, and capabilities to deliver turnkey solutions encompassing design, manufacturing, testing, installation, and lifecycle support services.

These major players differentiate themselves through investments in digitalization technologies, integration of IoT sensors and predictive maintenance capabilities, and development of sustainable solutions featuring SF?-free switchgear and energy-efficient designs.

Companies are pursuing growth through geographic expansion into emerging markets, strategic partnerships with EPC contractors and renewable energy developers, and continuous innovation in modular design architectures that reduce manufacturing costs while enhancing performance and reliability.

Key Market Developments

- June 2025: ABB secured a significant contract from Seatrium to supply advanced eHouse and automation systems for Petrobras’ P-84 and P-85 FPSO vessels in Brazil. The project includes design and construction of topside and hull electrical equipment, substation automation, and prefabricated eHouses integrating ABB Ability™ System 800xA® and IEC 61850 standards. Each FPSO will have a capacity of about 225,000 barrels per day, with eHouse delivery scheduled by 2027.

- March 2024: ABB introduced a modular plug-and-play eHouse system for mining operations, reducing on-site installation time by up to 30% through factory-tested, prefabricated components. The solution enhances deployment speed, safety, and reliability for remote mining projects, supporting ongoing electrification and operational efficiency efforts across the industry.

- January 2024: Schneider Electric launched a smart E-House integrated with its EcoStruxure platform, featuring AI-based monitoring, predictive maintenance, and real-time energy management. Designed for industrial and utility applications, the system improves energy efficiency, enhances equipment reliability, and supports digitalization and sustainability goals.

Companies Covered in E-house Market

- ABB Ltd.

- Eaton

- Becker Mining Systems AG

- Schneider Electric SE

- Siemens AG

- WEG

- Starflite Systems

- Sécheron

- Powergear Limited

- Powell Industries Inc.

- General Electric (GE)

- Meidensha Corporation

- TGOOD Global Ltd.

- Unit Electrical Engineering

- LS Electric Co., Ltd.

- CR Technology Systems S.P.A

- Delta Star, Inc.

- EKOS Eclectic

- Elgin Power Solutions

- Matelec

- PME Power Solutions

- Efacec

Frequently Asked Questions

The global E-house market is projected to reach US$ 2.7 Bn by 2032, growing from US$ 1.8 Bn in 2025 at a CAGR of 6.2% during the forecast period 2025 - 2032.

Key demand drivers include accelerating grid modernization initiatives, explosive data center infrastructure growth, and rapid renewable energy expansion requiring flexible substation solutions for solar and wind projects.

The utilities application segment maintains market leadership with approximately 53% market share in 2025, driven by widespread deployment of E-house substations for grid modernization, distributed energy resource integration, and flexible power distribution capacity supporting transmission network expansion across global utility infrastructure.

Asia Pacific dominates the global E-house market with approximately 39% market share in 2025, propelled by rapid industrialization, massive infrastructure investments particularly in China and India, and aggressive renewable energy capacity additions

Significant opportunities include serving the expanding renewable energy sector, supporting mining industry electrification, and addressing data center power demand.

Major market participants include ABB Ltd., Siemens AG, Schneider Electric SE, Eaton, Powell Industries Inc., Becker Mining Systems AG, TGOOD Global Ltd., WEG, Meidensha Corporation, General Electric (GE), and others.