- Medical Devices

- Dual Energy X-ray Absorptiometry Market

Dual Energy X-ray Absorptiometry Market Size, Share, and Growth Forecast, 2026 - 2033

Dual Energy X-ray Absorptiometry Market by Product Type (Axial DEXA, Peripheral DEXA), Application (Osteoporosis, Others), End-user (Hospitals and Clinics, Mobile Health Centers, Others), and Regional Analysis for 2026 - 2033

Dual Energy X-ray Absorptiometry Market Size and Trends Analysis

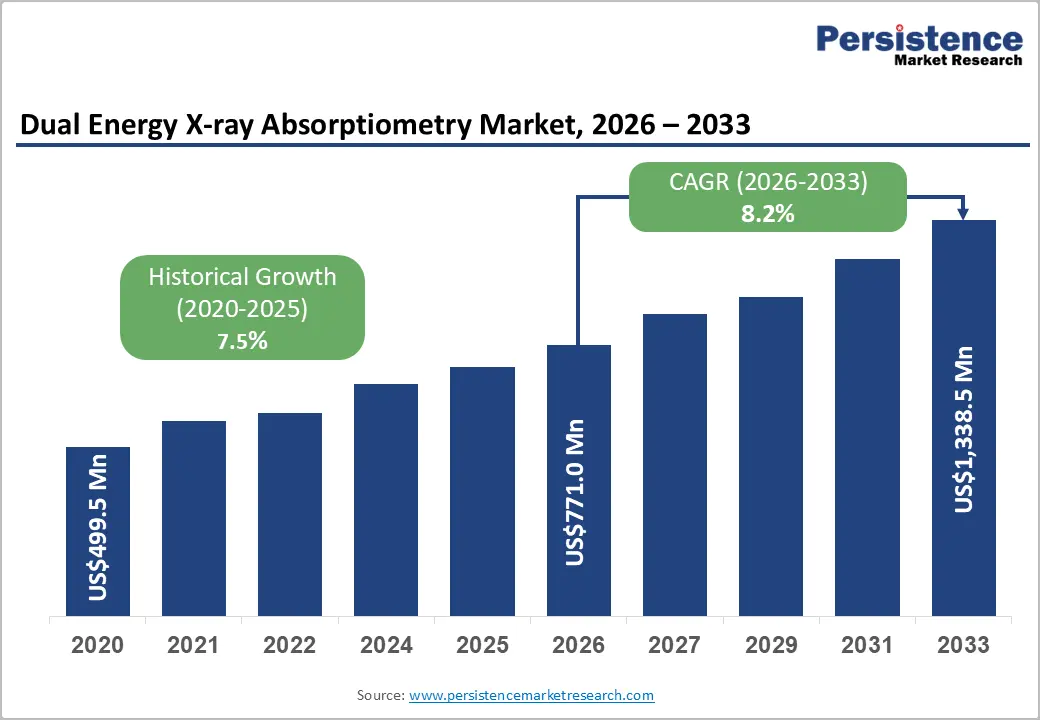

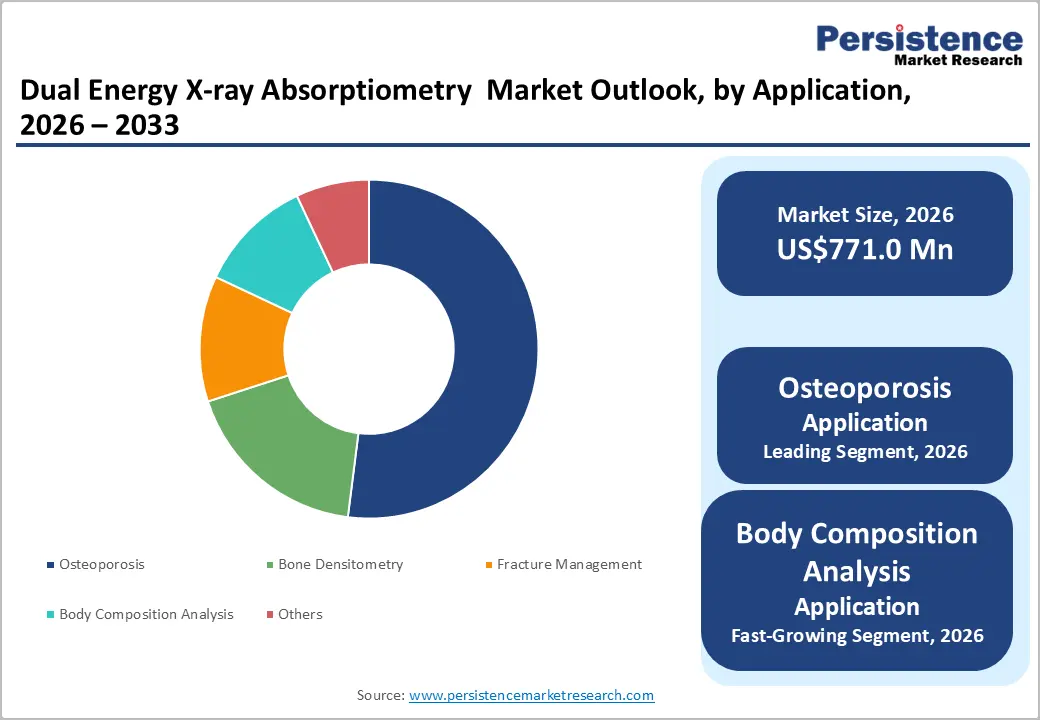

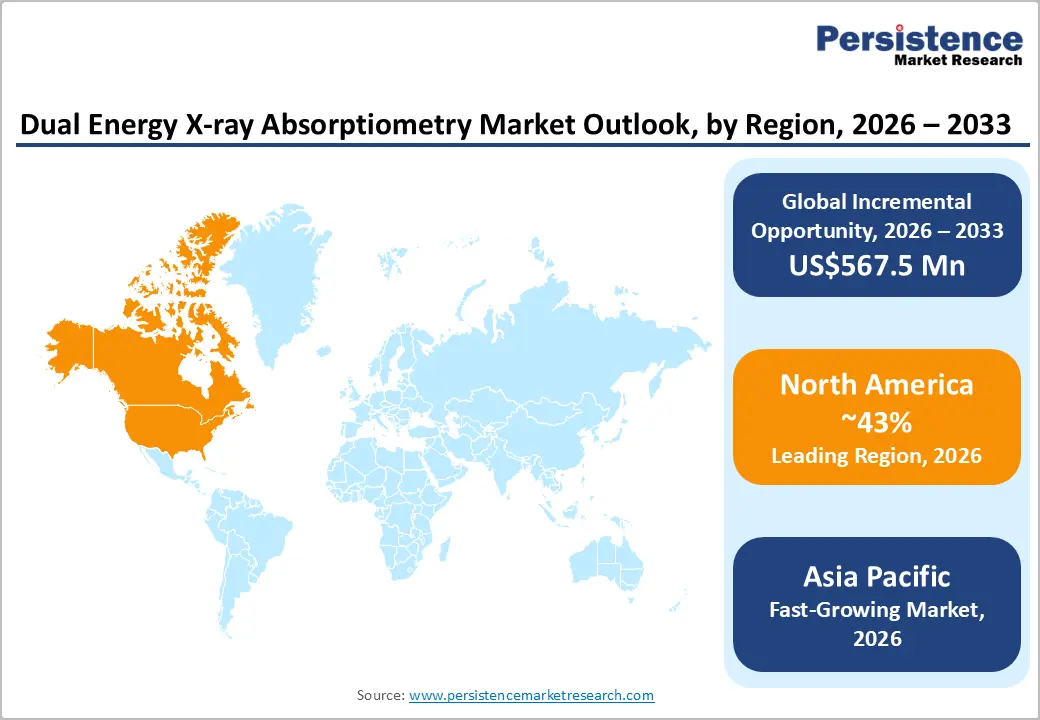

The global dual energy x-ray absorptiometry market size is projected to be valued at US$ 771.0 million in 2026 and is expected to reach US$ 1,338.5 million by 2033, growing at a CAGR of 8.2% during the forecast period from 2026 to 2033, driven by the increasing adoption of Dual Energy X-ray Absorptiometry (DEXA), widely recognized as the global gold standard for assessing bone mineral density (BMD), evaluating fracture risk, and analyzing body composition.

The technology utilizes two low-dose X-ray beams at different energy levels, commonly around 40 keV and 100 keV, to measure the varying absorption characteristics of bone and soft tissues. This enables accurate, non-invasive evaluation of bone mineral content, lean body mass, fat composition, and visceral fat distribution through a single scan with minimal radiation exposure.

Key Industry Highlights:

- Dominant Region: North America is expected to dominate the market, holding approximately 43% of total revenue in 2026, supported by comprehensive osteoporosis screening guidelines, advanced hospital radiology infrastructure, and the concentrated presence of leading DEXA system manufacturers, including GE Healthcare and Hologic.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing, driven by rapidly expanding healthcare infrastructure in China and India, rising osteoporosis awareness, and growing adoption of body composition analysis in sports medicine and metabolic health programs.

- Leading Product Type: Axial DEXA systems are expected to dominate, capturing approximately 72% of product revenue in 2026, reflecting their clinical primacy for spine and hip BMD measurement, the diagnostic gold standard for osteoporosis diagnosis, and their advanced body composition analysis capabilities.

- Dominant Application: Osteoporosis is anticipated to dominate the application segment, accounting for approximately 45% of market revenue in 2026, underpinned by the WHO's identification of osteoporosis as a major global public health challenge affecting approximately 200 million women worldwide.

DRO Analysis

Driver- Rising Global Osteoporosis Burden and Aging Population Driving DEXA Screening Demand

The escalating global burden of osteoporosis, driven by demographic aging across North America, Europe, and increasingly Asia Pacific, is the foundational structural demand driver for the market. According to the International Osteoporosis Foundation, osteoporosis affects around 200 million women worldwide and causes nearly 8.9 million fractures annually, with one fracture occurring every three seconds globally. In the U.S., the National Osteoporosis Foundation estimates that 10.2 million people have osteoporosis, while 43.4 million have low bone mass, creating a large population at high fracture risk and driving demand for DEXA screening.

The U.S. Preventive Services Task Force (USPSTF) recommends bone density screening using DEXA for all women aged 65 and older, and for younger postmenopausal women with elevated fracture risk. This guideline establishes DEXA screening as a recommended preventive service across the largest segment of the U.S. Medicare population.

Restraint - Underdiagnosis of Osteoporosis and Low Screening Rates Despite Clinical Guidelines

A paradoxical structural market constraint is the widespread underutilization of DEXA screening relative to clinical guideline recommendations, driven by patient unawareness, referring physician screening gap, and healthcare system access barriers, which limit the DEXA market's realized volume potential relative to its theoretical addressable base. The IOF estimates that approximately 80% of individuals who suffer an osteoporotic fracture are not subsequently screened with DEXA or treated for osteoporosis within the following 12 months, a clinical care gap that prevents the guideline-appropriate fracture prevention cascade from generating secondary DEXA scan volume.

Primary care physician awareness gaps regarding DEXA screening eligibility criteria, time constraints in primary care consultation settings that deprioritize preventive screening referrals, and patient transportation barriers to hospital or outpatient imaging center DEXA facilities collectively suppress realized scan volumes.

Opportunity - AI-Enhanced DEXA Analysis and Integration with Digital Health Fracture Risk Platforms

Artificial intelligence and machine learning integration into DEXA scan analysis workflows represents a high-growth frontier opportunity for the dual-energy X-ray absorptiometry market. AI-powered DEXA analysis platforms are being developed to automate bone mineral density measurement, enhance vertebral fracture assessment (VFA) accuracy, predict 10-year fracture probability incorporating DEXA BMD data with clinical risk factor algorithms beyond FRAX, and identify opportunistic findings in whole-body DEXA scans that are currently systematically underreported in routine clinical interpretation.

Integration of DEXA systems with digital health platforms, including electronic patient engagement tools, telemedicine fracture risk consultation services, and population health management programs operated by health systems and accountable care organizations (ACOs), is creating new data-driven care pathway models that enhance DEXA's clinical utility and scan referral volumes.

Category-wise Analysis

Product Type Insights

Axial DEXA systems are projected to dominate the market with nearly 72% revenue share in 2026, driven by their role as the clinical gold standard for osteoporosis diagnosis and fracture risk assessment at key skeletal sites such as the spine and hip. Advanced platforms such as GE Healthcare Lunar iDXA and Hologic Horizon A offer high-resolution imaging, body composition analysis, and trabecular bone score capabilities, strengthening their widespread clinical adoption.

Peripheral DEXA (pDXA) systems represent the fastest-growing product type. This growth reflects the expanding deployment of pDXA in community screening, primary care, pharmacy, mobile health, and point-of-care settings, driven by the clinical imperative to expand osteoporosis screening access beyond hospital-based Axial DEXA availability. BeamMed's Sunlight Omnisense ultrasound-combined pDXA system and Osteometer Meditech's DTX-200 DexaCare forearm densitometer exemplify the compact, cost-efficient peripheral bone density measurement platforms driving the pDXA segment's rapid growth in community and primary care settings across both established and emerging markets.

Application Insights

The osteoporosis segment is estimated to dominate, accounting for approximately 45% of market revenue in 2026. Its market leadership reflects the clinical centrality of DEXA-measured bone mineral density T-scores in osteoporosis diagnosis. The WHO diagnostic criterion for osteoporosis is intrinsically defined by DEXA measurement and the enormous scale of the at-risk patient population.

Body composition analysis represents the fastest-growing application segment. The convergence of GLP-1 receptor agonist weight loss pharmacotherapy, growing sports science investment in lean mass optimization, and expanding clinical recognition of sarcopenia as an independent mortality risk factor across aging, oncology, and critical care patient populations is generating rapidly expanding DEXA body composition scan demand across hospital, sports medicine, and research settings. GE Healthcare's CoreScan visceral fat quantification software and Hologic's Horizon whole-body composition analysis platform with android/gynoid fat ratio reporting exemplify the advanced body composition analytics capabilities that are driving DEXA adoption in metabolic health and sports performance clinical contexts.

End-user Insights

Hospitals and clinics are anticipated to dominate the end-user segment, capturing approximately 48% of global DEXA market revenue in 2026. The segment's dominant position reflects the concentration of Axial DEXA system installations in hospital radiology departments, rheumatology clinics, endocrinology practices, and orthopedics centers, the clinical settings where the highest-complexity osteoporosis and metabolic bone disease patient populations are managed.

Mobile health centers represent the fastest-growing end-user segment. Government and health system investments in mobile health infrastructure targeting rural osteoporosis screening access gaps, elderly patient mobility limitations, and community health screening event programs are driving systematic expansion of mobile DEXA deployment beyond urban hospital-centered scanning environments.

Regional Insights

North America Dual Energy X-ray Absorptiometry Market Trends

North America market is projected to dominate, holding approximately 43% of the total share in 2026. The U.S. market growth is driven by the world's most structured osteoporosis screening guideline infrastructure, including USPSTF Grade B recommendations, CMS Medicare reimbursement coverage, and major specialty society clinical practice guidelines from the NOF, ISCD, and ACR that collectively define a large, reimbursement-supported institutional DEXA scanning demand base.

U.S. Dual Energy X-ray Absorptiometry Market Insights

The U.S. DEXA market is fueled by the Medicare-eligible population's DEXA scan entitlement, which CMS covers bone density testing every 24 months for qualifying beneficiaries, which generates over 5 million DEXA bone density scans annually in the U.S. healthcare system. The U.S. market is the primary battleground for GE Healthcare (Lunar brand) and Hologic, the two dominant global Axial DEXA manufacturers.

Canada Dual Energy X-ray Absorptiometry Market Insights

Canada's DEXA market is shaped by Osteoporosis Canada's national clinical practice guidelines, which recommend BMD testing using DEXA for women aged 65 and older and men aged 70 and older, as well as for younger individuals with risk factors including prior fragility fracture, glucocorticoid use, and rheumatoid arthritis.

Europe Dual Energy X-ray Absorptiometry Market Trends

Europe shows steady growth, driven by national osteoporosis prevention programs, FRAX-integrated BMD screening frameworks, and the European Society for Clinical and Economic Aspects of Osteoporosis (ESCEO) clinical guidelines that support DEXA as the primary bone density measurement tool across European healthcare systems.

Germany Dual Energy X-ray Absorptiometry Market Trends

Germany is the leading European DEXA market, driven by comprehensive statutory health insurance (GKV) coverage for DEXA bone density testing in high-risk patient categories, a dense network of rheumatology and osteology specialist practices deploying Axial DEXA systems, and the Dachverband Osteologie (DVO) clinical guidelines that define evidence-based osteoporosis fracture risk assessment protocols.

U.K. Dual Energy X-ray Absorptiometry Market Trends

The U.K. DEXA market is shaped by NICE (National Institute for Health and Care Excellence) clinical guidelines for osteoporosis, which recommend DEXA bone density measurement as the primary diagnostic tool for osteoporosis confirmation and fracture risk assessment, and NHS commissioning frameworks that fund DEXA scanning through hospital trusts and community diagnostic centers.

Asia Pacific Dual Energy X-ray Absorptiometry Market Trends

Asia Pacific is likely to be the fastest-growing, propelled by rapidly expanding healthcare infrastructure, growing osteoporosis awareness and clinical guideline adoption, rising body composition analysis demand in sports medicine and metabolic health, and large at-risk aging populations across China, Japan, and Southeast Asia.

China Dual Energy X-ray Absorptiometry Market Trends

China is the dominant Asia Pacific DEXA market. The China Osteoporosis Foundation's national BMD screening initiative is expanding physician awareness of DEXA-based fracture risk assessment. Domestic DEXA manufacturers, including Shenzhen XRAY Electric Co., Ltd., are developing cost-optimized systems targeting the large volume hospital procurement market.

India Dual Energy X-ray Absorptiometry Market Trends

India is one of the fastest-growing DEXA markets in Asia Pacific, driven by the country's large and clinically underdiagnosed osteoporosis burden. The Indian Osteoporosis Society estimates that over 50 million Indians are affected by osteoporosis, and a rapidly expanding private hospital and diagnostic imaging center infrastructure.

Competitive Landscape

The global dual energy X-ray absorptiometry market is moderately consolidated at the premium Axial DEXA segment level, with GE Healthcare and Hologic, Inc. collectively commanding an estimated 70%-80% of the global Axial DEXA installed base, making the DEXA equipment market one of the more concentrated segments within the broader medical imaging industry. GE Healthcare's Lunar DEXA product line, spanning the iDXA (premium full-body system), the Prodigy Advance, and the Lunar DPX, serves hospital, clinic, and research settings across 100+ countries, supported by a comprehensive global service and software update infrastructure.

The peripheral DEXA and mid-market DEXA segment features a more diverse competitive landscape, including Medilink International, Osteometer Meditech Inc., BeamMed Ltd., Scanflex Healthcare AB, Medonica Co. Ltd., Furuno Electric Co. Ltd., Kingaroy, and Fona Corporation companies that compete through cost-optimized system pricing, compact form factor designs suitable for clinic and mobile health deployment, and regional distribution network strength in emerging markets where premium Axial DEXA pricing creates adoption barriers.

Key Industry Developments:

- In February 2026, BPL Medical Technologies acquired Yozma BMTech Co., Ltd. to strengthen its presence in diagnostic imaging and expand into the bone densitometry segment. Through the acquisition, BPL added DEXA (Dual-Energy X-ray Absorptiometry) systems to its portfolio, enhancing its capabilities in osteoporosis screening, bone mineral density assessment, and overall bone health diagnostics.

- In May 2025, SimonMed Imaging launched an advanced DEXA bone density scan that combined traditional bone mineral density testing with Trabecular Bone Score (TBS) analysis to improve early osteoporosis detection and fracture risk assessment. Developed in partnership with Medimaps Group, the enhanced screening integrated FDA-cleared software into standard DEXA scans, enabling clinicians to evaluate both bone density and bone microarchitecture.

Companies Covered in Dual Energy X-ray Absorptiometry Market

- GE Healthcare

- Hologic, Inc.

- Medilink International

- Osteometer Meditech Inc.

- Medonica Co., Ltd.

- Furuno Electric Co., Ltd.

- BeamMed Ltd.

- Scanflex Healthcare AB

Frequently Asked Questions

The global dual energy X-ray absorptiometry market is projected to reach US$771.0 million in 2026.

The rising global prevalence of osteoporosis and age-related bone disorders is driving demand for early and accurate bone density screening. Increasing awareness of preventive healthcare and fracture risk assessment is further accelerating the adoption of advanced DEXA systems.

The dual energy X-ray absorptiometry market is poised to witness a CAGR of 8.2% from 2026 to 2033.

Growing adoption of AI-enabled and portable DEXA systems in emerging healthcare markets is creating significant growth opportunities for manufacturers.

Key players include GE Healthcare, Hologic Inc., Medilink International, Osteometer Meditech Inc., Medonica Co. Ltd., Furuno Electric Co. Ltd., BeamMed Ltd., and Scanflex Healthcare AB.