- Industrial Machinery

- Dredging Market

Dredging Market Size, Share, Trends, and Growth Forecast 2025 - 2032

Dredging Market Analysis By Application (Seaborn Trade & Navigational Channels), Customer Type (Government, O&G Companies, Mining Companies, Others), and Regional Analysis 2025 - 2032

Dredging Market Share and Trends Analysis

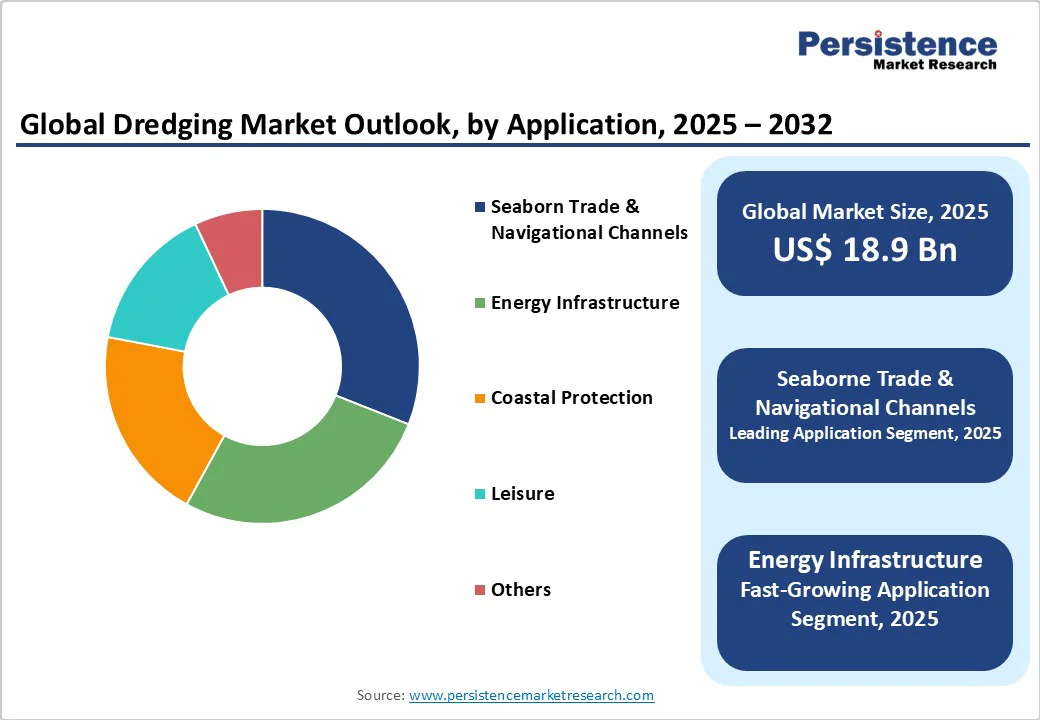

The global dredging market size is likely to be valued at US$18.9 billion in 2025 and is projected to reach US$22.2 billion by 2032, growing at a CAGR of 2.3% between 2025 and 2032.

Market expansion is primarily driven by increasing maritime trade volumes, port modernization initiatives, and rising coastal protection requirements due to climate change impacts.

Growing demand for deeper navigation channels to accommodate larger vessels and government investments in infrastructure development further support the market's steady growth trajectory.

Key Industry Highlights:

- Leading Application: Seaborne trade and navigational channels dominate with a ~31% share, driven by recurring maintenance dredging, deeper navigation channels, and port expansion projects to accommodate larger container vessels globally.

- Leading Customer Segment: Government accounts for a 46% market share, driven by coastal protection, harbor modernization, and strategic infrastructure projects, which offer high-value, long-duration contracts with stable financial returns.

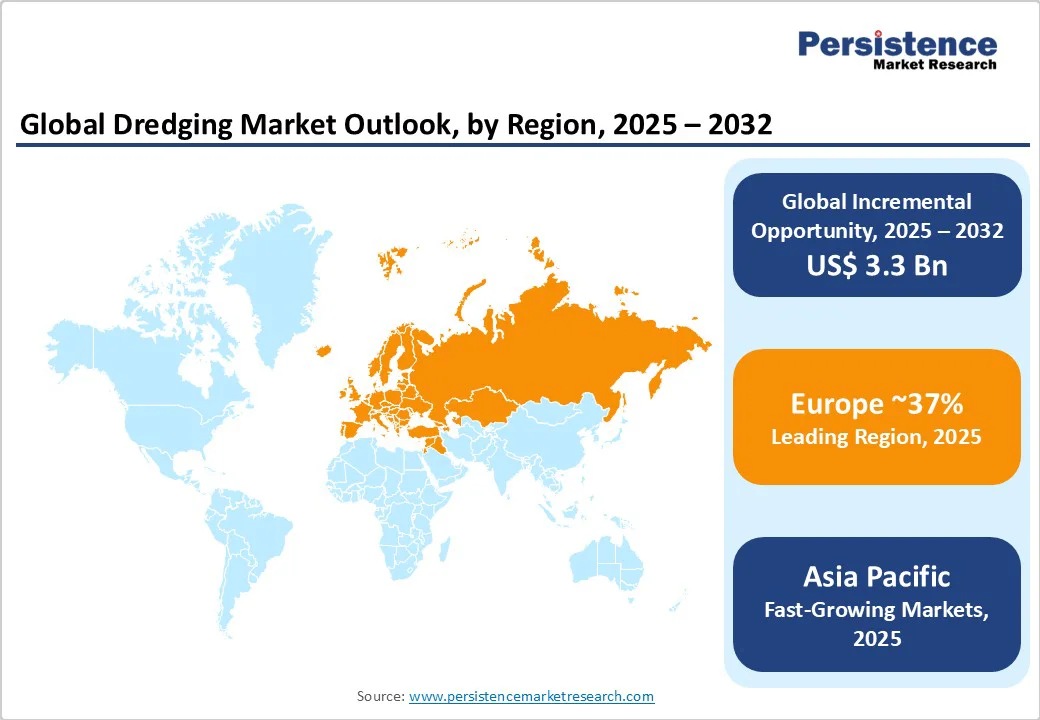

- Leading Region: Europe holds the largest share, supported by advanced dredging technology, environmental compliance expertise, offshore renewable energy initiatives, and substantial investments in port modernization and coastal protection programs.

- Fastest-Growing Region: The Asia Pacific region grows at a 4.4% CAGR, fueled by projects in India, China, and ASEAN, as well as government initiatives, port development, and increasing regional trade volumes.

- Key Growth Opportunity: Renewable Energy & Offshore Wind Projects provide high-value contracts for seabed preparation, cable installation, and sustainable marine infrastructure, enabling revenue diversification and adoption of advanced technologies.

| Key Insights | Details |

|---|---|

| Dredging Market Size (2025E) | US$18.9 Bn |

| Market Value Forecast (2032F) | US$22.2 Bn |

| Projected Growth CAGR(2025-2032) | 2.3% |

| Historical Market Growth (2019-2024) | 1.6% |

Market Dynamics

Drivers - Expanding Global Maritime Trade and Port Infrastructure Development

The dredging market is experiencing significant momentum due to the steady growth of global maritime trade and the increasing demand for advanced port infrastructure. According to the United Nations Conference on Trade and Development (UNCTAD), seaborne trade volumes were projected to grow by 2.4% in 2023, underscoring the continuous rise in demand for efficient port facilities.

As container vessels increase in size and capacity, ports worldwide require deeper navigation channels, larger berths, and expanded docking facilities. This growing requirement directly fuels the demand for dredging services, enhancing port competitiveness and accommodating larger cargo traffic.

Government support and investment in maritime infrastructure further strengthen this driver. The U.S. Army Corps of Engineers awarded nearly $2.1 billion in federal dredging contracts in FY23, reflecting a 39% rise from the previous year. This surge underscores the crucial role of dredging in maintaining efficient maritime operations and ensuring the seamless flow of international trade.

Climate Change Adaptation and Coastal Protection Requirements

Climate change has become a major factor shaping the dredging industry, particularly through its impact on coastal resilience. Rising sea levels, frequent flooding, and intensified storms have increased the urgency for dredging projects focused on shoreline protection, flood management, and habitat restoration.

These projects not only protect vulnerable coastal populations but also ensure the long-term viability of critical infrastructure in high-risk zones. By addressing these challenges, dredging plays a pivotal role in safeguarding both economies and ecosystems against climate-related disruptions.

Sustainability goals are also reinforcing this trend. The U.S. Army Corps of Engineers has set a target to beneficially use 70% of dredged sediment by 2030, underscoring the importance of environmentally responsible practices.

Significant government budgets are being allocated to shoreline stabilization and coastal defense programs, ensuring recurring opportunities for dredging contractors. This alignment of climate adaptation and sustainable development further strengthens the long-term growth trajectory of the dredging market.

Restraint - Stringent Environmental Regulations and Compliance Costs

Increasingly strict environmental regulations impose significant operational constraints on dredging activities, complicating project approval processes and substantially increasing compliance costs. Marine ecosystem protection requirements necessitate comprehensive ecological impact assessments, the deployment of specialized equipment, and extensive monitoring protocols, which extend project timelines and increase budgets. These regulatory frameworks, while essential for ecological preservation, create barriers to market entry for smaller operators and reduce profit margins across the industry.

High Capital Investment Requirements and Equipment Costs

The dredging industry demands substantial capital investments for specialized vessels, advanced positioning systems, and automated control technologies. Equipment acquisition costs, combined with ongoing maintenance and fuel expenses, create significant financial barriers that limit market participation and constrain expansion opportunities for existing companies.

Fluctuating fuel prices further impact operational profitability, as dredging operations are inherently fuel-intensive activities requiring continuous power generation for excavation and material transport functions.

Opportunity - Renewable Energy Infrastructure Development and Offshore Wind Projects

The global shift toward renewable energy presents significant opportunities for dredging contractors, particularly in offshore wind farm construction and related marine infrastructure development. The growing demand for seabed preparation, cable laying, and port expansion for renewable energy projects is driving the need for specialized dredging services. Companies leveraging advanced technologies, such as autonomous underwater vehicles, are enhancing survey accuracy and operational efficiency, enabling cost-effective project execution.

This sector also offers higher-value, long-term contracts, providing stable revenue streams for forward-looking dredging operators. For example, DEME Group’s renewable energy segment grew 15% in 2022, reflecting the rising importance of dredging in supporting sustainable energy infrastructure. The expansion of offshore wind installations and other marine renewable energy projects is expected to continue creating strategic growth opportunities for industry players worldwide.

Beneficial Use of Dredged Material and Circular Economy Integration

Sustainable practices and circular economy initiatives are creating new opportunities in the dredging market through the beneficial reuse of dredged materials. Increasingly, dredged sediments are being repurposed for beach nourishment, habitat restoration, and even innovative 3D printing applications in infrastructure projects, thereby adding both environmental and economic value.

The government's adoption of such practices is increasing, with 66% of federal dredging projects in FY23 incorporating beneficial use strategies. The expansion of offshore support vessels and marine navigation technologies further facilitates efficient transport, placement, and monitoring of reused materials. By integrating circular economy principles, dredging contractors can diversify revenue streams, enhance sustainability credentials, and position themselves as key enablers of eco-friendly coastal and marine development initiatives.

Category-wise Insights

Application Analysis

Seaborne trade and navigational channels dominate the dredging market, accounting for approximately 31% of the total share, due to recurring maintenance needs and the increasing size of vessels. Sediment accumulation in shipping channels necessitates consistent dredging, resulting in predictable schedules and stable revenue streams for contractors.

Major port authorities continue to invest heavily in channel deepening projects to accommodate Post-Panamax and Ultra Large Container Vessels, with initiatives like the Panama Canal expansion highlighting the strategic importance of dredging. Government funding for harbor development and international shipping route optimization further reinforces the segment’s leadership, ensuring steady demand and long-term market growth.

Customer Type Analysis

Government clients represent the most lucrative segment, capturing an estimated 46% market share valued at around $7.7 billion in 2025. Large-scale infrastructure projects, coastal protection initiatives, and strategic port expansion programs drive consistent demand for dredging services.

High-value government contracts often feature long durations and secure payment terms, providing financial stability and reduced pricing pressures compared to private sector projects. For instance, the Dredging Corporation of India reported 147% revenue growth in FY2024, reaching 945.50 crore, illustrating strong government investment in maritime infrastructure across developing economies.

Regional Insights

North America Dredging Market Trends

The United States dredging market is expected to maintain steady growth at a 2.0% CAGR, primarily driven by federal government funding for harbor maintenance and coastal resilience projects. The US Army Corps of Engineers continues prioritizing navigation channel maintenance and flood protection initiatives, with substantial investments in Mississippi River dredging operations and hurricane recovery projects.

Great Lakes Dredge & Dock Company and other domestic contractors benefit from consistent federal contract awards, while technological upgrades, including GPS-based dredging solutions, enhance operational efficiency and environmental compliance.

North American market dynamics reflect mature infrastructure requirements, combined with increasing needs for climate adaptation. Environmental constraints and regulatory approval processes add complexity to projects, yet sustained government funding ensures market stability.

The region's extensive coastline and inland waterway systems generate a continuous demand for maintenance dredging, supporting established industry relationships and long-term contract frameworks.

Europe Dredging Market Trends

European markets demonstrate strong performance, driven by the success of major contractors, with Royal Boskalis Westminster achieving a record €4.4 billion in revenue in 2024, representing EUR 1.3 billion in EBITDA and EUR 781 million in net profit.

The Netherlands, Germany, and the United Kingdom lead regional demand through investments in port modernization and coastal protection, while European Union regulatory harmonization initiatives standardize dredging practices across member states. DEME Group reported €2.3 billion in revenue in 2022, with significant growth in renewable energy projects supporting offshore wind development across the North Sea region.

Regional trends emphasize sustainability and technological innovation, with European contractors leading the way in environmental dredging solutions and beneficial material use applications. Climate change adaptation drives substantial funding for coastal protection projects, while Brexit-related port infrastructure adjustments create additional demand in UK markets. Advanced automation and digitalization adoption positions European companies as technology leaders in global dredging markets.

Asia Pacific Dredging Market Trends

India's dredging sector exhibits exceptional growth potential, with a 4.4% CAGR, driven by government initiatives, including the Sagarmala and Bharatmala programs, which prioritize port modernization and inland waterway development.

China remains the dominant regional market, driven by massive infrastructure projects and investments in the Belt and Road Initiative, while Japan focuses on improving disaster resilience and port efficiency. ASEAN countries are demonstrating an increasing demand for coastal protection and trade infrastructure development, supported by financing from multilateral development banks and private sector partnerships.

Regional manufacturing advantages and government policy support create favorable conditions for expanding domestic dredging capacity. India promotes indigenous vessel production and technology transfer initiatives, while China leads global dredging vessel manufacturing and export activities.

Prime Minister Modi launched Rs 34,200 billion worth of maritime and port projects in Gujarat, demonstrating an unprecedented government commitment to maritime infrastructure development. Rising cargo handling volumes and maritime trade growth across the region sustain long-term demand for dredging services and related marine infrastructure projects.

Competitive Landscape

The global dredging market is moderately consolidated, with a few dominant multinational contractors controlling a significant share, while numerous regional operators serve localized markets. Competition centers on technological innovation, project execution efficiency, and geographic diversification, enabling leading players to differentiate through specialized vessel fleets, advanced automation, and strong environmental compliance capabilities.

Emerging trends in the industry include integrated project delivery, sustainable material management, and a focus on renewable energy infrastructure projects. Additionally, the adoption of digitalization and autonomous dredging systems is enhancing operational efficiency, safety performance, and cost-effectiveness, further intensifying competition and driving continuous innovation across the market.

Key Market Developments

- In March 2025, Royal Boskalis Westminster achieved record financial performance, reporting EUR 4.4 billion in revenue, EUR 1.3 billion in EBITDA, and EUR 781 million in net profit, surpassing all previous performance benchmarks.

- In February 2025, the NMDC Group recorded exceptional results, achieving AED 26.3 billion in revenue, a 57% year-over-year increase, and AED 3.1 billion in net profit, driven by operational efficiency and strategic market expansion initiatives.

- In May 2024, Dredging Corporation of India reported a remarkable 147% revenue growth, reaching ? 945.50 crore in FY2024, reflecting a strong performance in Indian maritime infrastructure and port development projects.

Companies Covered in Dredging Market

- Adani Ports and Special Economic Zone Limited

- Dredging Corporation of India, DEME Group

- Royal Boskalis Westminster N.V.

- Van Oord

- Jan De Nul Group

- HYUNDAI E&C

- CASHMAN DREDGING INC.

- Great Lakes Dredge & Dock Company LLC

- TOA Corporation

- Penta-Ocean Construction Co. Ltd.

- National Marine Company

- CALLAN MARINE LTD.

- China Harbour Engineering Company Limited

- Dredge America

- NMDC Group

- China Communications Construction Company

Frequently Asked Questions

The global dredging market was valued at US$ 18.9 billion in 2025 and is projected to reach US$ 22.2 billion by 2032, growing at a CAGR of 2.3% during the forecast period.

Key growth drivers include expanding maritime trade volumes, increasing demand for deeper navigation channels to accommodate larger vessels, and rising coastal protection requirements due to climate change impacts.

Seaborn Trade & Navigational Channels represents the leading application segment with approximately 31% market share, driven by continuous maintenance requirements and port infrastructure expansion needs.

Europe dominates the market through established contractors like Royal Boskalis Westminster and DEME Group, supported by advanced technology, comprehensive regulatory frameworks, and significant renewable energy investments.

Beneficial use of dredged materials emerges as the primary opportunity, with the US Army Corps of Engineers targeting 70% material utilization by 2030 for habitat restoration and sustainable infrastructure applications.

Key market players include Royal Boskalis Westminster N.V., DEME Group, Van Oord, Jan De Nul Group, Dredging Corporation of India, and Great Lakes Dredge & Dock Company, among others.