- Executive Summary

- Global Domestic Booster Pump Market Snapshot 2025 and 2032

- Market Opportunity Assessment, 2025-2032, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply-Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Residential Industry Overview

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2019 – 2032

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Domestic Booster Pump Market Outlook:

- Key Highlights

- Global Domestic Booster Pump Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Product Type, 2019-2024

- Current Market Size (US$ Bn) Analysis and Forecast, by Product Type, 2025-2032

- Single Stage

- Multi Stage

- Market Attractiveness Analysis: Product Type

- Global Domestic Booster Pump Market Outlook: Pressure Range

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Pressure Range, 2019-2024

- Current Market Size (US$ Bn) Analysis and Forecast, by Pressure Range, 2025-2032

- Low (up to 2 Bar)

- Medium (2-5 Bar)

- High (above 5 Bar)

- Market Attractiveness Analysis: Pressure Range

- Global Domestic Booster Pump Market Outlook: End-use

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by End-use, 2019-2024

- Current Market Size (US$ Bn) Analysis and Forecast, by End-use, 2025-2032

- Residential Buildings

- Commercial

- Industrial

- Other

- Market Attractiveness Analysis: End-use

- Global Domestic Booster Pump Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis by Region, 2019-2024

- Current Market Size (US$ Bn) Analysis and Forecast, by Region, 2025-2032

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Domestic Booster Pump Market Outlook:

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) Analysis and Forecast, by Country, 2025-2032

- U.S.

- Canada

- North America Market Size (US$ Bn) Analysis and Forecast, by Product Type, 2025-2032

- Single Stage

- Multi Stage

- North America Market Size (US$ Bn) Analysis and Forecast, by Pressure Range, 2025-2032

- Low (up to 2 Bar)

- Medium (2-5 Bar)

- High (above 5 Bar)

- North America Market Size (US$ Bn) Analysis and Forecast, by End-use, 2025-2032

- Residential Buildings

- Commercial

- Industrial

- Other

- Europe Domestic Booster Pump Market Outlook:

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) Analysis and Forecast, by Country, 2025-2032

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) Analysis and Forecast, by Product Type, 2025-2032

- Single Stage

- Multi Stage

- Europe Market Size (US$ Bn) Analysis and Forecast, by Pressure Range, 2025-2032

- Low (up to 2 Bar)

- Medium (2-5 Bar)

- High (above 5 Bar)

- Europe Market Size (US$ Bn) Analysis and Forecast, by End-use, 2025-2032

- Residential Buildings

- Commercial

- Industrial

- Other

- East Asia Domestic Booster Pump Market Outlook:

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) Analysis and Forecast, by Country, 2025-2032

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) Analysis and Forecast, by Product Type, 2025-2032

- Single Stage

- Multi Stage

- East Asia Market Size (US$ Bn) Analysis and Forecast, by Pressure Range, 2025-2032

- Low (up to 2 Bar)

- Medium (2-5 Bar)

- High (above 5 Bar)

- East Asia Market Size (US$ Bn) Analysis and Forecast, by End-use, 2025-2032

- Residential Buildings

- Commercial

- Industrial

- Other

- South Asia & Oceania Domestic Booster Pump Market Outlook:

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) Analysis and Forecast, by Country, 2025-2032

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) Analysis and Forecast, by Product Type, 2025-2032

- Single Stage

- Multi Stage

- South Asia & Oceania Market Size (US$ Bn) Analysis and Forecast, by Pressure Range, 2025-2032

- Low (up to 2 Bar)

- Medium (2-5 Bar)

- High (above 5 Bar)

- South Asia & Oceania Market Size (US$ Bn) Analysis and Forecast, by End-use, 2025-2032

- Residential Buildings

- Commercial

- Industrial

- Other

- Latin America Domestic Booster Pump Market Outlook:

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) Analysis and Forecast, by Country, 2025-2032

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) Analysis and Forecast, by Product Type, 2025-2032

- Single Stage

- Multi Stage

- Latin America Market Size (US$ Bn) Analysis and Forecast, by Pressure Range, 2025-2032

- Low (up to 2 Bar)

- Medium (2-5 Bar)

- High (above 5 Bar)

- Latin America Market Size (US$ Bn) Analysis and Forecast, by End-use, 2025-2032

- Residential Buildings

- Commercial

- Industrial

- Other

- Middle East & Africa Domestic Booster Pump Market Outlook:

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) Analysis and Forecast, by Country, 2025-2032

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) Analysis and Forecast, by Product Type, 2025-2032

- Single Stage

- Multi Stage

- Middle East & Africa Market Size (US$ Bn) Analysis and Forecast, by Pressure Range, 2025-2032

- Low (up to 2 Bar)

- Medium (2-5 Bar)

- High (above 5 Bar)

- Middle East & Africa Market Size (US$ Bn) Analysis and Forecast, by End-use, 2025-2032

- Residential Buildings

- Commercial

- Industrial

- Other

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Grundfos

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Pentair Plc.

- Xylem Inc.

- KSB AG

- Franklin Electric

- ESPA

- Zoeller Company

- Aqua Groups

- Donaldson

- Ebara

- Euro Molten Pumps

- Kirloskar Brothers

- Sulzer

- Grundfos

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Industrial Machinery

- Domestic Booster Pump Market

Domestic Booster Pump Market Size, Share, and Growth Forecast 2025 - 2032

Domestic Booster Pump Market By Product Type (Single Stage, Others), Pressure Range (Low (up to 2 Bar), Others), End-user (Residential Buildings, Others), and Regional Analysis for 2025 - 2032

Domestic Booster Pump Market Size and Trends Analysis

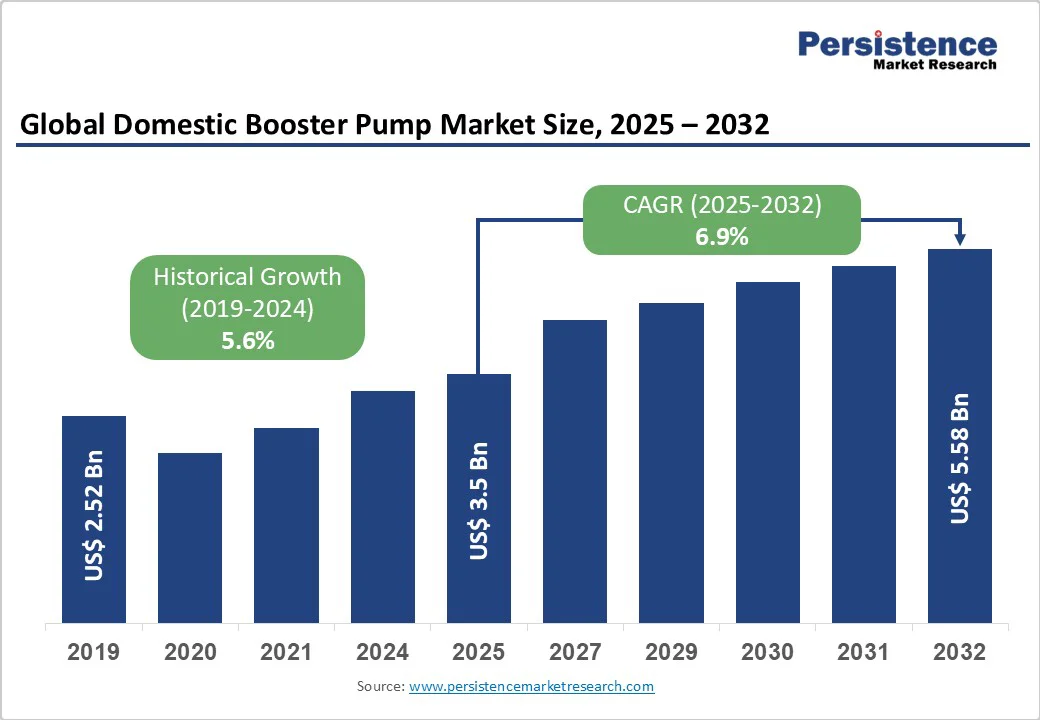

The global domestic booster pump market is expected to reach US$3.5 billion in 2025. It is expected to reach US$5.6 billion by 2032, growing at a CAGR of 6.9% during the forecast period from 2025 to 2032, driven by urbanization and increased residential construction, which are boosting demand for reliable water pressure in homes. Water scarcity challenges in urban areas, combined with a global population exceeding 8 billion according to United Nations estimates, are also fueling the need for booster pumps to ensure a consistent daily water supply.

Key Industry Highlights

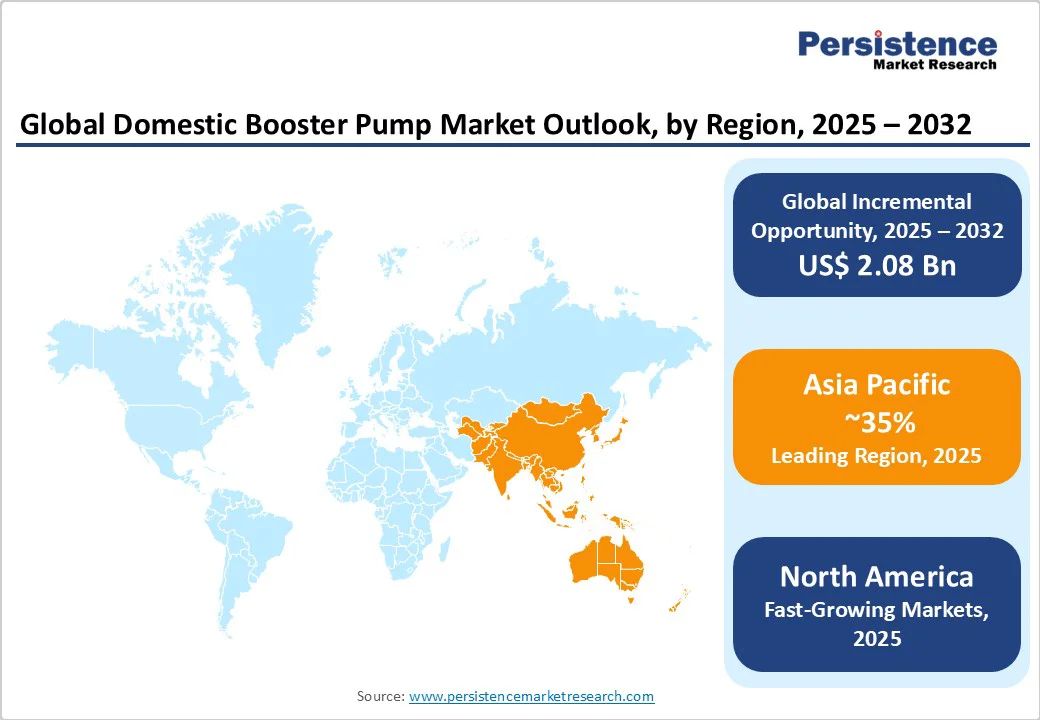

- Regional Leader: Asia Pacific dominates the domestic booster pump market with 35% market share, primarily due to rapid urbanization and infrastructure projects in China and India, which are driving consistent demand for reliable water systems.

- Fastest-growing Region: North America emerges as the fastest-growing region, driven by innovation in smart technologies and stringent energy regulations, boosting adoption rates.

- Leading Segment: Multi-stage product type leads the segment with 60% market share, preferred for superior pressure handling in multi-story homes amid rising construction.

- Fastest-growing Segment: The high-pressure range is growing fastest, supported by high-rise developments and water scarcity in urban areas.

- Growth Opportunities: Key opportunities lie in smart, IoT-integrated pumps that enable energy savings and remote control for eco-friendly residential applications.

| Key Insights | Details |

|---|---|

|

Domestic Booster Pump Size (2025E) |

US$3.5 Bn |

|

Market Value Forecast (2032F) |

US$5.6 Bn |

|

Projected Growth CAGR (2025-2032) |

6.9% |

|

Historical Market Growth (2019-2024) |

5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Urbanization and Infrastructure Development in Multi-Story Residential Buildings

The accelerating global urbanization trend is fundamentally reshaping water infrastructure requirements, with multi-story residential buildings and high-rise complexes demanding reliable water pressure solutions throughout all floors. By the end of 2024, China had constructed 95,000 reservoirs and 318,000 kilometers of dikes, with total water conservancy investment reaching 1.3529 trillion yuan (US$189.7 billion) under the 14th Five-Year Plan (2021-25), reflecting massive infrastructure modernization that directly drives booster pump adoption.

In urban centers with low municipal water pressure, booster pumps have become essential for ensuring a uniform water supply to bathrooms, kitchens, and appliances across residential infrastructure. In 2024, the Asia Pacific region commanded 42.5% of the market share, driven by population growth and government water management initiatives. This infrastructure expansion trend is particularly pronounced in developing economies, where rapid construction of residential complexes necessitates integrated water-pressure management systems from the design phase.

Increasing Water Scarcity and Energy-Efficient Solutions

Water scarcity affects over 2 billion people globally, according to the World Health Organization, fueling reliance on booster pumps to ensure optimal distribution in homes with an inconsistent water supply. In regions, including India and China, erratic municipal services prompt the installation of these systems, ensuring reliable access for cooking, bathing, and sanitation. Government initiatives, such as India's Jal Jeevan Mission, which aims to achieve 100% rural piped water by 2024, indirectly spur market growth by upgrading infrastructure. Advanced pumps with variable-speed drives minimize energy use, making them ideal for off-grid areas and supporting long-term water conservation efforts.

Leading manufacturers such as Grundfos, Pentair Plc., and Xylem Inc. are leveraging these smart pump technologies with automated pressure control to gain market share. In contrast, variable speed drive (VSD) pumps offer significant energy savings by adjusting motor speed to match demand, reducing operational costs by up to 20% for energy-related water products. In March 2024, Grundfos announced a strategic partnership with Schneider Electric to integrate EcoStruxure for Pumps with booster pump systems, enabling real-time monitoring and optimized energy consumption for municipal and commercial water networks.

Barrier Analysis - High Initial and Installation Costs

The substantial upfront costs of domestic booster pumps —often ranging from US$500 to US$2,000 per unit, including installation —deter adoption in cost-sensitive markets. Professional setup requires plumbing and electrical modifications, adding 20-30% to expenses, particularly in older homes lacking compatible infrastructure. This barrier is pronounced in low-income households, where alternatives such as basic pressure tanks are cheaper, slowing penetration despite long-term savings on water efficiency. Economic pressures, including inflation rates above 5% in emerging economies, exacerbate this issue, according to International Monetary Fund data.

The lack of standardized regulations across countries for smart pump data handling and storage complicates compliance for manufacturers and service providers operating globally, further increasing the total cost of ownership. These financial barriers are most pronounced in regions with high-cost sensitivity, where consumers prioritize initial investments over long-term operational savings, thereby limiting market penetration of advanced energy-efficient booster pump systems.

Technical and Maintenance Challenges

Operational issues such as noise, vibration, and component failures hinder domestic booster pump uptake, especially in quiet residential settings. Pumps exceeding 60 dB can disturb neighbors, leading to regulatory complaints in urban areas under noise standards from bodies such as the Environmental Protection Agency.

Maintenance demands skilled technicians, with repair costs averaging US$200 annually, and supply chain disruptions, seen in 15% of global manufacturing delays per World Trade Organization reports, further complicate availability. These factors reduce consumer confidence and limit market expansion in retrofit applications.

Opportunity Analysis - Adoption of Smart and Energy-Efficient Technologies

The shift toward smart domestic booster pumps integrated with IoT and AI presents significant growth potential, enabling remote monitoring and adaptive pressure control to cut energy use by 40%. With the global smart home market expanding at a 25% CAGR, manufacturers can target tech-savvy consumers in North America and Europe.

Recent innovations, such as variable frequency drives, allow pumps to adjust to real-time demand, aligning with Energy Star certifications and appealing to eco-conscious buyers. This opportunity is bolstered by government incentives, such as US$1.2 trillion infrastructure bills promoting efficient water systems, promising revenue streams for companies investing in R&D.

Expansion in Emerging Markets and Retrofitting

Emerging economies in Asia Pacific and Latin America offer vast opportunities for retrofitting older buildings with modern domestic booster pumps, driven by annual urbanization rates of 4%, per the World Bank. Policies such as China's 14th Five-Year Plan, which emphasizes water security, could drive demand for over 10 million units by 2030.

Focusing on corrosion-resistant, low-noise models for high-rise retrofits aligns with the high-pressure booster market dynamics, where sustainable materials meet regulatory requirements. News of partnerships between local firms and global companies, such as those in India's rural electrification, underscores the potential for 20% market share gains in underserved segments.

Category-wise Analysis

Product Type Insights

The multi-stage segment is anticipated to lead with a market share of 60% in 2025, owing to its superior ability to generate higher pressures essential for multi-story residences. Multi-stage pumps use sequential impellers to boost efficiency, handling elevations up to 100 meters, which is critical in urban high-rises, where single-stage models falter.

Data from the International Pump Users Association shows that 70% of new construction in Asia opt for multi-stage pumps due to their reliability in variable-flow conditions, reduced cavitation risk, and a 25% lifespan extension compared to alternatives. This dominance is reinforced by technological advancements in compact designs, making them suitable for space-constrained homes.

Pressure Range Insights

The Medium (2-5 Bar) pressure range dominates the category with a 50% share, as it balances everyday domestic needs such as consistent shower flow without excessive energy draw. Ideal for apartments and villas, these pumps maintain optimal pressure for appliances, helping prevent issues such as weak faucets, reported in 40% of urban households in World Health Organization surveys.

Industry statistics from the European Pump Manufacturers Association indicate medium-range models consume 15% less power than high-pressure variants, appealing to energy-conscious markets. Their versatility in handling fluctuating municipal supplies solidifies leadership, especially in regions with moderate water infrastructure.

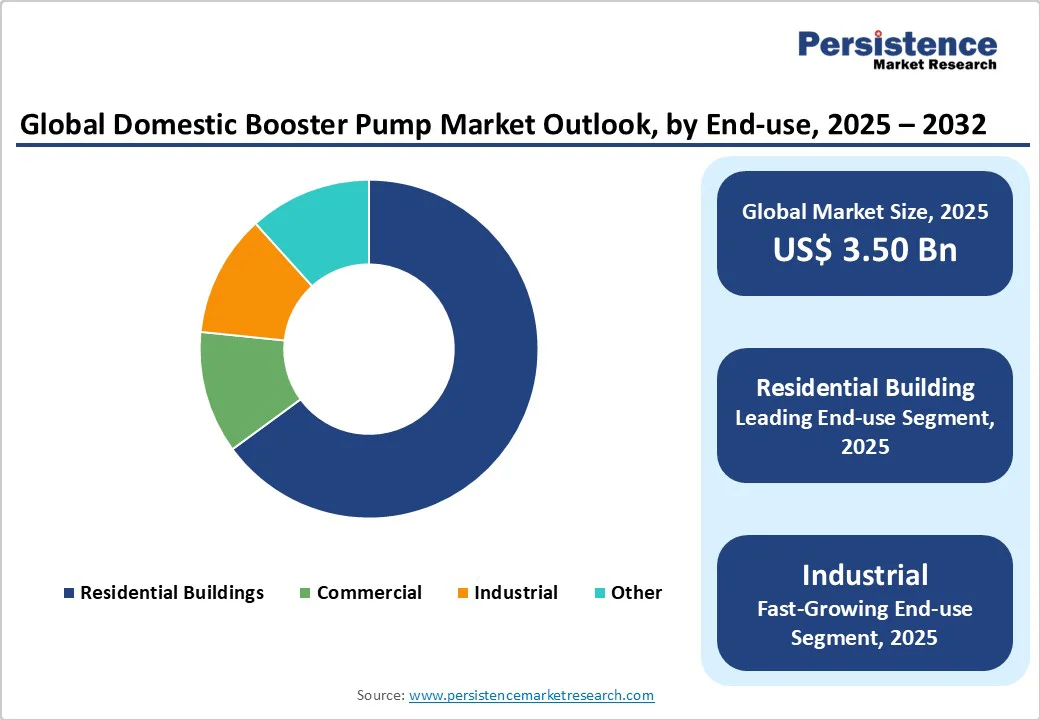

End-user Insights

Among end-user segments, residential buildings account for 65% of the market, driven by the surge in homeownership and the need for reliable water systems in private dwellings. Residential applications prioritize quiet, compact pumps for daily chores, with 80% of installations in single-family homes and apartments, according to U.S. Census Bureau housing data. This segment's lead is justified by population-driven demand, with 2.5 billion additional urban dwellers by 2050 necessitating efficient boosting, according to United Nations projections. Innovations such as app-controlled units further enhance appeal, ensuring steady pressure for modern lifestyles.

Regional Insights

North America Domestic Booster Pump Trends

North America leads in innovation for domestic booster pumps, with the U.S. holding dominance through stringent regulations, such as those from the Environmental Protection Agency, mandating 20% energy reductions in appliances. The region's ecosystem fosters R&D, as evidenced by Grundfos's launch of IoT-enabled models in 2024, improving efficiency amid water conservation drives. Adoption in smart homes is rising, supported by US$50 billion in federal infrastructure funding. California's drought policies are accelerating booster pump use, with installations up 15% in the residential sector, according to state water board reports, while emphasizing sustainable tech integration.

Europe Domestic Booster Pump Trends

Europe's domestic booster pump market thrives on regulatory harmonization under the EU Energy Efficiency Directive, targeting 32.5% improvements by 2030, boosting demand in Germany, the U.K., France, and Spain. Germany's Energiewende initiative promotes low-energy pumps, with sales rising 12% in 2024 per Eurostat. France's building codes favor multi-stage units for high-rises.

Harmonized standards such as CE marking facilitate cross-border trade, while the U.K.'s green homes grant spurs retrofits, enhancing performance in aging infrastructure. Spain's tourism-driven coastal developments further drive adoption.

Asia Pacific Domestic Booster Pump Trends

Asia Pacific is experiencing robust growth in domestic booster pumps, driven by manufacturing advantages in China, Japan, India, and ASEAN nations, well and urbanization. China's Belt and Road projects install millions of units annually, with India's Smart Cities Mission targeting 100 cities by 2025, increasing demand 18% per government reports.

ASEAN's economic boom, with GDP growth at 5%, leverages cost-effective production in Vietnam and Indonesia, focusing on affordable medium-pressure models for rural electrification. Japan's tech focus yields energy-saving innovations.

Competitive Landscape

The global domestic booster pump market is moderately consolidated, with top players such as Grundfos and Xylem holding a 40% share through global networks and R&D investments exceeding US$500 Million annually. Companies pursue expansion via acquisitions and partnerships, emphasizing energy-efficient models to differentiate via IoT integration. Emerging trends include subscription-based maintenance services, fostering loyalty in fragmented residential segments.

Key Market Developments

- January 2025: Grundfos unveiled a solar-compatible booster pump series, reducing energy costs by 35%, targeting off-grid homes in emerging markets amid global sustainability pushes.

- October 2024: Xylem Inc. expanded its domestic line with AI-driven pressure optimization, enhancing reliability for multi-family units following successful pilots in the U.S.

- March 2024: Pentair Plc. acquired a key supplier to bolster variable speed technology, aiming to capture 10% more share in energy-efficient residential applications.

Companies Covered in Domestic Booster Pump Market

- Grundfos

- Pentair Plc.

- Xylem Inc.

- KSB AG,

- Franklin Electric

- ESPA

- Zoeller Company

- Aqua Groups

- Donaldson

- Ebara

- Euro Molten Pumps

- Kirloskar Brothers

- Sulzer

- Wilo SE

- DAB Pumps

Frequently Asked Questions

The domestic booster pump market is expected to reach US$5.6 Billion by 2032, growing from US$3.5 Billion in 2025 at a 6.9% CAGR, driven by urbanization and efficiency demands.

Key drivers include rapid urbanization, which is boosting residential construction, and growing water scarcity, which is driving demand for reliable pressure systems. According to the United Nations, the global urban population is projected to reach 68% by 2050.

The multi stage segment leads with 55% share, favored for higher pressure efficiency in multi-story homes, reducing energy use by 25% as per industry associations.

Asia Pacific leads the domestic booster pump market due to manufacturing advantages and urbanization in China and India, holding over 40% share amid infrastructure booms.

Smart IoT-integrated pumps offer major potential, cutting energy by 40% and aligning with sustainability policies such as EU directives.

Leading players in the domestic booster pump market include Grundfos, Xylem Inc., and Pentair Plc., dominating through R&D and global presence in efficient water solutions.