- Display Technologies

- DLP Projector Market

DLP Projector Market Size, Share, and Growth Forecast, 2026- 2033

DLP Projector Market Light Source (Lamp, LED, Laser), Chip Model (One Chip, Three Chip), Brightness (Less than 2999 Lumens, 3000 to 5999 Lumens, 6000 Lumens & Above), Application (Home Entertainment & Cinema, Business, Education & Government, Large Venues, Others), and Region Analysis 2026 to 2033

Market Overview

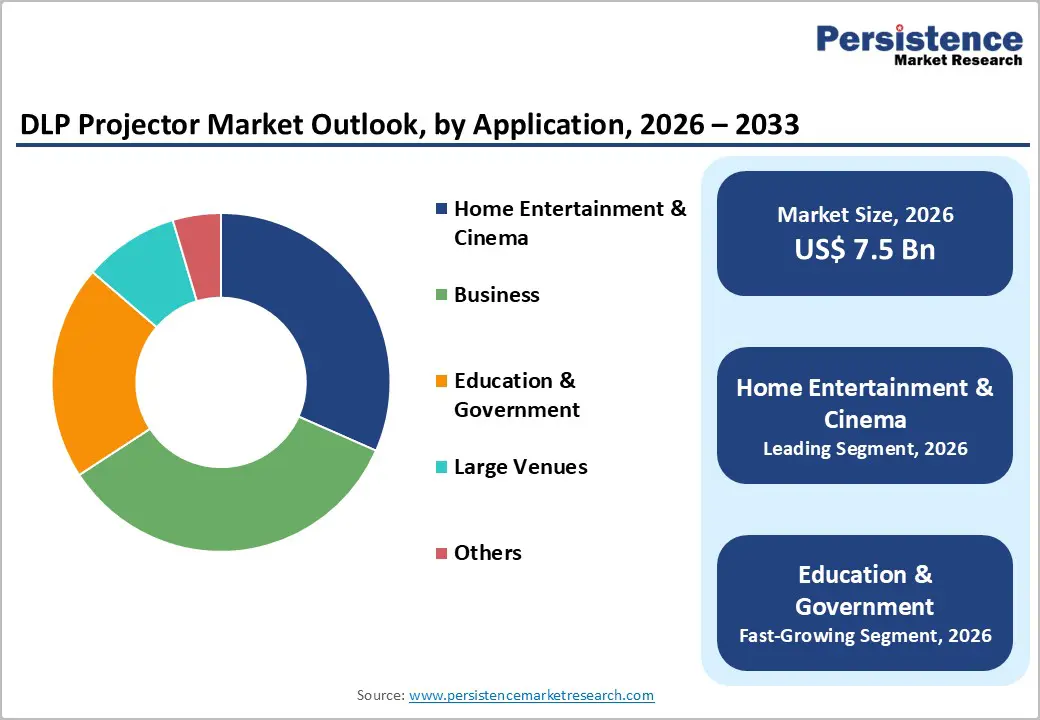

The global DLP Projector Market size is projected to reach US$7.5 Billion in 2026 and is anticipated to grow to US$10.8 Billion by 2033, expanding at a CAGR of 5.4% between 2026 and 2033. This expansion reflects sustained demand across education, corporate, entertainment, and cinema sectors, driven by digital transformation initiatives and rising investment in visual communication infrastructure. The shift toward laser light sources, enhanced brightness capabilities, and 4K resolution standards continues to elevate market dynamics. Additionally, emerging economies' growing digitalization in classrooms and entertainment venues, coupled with the proliferation of smart home technologies, provides significant momentum for sustained expansion throughout the forecast period.

Key Highlights Summary

- Laser segment grows fastest at 6.4% CAGR; lamp systems lead with 34% share; single-chip DLP dominates 68%, three-chip grows 5.9% for professional use.

- Home Entertainment & Cinema fastest-growing; Business leads; 3,000–5,999 lumens category holds 40%; ultra-short throw projectors rise 6.4% CAGR.

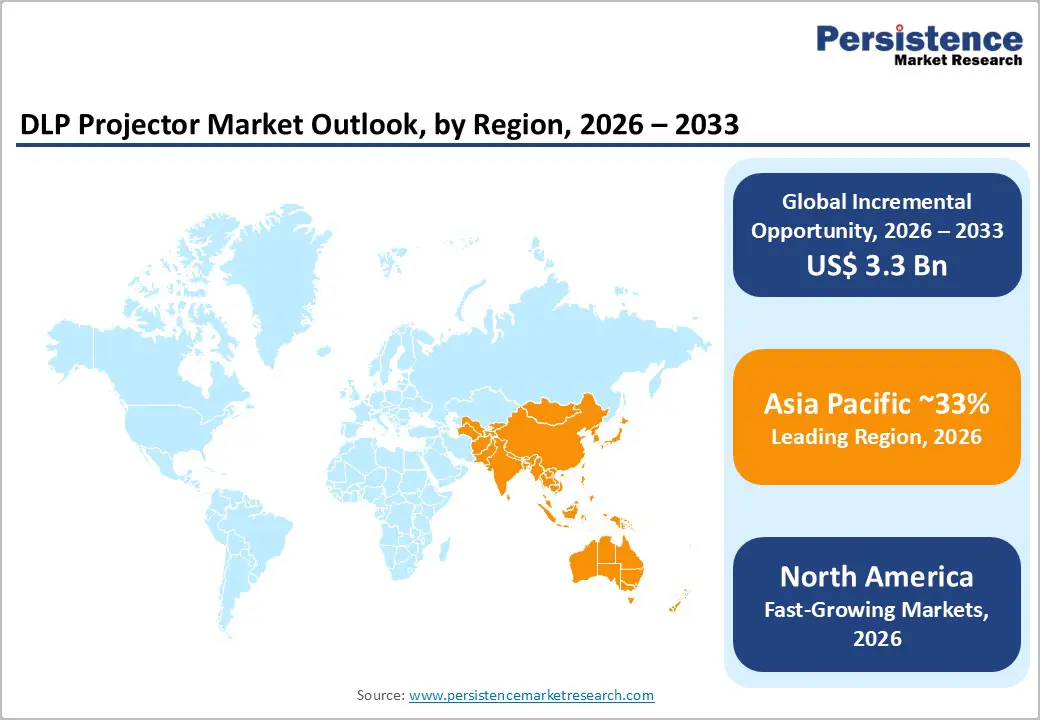

- North America grows 5.1% CAGR; Europe 4.6% with 21% share; Asia-Pacific leads 33%, driven by cinema and education investments.

- Key strategies include Barco-CJ 4DPLEX 1,000-projector deal, Optoma UHZ premium laser launches, and Barco India expansion to 50–80 screens by 2030.

| Key Insights | Details |

|---|---|

|

DLP Projector Market Size (2026E) |

US$ 7.5 billion |

|

Market Value Forecast (2033F) |

US$ 10.8 billion |

|

Projected Growth CAGR (2026-2033) |

5.4% |

|

Historical Market Growth (2020-2025) |

4.3% |

Market Dynamics Analysis

Market Drivers

Digital Transformation in Educational Institutions

The education sector represents a critical growth catalyst, with governments and educational authorities worldwide implementing comprehensive digitalization programs. Smart classroom initiatives, particularly in Asia-Pacific and emerging markets, mandate adoption of high-quality projection systems for interactive learning environments. India's government-backed smart classroom programs and similar initiatives across Southeast Asian nations have substantially increased institutional procurement budgets. The shift from traditional chalkboards to digital displays enhances student engagement through multimedia content delivery, collaborative tools, and e-learning platforms. Educational institutions recognize projection technology as cost-effective solutions compared to large-format LED displays, with DLP projectors offering superior image quality, durability, and longevity. Growing online learning accessibility, expanded through COVID-19 pandemic adaptations, has normalized digital presentation requirements, driving sustained demand beyond pandemic periods.

Expansion of Cinema Digitalization and Home Entertainment Sectors

The entertainment industry's rapid digitalization creates substantial demand across cinema halls, gaming venues, and residential applications. Film industry conversion from analog to digital cinema projection has become imperative, with China operating over 82,248 cinema screens requiring digital upgrading. DLP projectors dominate digital cinema installations due to superior contrast ratios, operational speed, and cost-effectiveness compared to traditional projection technologies. Simultaneous growth in home entertainment investments reflects consumer preference for cinematic experiences within residential spaces, supported by declining projector prices and improving technology accessibility. Streaming services and gaming applications further amplify demand for high-resolution, high-brightness projection systems. The segment's expansion is supported by increasing investments in premium entertainment facilities, including theaters, museums, theme parks, and entertainment venues globally.

Market Restraints

Intensified Competition from Alternative Display Technologies

Emerging competition from large-format LED displays, OLED screens, and advanced flat-panel technologies poses structural market challenges. LED display manufacturers continuously reduce installation costs and improve resolution capabilities, creating viable alternatives for applications traditionally served by projection systems. Unlike projectors, large LED screens provide immediate illumination without installation complexity, appealing to venues prioritizing operational simplicity. Additionally, microLED television technology advances toward extremely large screen sizes (exceeding 100 inches) at declining prices, capturing segments previously dominated by high-end projectors. This technological competition constrains pricing power and necessitates continuous innovation investments to maintain competitive differentiation.

Economic Sensitivity and Price Volatility in Target Markets

DLP projector markets demonstrate susceptibility to macroeconomic fluctuations, particularly in discretionary spending categories. Emerging markets experiencing currency volatility, inflation pressures, and variable disposable income levels exhibit inconsistent purchasing patterns for premium audio-visual equipment. Budget constraints within educational institutions, despite government digitalization mandates, frequently delay or limit procurement volumes. Commercial sectors facing economic uncertainty defer capital expenditure decisions for venue upgrades and installation projects. Supply chain disruptions continue affecting component availability and manufacturing timelines, while raw material cost volatility impacts final product pricing, reducing market competitiveness during inflationary periods.

Market Opportunities

Premium Cinematic Experiences and HDR Technology Adoption

Advanced HDR projection technology, exemplified by Barco's HDR by Barco platform expanding across North American, European, and Asian cinemas, creates differentiated premium offerings justifying higher ticket prices and venue investments. Premium cinema formats increasingly incorporate laser projection with HDR capabilities, generating substantial revenue uplift for exhibition operators and equipment manufacturers. The global premium cinema market, characterized by higher profit margins and customer willingness to pay premiums for superior experiences, offers significant revenue expansion potential as installations proliferate across major entertainment markets.

Ultra-Short Throw Projectors and Flexible Installation Solutions

Ultra-short throw (UST) DLP projectors enable installation flexibility previously impossible with standard projection systems. These devices project large images from minimal distances, facilitating deployment in space-constrained environments including small apartments, retail spaces, and interactive learning environments. The residential segment shows accelerating adoption as consumers invest in home entertainment systems within spatial limitations. Commercial applications spanning retail signage, museum exhibitions, and interactive displays expand addressable markets. Current market data indicates ultra-short throw segments growing at 6.4% CAGR, reflecting strong consumer demand for space-efficient, versatile projection solutions.

Segmentation Analysis

Light Source Analysis

The lamp-based segment maintains market leadership with 34% share, supported by established manufacturing infrastructure, backward compatibility with existing installations, and cost-effective initial procurement. Lamp technology, refined through decades of commercial deployment, delivers proven brightness levels between 2,000 and 6,000 lumens for education, business, and mid-scale venues. Competitive pricing attracts budget-conscious buyers, particularly across emerging markets. Although regular lamp replacements create downtime and higher lifecycle costs, the vast installed base and reliable performance sustain strong absolute demand globally today across segments.

The laser light source segment is the fastest growing, expanding at 6.4% CAGR while displacing lamp installations. Laser systems exceed 20,000 operating hours, deliver consistent brightness, and eliminate maintenance. Superior color stability, HDR capability, and improving cost-per-lumen economics drive adoption in digital cinema, large venues, and premium home entertainment applications.

Chip Model Analysis

One-chip DLP architectures command a dominant 68% market share, driven by cost efficiency, compact form factors, and versatility across consumer and commercial applications. Single-chip systems leverage advanced pixel-shifting to deliver effective high resolution, including pseudo 4K, without the complexity of multi-chip designs. Manufacturers favor these platforms for home entertainment, corporate presentation, and education due to manufacturing scale benefits, portability, and simplified installation. Market leadership reflects alignment with mainstream needs, where affordability, reliability, and deployment flexibility outweigh absolute color precision.

Three-chip DLP implementations grow at a 5.9% CAGR, addressing premium cinematic and professional applications requiring exceptional brightness, contrast, and color accuracy. Dedicated RGB optical paths eliminate rainbow artifacts and enable trillions of color gradations. Adoption accelerates in digital cinema, medical imaging, scientific visualization, and live-event staging despite higher system costs.

Brightness Analysis

The 3,000–5,999 lumens brightness category leads with 40% market share, representing an optimal balance between brightness performance, cost efficiency, and energy consumption across applications. This range meets typical classroom needs, mid-sized business environments, and home entertainment under moderate ambient light. Manufacturer standardization reflects consensus that this level satisfies nearly 80% of use cases. Competitive mid-tier pricing supports large institutional procurement while preserving margins, driving volume adoption across education, corporate offices, and mid-scale entertainment venues globally with consistent deployment scalability benefits.

High-brightness projectors above 6,000 lumens address large venues, outdoor events, theaters, and arenas requiring strong visibility under intense ambient light. Cinema increasingly specifies outputs exceeding 15,000 lumens. Despite premium pricing and higher energy use, demand rises with venue expansion, live events, and entertainment infrastructure investments globally across professional display markets.

Application Analysis

The business application segment leads the market with 34% share, driven by sustained corporate investment in presentation and collaboration infrastructure. Executive conference rooms, training centers, and corporate headquarters rely on DLP projectors for boardroom presentations, video conferencing, and large-screen content sharing. Digital transformation mandates updated collaboration technologies supporting hybrid work, remote engagement, and virtual presentations. Premium laser systems with short-throw capabilities integrate seamlessly into modern offices without ceiling obstructions, enabling efficient deployment and reliable performance across professional environments globally.

Home entertainment and cinema applications are the fastest-growing segment, expanding at 5.7% CAGR, fueled by consumer investment in residential cinematic setups and gaming. Lower projector costs, advanced technologies, streaming proliferation, and immersive entertainment preferences drive adoption, while manufacturers increasingly prioritize consumer-focused portfolios, accelerating growth in home entertainment markets worldwide.

Throw Distance Analysis

Normal throw projectors, requiring 1-3 meter distances for standard screen sizes, maintain 51% market share through versatile application compatibility across schools, corporate offices, and entertainment venues. Standard installation practices, established mounting infrastructure, and backward compatibility with existing room designs favor normal throw configurations. Ceiling mounting, wall installation, and rear-projection implementations distribute projector placement flexibility, accommodating diverse venue architectures.

Ultra-short throw projectors expanding at 6.4% CAGR enable space-constrained installations, small apartments, retail environments, and interactive displays. Installation flexibility, elimination of mounting complexity, and shadow-free viewing advantages appeal to modern installation preferences. Residential market growth, retail applications, and education sector investments increasingly specify ultra-short throw systems, driving segment expansion.

Regional Market Insights

North America

North America maintains significant market influence driven by established entertainment industries, mature corporate infrastructure, and substantial consumer spending on home entertainment systems. The region accounts for approximately 40% of global digital cinema market share, with the United States anchoring regional demand. Premium cinema format expansion, including HDR by Barco installations reaching 30 theaters by 2025, demonstrates sustained theatrical upgrade investments. Corporate presentation technology adoption remains robust as organizations prioritize upgraded collaboration infrastructure supporting hybrid work environments. Consumer home theater segment expansion reflects rising discretionary income allocation toward residential entertainment amenities.

North America's growth trajectory of 5.1% CAGR reflects mature market characteristics where upgrade cycles drive expansion rather than new installation growth. Technological advancements, including 4K resolution, laser light sources, and HDR capabilities, justify premium pricing supporting manufacturer margin expectations. Regional regulatory emphasis on energy efficiency favors advanced projection technologies offering extended operational lifespans and reduced maintenance requirements compared to legacy lamp-based systems.

Europe

Europe's DLP projector market demonstrates steady 4.6% CAGR expansion while maintaining approximately 21% global market share. Germany, United Kingdom, and France lead regional demand through robust cinema infrastructure, established corporate presentation markets, and growing residential entertainment sector participation. European regulatory frameworks emphasizing environmental sustainability encourage adoption of energy-efficient laser and LED light source technologies. Government initiatives promoting education digitalization, particularly in Central and Eastern European markets, expand institutional procurement budgets for classroom projection systems.

Regional market characteristics emphasize technology quality, sustainability credentials, and long-term reliability. European institutional buyers prioritize established brand recognition, comprehensive warranty support, and compliance with regional technical standards. Entertainment venue modernization initiatives continue supporting cinema digitalization and premium format expansion across established markets.

Asia-Pacific

Asia-Pacific dominates global market dynamics with commanding 33% market share and accelerating expansion momentum. China's cinema infrastructure modernization, encompassing 82,000+ screen installations, creates unmatched equipment procurement opportunities. India's government-mandated smart classroom programs, combined with rapid urbanization and rising disposable incomes, drive substantial educational institution procurement. ASEAN nations' entertainment industry growth, manufacturing sector expansion, and digital infrastructure development further amplify regional demand.

Regional manufacturers including BenQ, Vivitek, Panasonic, and Sharp leverage cost-competitive production supporting price-sensitive market segments while maintaining profitability. Rapid economic development, increasing consumer purchasing power, and substantial corporate infrastructure investments position Asia-Pacific as the primary market growth engine. The region's demographic profile featuring younger populations with entertainment-focused spending preferences supports sustained expansion throughout forecast periods.

Competitive Landscape

Strategic Developments

- In April 2025, Barco and CJ 4DPLEX announced commitment for deployment of up to 1,000 laser projectors by 2030, expanding SCREENX premium cinema format globally. Agreement strengthens collaborative positioning for premium exhibition market expansion.

- In September 2024, Optoma introduced advanced gaming and home entertainment laser projector featuring 4K UHD resolution, 3,500 lumens brightness, 30,000-hour laser longevity, and ultra-low gaming input lag (4.4ms), targeting gaming enthusiasts and cinematic experience seekers.

- February 2025, Optoma debuted premium dual-laser projector with 5,000 lumens brightness, 4K UHD resolution, and 300-inch projection capability at ISE 2025, advancing high-brightness cinema projector market segment with advanced color accuracy and flexible installation options.

Business Strategies

Market leaders pursue multi-dimensional strategies focused on innovation, geographic expansion, and segment diversification. Key approaches include laser technology adoption, balancing premium and cost-sensitive markets, strategic partnerships, and smart connectivity integration. Optoma, Barco, and BenQ exemplify targeted portfolios, emphasizing HDR, LED longevity, maintenance efficiency, and ecosystem-enabled professional and consumer applications.

Companies Covered in DLP Projector Market

- Texas Instruments Inc.

- Optoma Corporation

- Barco NV

- BenQ Corporation

- Digital Projection Limited

- NEC Corporation

- Sharp Corporation

- Panasonic Corporation

- Vivitek / Delta Electronics

- ViewSonic Corporation

- XGIMI

- Christie Digital Systems

- Acer Inc.

- LG Electronics

- Epson Corporation

Frequently Asked Questions

The global DLP Projector Market is valued at US$5.8 billion (2020) and is projected to reach US$10.8 billion by 2033.

Market growth is driven by smart classroom digitalization, cinema modernization, laser and LED technology adoption, rising home entertainment demand, and corporate investment in hybrid work collaboration infrastructure.

The DLP Projector Market is anticipated to expand at a CAGR of 5.36% between 2026 and 2033.

Key opportunities include HDR laser cinema expansion, ultra-short-throw projector adoption, rapid Asia-Pacific infrastructure upgrades, and emerging applications in interactive displays and retail digital signage.

Leading players include Texas Instruments, Optoma, Barco, BenQ, NEC, Panasonic, Christie Digital, ViewSonic, LG Electronics, Epson, Acer, XGIMI, Sharp, Vivitek, and Digital Projection.