- Home Appliances

- Desktop Calculator Market

Desktop Calculator Market Size, Share, and Growth Forecast, 2026 - 2033

Desktop Calculator Market by Component Type (Basic Functional Calculators, Scientific Calculators, Financial/Business Calculators, Graphing Calculators, Misc.), End user (Education, Corporate & Office Use, Personal/Home Use, Retail & Commercial Use, Misc.) and Regional Analysis for 2026 - 2033

Desktop Calculator Market Size and Trends Analysis

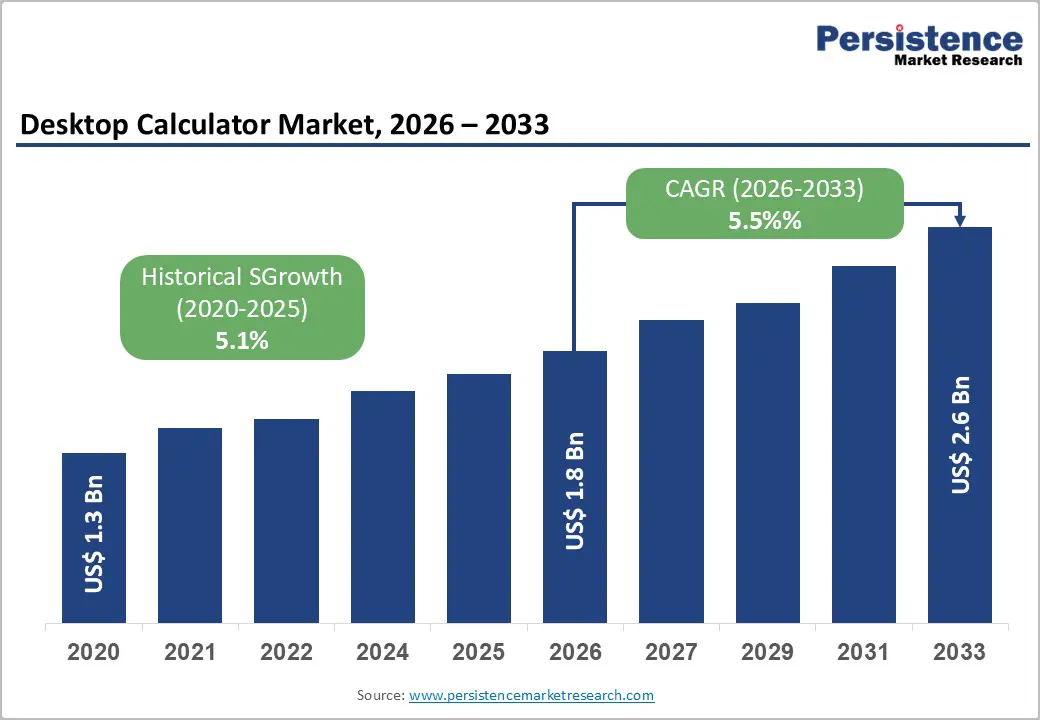

The Global Desktop Calculator Market size was valued at US$ 1.8 Bn in 2026 and is projected to reach US$ 2.6 Bn by 2033, growing at a CAGR of 5.5% between 2026 and 2033. The market demonstrated resilience with historical growth from US$1.3 billion in 2020, achieving a 5.1% CAGR through 2026.

Sustained expansion reflects persistent institutional demand from financial services, educational infrastructure investment aligned with record global tertiary enrollment of 264 million students, and professional workplace requirements. The acceleration from a 5.1% historical CAGR to a projected 5.5% growth rate indicates strengthening demand dynamics driven by specialised computational needs across corporate, academic, and household financial management applications.

Key Industry Highlights:

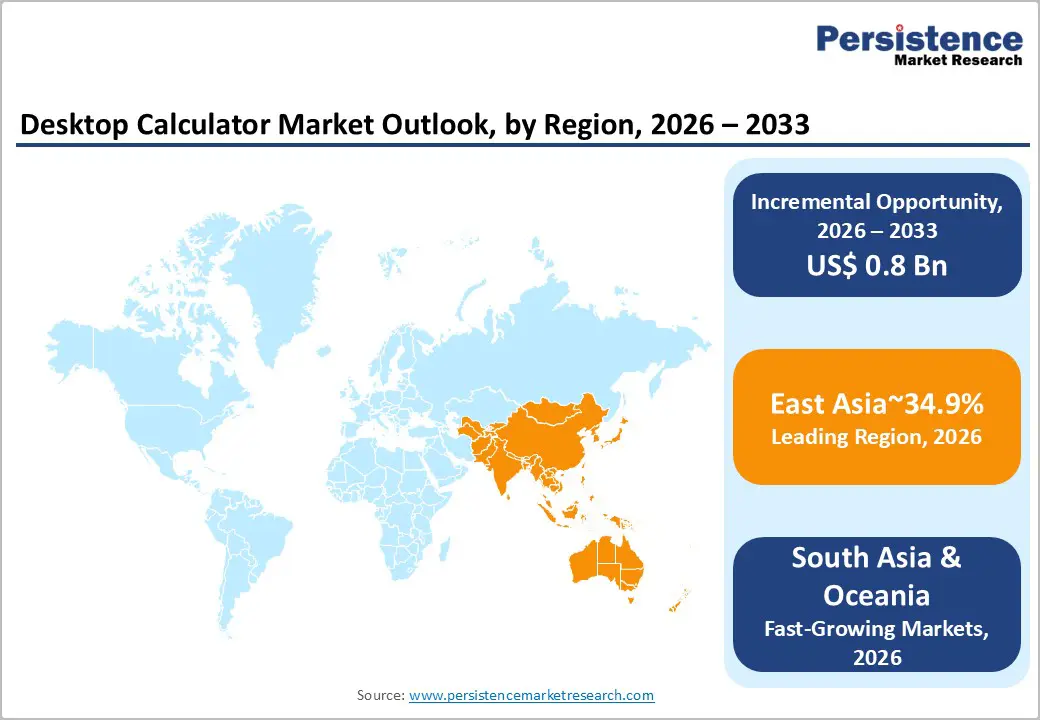

- Leading Region: East Asia leads the global market with a dominant 34.9% share, driven by high educational enrollment, robust professional services growth, manufacturing sector demand, and strong international student mobility.

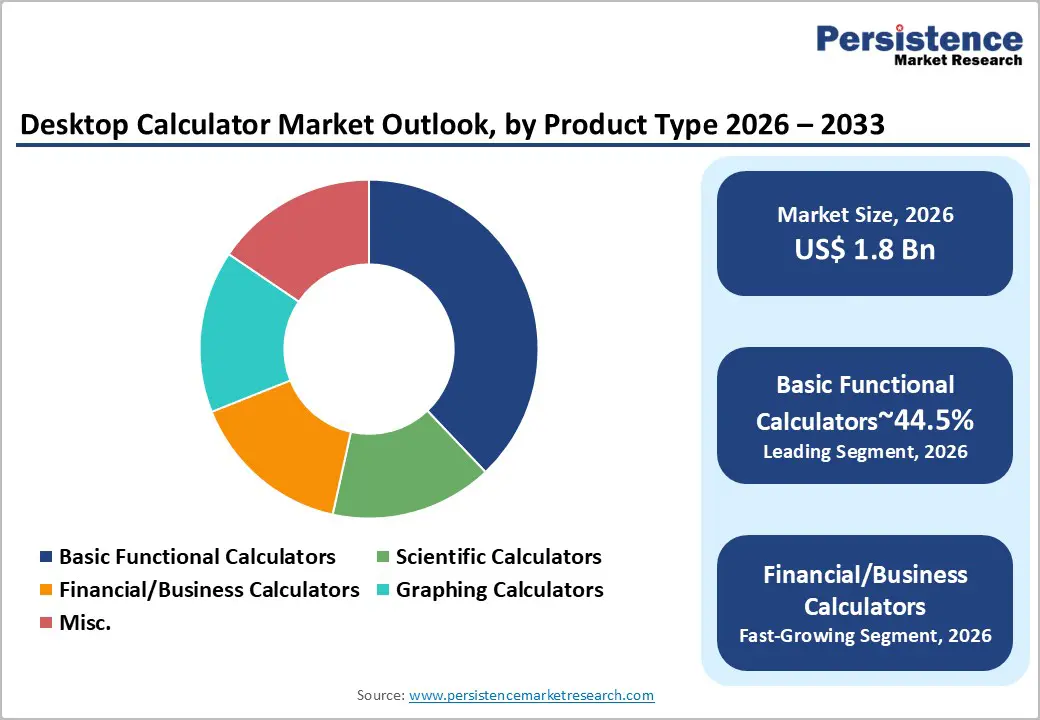

- Dominant Segment: Basic functional calculators remain the leading product segment with 44.5% share in 2025, reflecting widespread adoption across educational institutions, retail, and corporate office environments.

- Leading End User Segment: Corporate and office environments are the largest end-user segment at 38.9% in 2025, supported by institutional procurement cycles, professional services expansion, and standardised workplace equipment requirements.

- Fastest-Growing Segment: Financial and business calculators are the fastest-growing product segment, propelled by professional services sector employment growth, increasing household financial planning complexity, and adoption for quantitative and statistical analysis workflows.

- Key Driver: Key growth drivers include expanding global educational enrollment, standardised assessment requirements, and professional services employment growth requiring precise, compliant computational tools.

| Global Market Attributes | Key Insights |

|---|---|

| Desktop Calculator Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 2.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Dynamics

Growth Drivers

Educational Enrollment Expansion and Standardized Assessment Requirements

Global higher education infrastructure is experiencing unprecedented growth, with tertiary enrollment reaching a record 264 million students worldwide as of 2023. This represents a surge of 25 million students since 2020 and is more than double the enrollment levels of 2000, according to UNESCO data.

The Market benefits directly from this educational expansion as mathematics, science, and technology curricula mandate approved calculation devices for coursework completion and standardised examination protocols. Academic mobility has tripled since 2000, with 6.9 million students currently studying outside their home countries, creating standardised equipment requirements across international educational systems.

UNESCO's Global Convention on the Recognition of Qualifications encompasses 38 States Parties hosting 2 million internationally mobile students, establishing unified academic standards that include approved calculation tool specifications. This institutional framework generates consistent procurement cycles across secondary and tertiary educational institutions, sustaining calculator demand independent of consumer technology substitution trends.

Professional Services Sector Employment Trajectory and Computational Accuracy Standards

The U.S. Bureau of Labour Statistics projects total employment will increase from 170.0 million in 2024 to 175.2 million in 2034, adding 5.2 million new jobs with significant concentration in professional, scientific, and technical services sectors. The Desktop Calculator Market captures sustained demand from business and financial operations occupations where computational accuracy, audit trail requirements, and regulatory compliance protocols necessitate dedicated calculation hardware.

Computer and mathematical occupational groups are projected to experience substantially faster than average employment growth, with data scientists, statisticians, and information security analysts requiring precise calculation tools for quantitative analysis workflows.

The expansion of digital business operations generates massive data volumes requiring workers who collect, organise, analyse, and protect information using specialised computational tools. Financial services institutions operating under securities regulatory oversight maintain a preference for dedicated calculation devices that provide tactile feedback, error reduction, and documentation capabilities unavailable through general-purpose software alternatives.

Market Restraining Factors

Digital Native Workforce Preferences and Software-Based Calculation Ecosystems

Younger workforce entrants demonstrate a strong preference for integrated software solutions and mobile applications that consolidate calculation functionality within general-purpose devices. Professional services firms increasingly adopt cloud-based financial modelling platforms, enterprise resource planning systems, and collaborative spreadsheet applications that reduce the perceived necessity for standalone calculation hardware.

Software-as-a-Service business intelligence tools incorporate advanced calculation engines with visualisation capabilities exceeding traditional calculator functionality. This generational shift in computational tool preferences creates headwinds for desktop calculator adoption, particularly within technology-forward industries and startup environments where device minimisation aligns with operational efficiency objectives and remote work flexibility requirements.

Key Market Opportunities

Academic Mobility Infrastructure and Cross-Border Educational Standardisation

International student mobility tripled since 2000 to reach 6.9 million students studying outside their home countries, creating opportunities for the Desktop Calculator Market through standardised educational equipment requirements.

UNESCO's Global Convention framework encompasses 131 million students representing 50 percent of global tertiary enrollment, establishing unified qualification recognition standards that extend to approved calculation tool specifications. Countries including France, the United Kingdom, Australia, Japan, and the Republic of Korea demonstrate substantial international education hosting capacity requiring consistent academic infrastructure.

The Market can leverage this mobility through the development of internationally certified calculator models meeting multiple curriculum standards simultaneously, enabling students to utilize consistent tools across geographic transitions. Educational institutions implementing UNESCO Convention principles require equipment suppliers capable of supporting diverse international student populations with unified product offerings. Manufacturers establishing partnerships with international education agencies and cross-border university consortia position themselves to capture procurement opportunities as global academic integration accelerates beyond the current 72 percent coverage among convention signatory nations.

Healthcare Sector Employment Expansion and Specialised Calculation Requirements

The healthcare and social assistance sector is projected to create approximately 45 percent of all new jobs through 2032, according to U.S. Bureau of Labour Statistics projections, representing massive workforce expansion requiring specialised computational tools. The Desktop Calculator Market benefits from healthcare-specific calculation requirements, including pharmaceutical dosage computations, medical billing and coding, health insurance claim processing, and biostatistical analysis supporting clinical research. Home health and personal care aides, nurse practitioners, and medical and health services managers represent occupations projected for both large-scale employment increases and rapid growth rates.

Healthcare calculation requirements emphasise accuracy, compliance documentation, and error prevention in contexts where computational mistakes carry patient safety implications and regulatory consequences. Desktop calculators designed for healthcare applications with specialised functions for unit conversions, dosage calculations, and statistical analysis address unmet professional needs. Manufacturers can develop healthcare-certified calculator models meeting medical device standards, potentially capturing premium pricing through specialised functionality and regulatory compliance features addressing this substantially expanding employment sector.

Category-wise Analysis

Product Type Insights

Basic functional calculators maintain a share of 44.5% leadership through universal applicability across diverse use cases requiring fundamental arithmetic operations without specialised training. The segment benefits from price accessibility, enabling widespread adoption in retail environments, small business operations, household budget management, and educational contexts where advanced functionality remains unnecessary. Distribution advantages through office supply retailers, e-commerce platforms, and mass merchandisers sustain a volume-driven market position.

Manufacturing scale economies enable competitive unit economics supporting replacement purchase patterns across corporate and institutional environments. The 5.2 million projected new jobs through 2034 in the U.S. economy create sustained demand for basic workplace peripherals, including entry-level calculation tools. Basic calculators serve as standard office equipment across administrative functions, reception areas, and retail point-of-sale applications where dedicated calculation devices complement computer-based systems without requiring software navigation or digital device access.

Financial and business calculators experience accelerated adoption driven by professional services sector employment expansion and increasing household financial planning complexity. The computer and mathematical occupational group is projected to grow substantially faster than average employment rates require sophisticated calculation tools for quantitative analysis, financial modelling, and statistical computations. These specialized devices incorporate time value of money functions, amortisation calculations, bond valuation, depreciation schedules, and break-even analysis capabilities essential for business financial decision-making.

End User Insights

Corporate and office environments represent the dominant end-user segment, holding a share of 38.9 percent through a combination of institutional procurement scale, standardised workplace equipment specifications, and predictable replacement cycles. The professional, scientific, and technical services sector is projected to capture significant portions of 5.2 million new jobs through 2034, sustaining demand for workplace calculation tools. Organisations maintain calculator inventories across accounting departments, financial analysis teams, administrative operations, and facilities management functions, where quick calculations support daily workflows.

Enterprise technology standardisation initiatives incorporate peripheral device specifications, ensuring operational consistency across geographic locations and departmental structures. The healthcare and social assistance sector creating approximately 45percent of projected new jobs, requires medical billing, insurance claim processing, and patient account management functions utilising dedicated calculation devices. Corporate procurement departments source calculators through established office supply contracts and vendor relationships, generating stable demand patterns resistant to consumer technology substitution trends.

Regional Insights and Trends

North America Market Trend

North America maintains a substantial market presence driven by mature educational infrastructure, extensive corporate office environments, and sustained professional services employment despite experiencing slower overall economic growth trajectories. The U.S. total employment projected to increase from 170.0 million in 2024 to 175.2 million in 2034 represents 3.1 percent growth, significantly slower than the 13.0 percent employment growth recorded over the 2014-2024 decade, indicating market maturation requiring a replacement demand focus rather than expansion-driven growth strategies.

The healthcare and social assistance sector, creating approximately fifty percent of all projected job gains from 2022 to 2032, generates concentrated regional demand for basic functional and financial calculators serving administrative, billing, and patient care coordination functions across hospital systems, outpatient facilities, and home healthcare agencies managing aging population care requirements

Regional opportunities emerge through hybrid work environment adaptation, with remote worker home office equipment purchases supplementing traditional corporate procurement channels. The projected around 2.2 percent growth in self-employed workers creates direct-to-consumer sales opportunities for financial calculators addressing small business accounting, freelance professional invoicing, and independent contractor tax preparation requirements. Educational institutional demand remains stable across K-12 standardised testing requirements, university STEM program enrollment, and community college technical training initiatives requiring approved calculator models for mathematics and science coursework, despite overall enrollment growth constraints from demographic trends.

East Asia Market Trend

East Asia commands 34.9% share in the global market position through substantial educational enrollment, manufacturing sector concentration, expanding professional services employment, and robust international student mobility patterns. The region's 264 million students enrolled in higher education globally in 2025 includes significant East Asian concentration, with regional institutions increasingly hosting international students

The threefold increase in internationally mobile students since 2000 reaching 6.9 million globally demonstrates sustained academic mobility benefiting regional calculator demand through examination requirements, curriculum standardization, and STEM program proliferation across engineering, mathematics, and science disciplines requiring specialized calculation tools.

Manufacturing sector dominance across electronics production, automotive assembly, and industrial equipment fabrication generates substantial calculator demand for quality control, production planning, inventory management, and shop floor calculation requirements serving operational efficiency objectives. Regional professional services expansion, financial sector development, and corporate office environment modernization drive financial calculator adoption for investment analysis, accounting functions, and business planning activities supporting economic growth trajectories.

Government educational investment initiatives targeting STEM curriculum enhancement, technical training program expansion, and university research infrastructure development sustain institutional procurement patterns. The gender parity achievement in global higher education with 113 women enrolled per 100 men in 2023 broadens addressable market demographics across East Asian nations experiencing female education participation expansion. E-commerce platform proliferation, digital retail channels, and online educational supply networks provide accessible distribution mechanisms reaching individual consumers, educational institutions, and corporate purchasers through integrated logistics infrastructure supporting regional market leadership positioning.

Europe Market Trend

Europe maintains substantial market presence through established educational systems, professional services employment, and regulatory framework stability, supporting sustained calculator demand across institutional and consumer segments.

The 38 States Parties to the Global Convention, representing 2 million internationally mobile students, includes substantial European participation facilitating cross-border education recognition, necessitating approved calculator models for qualification equivalency and examination standardisation.

Competitive Landscape

The global desktop calculator market is moderately consolidated, with a mix of long-established electronics manufacturers and specialised calculator brands competing across consumer, educational, and professional segments. Industry leaders such as Casio Computer Co. Ltd, Canon USA Inc., Hewlett-Packard Development Company, Sharp Electronics Corporation, and Citizen Systems hold significant market share due to their strong brand equity, extensive distribution networks, and continuous product innovation in both basic and advanced desktop calculators.

These key players focus on design differentiation, durability, and feature enhancements such as solar power and ergonomic layouts to maintain their competitive edge. Alongside these incumbents, regional and niche players like Lyreco and Claro Calculators contribute to market diversity by offering cost-effective solutions for bulk office procurement and specific user needs. While major manufacturers dominate in terms of global reach and technological investment, smaller brands prevent full consolidation by catering to localised demand and price-sensitive customers.

Key Industry Developments

- On 1 December 2025, CASIO COMPUTER CO., LTD. announced the launch of 25 new desktop calculators, introducing expanded colour palettes, updated aesthetics, and refined textures to celebrate the 60th anniversary of its electronic desktop calculator business. The new lineup covering compact, mini-desk, and stylish metal-finish variants aims to enhance user personalisation while maintaining practicality. This product expansion reinforces Casio’s strategic focus on design differentiation and lifestyle-driven calculator offerings within the desktop calculator segment.

- On April 15, 2025, Casio Computer Co., Ltd. launched commemorative desktop calculator models under the MS-20UC-J series featuring traditional Japanese patterns, alongside the new Comfy JT-200T design calculator with simplified layout, relocated solar panel, recycled materials, and enhanced usability. Marking the 60th anniversary of Casio calculators, this release highlights product diversification through cultural aesthetics and sustainability-focused innovations within the desktop calculator segment.

Companies Covered in Desktop Calculator Market

- Casio Computer Co. Ltd

- Canon USA Inc.

- Citizen Systems

- Sunway Electronics Company

- Ultmost Technology Group

- Hewlett Packard Development Company

- Orpat Group

- Flair Calculators

- Liquidware Labs, Inc.

- Sharp Electronics Corporation

- Claro Calculators

- Desmos

Frequently Asked Questions

The global Desktop Calculator Market is projected to be valued at US$ 1.8 Bn in 2026.

The Basic Functional Calculators segment is expected to account for approximately 44.5% of the global Desktop Calculator Market by Product type in 2026.

The market is expected to witness a CAGR of 5.5% from 2026 to 2033.

The Desktop Calculator Market is driven by rising global educational enrollment with standardised assessment requirements and growing demand in professional services for precise, compliant computational tools.

Key market opportunities in the Desktop Calculator market lie in developing internationally certified calculators for cross-border educational standards and specialised models for the rapidly expanding healthcare sector, requiring precise, compliant computations.

Key players in the Desktop Calculator market include Casio Computer Co., Ltd., Texas Instruments Incorporated, Sharp Corporation, Canon Inc., Hewlett-Packard Company, and Citizen Systems Japan Co., Ltd.