- Industrial Machinery

- Delumper Market

Delumper Market Size, Share, and Growth Forecast, 2026- 2033

Delumper Market by Shaft Processor Type (Single‑shaft processors, Multi‑shaft/others , Twin‑shaft processors), Application (Food processing, Wastewater & sludge, Pharmaceuticals, Chemicals, Mining & minerals, Others), and Regional Analysis for 2026 – 2033

Delumper Market Size and Trends Analysis

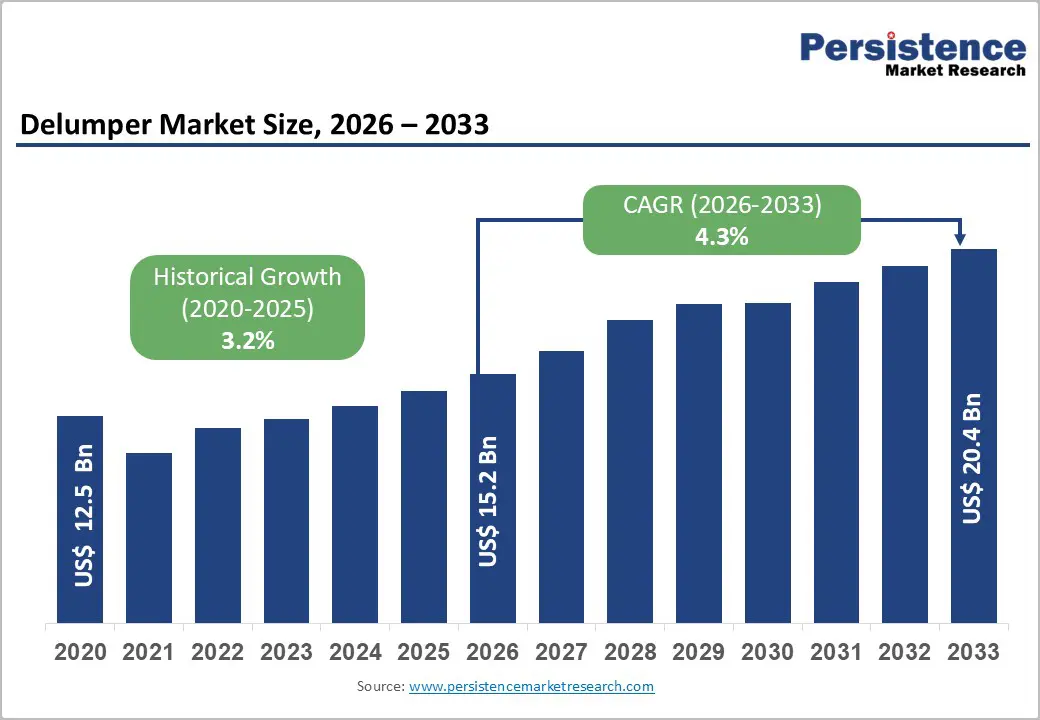

The global delumper market was valued at US$ 15.2 billion in 2026 and is projected to reach US$ 20.4 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033. This growth trajectory builds upon a historical CAGR of 3.2% (2020–2025), reflecting strengthened demand momentum across industrial processing sectors. The market expansion is primarily driven by accelerating industrialization in emerging economies, increasing demand for particle size uniformity in pharmaceutical and food processing applications, and technological advancements in multi-shaft processing systems. Rising investments in infrastructure development and stringent regulatory focus on product quality and environmental compliance further catalyze market growth, positioning delumpers as essential equipment across diverse industrial verticals.

Key Industry Highlights:

- Dominant Processor Technology: Single-shaft processors maintain market leadership with 45%+ revenue share, while multi-shaft and twin-shaft systems represent the fastest-growing segment with 5.1% CAGR, driven by superior processing efficiency and pharmaceutical/specialty chemical adoption.

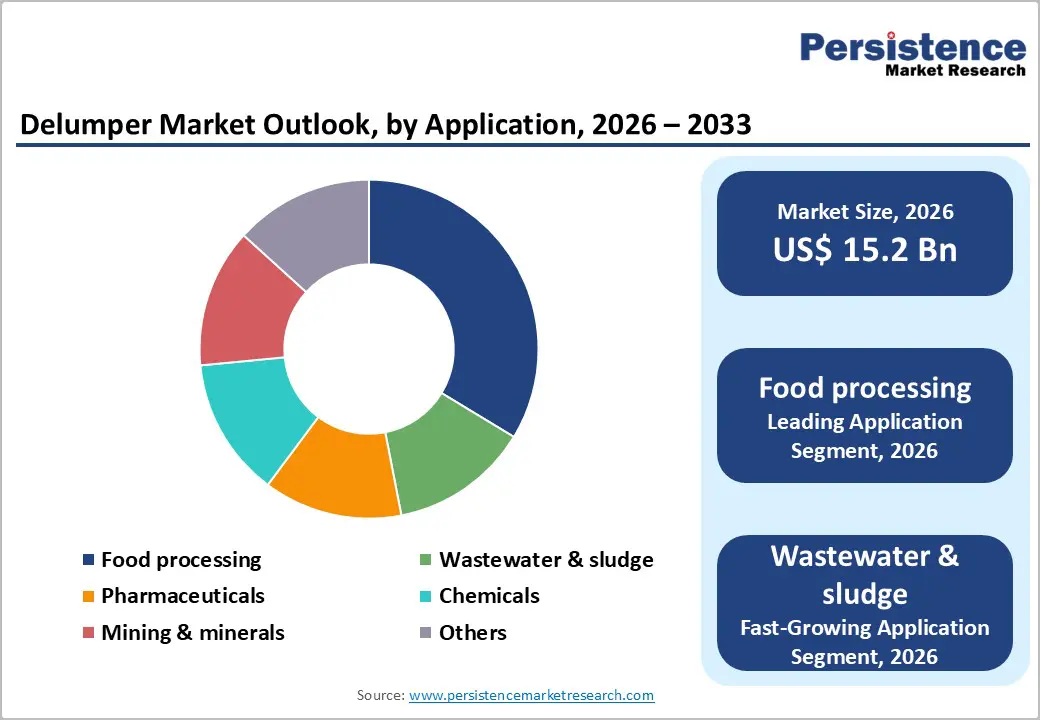

- Leading Application Segment: Food processing dominates with 30%+ revenue share, while wastewater and sludge treatment represents the fastest-growing application at 5.2% CAGR, reflecting environmental regulatory mandates and municipal infrastructure investments.

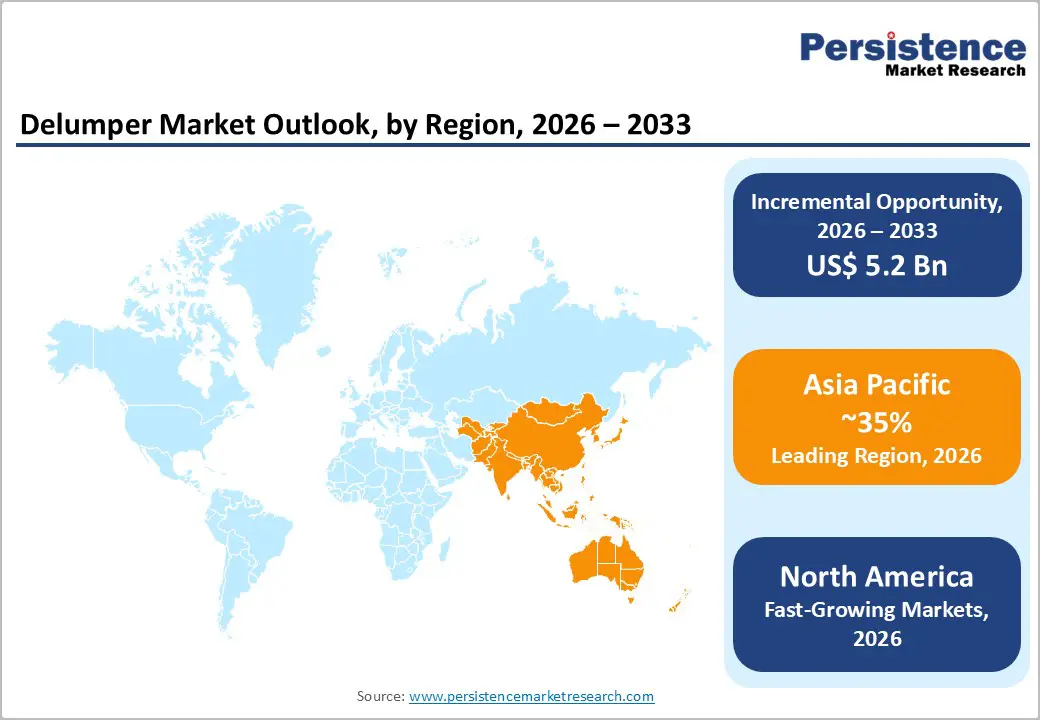

- Regional Market Leadership: Asia-Pacific commands 35%+ global market share and exhibits the strongest growth at 5.3% CAGR, driven by rapid industrialization, pharmaceutical manufacturing expansion, and government infrastructure investments totaling US$ 1.2+ trillion through 2030.

- Technology Innovation Drivers: Multi-shaft processor adoption, IoT integration, predictive maintenance technologies, and energy-efficient designs are creating approximately US$ 2.0 billion market opportunity through 2033, with companies achieving 15–20% pricing premiums through advanced feature integration.

- Strategic Market Developments: Recent product launches (FLSmidth Strike-Bar Crusher, Kason LB 550) and technology partnerships advancing automation integration indicate intensifying competitive differentiation and sustained market expansion through specialized application solutions and digital transformation initiatives.

| Global Market Attributes | Key Insights |

|---|---|

| Delumper Market Size (2026E) | US$ 15.2 Bn |

| Market Value Forecast (2033F) | US$ 20.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.2% |

Market Dynamics

Key Growth Drivers

Technological Innovation in Multi-Shaft Processing Systems

Quantitative Impact: Twin-shaft and multi-shaft processor segments are expected to capture approximately 65% market share during the forecast period, driven by efficiency improvements and superior lump-breaking capacity. Advanced delumper designs incorporate automated control systems, predictive maintenance capabilities through IoT integration, and improved wear-resistant materials that extend equipment lifespan by 30–40%. Manufacturers are investing heavily in R&D, with leading companies allocating 12–15% of revenues to technology development. These innovations enhance processing speeds by 25–35%, reduce maintenance downtime by 20–30%, and minimize energy consumption by 15–20% compared to legacy single-shaft systems. The competitive advantage created through technological differentiation is driving market consolidation and incentivizing adoption of next-generation equipment among cost-conscious industrial operators.

Market Restraining Factors

Regulatory Compliance Complexity and Environmental Standards

Stringent environmental regulations regarding noise emissions, particulate matter control, and wastewater management impose substantial compliance costs on manufacturers and end-users. Equipment retrofitting to meet evolving EU, EPA, and regional environmental standards requires capital reinvestment estimated at 10–15% of equipment value. Regulatory heterogeneity across jurisdictions complicates product standardization and increases manufacturing complexity, with compliance timelines often delaying market entry by 6–12 months. These regulatory burdens disproportionately affect regional manufacturers, creating market consolidation pressures and limiting product innovation velocity in price-sensitive segments.

Delumper Market Trends and Opportunities

Wastewater and Sludge Treatment Expansion

The wastewater treatment segment represents the fastest-growing application category with 5.2% CAGR, driven by global water scarcity and regulatory mandates for municipal wastewater processing. Municipal water authorities and industrial treatment facilities increasingly require efficient sludge delumping to optimize treatment processes and reduce disposal costs. This segment is estimated to expand from US$ 1.8 billion (2026) to US$ 2.6 billion (2033), offering approximately US$ 800 million in incremental opportunity. Government investments in environmental infrastructure, particularly in Asia-Pacific and emerging markets, are creating substantial procurement demand with favorable financing mechanisms and extended procurement cycles supporting market expansion.

Delumper Market Insights and Trends

Shaft Processor Type Insights

Multi-Shaft Innovation Unlocks Next-Generation Delumper Market Growth

The shaft processor landscape presents a clear technology-driven opportunity as industrial users transition from mature, cost-focused systems toward high-performance processing solutions. Single-shaft delumper processors continue to dominate current installations, accounting for over 45% of revenue, due to their affordability, compact footprint, and ease of maintenance. Their 30–40% lower acquisition cost makes them especially attractive for SMEs, retrofit projects, and developing markets, ensuring stable baseline demand. However, modest growth rates of 2.8–3.2% reflect increasing commoditization and limited scope for performance differentiation, signaling saturation in traditional applications such as basic food processing, chemicals, and minerals.

In contrast, multi-shaft and twin-shaft processors represent a high-value growth opportunity. Growing at a 5.1% CAGR, these systems address rising industry requirements for precision, throughput, and energy efficiency. Their ability to process larger feed sizes while achieving tighter particle size control directly supports premium applications in pharmaceuticals, specialty chemicals, and high-precision food processing. Although capital costs are higher, gains of 40–50% in throughput and 30–35% in energy efficiency deliver compelling lifecycle economics. Accelerating adoption across North America, Western Europe, and advanced Asia-Pacific manufacturing hubs positions multi-shaft technologies as the primary driver of future market expansion, with strong potential to redefine competitive differentiation by 2033.

Application Insights

Food and Wastewater Applications Driving Delumper Market Opportunities

The delumper market presents a strong opportunity landscape, led by food processing and wastewater & sludge treatment applications, which together combine revenue stability with high-growth potential. Food processing remains the largest application, accounting for over 30% of total market revenue, supported by steady demand for uniform particle sizing in flour milling, sugar processing, spice grinding, and ingredient blending. Delumpers play a critical role in improving production efficiency, minimizing contamination risks, and supporting just-in-time inventory practices. Stringent global food safety regulations related to hygiene, contamination control, and product consistency continue to drive capital investments in reliable size-reduction equipment. The resilience of food consumption demand across economic cycles and its broad geographic footprint across developed and emerging economies ensure sustained growth and predictable cash flows for manufacturers.

At the same time, wastewater and sludge treatment is emerging as the fastest-growing application, expanding at over 5% CAGR. Rapid urbanization, rising wastewater volumes, and tightening environmental regulations are increasing the need for efficient sludge handling and processing solutions. Delumpers enhance treatment efficiency, reduce downstream equipment wear, and lower sludge disposal costs, making them essential in modern treatment plants. Government infrastructure spending, public-private partnerships, and regulatory mandates for nutrient recovery and biosolids utilization further strengthen long-term growth prospects, positioning wastewater applications as a key future opportunity segment.

Regional Insights and Trends

Asia-Pacific Delumper Market: Scalable Manufacturing and Localization Opportunity

Asia-Pacific represents a compelling growth opportunity in the global delumper market, underpinned by its dominant revenue share of over 35% and its role in contributing nearly 60% of incremental global growth through 2033. The region’s rapid industrialization, infrastructure expansion, and manufacturing localization initiatives are creating sustained, multi-sector demand for bulk material size-reduction equipment. China anchors regional demand, supported by large-scale manufacturing capacity additions and policy-driven localization under industrial modernization programs, which favor domestically produced processing equipment. India presents a particularly attractive opportunity, as its expanding pharmaceutical manufacturing base—accounting for 12–15% of global output—drives consistent delumper adoption across APIs, excipients, and bulk solids handling applications.

Meanwhile, Japan offers opportunities in premium and automated delumper systems, aligned with its advanced manufacturing standards and focus on process efficiency. High-growth ASEAN economies, supported by rising foreign direct investment and industrial park development, further broaden the addressable market. Structural advantages such as competitive labor costs, skilled technical workforces, and government-backed incentives encourage local manufacturing and assembly of equipment. While capital constraints and regulatory diversity pose entry challenges for global suppliers, these same factors create opportunities for regional manufacturers and partnerships. Additionally, tightening environmental and efficiency regulations are accelerating replacement demand, favoring suppliers offering energy-efficient, high-throughput delumper solutions.

North America Delumper Market Opportunity Driven by Regulation, Modernization, and Capital Investment

North America represents a high-value growth opportunity for delumper manufacturers, combining strong market scale, regulatory pull, and sustained capital investment cycles. The region accounts for roughly 25–27% of global delumper revenue, valued at US$ 3.8–4.1 billion in 2026, with expansion projected to US$ 5.2–5.5 billion by 2033, making it the fastest-growing regional market at a 5.3% CAGR. Growth is underpinned by the revival of U.S. manufacturing, supported by federal infrastructure and semiconductor investments, which are accelerating capacity additions in pharmaceuticals, specialty chemicals, and food processing.

Stringent compliance requirements from the U.S. Environmental Protection Agency and the U.S. Food and Drug Administration are pushing end users toward high-precision delumpers with advanced particle control, contamination prevention, and emissions compliance, enabling premium pricing and technology differentiation. Facility modernization across mature industrial hubs such as Michigan, Ohio, Texas, and California further supports repeat equipment replacement cycles.

From a competitive and investment perspective, the presence of established suppliers like Franklin Miller and Stedman Machine Company, combined with robust service networks, reduces adoption risk for buyers. Additionally, US$ 8–10 billion in annual modernization spending across food and pharmaceutical processing creates sustained, long-term demand for advanced delumping solutions.

Delumper Market Competitive Landscape

The delumper market exhibits moderately fragmented characteristics with the top 5–7 companies controlling approximately 35–40% of global market revenue. Franklin Miller, Stedman Machine Company, Quadro Engineering, and regional specialists maintain significant market positions. Fragmentation reflects diverse regional preferences, application-specific requirements, and significant opportunities for regional manufacturers to develop specialized solutions. Mid-tier companies with strong engineering capabilities and regional distribution networks capture approximately 30–35% market share, while numerous smaller regional suppliers serve localized customer bases. This market structure supports innovation through niche specialization while creating consolidation opportunities for companies capable of building pan-regional distribution and technology platforms.

Key Industry Developments

- In June 2024, FLSmidth introduced its advanced Strike-Bar impact crusher designed for high-silica content materials with enhanced wear resistance and reduced maintenance requirements.

- In 2024, Kason Corporation expanded its delumper portfolio with the LB 550 model, capable of processing lumps up to 250mm into 2mm particles at rates of 2–25 TPH with minimal heat generation.

Companies Covered in Delumper Market

- Schutte Hammermill

- Bepex International

- Prab Inc.

- Palamatic Process

- Munson Machinery

- LumpMaster

- Atlantic Coast Crushers

- Stedman Machine Company

- Komar Industries

- Cumberland

- Other Market Players

Frequently Asked Questions

The Delumper market is estimated to be valued at US$ 15.2 Bn in 2026.

The primary demand driver for the delumper market is the need for consistent particle size control to meet stringent regulatory, quality, and process efficiency requirements across industrial manufacturing.

In 2026, the Asia Pacific region will dominate the market with an exceeding 35% revenue share in the global Delumper market.

Among applications, food processing has the highest preference, capturing beyond 30% of the market revenue share in 2026, surpassing other applications.

Schutte Hammermill, Bepex International,Prab Inc., Palamatic Process, Munson Machinery, LumpMaster, and Atlantic Coast Crushers. There are a few leading players in the Delumper market.