- Hardware & Software IT Services

- Data Center Cooling Market

Data Center Cooling Market Size, Share, and Growth Forecast, 2026 - 2033

Data Center Cooling Market by Component (Solution, Services), Technology (Air Cooling, Liquid Cooling, Hybrid Cooling), Data Center Size (Small and Medium-sized Data Centers, Large Data Centers), End-user (Cloud Providers, Colocation Providers, Enterprises, Hyperscale Data Centers) and Regional Analysis for 2026 - 2033

Data Center Cooling Market Size and Trends

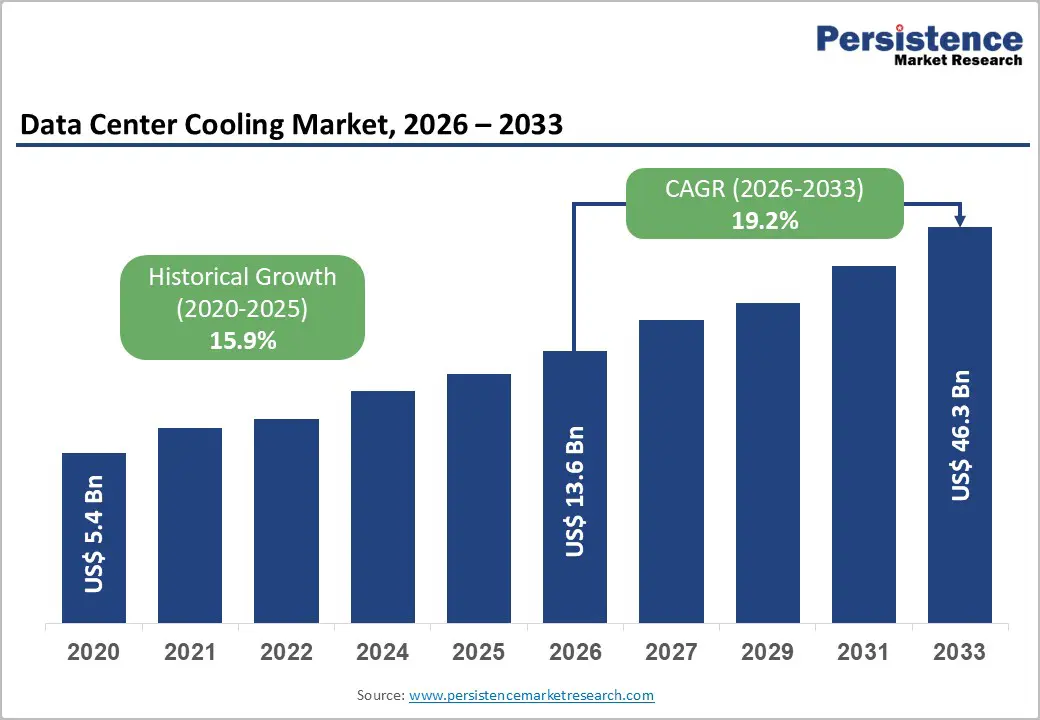

The global data center cooling market size is projected to rise from US$13.6 Bn in 2026 to US$46.3 Bn by 2033. It is anticipated to witness a CAGR of 19.2% during the forecast period from 2026 to 2033, driven by a structural shift toward high-density computing, the rapid rollout of AI and high-performance computing (HPC) workloads, and rising regulatory and investor pressure to reduce energy intensity and carbon emissions across data center portfolios.

Traditional air-based cooling architectures are increasingly unable to handle rack densities exceeding 20–30 kW, prompting operators to deploy advanced strategies such as liquid cooling, hybrid systems, and AI-driven precision control to maintain uptime while lowering Power Usage Effectiveness (PUE).

Key Industry Highlights:

- Leading Component: Solutions dominate with over 74% market share in 2026, valued at more than US$ 10.1 Bn, driven by the need for integrated cooling infrastructure, such as CRAC/CRAH systems, liquid-cooling loops, and containment solutions, to support high-density AI workloads. Services are the fastest-growing, driven by rising demand for predictive maintenance, lifecycle management, and the optimization of complex hybrid cooling systems.

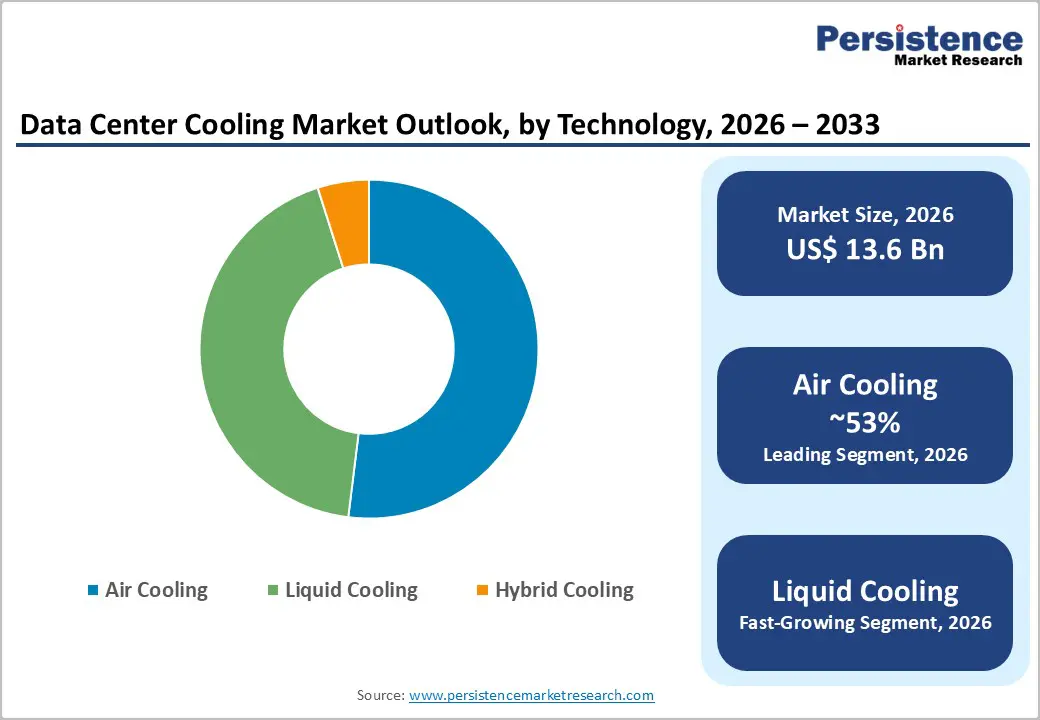

- Leading Technology: Air cooling holds over 53% share in 2026, valued at more than US$ 7.2 Bn, due to its cost-effectiveness, ease of deployment, and compatibility with existing infrastructure. Liquid cooling is the fastest-growing technology, driven by increasing rack densities and AI workloads, offering superior heat dissipation and energy efficiency, and the market is projected to grow from US$ 5.7 Bn in 2026 to US$ 29.2 Bn by 2033 at a CAGR of 26.4%.

- Leading Data Center Size: Large data centers command over 58% of the market in 2026, valued at more than US$ 7.9 Bn, driven by massive IT loads, scalability needs, and energy optimization requirements. Small and medium-sized data centers are expanding at a CAGR of 25.4%, supported by the rise of edge computing and demand for modular, energy-efficient cooling solutions.

- Leading End-user: Hyperscale data centers lead with over 35% share in 2026, valued at more than US$ 4.8 Bn, driven by exponential growth in AI, cloud computing, and big data workloads. Cloud providers are the fastest-growing segment, driven by rising enterprise cloud adoption, SaaS demand, and global digital transformation.

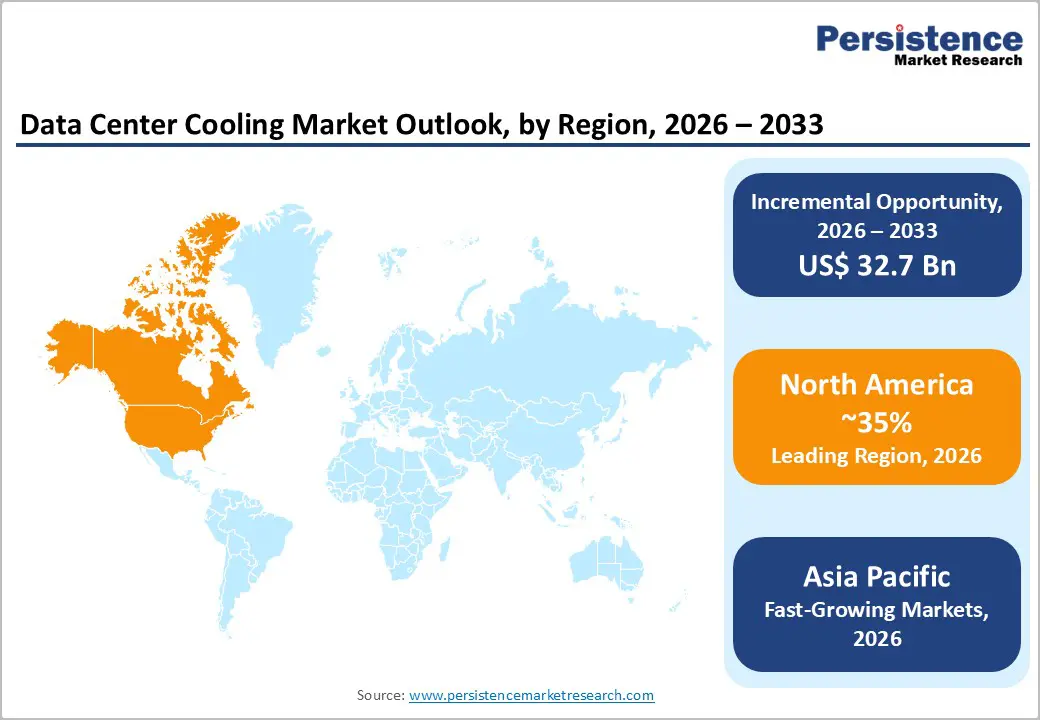

- Leading Region: North America leads with over 36% share in 2026, valued at US$ 4.9 Bn, supported by a strong hyperscale ecosystem, high AI adoption, and regulatory backing for energy efficiency. Asia Pacific is the fastest-growing region with a CAGR of 24.6%, driven by rapid digitalization, increasing data center electricity demand, and strong expansion in countries such as China, India, and Singapore.

| Key Insights | Details |

|---|---|

|

Data Center Cooling Market Size (2026E) |

US$13.6 Bn |

|

Market Value Forecast (2033F) |

US$46.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

19.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

15.9% |

Market Dynamics

Driver - Surge in AI-driven High-Density Computing and Rack Power

The rapid adoption of generative AI, large-scale machine learning, and HPC workloads is pushing rack power densities from single-digit kilowatts to 50–100 kW and beyond, a level that conventional air conditioning systems cannot manage efficiently without significant overdesign or oversizing. According to a study, GPU-based AI servers generate more than 1,200 W per accelerator under full load, requiring thermal management solutions that reject heat at much higher rates than traditional Computer Room Air Conditioners (CRACs). Direct-to-chip liquid cooling, immersion cooling, and hybrid air-liquid architectures are becoming standard design choices in hyperscale and specialized AI data centers, thereby expanding the Data Center Cooling Market.

Escalating Energy Efficiency Regulations and Net-Zero Commitments

Stringent government and industry-level sustainability mandates are compelling data center operators to adopt advanced cooling systems that deliver substantially lower Power Usage Effectiveness (PUE). The European Union's Energy Efficiency Directive (EED) and the European Green Deal mandate continuous improvements in data center energy performance, while the U.S. Department of Energy (DOE) has set targets to reduce federal data center energy consumption. Liquid cooling systems consistently achieve PUEs below 1.2, compared to 1.4–1.6 for traditional air-cooled facilities, resulting in energy savings of 30–40% in cooling-related expenses. In Scandinavia, data center heat reuse has become a policy requirement in urban zones, further accelerating the adoption of liquid-cooling infrastructure that enables waste heat recovery and district heating integration, driving long-term, policy-backed demand for the market.

Restraint - High Capital Expenditure and Complex Retrofitting of Legacy Facilities

Deploying direct-to-chip or immersion cooling systems requires specialized components, including intricate piping networks and heat-rejection systems, which are significantly more expensive than standard CRAC units. Retrofitting existing air-designed facilities poses severe logistical and financial challenges, as data centers must maintain operational continuity during transitions. According to a study, full liquid-cooling infrastructure increases upfront capital costs by 20–40% compared to conventional air systems, yet delivers ROI within 2–4 years through operational savings. This cost barrier particularly restricts adoption among small and medium-sized enterprises, creating a bifurcated market landscape.

Coolant Leakage Risks and Operational Complexity

The introduction of liquid into server environments introduces non-trivial operational risks, particularly leakage, that present a significant restraint on market expansion. Data center operators, especially those managing colocation and enterprise facilities that house multi-tenant hardware, exercise considerable caution when adopting liquid cooling due to liability risks arising from coolant contact with sensitive electronics. The complexity of managing dielectric fluids, ensuring regulatory compliance on fluid composition, and training facility staff for liquid-cooled environments adds to the total operational burden. These operational risks and knowledge gaps slow the transition from pilot deployments to full-scale production adoption, particularly in geographies with limited technical expertise.

Opportunity - AI-Driven Thermal Management and Immersion Cooling Emerging as Commercial Opportunity

New-generation Coolant Distribution Units (CDUs) are being commercialized with onboard inference chips that predict thermal spikes based on workload scheduling, reducing pump energy use by up to 20% compared to reactive cooling systems. Single-phase and two-phase immersion cooling technologies, once confined to pilot deployments, are transitioning to full commercial production, especially in Asia-Pacific and edge data center environments.

Vendors offering modular, self-contained immersion-cooling pods capable of accommodating rack densities of 100–140 kW without requiring facility-wide replumbing are particularly well positioned. Companies partnering with GPU architects such as NVIDIA and Advanced Micro Devices (AMD) on co-engineered reference cooling designs, similar to collaborations with Schneider Electric and Vertiv Group Corp., are well-positioned to benefit from strong alignment with demand, as these integrations increase their likelihood of adoption in large-scale AI infrastructure deployments globally.

Heat Recovery and Circular Energy Business Models

The concept of heat recovery from data center cooling loops is gaining traction as operators and municipalities look to repurpose waste heat for district heating, industrial processes, or agricultural applications. Several large data center campuses in Northern Europe and Canada have already implemented heat recovery heat exchangers and thermal byproduct networks that route warm water from chiller circuits into nearby homes, offices, or greenhouses, effectively turning cooling-related energy loss into revenue-generating thermal output.

The properly configured heat recovery systems recover 70–80% of the heat energy rejected by cooling infrastructure, provided specific climatic and grid planning conditions are met. For cooling equipment vendors, this shift opens opportunities to participate in circular energy business models, energy sharing partnerships, and public-private infrastructure consortia that treat data center cooling not just as a cost center but as a dual-purpose thermal management asset.

Category-wise Analysis

Component Insights

Solution component dominates, capturing more than 74% share in 2026 with a value exceeding US$ 10.1 Bn, due to the critical need for integrated, high-performance cooling infrastructure in modern data centers. Operators require end-to-end systems, such as CRAC/CRAH units, liquid-cooling loops, and containment solutions, to handle rising rack densities. The rapid expansion of AI workloads and hyperscale facilities has intensified demand for efficient thermal management systems that ensure uptime and reduce energy consumption. These solutions also enable scalability and modular deployment, aligning with evolving infrastructure needs.

Services are expected to grow significantly as cooling environments become increasingly complex, and the need for continuous optimization intensifies. With the rise of hybrid cooling technologies, skilled expertise is required for integration and performance tuning. Predictive maintenance and remote monitoring services are gaining traction to minimize downtime risks. Lifecycle management and retrofitting services are becoming essential as older facilities upgrade to modern cooling systems.

Technology Insights

Air cooling holds over 53% market share in 2026, with a value exceeding US$ 7.2 Bn, driven by its widespread adoption, cost-effectiveness, and established compatibility with existing infrastructure. Many existing data centers continue to rely on air-based systems because they are easier to deploy and maintain. Air cooling meets the needs of facilities with moderate power densities and offers flexibility for retrofitting legacy systems. It also benefits from continuous innovation, such as hot- and cold-aisle containment and free-cooling techniques. The familiarity and lower upfront investment make it a preferred choice for many operators.

Liquid cooling is expected to grow at the highest rate due to the urgent need to support high-density computing environments such as AI, machine learning, and high-performance computing workloads. It offers superior heat dissipation, improved energy efficiency, and reduced physical footprint. It also aligns with sustainability goals by lowering power usage effectiveness (PUE). As chip-level cooling becomes essential, adoption is accelerating across hyperscale and advanced enterprise facilities. The global data center liquid-cooling market is projected to grow at a CAGR of 26.4% by 2033.

Data Center Size Insights

Large Data Centers command the largest market share at over 58% in 2026, with a value exceeding US$ 7.9 Bn. These facilities host extensive IT loads, necessitating robust and scalable cooling systems to maintain operational stability. The need for redundancy, energy optimization, and compliance with environmental standards further drives investment in advanced cooling technologies. It also benefits from economies of scale, enabling the deployment of innovative cooling architectures.

Small and Medium-sized Data Centers are expected to grow at a positive CAGR due to the rising adoption of edge computing and localized data processing. Businesses increasingly require low-latency infrastructure closer to end users, fueling the development of smaller facilities. These data centers need compact, energy-efficient, and easy-to-deploy cooling solutions. Modular and prefabricated cooling systems are gaining popularity in this segment. Digital transformation among SMEs is accelerating demand for cost-effective and scalable cooling technologies.

End-user Insights

Hyperscale data centers held over 35% share in 2026, with a value exceeding US$ 4.8 Bn, driven by the exponential growth of cloud computing, AI workloads, and big data analytics. These operators require highly efficient and scalable cooling systems to manage extreme power densities. Continuous infrastructure expansion and the need to optimize operational costs are key drivers of advanced cooling adoption. Hyperscale players also prioritize sustainability, driving the adoption of innovative cooling technologies, such as liquid and immersion cooling. Their massive energy consumption makes efficient thermal management a strategic necessity.

Cloud providers are expected to grow rapidly as global reliance on digital services, SaaS platforms, and remote computing increases. As enterprises migrate workloads to the cloud, providers must expand their infrastructure footprint, increasing cooling requirements. The need for high availability and performance drives investment in efficient and resilient cooling systems. Cloud providers are also adopting green data center initiatives, accelerating demand for energy-efficient cooling technologies. Their rapid scaling strategies and distributed architectures further contribute to sustained growth in cooling solutions.

Regional Insights

North America Data Center Cooling Market Trends

North America holds over 36% share in 2026, reaching US$ 4.9 Bn value, driven by a high concentration of hyperscale and AI-driven infrastructure. The United States accounts for over 4% of global data center electricity consumption, reaching approximately 183 TWh in 2024. Northern Virginia, the world’s largest data center hub with over 4,000 MW of operational and pipeline capacity, continues to attract major deployments from AWS, Microsoft, and Google, accelerating the adoption of liquid cooling technologies. Regulatory support, including state-level efficiency mandates and the U.S. Executive Order on Data Center Infrastructure issued in July 2025, is further boosting investments. The presence of key innovators strengthens the region’s leadership in advanced thermal management.

Asia Pacific Data Center Cooling Market Trends

Asia Pacific is expected to grow at a significant CAGR fueled by rapid digitalization, cloud adoption, and AI-driven workloads. China accounts for nearly 25% of global data center electricity consumption, with demand expected to increase by over 170% by 2030. Increasing rack densities, often exceeding 30-100 kW per rack, are accelerating the shift toward liquid-cooling solutions. Countries such as India, Singapore, and South Korea are witnessing strong data center expansion supported by government initiatives and enterprise demand. Singapore’s easing of data center restrictions and India’s adoption of hybrid and adiabatic cooling systems highlight regional adaptation to energy and water constraints, while companies like Chindata continue to advance integrated cooling solutions.

Europe Data Center Cooling Market Trends

Europe is expected to hold more than 26% share by 2026, shaped by stringent sustainability regulations such as the EU Energy Efficiency Directive and the European Green Deal, which enforce strict PUE targets and reporting standards. Germany and the United Kingdom remain key hubs for enterprise and hyperscale investments, while Scandinavia leads in sustainable cooling due to cold climates, renewable energy availability, and district heating integration. France and Spain are advancing low-water and energy-efficient cooling solutions to meet environmental constraints. Regional players such as STULZ GmbH and Rittal are driving innovation in free cooling and economizer-based systems.

Competitive Landscape

The data center cooling market is moderately consolidated, with the top players collectively accounting for approximately 30% - 40% of global revenues in 2025. Market leaders are pursuing aggressive M&A strategies to expand their liquid-cooling portfolios and to pursue R&D collaborations with semiconductor companies. Key differentiators include end-to-end portfolio breadth from chip to chiller, AI-driven thermal management software, and established reference design partnerships with GPU architects. Emerging business models include Cooling-as-a-Service (CaaS), modular prefabricated cooling pods, and AI-powered predictive maintenance platforms.

Key Industry Developments:

- In March 2026, Panasonic Corporation announced the launch of new Coolant Distribution Units (400kW–800kW) and free-cooling chillers (800kW–1,200kW) for generative AI data centers in Europe, with higher-capacity CDUs under development. The move addresses rising heat loads from advanced GPU-driven workloads by enabling hybrid air and liquid cooling, improving energy efficiency, reducing footprint, and supporting sustainable data center operations with low-GWP refrigerants.

- In November 2025, Green Revolution Cooling (GRC) launched the ICEraQ Nano, a compact immersion cooling rack designed for edge data centers and small IT environments. The 10U system delivers up to 13 kW cooling without chilled water, featuring integrated heat exchange, pre-filled dielectric fluid, and simplified maintenance with automated fluid management.

Companies Covered in Data Center Cooling Market

- Schneider Electric

- Vertiv Group Corp.

- DAIKIN INDUSTRIES, Ltd.

- Johnson Controls

- Carrier

- STULZ GMBH

- Rittal

- CoolIT Systems

- Asetek

- LiquidStack

- Green Revolution Cooling

- DCX Liquid Cooling Systems

- Other

Frequently Asked Questions

The global data center cooling market is projected to be valued at US$13.6 Bn in 2026.

The growing need for energy-efficient, sustainable cooling solutions to reduce operational costs and meet environmental regulations are key driver of the market.

The market is expected to witness a CAGR of 19.2% from 2026 to 2033.

AI-driven thermal management systems to handle high-density workloads efficiently & rising investments in green data centers and renewable-powered cooling solutions is creating strong growth opportunities.

Schneider Electric, Vertiv Group Corp., DAIKIN INDUSTRIES, Ltd., Johnson Controls, Carrier, STULZ GMBH, Rittal, CoolIT Systems, Asetek, LiquidStack are among the leading key players.