- Medical Devices

- Cystoscopes Market

Cystoscopes Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Cystoscopes Market by Product (Rigid Cystoscope and Flexible Cystoscope), by Usage (Single-Use Cystoscope and Reusable Cystoscope), by Application (Urology, Gynecology, and Others) by End User (Hospitals, Diagnostic Imaging Centers, Ambulatory Surgery Centers, and Others), and Regional Analysis from 2026 to 2033

Cytoscopes Market Share and Trends Analysis

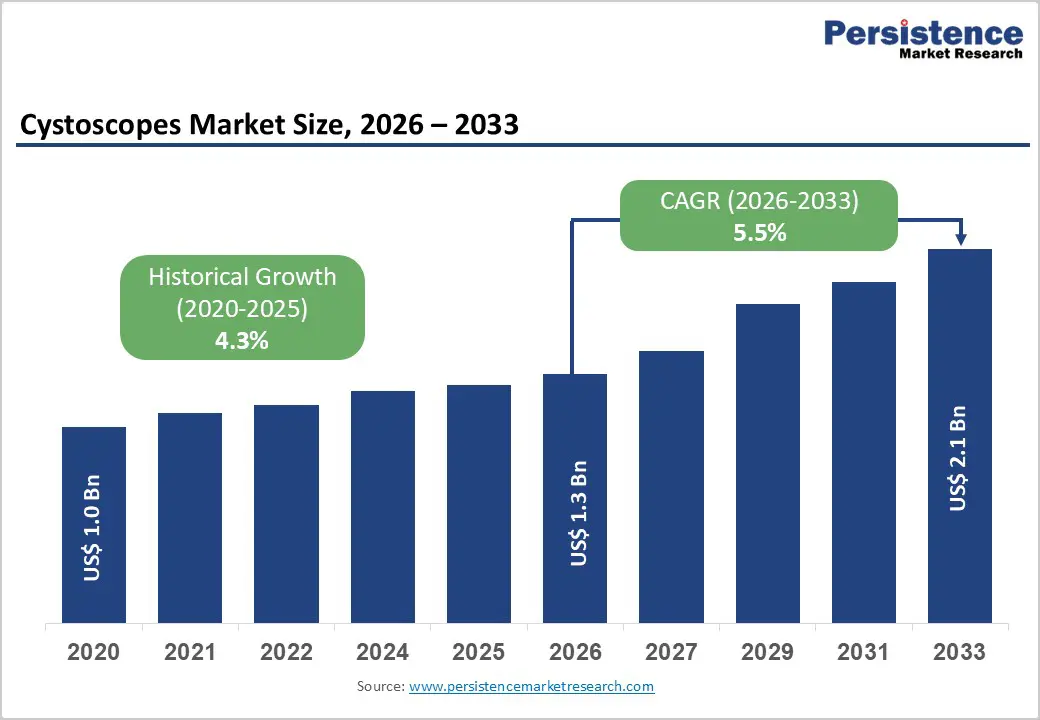

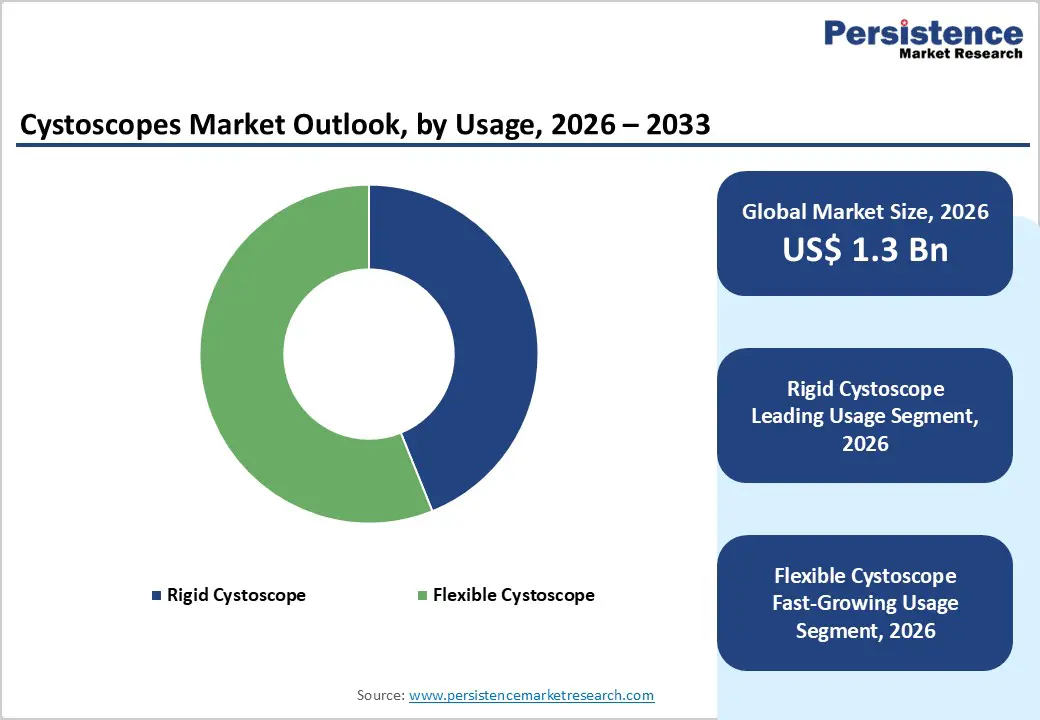

The global cystoscopes market size is estimated to be valued at US$ 1.3 billion in 2026 to US$ 2.1 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033.

The global demand for cystoscopes is rising steadily, driven by the increasing prevalence of urological disorders such as bladder cancer, hematuria, urinary tract infections, benign prostatic hyperplasia, and urolithiasis, alongside growing preference for minimally invasive, infection-controlled diagnostic and therapeutic procedures. Expanding utilization of cystoscopy across hospitals, specialty urology clinics, ambulatory surgical centers, and outpatient facilities is supporting consistent market expansion.

Higher volumes of bladder cancer surveillance procedures, improved clinician awareness regarding early diagnosis, and rising patient preference for less invasive evaluation methods are further accelerating adoption. In addition, increasing healthcare expenditure and improved access to advanced endoscopic imaging platforms are enabling broader penetration across both developed and emerging markets. Continuous innovation in high-definition visualization, scope maneuverability, ergonomic design, and digital integration with hospital information systems is enhancing procedural precision and workflow efficiency.

The growing emphasis on outpatient urology, portable systems, and digitally connected diagnostic pathways is further propelling the global cystoscopes market.

Key Industry Highlights

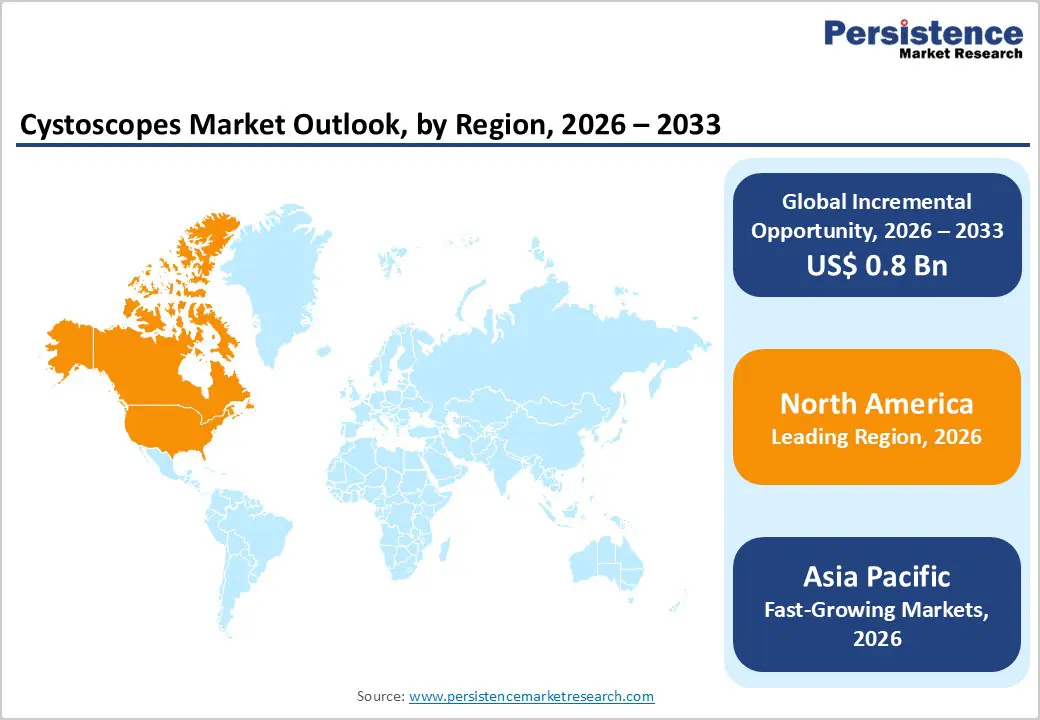

- Leading Region: North America holds the largest share at 46.7%, supported by advanced healthcare infrastructure, high adoption of minimally invasive urological diagnostics, early uptake of digital cystoscopy systems, and strong presence of leading medical device manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to large undiagnosed patient populations, rapid development of tertiary urology centers, improving healthcare access, and rising investments in outpatient and minimally invasive surgical services.

- Leading Product Segment: Rigid cystoscope dominates the market due to extensive utilization in operative urology, superior optical clarity, and strong compatibility with surgical instruments.

- Fastest-Growing Product Segment: Flexible cystoscope is expanding rapidly as demand increases for office-based procedures, enhanced patient comfort, and minimally invasive outpatient diagnostics.

- Leading Application Segment: Urology remains the top application, driven by high global prevalence of bladder cancer and routine cystoscopic surveillance protocols.

- Fastest-Growing Application Segment: Gynecology is scaling quickly as clinical integration of cystoscopy increases in urogynecologic evaluations and minimally invasive pelvic procedures.

| Key Insights | Details |

|---|---|

| Cystoscopes Market Size (2026E) | US$ 1.3 Bn |

| Market Value Forecast (2033F) | US$ 2.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Increasing Incidence of Urological Disorders and Growing Preference for Minimally Invasive Diagnostics

The rising global burden of urological conditions is a primary catalyst accelerating demand for cystoscopic procedures. Bladder cancer, recurrent urinary tract infections, benign prostatic hyperplasia (BPH), urethral strictures, hematuria, and urolithiasis are being diagnosed with greater frequency, particularly among aging populations. Cystoscopy remains the gold-standard modality for direct visualization of the lower urinary tract, making it indispensable for diagnosis, biopsy guidance, tumor resection, and post-treatment surveillance. Growing awareness regarding early detection of bladder malignancies and structured follow-up protocols significantly increases repeat procedure volumes.

Minimally invasive approaches are increasingly preferred over exploratory surgery due to shorter recovery times, reduced complications, and improved patient comfort. Advancements in high-definition imaging, enhanced illumination systems, digital video integration, and improved scope maneuverability have elevated diagnostic precision. Flexible cystoscopes are increasingly adopted in outpatient and office-based settings, while rigid systems remain central to operative interventions. Additionally, expanding ambulatory surgical infrastructure and improved reimbursement pathways in developed healthcare systems are strengthening procedural accessibility. Continuous innovation in ergonomic design, infection-control features, and compatibility with digital documentation platforms further reinforces sustained clinical adoption across hospitals and specialty urology centers worldwide.

Restraints - High Capital Investment and Reprocessing Complexities

Adoption of advanced cystoscopic systems is constrained by financial and operational considerations, particularly in cost-sensitive healthcare environments. High upfront capital expenditure for video cystoscopy towers, digital imaging processors, light sources, and compatible endoscopic instruments can pose barriers for small and mid-sized facilities. Although reusable cystoscopes may reduce per-procedure costs over time, they require dedicated reprocessing infrastructure, including sterilization units, trained personnel, and compliance with stringent infection control protocols. Maintenance expenses, repair costs due to delicate optical components, and downtime during servicing further elevate total ownership costs.

Reprocessing challenges also influence operational efficiency. Strict adherence to sterilization guidelines is critical to prevent cross-contamination, yet improper handling or inadequate disinfection can lead to infection risks and liability concerns. In some regions, limited availability of trained technicians and inconsistent adherence to standardized protocols complicate safe device management. Additionally, reimbursement variability for diagnostic cystoscopy procedures may restrict investment in premium digital systems. Emerging markets often prioritize essential medical equipment over specialized endoscopic platforms, delaying upgrades to advanced technologies. These economic and logistical constraints moderate overall adoption rates despite strong clinical demand and expanding procedural indications globally.

Opportunity - Growth of Disposable Platforms, Office-Based Urology, and Digital Integration

The shift toward infection-controlled, outpatient-centered healthcare delivery models presents substantial opportunities for innovation in cystoscopic technologies. Increasing interest in single-use cystoscopes is driven by heightened focus on cross-contamination prevention, workflow efficiency, and elimination of reprocessing burdens. Disposable platforms are particularly attractive in ambulatory surgical centers and office-based urology practices, where rapid patient turnover and streamlined operations are priorities. As outpatient bladder cancer surveillance and minor therapeutic procedures expand, portable and compact cystoscopy systems are gaining traction.

Digital transformation within healthcare further amplifies growth prospects. Integration of high-resolution imaging with electronic medical records, cloud-based storage, and tele-urology consultations enables real-time documentation and remote specialist collaboration. Enhanced visualization technologies such as narrow-band imaging and improved optical clarity support earlier lesion detection and better clinical outcomes. Emerging economies offer untapped potential as governments invest in tertiary care expansion and cancer screening programs. Increasing physician training initiatives and partnerships between manufacturers and hospital networks are facilitating technology penetration. As healthcare systems emphasize minimally invasive, patient-centric, and data-integrated care pathways, advanced and disposable cystoscopic solutions are well positioned for sustained long-term expansion.

Category-wise Analysis

By Product, Rigid Cystoscope Leads Owing to High Surgical Utilization and Procedural Stability

The rigid cystoscope segment is projected to dominate the global cystoscopes market in 2026, capturing a revenue share of 43.9%. Its leadership is primarily driven by extensive utilization in operative urology procedures, including transurethral resection of bladder tumors (TURBT), stone management, urethral interventions, and biopsy procedures. Rigid cystoscopes provide superior image clarity, enhanced durability, and better instrument channel compatibility, making them particularly suitable for therapeutic applications requiring precision and control.

Hospitals and specialty urology centers prefer rigid systems for high-volume surgical workflows due to their robustness and cost-effectiveness over repeated use. Growing incidence of bladder cancer, benign prostatic hyperplasia (BPH), and urolithiasis further sustains demand. Continuous advancements in optical systems, high-definition imaging, improved illumination, and ergonomic sheath designs enhance procedural efficiency and clinician comfort. The segment’s reliability in complex operative settings and compatibility with a wide range of surgical accessories ensure its continued dominance in the product landscape.

By Application, Urology Dominates Due to High Disease Burden and Routine Diagnostic Surveillance

The urology segment is expected to lead the global cystoscopes market in 2026, accounting for a 69.1% revenue share. This dominance is attributed to the rising global prevalence of bladder cancer, hematuria, recurrent urinary tract infections, urethral strictures, and other lower urinary tract disorders. Cystoscopy remains the gold-standard diagnostic and surveillance tool, particularly for bladder cancer follow-up, which requires repeated and long-term monitoring. Increasing geriatric populations, higher incidence of urological malignancies, and growing awareness of early diagnosis significantly contribute to sustained procedure volumes.

Both flexible and rigid cystoscopes are routinely employed across inpatient and outpatient settings, driving recurring device utilization. Expanding adoption of minimally invasive diagnostic techniques, integration of high-definition video platforms, and improved visualization technologies further enhance clinical accuracy. Rising physician recommendations for early intervention and standardized urological screening protocols reinforce the segment’s leadership across hospitals, specialty clinics, and ambulatory care facilities globally.

By End-user, Hospitals Lead Due to High Procedure Volumes and Advanced Urology Infrastructure

The hospitals segment is projected to dominate the global cystoscopes market in 2026, capturing a 65.5% revenue share. Hospitals account for the majority of cystoscopy procedures due to the presence of dedicated urology departments, advanced surgical infrastructure, and skilled specialists capable of performing both diagnostic and complex therapeutic interventions. High inpatient and outpatient volumes related to bladder cancer, urinary stones, prostate disorders, and hematuria evaluation generate consistent demand for both reusable and single-use cystoscopes.

Long-term procurement contracts and centralized purchasing frameworks further support recurring device utilization. Hospitals also prioritize infection control standards, encouraging gradual adoption of disposable cystoscopes in specific settings. Integration with digital imaging systems, electronic medical records, and advanced visualization platforms enhances procedural efficiency and documentation accuracy. Growing hospital admissions for urological disorders, combined with increasing investments in minimally invasive surgical technologies, ensure the continued dominance of hospitals within the end-user segment.

Regional Insights

North America Cystoscopes Market Trends

North America is expected to dominate the global cystoscopes market in 2026, holding a value share of 46.7%, with the United States contributing the largest portion. The region benefits from a mature healthcare ecosystem, widespread availability of board-certified urologists, and strong adoption of advanced endoscopic imaging technologies. High prevalence of bladder cancer, prostate disorders, and urinary tract diseases drives substantial procedural volumes. Routine bladder cancer surveillance programs and early diagnostic screening further contribute to repeated cystoscopy utilization.

Favorable reimbursement frameworks for minimally invasive procedures encourage hospitals and ambulatory centers to adopt advanced cystoscopic systems, including digital and single-use variants.

The region also demonstrates early integration of high-definition video cystoscopes and portable platforms, supporting outpatient and office-based procedures. Strong presence of leading manufacturers, continuous R&D investment, and strict regulatory compliance standards enhance product innovation and safety. Additionally, increasing emphasis on infection control, outpatient efficiency, and value-based healthcare delivery models sustains long-term market leadership.

Europe Cystoscopes Market Trends

Europe’s cystoscopes market is expected to witness steady growth in 2026, supported by aging demographics and rising incidence of urological cancers and chronic urinary conditions. Countries such as Germany, the U.K., France, Italy, and Nordic nations maintain strong adoption due to established healthcare systems and standardized diagnostic protocols. Bladder cancer surveillance programs and early detection initiatives significantly contribute to recurring cystoscopy procedures. Hospitals and specialty urology clinics increasingly incorporate flexible and digital cystoscopes to improve patient comfort and visualization accuracy.

Regulatory emphasis on infection prevention and medical device safety supports the gradual uptake of single-use systems in select facilities. Technological advancements in optics, illumination systems, and digital documentation platforms enhance workflow efficiency and clinical outcomes. Additionally, supportive reimbursement policies and investments in outpatient infrastructure facilitate procedural growth. Expansion of minimally invasive urological interventions and continuous clinician training programs further reinforce consistent market expansion across the region.

Asia Pacific Cystoscopes Market Trends

The Asia Pacific cystoscopes market is projected to register a higher CAGR of around 8.7% between 2026 and 2033, driven by expanding healthcare infrastructure and rising patient volumes. Large populations in China, India, Japan, and South Korea contribute significantly to procedural growth, particularly as awareness of bladder cancer and urinary tract disorders increases. Improving access to hospital-based diagnostics, growth of private healthcare networks, and broader insurance coverage are accelerating the adoption of minimally invasive urological procedures.

Governments across emerging economies are investing in the modernization of tertiary hospitals and specialty urology centers, supporting advanced endoscopic equipment procurement. Cost-sensitive markets encourage demand for competitively priced, portable, and locally manufactured cystoscopic systems.

Additionally, expansion of ambulatory care models and increasing physician training initiatives improve procedural capacity. Technological improvements in digital imaging, ergonomic scope design, and enhanced maneuverability further strengthen adoption. Strategic expansions by global manufacturers and localized production partnerships position the region for sustained long-term growth.

Competitive Landscape

The global cystoscopes market is highly competitive, with strong participation from Olympus, KARL STORZ SE & Co. KG, Boston Scientific Corporation, Ambu A/S, BD, and Stryker. These companies capitalize on extensive global distribution networks, established brand equity, and continuous innovation in endoscopic imaging, digital visualization platforms, scope maneuverability, and ergonomic design to address diverse urological diagnostic and therapeutic applications.

The increasing incidence of bladder cancer, urinary tract disorders, and growing preference for minimally invasive urological procedures are accelerating technological advancements. Manufacturers are emphasizing high-definition video cystoscopes, single-use disposable systems to reduce cross-contamination risks, improved patient comfort, and seamless integration with hospital IT infrastructure. Strategic collaborations with hospitals, expansion in emerging markets, and sustained R&D investments remain central to delivering advanced, cost-efficient, and clinically optimized cystoscopy solutions.

Key Industry Developments:

- In September 2025, Zenflow, Inc., a medical device innovator focused on advanced urological therapies, announced that it secured 510(k) clearance from the U.S. Food and Drug Administration (FDA) for its Zenflow Spring® Scope & Camera Control Unit (CCU).

- In August 2024, Richard Wolf partnered with Photocure to advance the development of a next-generation flexible PDD (photodynamic diagnosis) cystoscope aimed at improving bladder cancer detection. The collaboration focuses on enhancing fluorescence-guided visualization technology to support more accurate identification of non-muscle invasive bladder tumors during diagnostic and surveillance procedures.

- In January 2024, Boston Scientific initiated a limited market launch of its VersaVue™ single-use flexible cystoscope, broadening its portfolio for the diagnosis and management of urinary tract disorders. The device previously received 510(k) clearance from the U.S. Food and Drug Administration (FDA) in October 2023. VersaVue enables clear visualization of the bladder and urethral lining, supporting image-guided assessment and a range of diagnostic and therapeutic urological procedures.

Companies Covered in Cystoscopes Market

- Olympus

- KARL STORZ SE & Co. KG

- Boston Scientific Corporation

- Ambu A/S

- BD

- Stryker

- Richard Wolf GmbH

- SCHÖLLY Fiberoptic GmbH

- Coloplast Corp

- NeoScope Inc.

- PENTAX Medical

- OTU Medical

- InnoMedicus

- Cook

- Urovision-Urotech

- Others

Frequently Asked Questions

The global cystoscopes market is projected to be valued at US$ 1.3 Bn in 2026.

The market is primarily driven by the rising prevalence of urological disorders such as bladder cancer and UTI, an aging population, and advancements in minimally invasive and high-definition cystoscopy technologies.

The global cystoscopes market is poised to witness a CAGR of 5.5% between 2026 and 2033.

A key opportunity is the expanding adoption of flexible, single-use, AI-enhanced cystoscopes and growth in emerging healthcare markets seeking improved outpatient urological diagnostics.

Olympus, KARL STORZ SE & Co. KG, Boston Scientific Corporation, Ambu A/S, BD, and Stryker are some of the key players in the cystoscopes market.