- Pharmaceuticals

- Cushings Syndrome and Acromegaly Treatment Market

Cushings Syndrome and Acromegaly Treatment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Cushings Syndrome and Acromegaly Treatment Market by Test Type (Adrenal Surgery, Radiation Therapy, Consumables, and Others), by Drug Class (Steroidogenesis Inhibitors, Glucocorticoid Receptor Antagonists, Dopaminergic Agents, and Others), End-user (Hospitals, Specialty Clinics, and Ambulatory Surgery Centers), and Regional Analysis from 2026 to 2033

Cushings Syndrome and Acromegaly Treatment Market Share and Trends Analysis

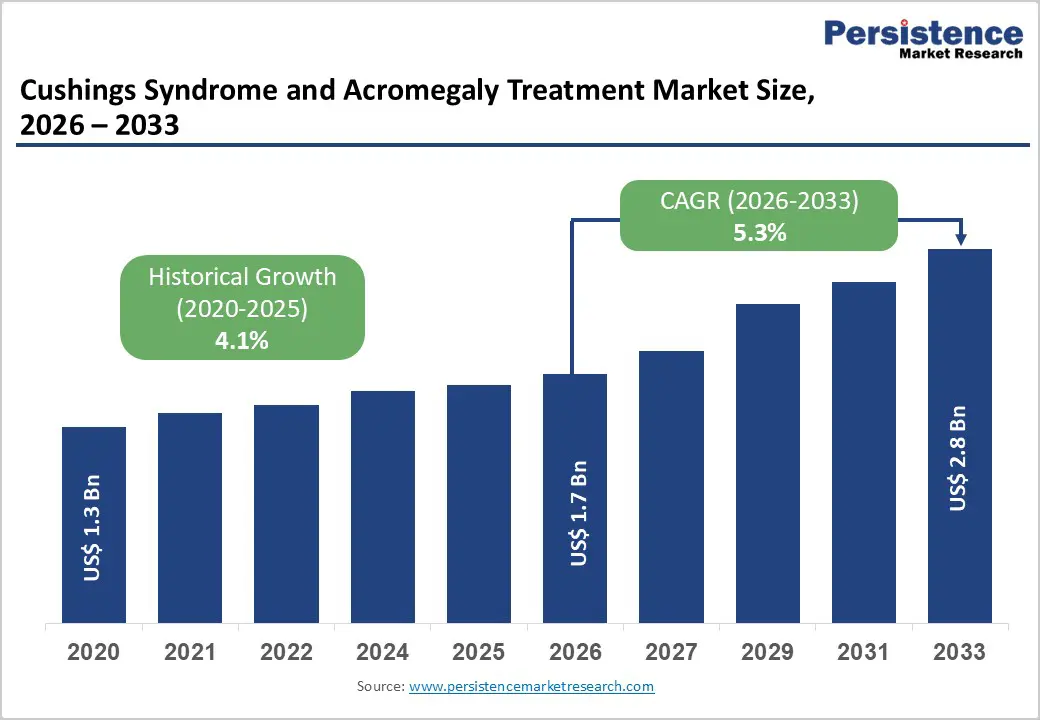

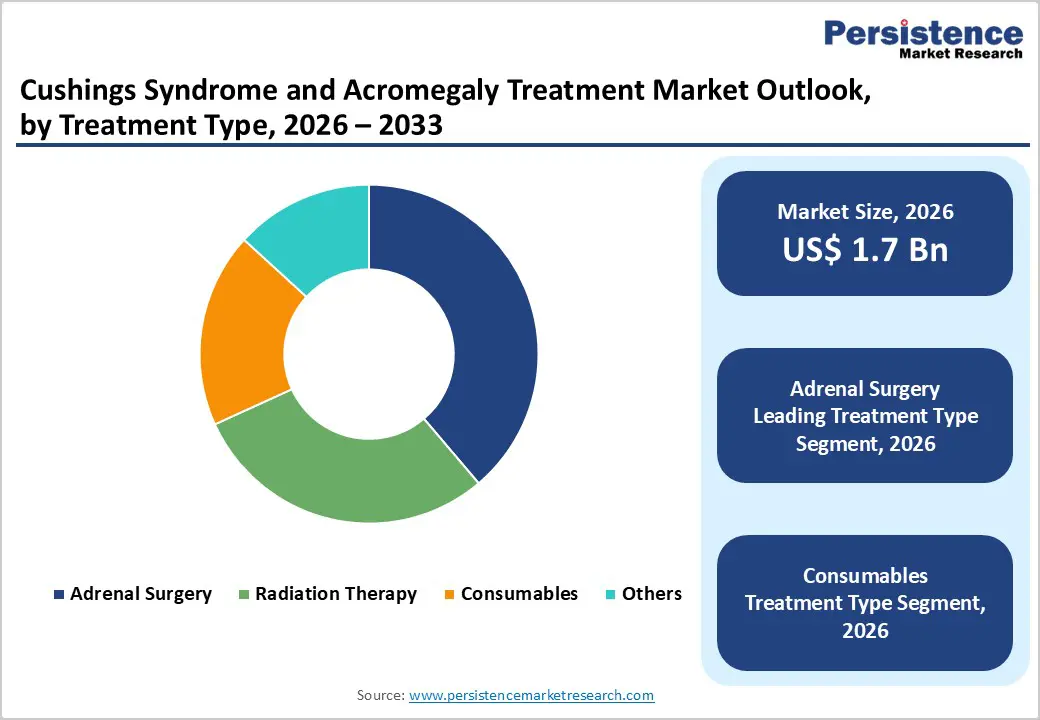

The global cushings syndrome and acromegaly treatment market size is estimated to grow from US$ 1.7 billion in 2026 and projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for Cushing's syndrome and acromegaly treatment is rising rapidly, driven by increasing awareness of endocrine disorders, expanding access to hormonal testing, and growing clinical emphasis on early diagnosis to prevent long-term metabolic and cardiovascular complications. Hospitals and specialty endocrine centers are increasingly utilizing steroidogenesis inhibitors, somatostatin analogs, glucocorticoid receptor antagonists, and targeted pituitary-directed therapies to stabilize hormone levels, control tumor progression, and improve quality of life.

Rise in investments in endocrine-care infrastructure, expansion of pituitary and adrenal surgery programs, and the growth of integrated hormone-disorder management pathways are accelerating global adoption. Continuous advancements in minimally invasive surgical techniques, long-acting injectable formulations, oral cortisol-control therapies, and AI-enabled endocrine monitoring technologies are significantly improving diagnostic precision, treatment continuity, and long-term therapeutic outcomes. Additionally, the growing adoption of guideline-based endocrine protocols, the increasing prevalence of hormone-secreting tumors, and the expanding clinical evidence supporting novel targeted therapeutics are further propelling global market growth.

Key Industry Highlights:

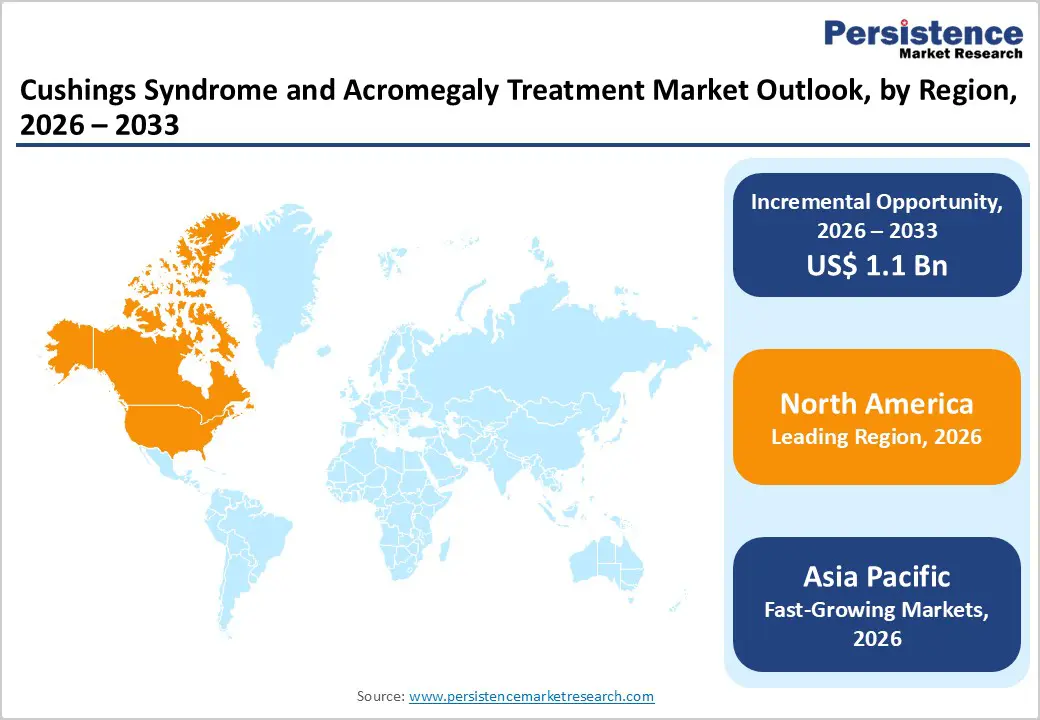

- Leading Region: North America holds the largest share at 44.7%, supported by advanced endocrine-care infrastructure, strong adoption of specialty hormonal therapeutics, high healthcare expenditure, and early access to FDA-approved Cushing’s syndrome and acromegaly treatment technologies.

- Fastest-Growing Region: Asia Pacific is expanding the fastest due to a large undiagnosed patient pool, rapid modernization of endocrine specialty centers, increasing medical tourism, and growing investments in hormone-disorder treatment capacity.

- Leading Treatment Type Segment: Adrenal surgery dominates the market due to its extensive use as a definitive intervention, offering high specificity, long-term biochemical remission, and strong inclusion in global clinical guidelines.

- Fastest-Growing Treatment Type Segment: Consumables grow rapidly as rising prevalence of endocrine disorders supports broader use of oral and non-invasive therapeutic accessories that improve treatment adherence and endocrine monitoring.

- Leading Drug Class Segment: Steroidogenesis inhibitors remain the top segment, driven by increasing use of oral cortisol synthesis blockers, strong preference for non-invasive treatment options, and expanding integration into first-line medical management of hypercortisolism.

- Fastest-Growing Drug Class Segment: Glucocorticoid receptor antagonists are scaling quickly as demand increases for advanced cortisol-modulating therapies, biologic hormone regulators, and hospital-administered options for moderate-to-severe hypercortisolism.

| Key Insights | Details |

|---|---|

| Cushings Syndrome and Acromegaly Treatment Market Size (2026E) | US$ 7.8 Bn |

| Market Value Forecast (2033F) | US$ 12.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Rising Global Prevalence and Therapeutic Advancements in Cushing’s Syndrome and Acromegaly

The global burden of cushings syndrome and acromegaly continues to rise, driven by the growing incidence of ACTH-secreting pituitary adenomas, adrenal neoplasms, and hormone-secreting tumors. Increased longevity, improved endocrine screening, and broader recognition of metabolic and cardiovascular complications are further expanding the identified patient pool. As more individuals undergo hormonal evaluations for nonspecific symptoms such as fatigue, weight gain, hypertension, and glucose abnormalities, clinicians are identifying these disorders earlier and more frequently. This expanding prevalence directly strengthens demand for diagnostic imaging, biochemical assays, long-term pharmacological management, and advanced surgical interventions. The progressive nature of these diseases emphasizes the need for timely therapeutic decision-making, propelling sustained clinical utilization across hospitals, endocrine centers, and specialty practices.

Furthermore, the rising disease prevalence and advancements in targeted hormonal therapeutics are transforming treatment paradigms. The increasing adoption of steroidogenesis inhibitors, somatostatin analogs, and glucocorticoid receptor antagonists has created a robust, diversified therapeutic landscape. These agents offer improved biochemical control, reduced tumor progression risk, and meaningful long-term symptom relief, especially for patients who are inoperable or require adjunctive therapy after surgery. Innovations in long-acting injectable formulations, selective receptor modulators, and combination regimens are enhancing treatment adherence and improving endocrine stability. As evidence supporting targeted therapies grows, clinicians are increasingly integrating personalized approaches to achieve deeper hormonal normalization and better patient outcomes.

Restraints - Economic Burden and Diagnostic Barriers in Cushing’s Syndrome and Acromegaly Management

The high cost associated with specialty therapeutics remains a major barrier to optimal management of Cushing’s syndrome and acromegaly. Somatostatin analogs, steroidogenesis inhibitors, and glucocorticoid receptor antagonists are often required over a longer duration, and in many cases, lifelong administration is necessary to maintain hormonal control. These agents are priced at a premium due to complex manufacturing processes, limited patient populations, and stringent regulatory requirements for rare diseases.

Additionally, many patients require combination therapies, recurrent imaging, routine biochemical monitoring, and periodic dose adjustments, further escalating overall expenditures. The financial burden is especially challenging in regions with limited insurance coverage or out-of-pocket payment systems, frequently resulting in delayed initiation, treatment discontinuation, or suboptimal dosing strategies. Across healthcare systems, high therapeutic cost remains a key restraint that limits broad and equitable access to advanced endocrine treatments.

Moreover, limited awareness and underdiagnosis. Both Cushing’s syndrome and acromegaly present with non-specific symptoms such as weight gain, fatigue, hypertension, menstrual irregularities, and insulin resistance that often mimic common metabolic conditions. As a result, many patients remain undiagnosed for years, progressing to severe comorbidities before receiving appropriate evaluation. Primary-care clinicians may encounter only a few cases in their careers, contributing to delayed referral patterns and missed early diagnostic windows. This under-recognition reduces timely treatment initiation, allowing hormonal excess to continue damaging organ systems. Enhancing clinical awareness, improving screening tools, and integrating standardized diagnostic pathways are essential to counteract these systemic delays and support earlier, outcome-improving interventions.

Opportunity - Therapeutic Innovation and Surgical Advancements Driving Market Expansion

The development of long-acting and oral therapeutics is creating substantial growth momentum in the treatment landscape for cushing’s syndrome and acromegaly. Next-generation formulations of steroidogenesis inhibitors, somatostatin analogs, and cortisol receptor modulators are designed to reduce dosing frequency, minimize the burden of frequent injections, and enhance long-term adherence. Oral therapies, in particular, are gaining strong clinical traction as they offer greater convenience, improved patient compliance, and more flexible dosing strategies suitable for chronic disease management. Long-acting injectables further support consistent biochemical control, lowering fluctuations in hormone levels and reducing the need for intensive follow-up. As pharmaceutical companies expand research into targeted small molecules, receptor-selective agents, and sustained-release delivery systems, treatment regimens are becoming more patient-centric and better aligned with real-world requirements.

Furthermore, the growing adoption of minimally invasive surgical techniques is reshaping clinical outcomes. Transsphenoidal pituitary surgery and laparoscopic adrenalectomy have evolved with improvements in endoscopic visualization, navigation technologies, and microsurgical tools, enabling higher accuracy in tumor localization and removal. These procedures reduce operative trauma, shorten hospital stays, and enhance postoperative recovery, making them preferred first-line interventions for eligible patients. Broader availability of experienced surgical teams and advanced imaging systems is increasing patient access to these procedures globally. As surgical success rates improve and perioperative risks decline, minimally invasive surgery continues to strengthen its role as a cornerstone of definitive treatment and a major driver of market growth.

Category-wise Analysis

By Treatment Type, Adrenal Surgery Dominates Globally Owing to Its Proven Clinical Efficacy and Widespread Use in Hypercortisolism Management

The adrenal surgery segment is projected to dominate the global cushings syndrome and acromegaly treatment market in 2026, accounting for a significant revenue share of 38.8%. This leadership is driven by the widespread clinical use of adrenalectomy as a definitive treatment for adrenal-dependent Cushing’s syndrome, offering rapid and sustained cortisol normalization. Its ability to deliver high cure rates, reduce long-term complications, and provide durable hormone regulation supports broad adoption across tertiary endocrine and surgical centers. Continued advancements in minimally invasive adrenal surgery, increasing availability of laparoscopic and robotic procedures, and strong guideline recommendations further strengthen its clinical appeal. Rising detection of adrenal tumors, expanding surgical infrastructure, and enhanced perioperative safety data continue to reinforce adrenal surgery’s dominant position in global Cushing’s syndrome management.

By Drug Class, Steroidogenesis Inhibitors Dominates Globally Due to High Disease Prevalence and Strong Clinical Focus on Hormonal Control

The steroidogenesis inhibitors segment is projected to dominate the global market in 2026, accounting for a significant revenue share of 36.9%. This dominance stems from the central role of cortisol synthesis inhibitors in managing hypercortisolism across diverse Cushing’s presentations, including pituitary, ectopic, and adrenal forms. Their ability to rapidly suppress excess cortisol production, provide dose flexibility, and support pre- and post-surgical stabilization drives extensive clinical use. Routine endocrine evaluations, strong guideline-supported treatment pathways, and well-established monitoring protocols further support higher adoption rates. Growing patient populations diagnosed through improved imaging, rising incidence of hormone-secreting tumors, and increasing preference for non-invasive medical management reinforce the strong market positioning of steroidogenesis inhibitors.

By End-user, Hospitals Dominate Globally Due to Their Advanced Renal-Care Infrastructure and High Treatment Volume

The hospitals segment is projected to dominate the global cushings syndrome and acromegaly treatment market in 2026, capturing a revenue share of 54.5%. Hospitals particularly tertiary endocrine centers, pituitary specialty units, and academic medical institutions serve as primary hubs for diagnosing and managing complex hormonal disorders due to their ability to conduct advanced biochemical testing, perform adrenal and pituitary surgeries, and administer long-acting injectable therapies.

High patient inflow, availability of multidisciplinary teams including endocrinologists and neurosurgeons, and integration of advanced imaging and interventional technologies contribute to strong hospital-based demand. Additionally, hospitals play a central role in rare-disease screening, hormone regulation management, and clinical trials evaluating next-generation targeted therapies. Their comprehensive capabilities and central role in managing severe endocrine disorders solidify hospitals as the leading end-user segment globally.

Region-wise Insights

North America Cushings Syndrome and Acromegaly Treatment Market Trends

North America is expected to maintain global dominance in the cushings syndrome and acromegaly treatment market with a market share value of 44.7%, supported by its advanced healthcare infrastructure, strong endocrine disease management programs, and widespread adoption of somatostatin analogs, steroidogenesis inhibitors, GH-receptor antagonists, and other targeted hormonal therapies. The U.S. leads the region due to frequent FDA approvals of new endocrine therapeutics, strong presence of leading biopharmaceutical manufacturers, and extensive collaborations between specialty hospitals, pituitary centers, and academic research institutions. Major endocrine networks continuously evaluate improved somatostatin analogs, novel cortisol-modulating drugs, and long-acting injectables, accelerating clinical integration. Rising demand for early diagnosis of pituitary disorders and decentralized specialty care delivery continues to drive investments from large healthcare systems.

The region also benefits from strong reimbursement frameworks for rare endocrine diseases, high clinician preference for long-acting hormonal injectables and advanced cortisol-lowering agents, and expanding adoption of next-generation oral therapies. Increasing investment in specialty clinics, digital endocrinology platforms, and AI-supported hormonal disorder management tools is improving treatment efficiency. Additionally, rising public awareness of pituitary tumor-related complications and expanding neuroendocrinology research hubs continue to strengthen North America’s long-term leadership in the global cushings syndrome and acromegaly treatment market.

Europe Cushings Syndrome and Acromegaly Treatment Market Trends

Europe shows steady and mature adoption of Cushings syndrome and acromegaly treatment solutions, supported by strong public-health frameworks, well-established endocrinology networks, and stringent management guidelines across major markets such as Germany, the U.K., France, Italy, Switzerland, and the Nordic region. Robust epidemiological surveillance systems and consistent clinical validation of new endocrine therapies support the use of somatostatin analogs, steroidogenesis inhibitors, and pituitary-targeted formulations across primary and specialty care.

The region demonstrates high integration of automated drug-delivery systems, standardized endocrine protocols, and evidence-based management pathways aimed at improving hormonal stability and reducing surgical dependency.

Europe’s favorable regulatory environment, emphasis on safety and efficacy, and strong contributions from clinical research centers support the evaluation of next-generation endocrine therapeutics. Growing demand for cost-effective long-acting injectables, improved cortisol-modulating agents, and orally administered pituitary-directed drugs continues to strengthen uptake. Regional pharmaceutical manufacturers are investing in formulation innovation, GMP-compliant production, and resilient supply chains. Government initiatives supporting rare-disease registries, early hormonal disorder screening, and digital treatment monitoring further drive Europe’s overall market growth.

Asia Pacific Cushings Syndrome and Acromegaly Treatment Market Trends

Asia Pacific is projected to be the fastest-growing region for Cushing’s syndrome and acromegaly treatment with a CAGR of 7.6%, driven by rising healthcare expenditure, increasing prevalence of pituitary and adrenal disorders, and rapid expansion of specialty hospitals. Countries such as China, Japan, South Korea, Singapore, and India are increasing the adoption of somatostatin analogs, GH-receptor antagonists, and new cortisol synthesis inhibitors across tertiary hospitals, endocrinology clinics, and government healthcare programs. Growing availability of cost-effective biologics and generic hormonal therapies, combined with strong participation from regional pharmaceutical manufacturers, is improving affordability and expanding access across mid-sized hospitals and community settings.

Government-supported hormonal disorder screening programs, investments in specialty endocrine infrastructure, and partnerships with global biopharma companies for technology transfer are accelerating adoption. The increasing need for early detection of pituitary tumors, streamlined endocrine management, and oral therapy options is driving strong clinical uptake. Endocrinologists across Asia Pacific are increasingly participating in global neuroendocrine research networks, enabling the adoption of advanced therapeutic protocols to reduce disease progression. Expanding private healthcare networks, rising medical tourism, and the growth of specialized endocrine centers continue to support robust market growth across the region.

Competitive Landscape

The global Cushing’s syndrome and acromegaly treatment market is highly competitive, with active participation from Novartis AG, Pfizer, Corcept Therapeutics, Incorporated, Ipsen Biopharmaceuticals, Inc., and Perrigo Company plc. These companies leverage strong endocrinology and rare-disease portfolios, along with established biologics and hormonal therapy capabilities, to expand their presence across hospitals, specialty clinics, and advanced endocrine centers. Rising diagnosis rates and the need for effective hormonal modulators continue to drive the adoption of somatostatin analogs, steroidogenesis inhibitors, and glucocorticoid receptor antagonists.

Manufacturers are prioritizing long-acting somatostatin analogs, next-generation oral therapies, and improved cortisol-modulating agents, while focusing on regulatory approvals, scaled production, and strategic collaborations with healthcare providers to strengthen treatment access and support market expansion.

Key Industry Developments:

- In December 2025, Debiopharm initiated a Phase 3 trial for Debio 4126, a new three-month sustained-release octreotide formulation for acromegaly. The company has begun patient recruitment, aiming to improve convenience and adherence compared to traditional monthly somatostatin analogue injections.

- In May 2025, Crinetics Pharmaceuticals, Inc., reported two presentations at the AACE Annual Meeting. A post-hoc analysis showed its investigational candidate, paltusotine delivered rapid, durable, and well-tolerated effects in surgically naïve acromegaly patients. A second analysis highlighted symptom variability and the substantial disease burden experienced by patients on long-acting injectable somatostatin analogs.

- In September 2025, Crinetics Pharmaceuticals, Inc., received U.S. FDA approval for paltusotine (Palsonify), the first oral, once-daily small-molecule somatostatin analogue for acromegaly, offering a convenient alternative to injectable therapies.

Companies Covered in Cushings Syndrome and Acromegaly Treatment Market

- Novartis AG

- Pfizer

- Corcept Therapeutics, Incorporated

- Ipsen Biopharmaceuticals, Inc.

- Perrigo Company plc,

- ESTEVE

- Crinetics Pharmaceuticals, Inc.

- Sparrow Pharmaceuticals,

- SteroTherapeutics

- Recordati Rare Diseases

- Xeris Pharmaceuticals, Inc.

- Others

Frequently Asked Questions

The global cushings syndrome and acromegaly treatment market is projected to be valued at US$ 1.7 Bn in 2026.

High-growth opportunities emerge from novel drug development, improved long-acting hormonal therapies, and expanding access to specialized endocrine care across emerging markets.

The global cushings syndrome and acromegaly treatment market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Growing uptake of oral HIF-PH inhibitors, emerging CKD patient pools in developing regions, and innovation in long-acting anemia therapeutics are creating opportunities in the market.

Novartis AG, Pfizer, Corcept Therapeutics, Incorporated, Ipsen Biopharmaceuticals, Inc., and Perrigo Company plc., are some of the key players in the cushings syndrome and acromegaly treatment market.