- Medical Devices

- Cryoballoon Ablation System Market

Cryoballoon Ablation System Market Size, Share, and Growth Forecast 2026 - 2033

Cryoballoon Ablation System Market by Product (Cryoballoon catheters, Consoles/generators, Sheaths & accessories), Application (Atrial fibrillation – Paroxysmal AF, Persistent AF, Atrial flutter, Others), End -User (Hospitals, Cardiac centers/specialty clinics, Ambulatory surgical centers), and Regional Analysis for 2026 - 2033

Cryoballoon Ablation System Market Share and Trends Analysis

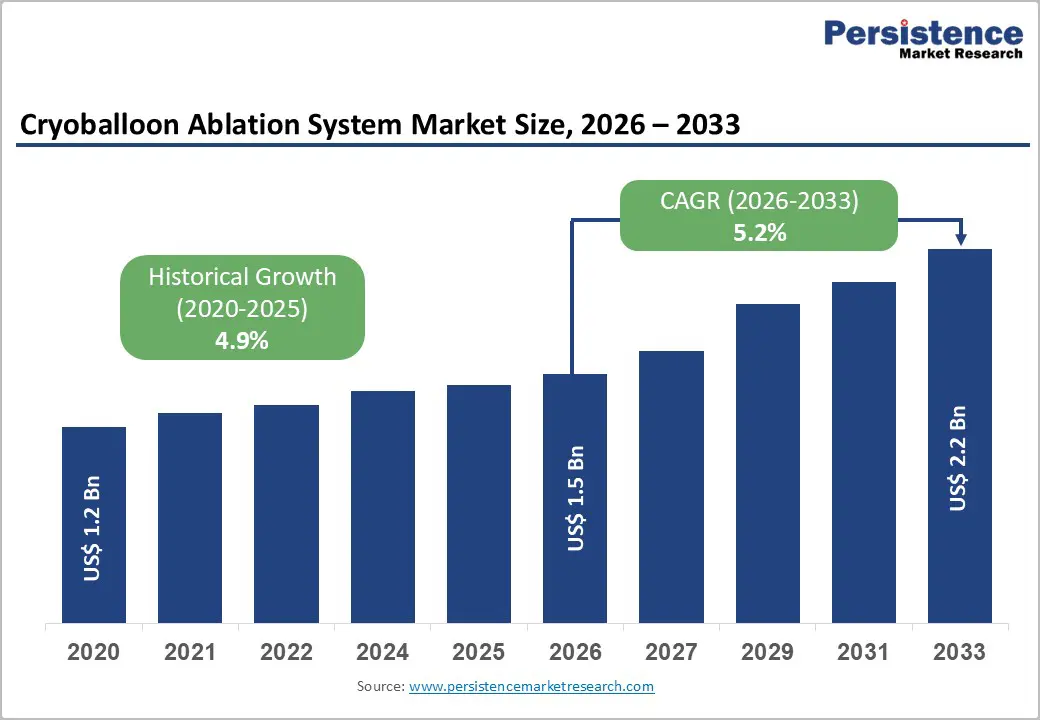

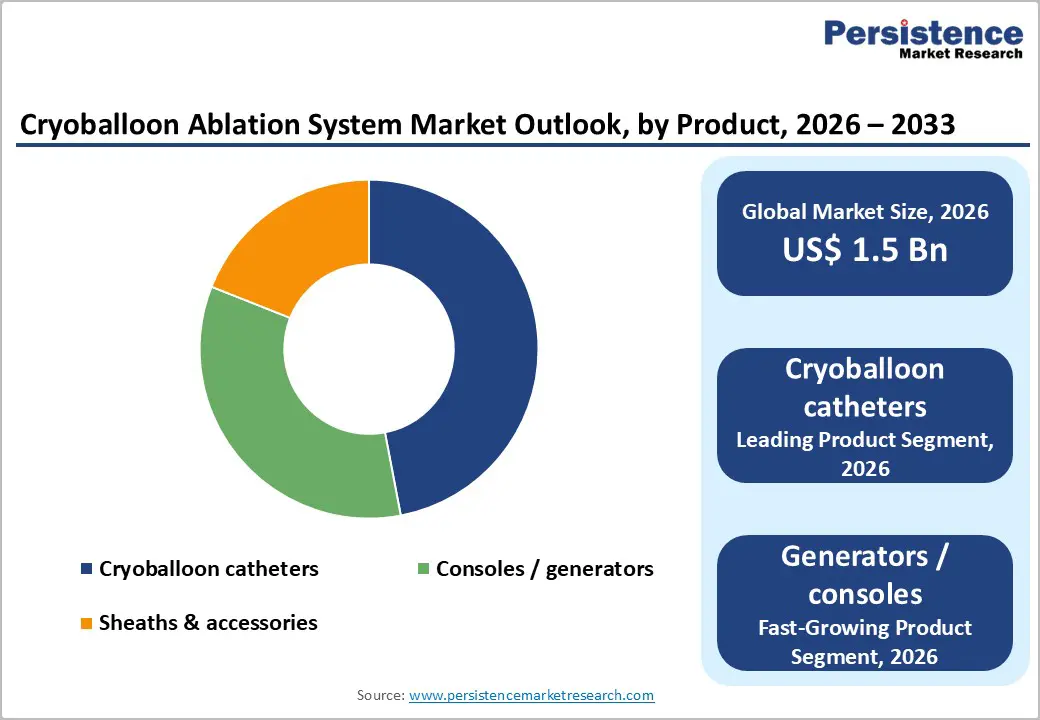

The global cryoballoon ablation system market size is expected to be valued at US$ 1.5 billion in 2026 and projected to reach US$ 2.2 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033. The market outlook is supported by the growing burden of atrial fibrillation, strong clinical evidence favoring catheter ablation, and rapid technology upgrades in cryo-based pulmonary vein isolation systems.

Hospitals across developed markets are increasingly shifting eligible patients from drug-only therapy to early rhythm-control strategies, where cryoballoon-based procedures offer faster case times and reproducible results versus point-by-point radiofrequency (RF) ablation. Together with favorable reimbursement moves and widening electrophysiology (EP) capacity, these factors underpin a steady but durable expansion in global cryoballoon system demand over the forecast period.

Key Market Highlights

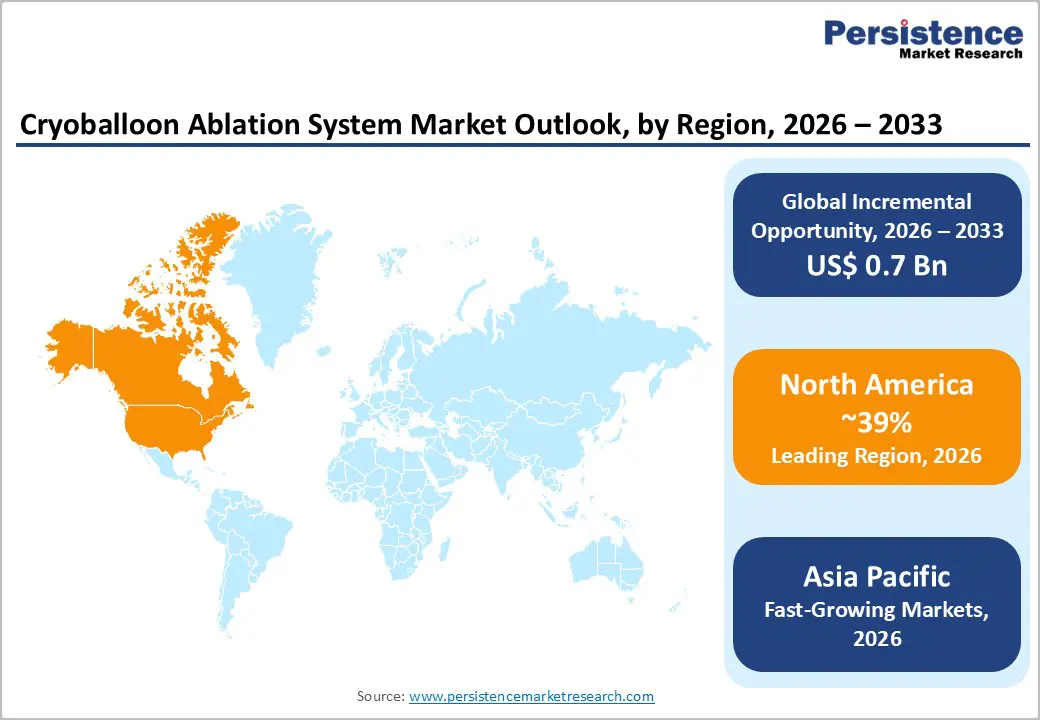

- Leading region: North America leads the cryoballoon ablation system market with about 39% share in 2025, supported by early regulatory approvals, strong EP capacity, and favorable reimbursement for ablation procedures across major U.S. and Canadian centers.

- Fastest-growing region: Asia Pacific is projected to record the highest CAGR for 2025-2032, driven by expanding cardiac infrastructure, rising AF prevalence in China, Japan, India, and ASEAN, and increased adoption of advanced ablation technologies from both global and regional manufacturers.

- Dominant Product: Among products, cryoballoon catheters hold around 47% share in 2025, reflecting their central therapeutic role, robust safety and efficacy evidence from multicenter registries, and continued design upgrades that support consistent pulmonary vein isolation outcomes.

- Fastest-growing Application: Within applications, persistent AF is expected to show the fastest growth, as new trial data and approvals extend cryoballoon use beyond paroxysmal cases and clinicians seek standardized, efficient strategies for more complex AF populations.

- Key opportunity: Expansion of AF ablation into ambulatory and office-based EP settings, underpinned by evolving CMS reimbursement and real-world safety data, offers a substantial opportunity for vendors to deploy more compact, workflow-optimized cryoballoon platforms and reach new provider segments.

| Key Insights | Details |

|---|---|

|

Cryoballoon Ablation System Market Size (2026E) |

US$ 1.5 Bn |

|

Market Value Forecast (2033F) |

US$ 2.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.9% |

Market Dynamics

Drivers - Technological advancements and expanding regulatory approvals

Continuous innovation in cryoballoon technology and a favorable regulatory pipeline significantly reinforce growth. Medtronic’s Arctic Front Advance™ family was among the first cryoballoon platforms to receive FDA and CE Mark approvals for treatment of paroxysmal AF, and subsequent data supported its use earlier in the rhythm-control strategy. In 2023, Boston Scientific secured FDA approval for its POLARx™ Cryoablation System, including an expandable cryoballoon designed to transition between 28 mm and 31 mm, addressing anatomical variability and potentially reducing the need for catheter exchanges. Comparative trials such as FIRE AND ICE and subsequent meta-analyses have shown cryoballoon ablation to be non-inferior to RF with advantages in procedural standardization and often shorter procedure times. Meanwhile, console platforms now integrate refined temperature control, real-time pressure monitoring, and improved catheter feedback, which together enhance safety and repeatability. As more indications (for example, persistent AF) are added and next-generation systems reach more geographies, the addressable market for cryoballoon systems is poised to widen steadily.

Restraints - High capital requirements and procedure costs

Despite its clinical benefits, cryoballoon ablation remains capital- and resource-intensive, limiting adoption in cost-constrained settings. Establishing a full EP lab with mapping, imaging, and cryo console infrastructure can require investments in the high six-figure range in US$, which is challenging for smaller hospitals and centers in emerging markets. Single-use cryoballoon catheters and related disposables add significant per-procedure cost relative to pharmacotherapy and even some RF catheters. Studies in Europe and North America estimate that AF patients accrue thousands of US$ or EUR in incremental annual healthcare expenditures compared with matched controls, and while ablation can reduce the long-term burden, the upfront cost remains a barrier for payers with constrained budgets. Uneven reimbursement policies, delayed tariff updates, and administrative hurdles can further slow adoption, particularly where cost-effectiveness data specific to cryoballoon versus other strategies are still being evaluated.

Competition from alternative ablation and emerging energy modalities

Cryoballoon systems operate in a competitive landscape that includes conventional RF ablation and novel pulsed field ablation (PFA), among other technologies. RF ablation remains widely entrenched due to long operator experience, broad device availability, and flexible lesion creation, especially in complex arrhythmia substrates. More recently, PFA has garnered strong interest for its ultra-rapid energy delivery and tissue selectivity, with early studies suggesting a lower risk of collateral damage to structures such as the esophagus and phrenic nerve. Health systems and operators may prioritize investments in next-wave platforms like PFA, potentially diverting capital from cryoballoon systems in certain centers. Additionally, incremental improvements in antiarrhythmic drugs and rate-control strategies provide non-invasive options for patients who are unwilling or unsuitable for ablation, thereby constraining the ultimate penetration of device-based rhythm control.

Opportunity - Shift toward ambulatory and outpatient electrophysiology settings

The gradual migration of EP procedures from inpatient hospital settings to outpatient or ambulatory facilities represents a major opportunity for cryoballoon system vendors. Professional societies and payers in the U.S. have been exploring pathways for more EP procedures, including AF ablation, to be safely performed in ambulatory surgical centers (ASCs) and office-based labs, driven by the potential for cost savings and efficiency gains. Policy moves from agencies such as CMS to include more EP ablation codes on outpatient or ASC payment schedules are expected to unlock new procedure volumes while relieving pressure on hospital cath-lab capacity. Cryoballoon ablation, with its relatively standardized workflows and single-shot pulmonary vein isolation, is well-suited to streamlined outpatient protocols once centers are appropriately staffed and equipped. As more real-world data support equivalent or favorable safety profiles for selected low-risk patients treated outside hospital settings, EP groups can scale case throughput, creating a strong pull for compact, easy-to-use cryo consoles and optimized catheter-and-sheath ecosystems.

High-growth potential in the Asia Pacific, driven by EP capacity build-out

Asia Pacific is expected to deliver the fastest growth in cryoballoon system demand due to the rapid expansion of EP infrastructure and a rising AF burden in large populations. Countries such as China, Japan, India, and key ASEAN members are investing heavily in cardiovascular care, expanding catheterization labs and training EP specialists to handle growing volumes of complex arrhythmia cases. Studies and local society data indicate that AF and atrial flutter prevalence is rising as lifestyle risk factors and longevity increase, yet procedure rates per capita remain below those of North America and Western Europe, pointing to significant latent demand. Regional ablation markets for AF and other supraventricular tachyarrhythmias are projected to grow at double-digit CAGRs over the coming decade, outpacing global averages and providing a favorable backdrop for cryoballoon adoption. Local manufacturing partnerships, technology transfers, and tailored training programs can help global players and regional manufacturers lower device costs and accelerate market penetration, particularly in large public hospital networks and high-volume cardiac centers.

Category-wise Analysis

Product Insights

Within products, cryoballoon catheters account for a 47% of total market revenue in 2025, making them the leading segment. They are the core therapeutic interface for delivering cryothermal energy to the pulmonary veins, and thus represent a major share of per-procedure spend for providers. Clinical registries such as Cryo AF Global, spanning thousands of patients in dozens of countries, have demonstrated high acute isolation rates and low serious complication rates when using contemporary cryoballoon designs. This evidence, combined with iterative design upgrades—such as enhanced coolant distribution, optimized balloon compliance, and better shaft torque control—underpins physicians’ comfort with the technology. At the same time, consoles/generators are expected to post the fastest growth through 2032, as EP labs in emerging markets install their first cryo platforms and experienced centers upgrade to more advanced consoles with improved monitoring and integration capabilities.

Application Insights

By application, atrial fibrillation, particularly paroxysmal AF is the predominant use case for cryoballoon ablation, capturing a majority share that can be approximated at around 60% of total procedures in 2025. Multiple trials have shown that for symptomatic paroxysmal AF, cryoballoon pulmonary vein isolation provides durable rhythm control and can delay or prevent progression to more persistent forms of AF. A landmark trial in patients with early AF progression risk demonstrated that cryoballoon ablation was more effective than drug therapy in reducing AF burden and delaying disease progression over multi-year follow-up. Regulatory decisions to approve cryoballoon ablation as an initial rhythm-control strategy in selected paroxysmal AF patients, rather than only after drug failure, effectively enlarge the eligible population. Looking ahead, persistent AF is expected to be the fastest-growing application segment as new data and approvals support the use of cryoballoon systems beyond classic paroxysmal presentations, particularly when combined with adjunctive lesion sets or in hybrid strategies.

End-user Insights

Hospitals currently dominate end-user demand, accounting for an estimated 55% of cryoballoon system utilization in 2025, due to their ability to support complex EP procedures and manage higher-risk patients. Large tertiary and academic centers typically lead adoption of new ablation technologies, generate early clinical evidence, and act as training hubs for community cardiologists and EP specialists. These hospitals often run high-volume EP labs that perform thousands of AF and atrial flutter procedures annually, many of which now incorporate cryoballoon or hybrid strategies. However, ambulatory surgical centers and specialized cardiac centers are poised for faster growth as reimbursement, safety data, and facility capabilities converge to support more AF ablations outside the inpatient environment. Emerging data indicate that carefully selected patients can undergo AF ablation in ambulatory or office-based settings with complication and unplanned transfer rates comparable to hospital outpatient departments, which should progressively shift a portion of volume away from traditional hospitals.

Regional Insights

North America Cryoballoon Ablation System Market Trends and Insights

North America is the leading regional market, with an estimated 39% share of global cryoballoon ablation system revenues in 2025. The U.S. anchors this position thanks to early FDA approvals, high AF prevalence, and well-developed EP networks concentrated in large cardiovascular centers and academic hospitals. Clinical practice guidelines from major cardiology societies in the region increasingly endorse catheter ablation for symptomatic AF earlier in the disease course, reinforcing procedure growth. The economic burden of AF measured in billions of US$ in direct and indirect costs has also motivated payers and providers to consider durable rhythm-control strategies that may reduce hospitalizations and stroke risk.

The regulatory and reimbursement environment is evolving in a way that favors the expansion of ablation capacity. CMS initiatives to recognize more EP ablation procedures in outpatient and ASC payment schedules are expected to alleviate cath-lab bottlenecks in hospitals and open additional procedural sites. Innovation remains strong, with North America serving as a launchpad for technologies such as POLARx™, next generation cryo consoles, and novel mapping systems. Ongoing head-to-head studies comparing cryoballoon, RF, and PFA in real-world cohorts will further clarify optimal technology selection and may spur additional procedure volumes as evidence solidifies.

Asia Pacific Cryoballoon Ablation System Market Trends and Insights

Asia Pacific is projected as the fastest-growing region for cryoballoon ablation systems through 2032, with growth underpinned by rising AF prevalence and rapid build-out of interventional cardiology and EP infrastructure. Large populations in China, India, and ASEAN markets are experiencing a growing cardiovascular burden tied to aging, urbanization, and increasing rates of hypertension, diabetes, and obesity. Yet AF ablation penetration remains relatively low on a per-capita basis, implying substantial room for catch-up compared with Western markets. Governments and private providers are expanding high-end cardiac centers, and domestic manufacturers are becoming more active in ablation technologies, creating a more favorable ecosystem for cryoballoon adoption.

Competitive Landscape

The cryoballoon ablation system market is moderately consolidated, with a few dominant players controlling a large share due to strong intellectual property portfolios, established clinical evidence, and wide hospital networks. Competition is driven by technological advancements such as improved balloon compliance, real-time temperature monitoring, and enhanced procedural efficiency. Companies focus heavily on regulatory approvals, geographic expansion in emerging markets, and partnerships with cardiac centers to increase adoption. Pricing strategies, bundled system offerings, and physician training programs play a critical role in customer retention. New entrants concentrate on differentiated designs and cost-effective platforms, intensifying innovation-led competition across developed and developing regions.

Key Developments:

- In October 2025, Merit Medical Systems, Inc. announced that it had signed a definitive asset purchase agreement with Pentax of America, Inc., a subsidiary of PENTAX Medical, Inc., to acquire the C2 CryoBalloon™ device and related technology. The company stated that the transaction was expected to close in the fourth quarter of 2025, subject to the receipt or waiver of customary closing conditions outlined in the asset purchase agreement.

- In January 2024, the FDA approved a second pulsed-field ablation system (the Farapulse PFA system), enabling U.S. clinicians to use another non-thermal ablation option to treat patients with paroxysmal atrial fibrillation. This approval expanded the available technology for atrial fibrillation treatment beyond the first cleared system, offering an alternative electroporation-based approach that minimizes damage to surrounding tissue while targeting arrhythmogenic cardiac cells.

Companies Covered in Cryoballoon Ablation System Market

- Medtronic plc

- Boston Scientific Corporation

- Abbott Laboratories

- Biosense Webster (Johnson & Johnson)

- AtriCure, Inc.

- Adagio Medical, Inc.

- CardioFocus, Inc.

- CryoCath Technologies

- HealthTronics, Inc.

- Pentax Medical

- CPSI Biotech

- Synmed Ltd.

- Others

Frequently Asked Questions

The global cryoballoon ablation system market is expected to reach about US$ 1.5 billion in 2026, supported by rising AF prevalence, growing use of catheter ablation as an early rhythm‑control strategy, and increasing installation of cryo platforms across hospitals and specialty centers worldwide.

A major demand driver is the rise in global burden of atrial fibrillation, now affecting tens of millions of patients and associated with substantially higher stroke and mortality risks, which pushes clinicians and payers toward durable rhythm‑control solutions where cryoballoon ablation has shown strong safety‑efficacy performance in randomized trials and large registries.

North America leads the market, with an estimated 39% share in 2025, owing to advanced EP infrastructure, early FDA approvals for cryoballoon platforms, relatively favorable reimbursement for ablation, and a high concentration of AF centers in the United States and Canada.

One of the most important opportunities is the shift of AF ablation to ambulatory surgical centers and other outpatient EP settings as CMS and private payers expand coverage, allowing lower-cost, high-throughput treatment of suitable patients and driving incremental demand for standardized, workflow-efficient cryoballoon systems.

Key players include Medtronic plc, Boston Scientific Corporation, Abbott Laboratories, Biosense Webster (Johnson & Johnson), AtriCure, Inc., Adagio Medical, Inc., CardioFocus, Inc., CryoCath Technologies, HealthTronics, Inc., Pentax Medical, CPSI Biotech, Synmed Ltd., and select regional firms and innovators active in complementary ablation technologies.