- Pharmaceuticals

- Crisaborole Market

Crisaborole Market Size, Share, and Growth Forecast, 2026 - 2033

Crisaborole Market by Product Type (Ointments, Creams, Gels), Distribution Channel (Hospitals, Retail Pharmacies, Cosmetic Clinics, Online Pharmacies), and Regional Analysis for 2026 - 2033

Crisaborole Market Size and Trends Analysis

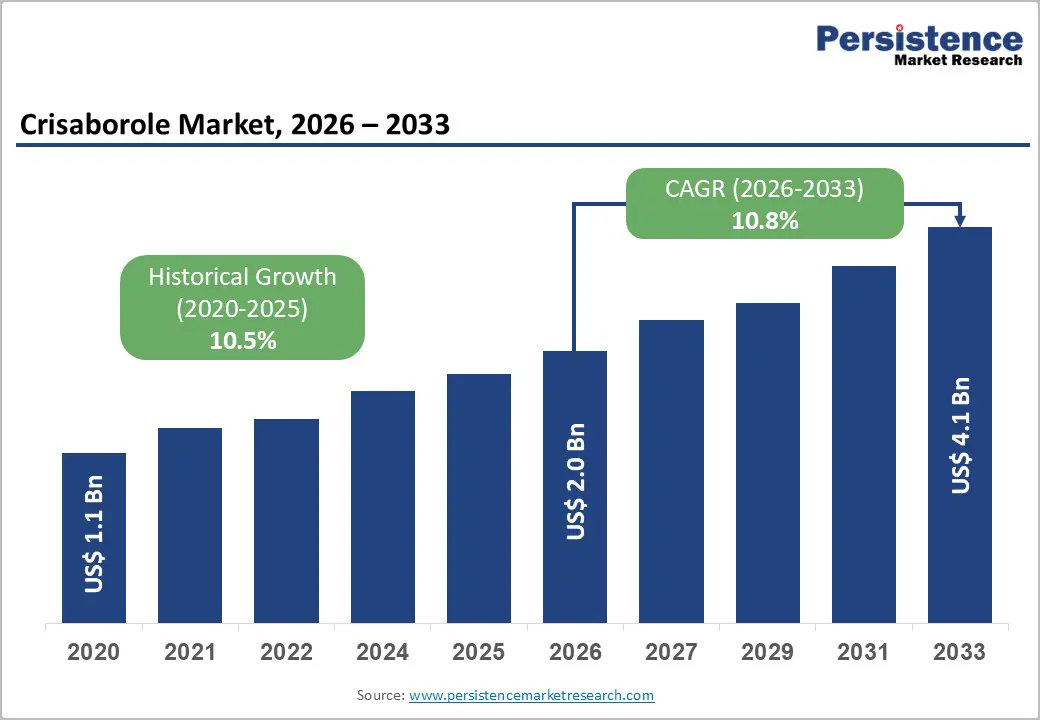

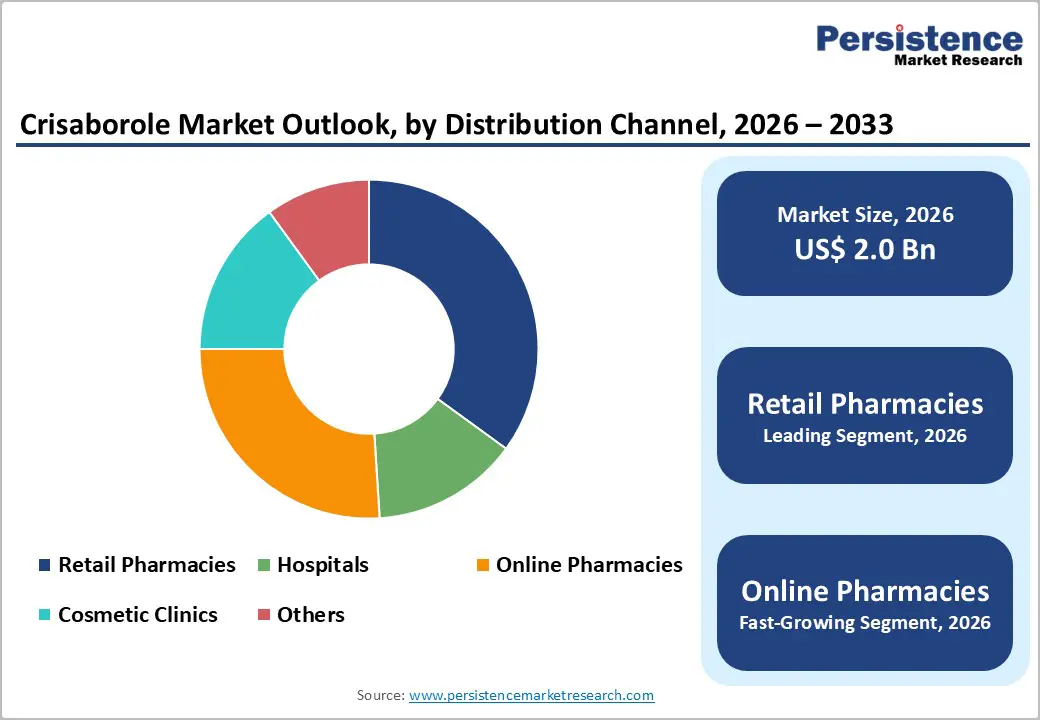

The global crisaborole market size is likely to be valued at US$2.0 billion in 2026 and is expected to reach US$4.1 billion by 2033, growing at a CAGR of 10.8% during the forecast period from 2026 to 2033, driven by the rising prevalence of atopic dermatitis, particularly among pediatric and adult populations, and the increasing preference for non-steroidal topical therapies due to their favorable safety profile for long-term use.

Regulatory approvals and label expansions by authorities such as the U.S. FDA have strengthened clinical adoption, while ongoing R&D and lifecycle management strategies support sustained demand. Expanding healthcare infrastructure, improved dermatology access in emerging economies, and growing awareness of chronic inflammatory skin disorders collectively contribute to increased diagnosis rates and wider adoption of crisaborole-based treatments.

Key Industry Highlights:

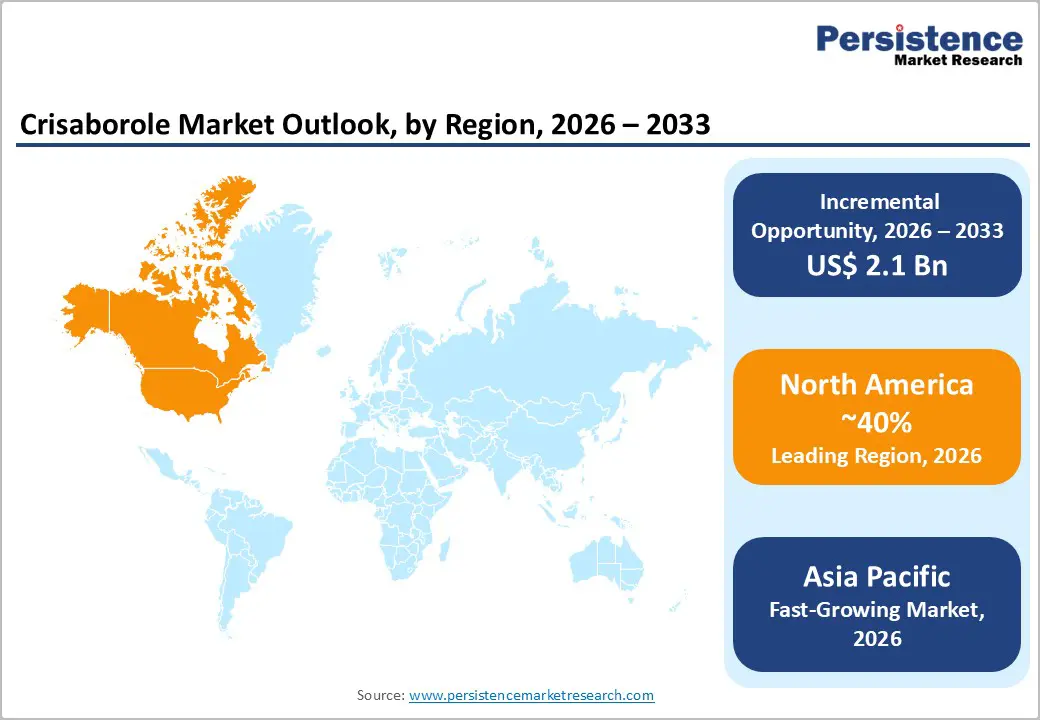

- Leading Region: North America is anticipated to be the leading region, accounting for 40% market share in 2026, driven by high atopic dermatitis prevalence, pediatric adoption, FDA support, and a strong dermatology innovation ecosystem.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by the rising prevalence of atopic dermatitis, expanding healthcare access, favorable regulatory frameworks, and cost-effective local manufacturing.

- Leading Product Type: Ointments are projected to be the leading product type in 2026, accounting for 60% of revenue share, driven by their strong clinical efficacy and widespread use in the treatment of atopic dermatitis.

- Leading Distribution Channel: Retail pharmacies are expected to be the leading distribution channel, accounting for over 45% of revenue in 2026, supported by easy accessibility, prescription fulfillment, and pharmacist guidance.

| Key Insights | Details |

|---|---|

|

Crisaborole Market Size (2026E) |

US$2.0 Bn |

|

Market Value Forecast (2033F) |

US$4.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

10.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Prevalence of Atopic Dermatitis and Chronic Skin Conditions

Atopic dermatitis is one of the most common chronic skin disorders worldwide, affecting a significant portion of infants, children, and adults, with many cases persisting into adulthood. Rapid urbanization, increasing exposure to environmental pollutants, changing lifestyles, and heightened allergen sensitivity have contributed to the growing incidence of these conditions. Climate variability and reduced skin barrier function linked to modern living environments further exacerbate disease prevalence. As atopic dermatitis is a long-term, relapsing condition, patients often require continuous and maintenance therapy, resulting in sustained demand for topical treatments.

Crisaborole has emerged as a preferred treatment option within this expanding patient population due to its non-steroidal mechanism of action and favorable safety profile for long-term use. Concerns over prolonged corticosteroid use, such as skin atrophy, pigmentation changes, and systemic side effects, have increased demand for steroid-sparing alternatives, particularly for pediatric patients and sensitive skin areas. Dermatologists increasingly recommend crisaborole for mild-to-moderate atopic dermatitis, supporting higher prescription volumes. Rising patient awareness, improved disease education, and increased focus on improving quality of life are driving treatment adherence.

Presence of Alternative Treatments and Regulatory Hurdles

Topical corticosteroids remain the primary treatment for atopic dermatitis due to their fast anti-inflammatory effects, wide availability, and relatively low cost, especially in developing countries. Calcineurin inhibitors such as tacrolimus and pimecrolimus offer viable non-steroidal alternatives with well-established prescribing records. The increasing use of biologics and targeted systemic therapies for moderate-to-severe cases is changing treatment protocols, often reducing the reliance on topical treatments. Crisaborole is typically reserved for mild-to-moderate cases or for steroid-sensitive patients, limiting its potential market.

Regulatory challenges are another significant barrier impacting the global crisaborole market. The stringent approval requirements for topical dermatology treatments, such as comprehensive safety, efficacy, and stability data, can prolong approval timelines and escalate development costs. Differences in regulatory frameworks across regions, including North America, Europe, and the Asia Pacific, further complicate market entry, requiring manufacturers to comply with multiple regulations. Post-approval responsibilities, such as pharmacovigilance and ongoing safety monitoring, add to operational complexity. In emerging markets, the lack of regulatory harmonization and the presence of pricing controls can further hinder commercialization opportunities.

Technological Convergence and Personalized Therapies

Advancements in drug delivery systems, including improved topical penetration technologies, nanocarriers, and enhanced formulation science, are facilitating better skin absorption and more sustained therapeutic effects. These innovations not only enhance treatment efficacy but also help reduce irritation, which is a critical consideration for chronic conditions such as atopic dermatitis. The integration of digital health tools, such as AI-driven diagnostics, mobile health apps, and teledermatology platforms, is improving early diagnosis, treatment monitoring, and patient adherence.

The shift toward personalized therapies offers significant long-term prospects for crisaborole manufacturers. With a deeper understanding of the genetic, environmental, and lifestyle factors that affect atopic dermatitis, there is increasing demand for tailored treatment approaches. Crisaborole’s favorable safety profile makes it well-suited for personalized regimens, especially in pediatric patients, sensitive skin areas, and long-term maintenance therapies. The use of real-world data, biomarkers, and patient-specific response tracking can help fine-tune dosing and treatment duration, ultimately improving patient outcomes and satisfaction. Collaborations between pharmaceutical companies, digital health firms, and research institutions are driving innovation in personalized dermatology care.

Category-wise Analysis

Product Type Insights

Ointments are expected to dominate the crisaborole market, accounting for around 60% of total revenue in 2026, owing to their established clinical effectiveness in treating atopic dermatitis. Their semi-occlusive formulation helps retain moisture, restore the skin barrier, and improve drug penetration, making them essential for managing chronic inflammatory skin conditions. Dermatologists commonly recommend ointments for patients with dry, sensitive, or compromised skin, especially in pediatric and long-term treatment scenarios. The non-irritating nature of ointments also fosters better patient adherence, which is crucial for managing recurrent dermatological disorders. For example, Eucrisa ointment has gained strong physician acceptance as a steroid-free option for mild-to-moderate atopic dermatitis.

Gels are anticipated to be the fastest-growing segment in 2026, driven by shifting patient preferences and changes in dermatological practices. Unlike ointments, gel formulations provide a lightweight, fast-absorbing, and non-greasy application, significantly enhancing comfort and cosmetic appeal. This is particularly attractive to patients in warm, humid climates, where heavier formulations may feel uncomfortable. Urban populations and younger patients are increasingly opting for gels due to their ease of use and minimal residue, which promotes higher treatment compliance. For instance, modern dermatological gel-based treatments are gaining popularity for daily use as they combine therapeutic efficacy with cosmetic benefits.

Distribution Channel Insights

Retail pharmacies are projected to lead the market, accounting for around 45% of total revenue in 2026, owing to their widespread accessibility and pivotal role in dermatological care. These pharmacies act as the primary point for dispensing prescription topical treatments, particularly for chronic skin conditions that require regular medication refills. Pharmacist-led counseling at retail locations enhances patient knowledge on proper application techniques, usage duration, and potential side effects, thereby improving treatment outcomes. Retail pharmacies also enjoy strong patient trust and seamless integration with healthcare providers. For instance, large retail pharmacy chains that dispense dermatologist-prescribed crisaborole products continue to attract high foot traffic due to their convenience and professional guidance.

Online pharmacies are expected to be the fastest-growing distribution channel in 2026, fueled by the rapid growth of digital healthcare ecosystems. The increasing use of teledermatology, electronic prescriptions, and home delivery services has revolutionized how patients access topical treatments for chronic skin conditions. Online platforms offer added convenience, privacy, and time savings, making them particularly appealing to urban and tech-savvy consumers. Patients managing long-term conditions such as atopic dermatitis benefit from subscription-based refills and doorstep delivery, which help improve adherence. For example, online pharmacy platforms integrated with telemedicine consultations allow dermatologists to prescribe crisaborole remotely, enabling patients to receive their medication without visiting physical stores.

Regional Insights

North America Crisaborole Market Trends

North America is expected to lead the market, capturing a 38% market share in 2026, driven by the high prevalence of atopic dermatitis and increasing awareness of long-term skin health concerns. Dermatologists in the region are increasingly opting for steroid-sparing treatments for chronic management, particularly in pediatric and sensitive-skin cases. The region's advanced healthcare infrastructure, widespread insurance coverage, and high rates of dermatology consultations contribute to early diagnosis and consistent treatment adherence. Ongoing clinical research and post-marketing studies continue to build physician confidence in topical PDE-4 inhibitors, ensuring steady prescription volumes. The rapid adoption of digital health tools, such as teledermatology and e-prescriptions, is improving patient access to dermatological care and sustaining market demand.

Innovation and strategic commercialization are the key trends shaping the North American market. Pharmaceutical companies are focusing on improving formulations, managing product lifecycles, and generating real-world evidence to maintain a competitive edge. For example, Pfizer Inc. enhanced its market penetration of Eucrisa by leveraging its established dermatology sales network and physician education programs across the U.S. Collaborations between pharmaceutical companies, research institutions, and digital health platforms also drive product differentiation and advance innovation in the sector.

Europe Crisaborole Market Trends

Europe is expected to be a key market for crisaborole in 2026, driven by increasing awareness of atopic dermatitis and a strong focus on long-term treatment safety. Dermatologists in major European countries are placing greater emphasis on steroid-sparing treatments, especially for pediatric and chronic cases, in line with updated clinical guidelines. Universal healthcare coverage and well-established referral systems enable timely diagnosis and treatment, ensuring a steady demand for topical dermatology products. Efforts to educate patients and improve access to specialist care in Western and Northern Europe are further boosting treatment adherence. The growth of digital health services, such as e-prescriptions and teledermatology, is also improving patient access to dermatological treatments.

Regulatory consistency and innovation are shaping market trends in Europe. Harmonized approval processes and stringent pharmacovigilance requirements promote high product quality and patient safety, while encouraging companies to invest in clinical evidence generation. For example, Sanofi S.A. is expanding its dermatology portfolio in Europe through research partnerships and targeted product positioning within the inflammatory skin disorder space. Collaborations between pharmaceutical companies and academic research institutions are also fostering innovation in topical therapies. These factors, combined with strong healthcare systems and increasing demand for safe, long-term treatments, are driving the evolution of the crisaborole market in Europe.

Asia Pacific Crisaborole Market Trends

The Asia Pacific region is expected to be the fastest-growing market for crisaborole in 2026, driven by increased awareness of atopic dermatitis and a rising demand for safe, long-term topical treatments. Urbanization, environmental pollution, and lifestyle changes in countries such as China, Japan, and India have led to a higher incidence of chronic inflammatory skin conditions. Improved healthcare infrastructure and better access to dermatology services are enabling earlier diagnosis and treatment, particularly in urban and semi-urban areas. Growing patient education and a greater acceptance of non-steroidal therapies are facilitating wider adoption of crisaborole-based products. The rise of teledermatology and online pharmacy platforms is also enhancing treatment accessibility, further accelerating market growth in the region.

Manufacturing capabilities and strategic regional investments are key factors influencing market trends in the Asia Pacific. The region benefits from cost-effective pharmaceutical production, a robust API manufacturing ecosystem, and government policies that support strengthening domestic drug supply chains. For instance, Sun Pharmaceutical Industries Ltd. is expanding its dermatology portfolio and manufacturing capacity in the Asia Pacific to meet the growing demand. Both local and multinational companies are increasing R&D collaborations to develop patient-friendly formulations that cater to regional preferences.

Competitive Landscape

The global crisaborole market is moderately fragmented, with both established pharmaceutical giants and emerging specialty companies competing in areas such as branded products, generics, and formulation enhancements. Companies are focused on increasing crisaborole availability, obtaining regulatory approvals in various regions, and strengthening their dermatology portfolios to capture a larger share of the mild-to-moderate atopic dermatitis market. Innovation efforts are centered on advanced topical delivery technologies, licensing agreements, and regional distribution partnerships to expand product reach and improve patient access.

Key players, including Pfizer Inc., Sun Pharmaceutical Industries Ltd., Anacor Pharmaceuticals Inc., Novartis AG, and Johnson & Johnson, create a competitive landscape where legacy brands balance against the aggressive expansion strategies of mid-sized and regional firms. These companies compete by offering differentiated products, improving formulations, expanding geographically, and employing integrated marketing approaches that target both dermatologists and patients. Competitive advantages are being built through substantial investments in R&D, the generation of real-world evidence, and the development of stronger distribution networks across retail, hospital, and digital channels.

Key Industry Developments:

- In February 2024, a Phase 2a proof-of-concept study published in the Journal of the American Academy of Dermatology reported that 2% crisaborole ointment (Eucrisa) demonstrated clinical improvement in patients with stasis dermatitis (venous eczema). The double-blind, vehicle-controlled study enrolled 65 patients aged 45 years and older and showed a reduction in lesional body surface area, as assessed by board-certified dermatologists via remote digital imaging. The study was led by Dr. Jonathan I. Silverberg of George Washington University and highlights crisaborole’s potential beyond its approved indication for atopic dermatitis.

Companies Covered in Crisaborole Market

- Pfizer Inc.

- Anacor Pharmaceuticals Inc.

- Novartis AG

- Sanofi S.A.

- GlaxoSmithKline plc

- AstraZeneca plc

- Johnson & Johnson

- Merck & Co., Inc.

- Eli Lilly and Company

- AbbVie Inc.

- Amgen Inc.

- Bristol-Myers Squibb Company

- Allergan plc

- Bayer AG

Frequently Asked Questions

The global crisaborole market is projected to reach US$ 2.0 billion in 2026.

The crisaborole market is driven by the increasing prevalence of atopic dermatitis, a growing preference for non-steroidal topical treatments, and heightened awareness of the importance of long-term skin safety.

The crisaborole market is expected to grow at a CAGR of 10.8% from 2026 to 2033.

Key market opportunities include targeting pediatric and infant populations, developing advanced topical formulations such as gels and creams, utilizing digital health and teledermatology to expand access, exploring new indications such as stasis dermatitis, and capitalizing on growth in emerging markets with improving dermatology infrastructure.

Pfizer Inc., Anacor Pharmaceuticals Inc., Novartis AG, Sanofi S.A., and GlaxoSmithKline plc are the leading players.