- Pharmaceuticals

- CRBSI Treatment Market

CRBSI Treatment Market Size, Share, and Growth Forecast 2026 - 2033

CRBSI Treatment Market by Treatment Type (Antibiotics, Antifungal medicines, Antiseptics & disinfectants, Catheter removal or replacement, Preventive therapies), by Product (Antimicrobial-coated catheters, Catheter lock solutions, Antiseptic dressings, Others), by End User (Hospitals, Clinics, Home care or long-term care facilities), and Regional Analysis, 2026 - 2033

CRBSI Treatment Market Share and Trends Analysis

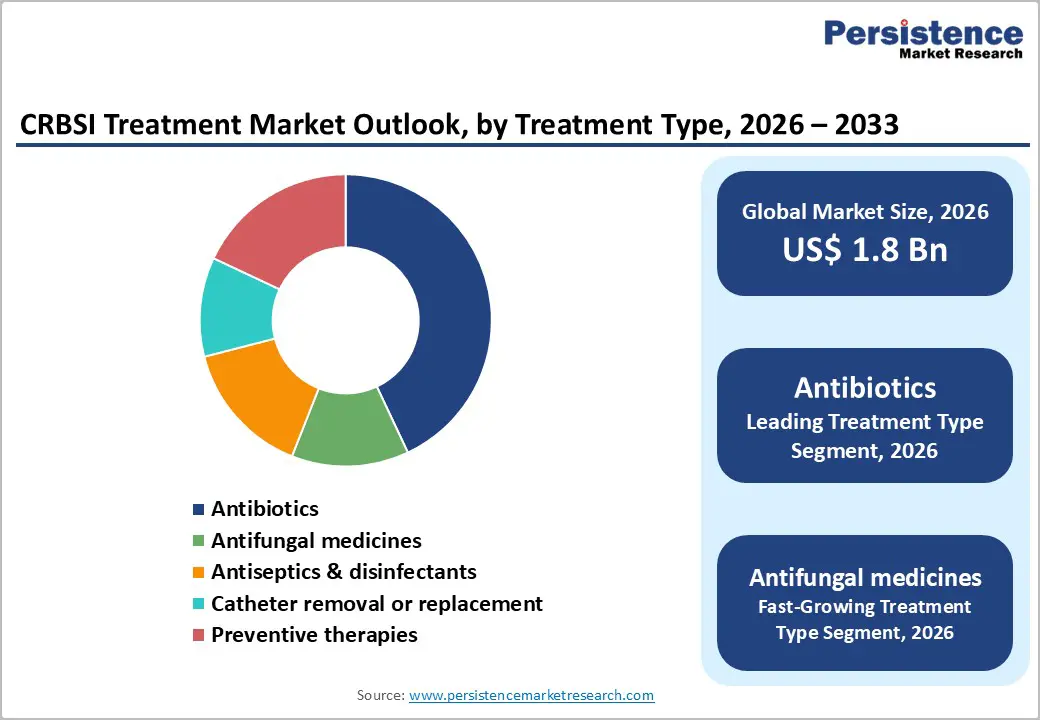

The global CRBSI treatment market size is expected to be valued at US$ 1.8 billion in 2026 and projected to reach US$ 2.7 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033.

This substantial growth trajectory reflects the escalating burden of catheter-related bloodstream infections across healthcare facilities worldwide, particularly in intensive care units where central venous catheters remain indispensable for patient care. The market expansion is fundamentally driven by the alarming incidence of CRBSI, which affects approximately 250,000 patients annually in the United States alone, with developing nations reporting significantly higher rates ranging from 1.7 to 44.6 per 1,000 catheter days. Furthermore, the 12% to 25% mortality rate associated with these infections, coupled with an additional US$ 46,000 per case in healthcare costs, has intensified the urgency for effective treatment and prevention solutions across global healthcare systems.

Key Industry Highlights:

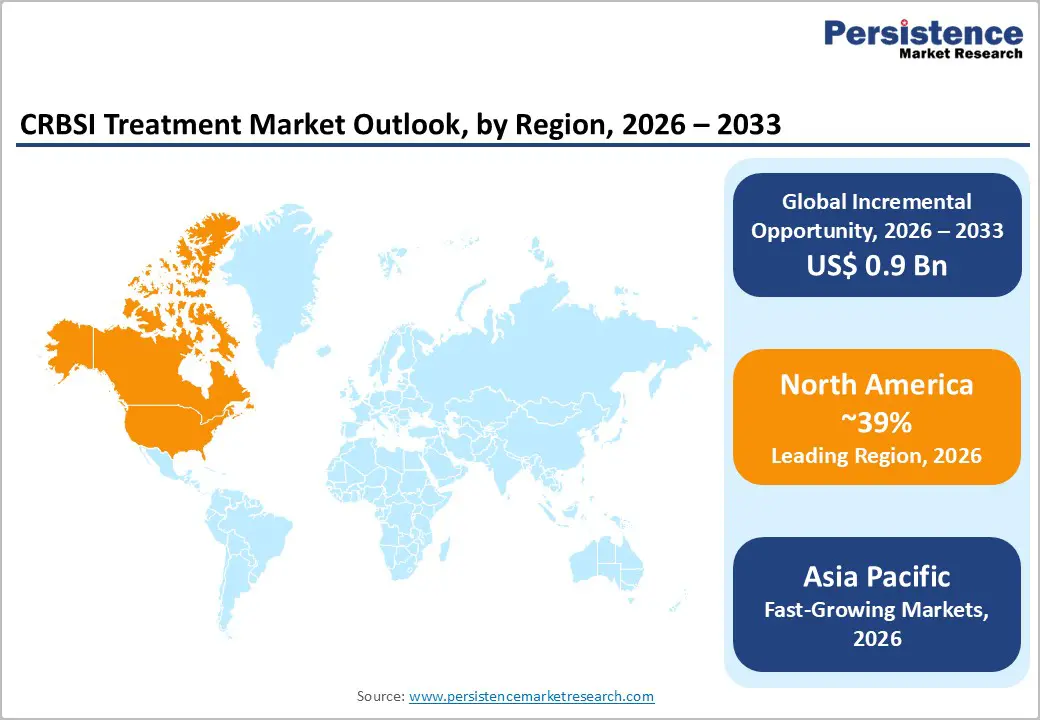

- North America leads the global CRBSI treatment market with around 39% share in 2025, supported by advanced hospitals, strong FDA and CDC regulatory oversight, and high infection-control spending estimated at over US$ 50 billion, while landmark approvals such as CorMedix’s antimicrobial lock solution further strengthen the regional technology base and clinical adoption.

- Within treatment types, antibiotics dominate with approximately 43% market share in 2025, reflecting their central role in CRBSI management and the continued launch of advanced agents targeting multidrug-resistant Gram-negative bacteria, while antifungal drugs are gaining traction due to increasing Candida-related bloodstream infections among immunocompromised and long-term catheterized patients.

- Among products, catheter lock solutions are emerging as the fastest-growing category after FDA approval of a taurolidine-based lock demonstrating about 74% reduction in CRBSI risk, supported by meta-analyses showing nearly 69% CLABSI reduction and attractive resistance profiles, positioning these solutions as key adjuncts to systemic therapy across dialysis and oncology populations.

- A major opportunity lies in pairing innovative non-antibiotic antimicrobial lock therapies with rapidly expanding Asia Pacific healthcare infrastructure, where high infection burdens and growing catheter usage, combined with China’s approximately 61% share of regional catheter production and supportive reforms, create fertile ground for scalable, cost-effective CRBSI prevention models.

| Key Insights | Details |

|---|---|

|

CRBSI Treatment Market Size (2026E) |

US$ 1.8 Bn |

|

Market Value Forecast (2033F) |

US$ 2.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.9% |

Market Dynamics

Drivers - Rise in Prevalence of Healthcare-Associated Infections in Critical Care Settings

The dramatic rise in healthcare-associated infections, particularly catheter-related bloodstream infections, constitutes a primary catalyst propelling market expansion. Surveillance data from the Centers for Disease Control and Prevention (CDC) indicate that CLABSI rates in United States intensive care units averaged around 0.87 per 1,000 central line days, although some medical–surgical units report rates as high as 2.8 per 1,000 central line days. In contrast, meta-analyses from China have shown intensive care unit CRBSI rates of about 2.65 per 1,000 central line days, with adult ICUs in northern regions reaching approximately 5.13 per 1,000 central line days. The problem is compounded by the growing prevalence of multidrug-resistant organisms; in some observational cohorts, up to 62.30% of CRBSI patients harbor multidrug-resistant pathogens compared with around 3.86% in non-CRBSI controls. With Gram-negative bacteria accounting for roughly 52.63% of CRBSI cases in several recent multicenter evaluations, hospitals are under mounting pressure to improve prevention and treatment practices, directly supporting sustained demand for CRBSI-focused therapies, optimized systemic antibiotics, and adjunctive technologies.

Stringent Regulatory Frameworks and International Infection Control Guidelines

Intensifying regulatory mandates and global infection prevention guidelines are significantly amplifying demand for CRBSI treatment solutions. The World Health Organization (WHO) released dedicated guidance in 2024 aimed at reducing bloodstream infections from catheter use, incorporating 14 good practice statements and 23 evidence-based recommendations spanning aseptic insertion techniques, hand hygiene, catheter site care, and maintenance protocols. In parallel, the Asia Pacific Society of Infection Control (APSIC) has issued revised CLABSI prevention guidelines emphasizing maximal sterile barrier precautions, chlorhexidine skin preparation, and standardized catheter-care bundles across adult and pediatric settings. Regulatory momentum is reinforced by therapeutic innovation: for example, the U.S. Food and Drug Administration (FDA) approval in 2023 of an antimicrobial catheter lock solution demonstrated a roughly 71% reduction in CRBSI risk in a pivotal Phase 3 trial, providing high-quality clinical evidence that accelerates adoption. National quality programs and payers increasingly link reimbursement to infection metrics, pushing hospitals to invest in advanced infection control products and robust CRBSI management pathways, underpinning market growth over the forecast period.

Restraints - Rising Antimicrobial Resistance Threatening Treatment Efficacy

The accelerating emergence of antimicrobial resistance remains a critical headwind for the CRBSI treatment market. The WHO has identified antimicrobial resistance as a top global health threat, with modeling studies suggesting up to 10 million deaths annually by 2050 if current trends are not reversed. Bacterial antimicrobial resistance was directly associated with an estimated 1.27 million deaths globally in 2019, with resistant Gram-negative organisms playing a major role in bloodstream infections. In the CRBSI setting, resistance to frontline agents such as vancomycin is particularly concerning, with clinical reports describing strains exhibiting minimum inhibitory concentrations above 2 mg/mL, prompting use of alternative agents such as daptomycin or linezolid. Biofilm formation on catheter surfaces can increase tolerance to antibiotics by 100–1,000 times compared with planktonic bacteria, further complicating eradication. These trends undermine the reliability of standard antibiotic regimens, increase treatment complexity and cost, and force continuous reformulation of therapeutic strategies, which can slow guideline adoption and constrain the effective growth of the traditional antibiotic-focused portion of the market.

High Cost Burden Associated with Advanced Infection Prevention Technologies

The high upfront cost of advanced CRBSI-focused technologies continues to limit their penetration, especially in low- and middle-income countries where infection prevalence is highest. Antimicrobial-coated catheters and sophisticated impregnated dressings often carry price premiums relative to standard devices, despite evidence showing 40–50% reductions in infection rates in some clinical studies. The global antimicrobial-coated catheter market has already reached well over US$ 1 billion, with North America accounting for about half of revenues, reflecting the concentration of purchasing power in high-income systems. At the same time, each CRBSI episode can add around US$ 46,000 in direct healthcare costs, but budget-constrained facilities still struggle to justify capital outlays for prevention technologies when short-term budgets are tight. Implementing comprehensive infection prevention programs also requires investment in staff training, surveillance, and quality improvement infrastructure. This cost barrier hinders universal implementation of best-practice bundles and limits uptake of the newest products, tempering market growth even as clinical and economic rationale for prevention strengthens.

Opportunities - Expanding Adoption of Novel Antimicrobial Lock Solutions and Non-Antibiotic Alternatives

The rise of antimicrobial catheter lock solutions particularly non-antibiotic formulations creates compelling growth opportunities in the CRBSI treatment landscape. The FDA approval in 2023 of a taurolidine–heparin-based lock solution for adult hemodialysis patients with central venous catheters marked the first U.S.-approved antimicrobial lock specifically indicated for reducing CRBSI incidence. In the pivotal randomized, double-blind Phase 3 study, this product lowered CRBSI risk by about 71–74% compared with heparin alone, while showing comparable safety. Meta-analyses of antimicrobial lock therapy have reported roughly 69% reductions in CLABSI rates and approximately 32% decreases in exit-site infections when such locks are added to standard care. Non-antibiotic locks are particularly attractive because they appear as effective as antibiotic-based solutions but with lower risk of promoting systemic antimicrobial resistance. With large group purchasing organizations and performance improvement networks in the United States granting innovative technology designations to such products, formulary access is broadening. As evidence accumulates across hemodialysis, oncology and long-term venous access populations, adoption of lock solutions is likely to expand rapidly, supporting a high-growth niche within the overall CRBSI treatment market.

Rapid Healthcare Infrastructure Development and Rising Catheter Usage in Asia Pacific Emerging Markets

The rapid expansion of healthcare infrastructure across Asia Pacific is generating strong demand for CRBSI treatment and prevention solutions. Regional catheter markets are forecast to grow at high double-digit rates; some analyses project the broader catheter segment in Asia Pacific reaching around US$ 28,000 million by the early 2030s, with a compound annual growth rate close to 10.9%. China alone accounts for nearly 47% of regional catheter consumption and around 61% of production capacity, underscoring its central role in supply and demand. At the same time, CLABSI and CRBSI rates in Asia are often higher than in high-income Western countries: pooled estimates from China show ICU CLABSI rates of about 2.65 per 1,000 central line days, with specific adult ICUs reporting rates above 5 per 1,000 central line days, and tertiary hospitals in India documenting incidences exceeding 9 per 1,000 catheter days. Governments across China, India, Japan and ASEAN are increasing healthcare spending, expanding insurance coverage, and promoting quality accreditation, which encourages adoption of guideline-based infection prevention bundles. Launches of advanced interventional platforms and catheters across Japan, China, Australia, Taiwan, and Korea further reflect strong technology pull. These dynamics position Asia Pacific as the fastest-growing region for CRBSI treatment solutions, offering substantial opportunities for companies that can balance innovation with cost-sensitive, scalable offerings.

Category-wise Analysis

Treatment Type Insights

Antibiotics remain the dominant treatment type, accounting for about 43% of the CRBSI treatment market share in 2025. This leadership is rooted in their central role as first-line therapy for confirmed or suspected catheter-related bloodstream infections. Consensus guidelines from bodies such as the CDC and infectious disease societies recommend prompt initiation of broad-spectrum parenteral antibiotics tailored to likely pathogens and local resistance patterns, typically vancomycin for methicillin-resistant staphylococci, often combined with agents targeting Gram-negative organisms. Observational data suggest that Gram-negative bacteria are responsible for around 50–55% of CRBSI cases in many hospitals, with Pseudomonas, Klebsiella, and Escherichia coli being frequent culprits, necessitating coverage with third- or fourth-generation cephalosporins, beta-lactam/beta-lactamase inhibitor combinations, or carbapenems in high-risk patients. Pharmaceutical pipelines continue to introduce new agents against multidrug-resistant strains; for example, combinations such as aztreonam–avibactam have shown cure rates above 70% in severe infections caused by metallo-beta-lactamase-producing bacteria. In parallel, antifungal medicines constitute the fastest-growing treatment subtype, reflecting increasing rates of Candida-related CRBSI in immunocompromised patients and those on prolonged parenteral nutrition, with echinocandins such as micafungin, caspofungin, and anidulafungin now preferred in many settings where azole resistance or non-albicans species are prevalent.

Product Insights

Antimicrobial-coated catheters hold the leading share among CRBSI-related products, supported by strong clinical evidence and broad integration into infection prevention bundles. The antimicrobial-coated catheter segment has already surpassed US$ 1.2–1.3 billion globally, with forecasts suggesting growth to more than US$ 2.0 billion over the next decade at mid- to high single-digit CAGRs. Silver-based and other antimicrobial coatings are widely adopted; silver-ion technologies alone account for roughly 60% of coated catheter usage in some markets. Randomized clinical studies have reported 40–50% reductions in catheter-related infection rates compared with uncoated devices, and some trials of specialized coatings have shown relative risk reductions close to 69% for urinary tract infections in hospitalized patients. Major manufacturers such as Becton, Dickinson and Company (BD) supply coated Foley catheters incorporating unique surface modifications to reduce bacterial adhesion and biofilm formation. At the same time, catheter lock solutions are emerging as the fastest-growing product segment. Following FDA approval of a taurolidine-based lock solution in 2023, which demonstrated approximately 71–74% reduction in CRBSI incidence in hemodialysis patients, antimicrobial lock therapy has gained traction as a key adjunct to systemic antibiotics. Meta-analyses indicating around 69% CLABSI reduction with lock therapy and comparable safety vs. standard heparin locks underpin rapid adoption, particularly in high-risk populations requiring long-term central venous access.

Regional Insights

North America CRBSI Treatment Market Trends and Insights

North America dominates the CRBSI treatment market due to the high prevalence of hospital-acquired infections, advanced healthcare infrastructure, and strong adoption of infection control practices. Hospitals in the United States and Canada increasingly focus on preventing catheter-related bloodstream infections through strict clinical guidelines, antimicrobial catheter technologies, and improved diagnostic monitoring. The growing use of central venous catheters in intensive care units, oncology treatments, and dialysis procedures continues to increase the risk of bloodstream infections, driving demand for antibiotics, antifungal therapies, and antiseptic solutions. In addition, government initiatives and regulatory programs aimed at reducing healthcare-associated infections have encouraged hospitals to adopt preventive strategies such as antimicrobial lock therapy and advanced catheter management protocols. Strong presence of pharmaceutical and medical device manufacturers also supports innovation in infection treatment and prevention solutions. Furthermore, increasing healthcare expenditure and ongoing research on antimicrobial resistance are contributing to the development of more effective CRBSI treatment approaches across the region.

Asia Pacific CRBSI Treatment Market Trends and Insights

The Asia Pacific CRBSI treatment market is emerging rapidly due to expanding healthcare infrastructure, rising hospital admissions, and increasing awareness of healthcare-associated infections. Countries such as China, India, Japan, and South Korea are witnessing a growing number of critical care procedures, including dialysis, chemotherapy, and intensive care treatments that require catheter use, thereby increasing the risk of catheter-related bloodstream infections. Hospitals across the region are gradually adopting stronger infection prevention protocols, antimicrobial catheters, and improved antibiotic therapies to reduce complications. Government investments in hospital infrastructure and infection control programs are also supporting market growth. In addition, the rising burden of chronic diseases such as cancer and kidney disorders is increasing the need for long-term catheterization, which further drives demand for effective CRBSI treatment solutions. The growing presence of global pharmaceutical and medical device companies, along with expanding healthcare access in developing economies, is expected to accelerate the adoption of advanced treatment and preventive technologies across the region.

Competitive Landscape

The CRBSI treatment market is characterized by a competitive environment driven by continuous innovation in antimicrobial therapies and infection prevention solutions. Market participants focus on developing advanced antibiotics, antifungal agents, and antiseptic formulations to improve treatment outcomes and reduce hospital-acquired infections. Companies are also investing in preventive technologies such as antimicrobial lock therapies and infection-resistant catheter management approaches to minimize infection risks. Strategic collaborations, product launches, and regulatory approvals play an important role in strengthening market presence and expanding product portfolios.

Key Developments:

- In May 2024, Citius Pharmaceuticals announced that its Phase 3 clinical trial of the antibiotic lock solution Mino-Lok successfully achieved both primary and secondary endpoints for the treatment of catheter-related bloodstream infections (CRBSI).

- In March 2024, the European Medicines Agency issued a positive opinion for Pfizer Inc.’s aztreonam–avibactam combination for the treatment of serious infections caused by multidrug-resistant Gram-negative bacteria, including organisms producing metallo-beta-lactamases, providing an important new option for difficult-to-treat bloodstream and hospital-acquired infections in the European Union.

Companies Covered in CRBSI Treatment Market

- Becton, Dickinson and Company (BD)

- 3M Company

- B. Braun Melsungen AG

- Medtronic plc

- Cook Medical

- Pfizer Inc.

- Eli Lilly and Company

- GSK plc

- Merck & Co., Inc.

- Aurobindo Pharma Limited

- Citius Pharmaceuticals

- CorMedix Inc.

- Others

Frequently Asked Questions

The global CRBSI treatment market is expected to be valued at US$ 1.8 billion in 2026 and is projected to reach about US$ 2.7 billion by 2033, reflecting a forecast CAGR of roughly 5.7% between 2026 and 2033 on the back of rising healthcare-associated infection rates and tighter infection prevention requirements.

Key demand drivers include high CRBSI and CLABSI incidence affecting around 1.7 million patients annually in North America with rates of 0.87–2.8 per 1,000 central line days, the growing burden of multidrug-resistant pathogens impacting more than 60% of CRBSI cases in some cohorts, and strong regulatory and guideline pressure from organizations such as the WHO and CDC, which issued comprehensive recommendations and global guidance on catheter-related infection prevention in 2024.

North America currently leads the CRBSI treatment market with an estimated 39% share in 2025, supported by advanced healthcare systems, significant infection control expenditures exceeding US$ 50 billion, stringent FDA and CDC oversight, and early adoption of innovative technologies such as CorMedix Inc.’s taurolidine–heparin lock solution approved in 2023 after demonstrating approximately 71% reduction in CRBSI risk.

Major opportunities include broader use of non-antibiotic antimicrobial lock solutions that can reduce CRBSI risk by around 70% while mitigating antibiotic resistance concerns, as well as rapid growth in Asia Pacific, where catheter markets are projected to reach roughly US$ 28,133.8 million by 2033 at about 10.9% CAGR, driven by high infection burdens, expanding hospital capacity, and policy pushes for quality improvement and infection prevention.

Prominent companies include Becton, Dickinson and Company (BD) with antimicrobial-coated catheter portfolios, 3M Company and B. Braun Melsungen AG in dressings and catheter systems, Medtronic plc and Cook Medical in vascular and access technologies, and pharmaceutical leaders such as Pfizer Inc., GSK plc, Merck & Co., Inc., Eli Lilly and Company, alongside specialized players CorMedix Inc., Citius Pharmaceuticals, Aurobindo Pharma Limited, Teleflex Incorporated, Bactiguard AB, and Johnson & Johnson, collectively shaping innovation and competition in CRBSI treatment and prevention.