- Hardware & Software IT Services

- Courier Software Market

Courier Software Market Size, Share, and Growth Forecast, 2026 - 2033

Courier Software Market by Component Type (Solution, Services), Deployment Mode (On-Premises, Cloud-Based), Deployment Mode (Cloud-Based, On-Premises), Organization Size (Small & Medium Enterprises (SMEs), Large Enterprises), End User (Courier & Logistics Companies, E-Commerce Businesses, Retailers, Manufacturers, Healthcare Providers) and Regional Analysis for 2026 - 2033

Courier Software Market Size and Trends Analysis

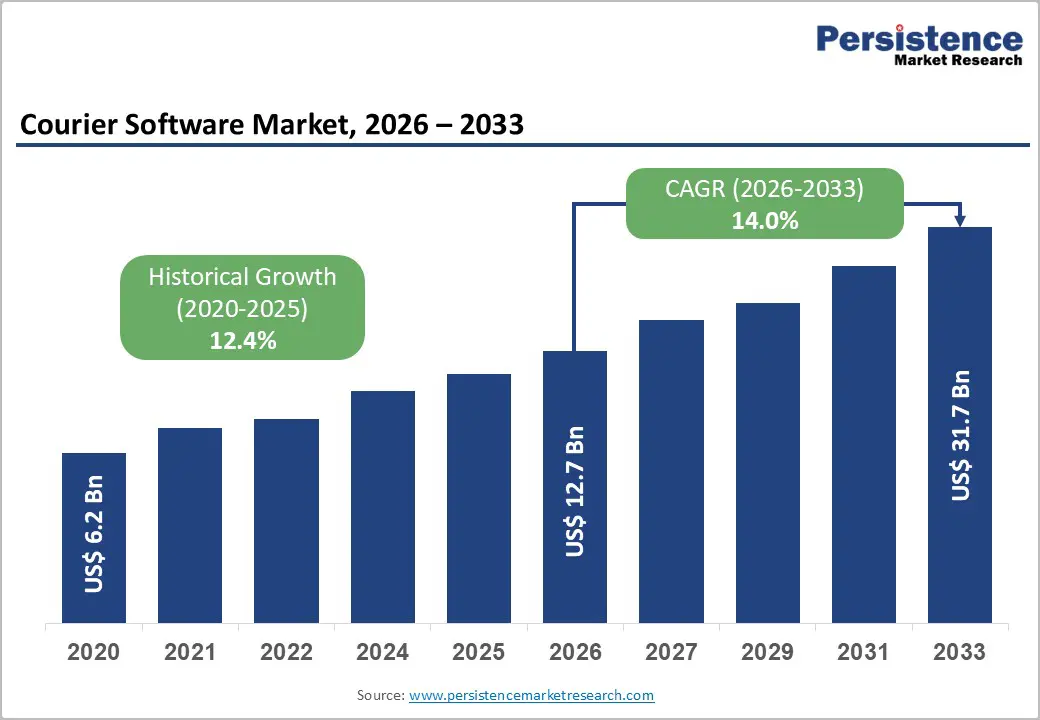

The Global Courier Software Market size was valued at US$ 12.7 billion in 2026 and is projected to reach US$ 31.7 billion by 2033, growing at a CAGR of 14.0% between 2026 and 2033. The market demonstrates accelerated momentum relative to its historical performance, with a CAGR of 12.4% from 2020 to 2026, during which the market expanded from US$6.2 billion to its current valuation.

This acceleration is driven by the digital transformation of logistics operations, the exponential expansion of B2B and B2C e-commerce ecosystems, and the integration of advanced technologies, including artificial intelligence, real-time tracking, and automated route optimization, into courier operations. The convergence of mobile-first delivery solutions, cloud-based platforms, and data analytics capabilities is reshaping traditional courier workflows, enabling service providers to achieve operational excellence while meeting heightened customer expectations for visibility, speed, and reliability.

Key Industry Highlights:

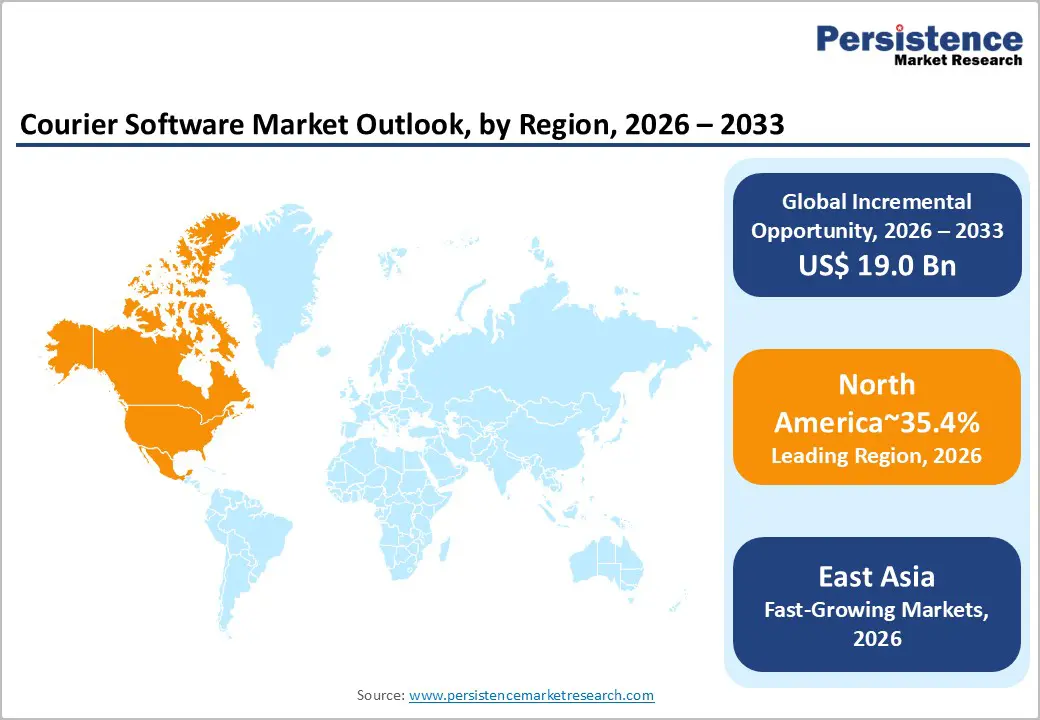

- Regional Leadership: North America leads the global Courier Software Market with 35.4% share, supported by mature logistics infrastructure, advanced warehouse automation, and strong digital transformation initiatives among courier operators.

- Strong European Presence: Europe holds 30% share, driven by cross-border logistics complexity, sustainability and compliance mandates, and cloud-driven modernisation across enterprise logistics networks.

- High-Growth East Asia Market: East Asia accounts for 20% share and remains the fastest-growing region, powered by explosive e-commerce expansion, government-backed smart logistics hubs, and rising last-mile delivery investments across China, South Korea, and Southeast Asia.

- Leading Solution Type: The Software segment dominates with 65.4% share, enabled by strong adoption of route optimisation, order management, real-time tracking, and unified multimodal logistics platforms.

- Fastest-Growing Solution Type: The Services segment is the fastest-growing, driven by rising demand for implementation support, platform customisation, training, and managed logistics IT services.

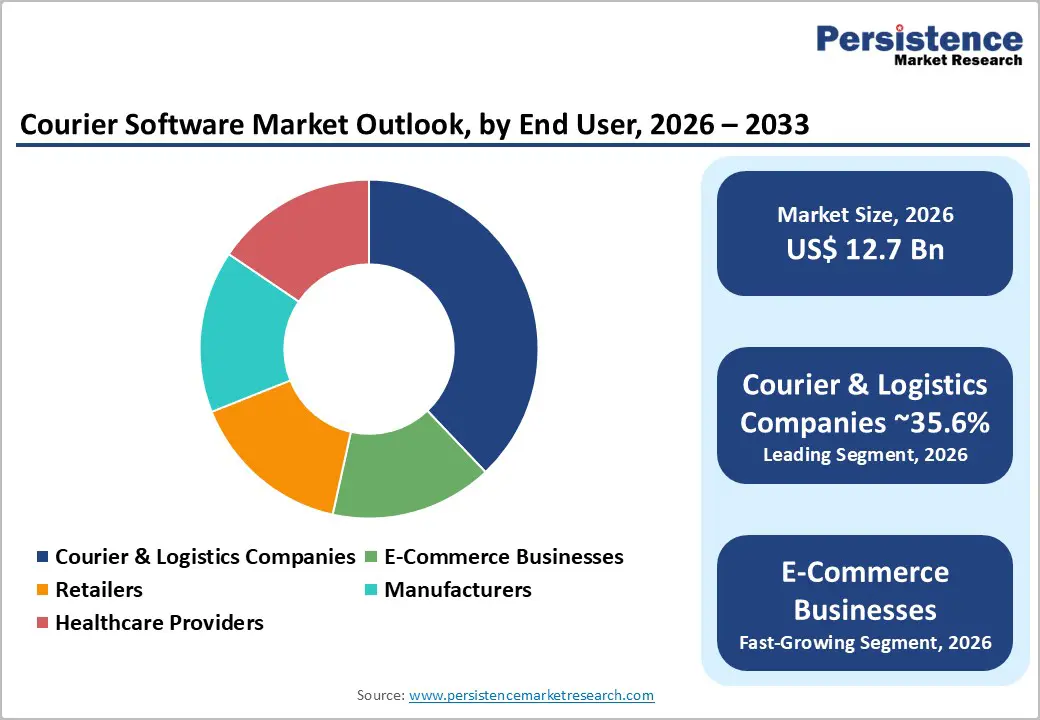

- Leading End-User Segment: Courier & Logistics Companies hold 40.3% share, reflecting deep reliance on software for fleet coordination, delivery visibility, high-volume order handling, and customer experience optimisation.

| Key Insights | Details |

|---|---|

|

Courier Software Market Size (2026E) |

US$ 12.7 Bn |

|

Market Value Forecast (2033F) |

US$ 31.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

14.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

12.4% |

Market Dynamics

Growth Drivers

E-Commerce Expansion and Omnichannel Logistics Complexity

The e-commerce landscape continues to undergo a structural transformation, compelling courier software platforms to deliver unprecedented operational sophistication. Global B2B eCommerce experienced a compound annual growth rate of 14.5 percent from 2017 to 2026, with Gross Merchandise Value climbing from US$9.8 trillion to a projected US$36.2 trillion, fundamentally reshaping logistics infrastructure requirements.

The Courier Software Market must accommodate the dual pressures of accelerating order volume and rising delivery speed expectations, with consumers increasingly demanding one-to-two-day delivery as a baseline service standard rather than a premium offering. This dynamic has prompted logistics providers to deploy sophisticated route-optimisation algorithms, multi-warehouse fulfilment strategies, and real-time inventory-visibility systems integrated through courier software platforms. The Asia-Pacific region, which will command 80 percent of global B2B eCommerce GMV by 2026, particularly drives this demand through rapid urbanisation and intensifying cross-border commerce, with courier software solutions enabling seamless coordination across fragmented regional logistics networks serving diverse consumer segments.

Modernization of Logistics Infrastructure Through Cloud-Based Platforms

Migration toward cloud-based logistics solutions fundamentally transforms courier operations by enabling real-time decision-making, scalability, and cross-border collaboration capabilities. WiseTech Global's launch of CargoWise Value Packs in December 2025 exemplifies this transformation, introducing over 216 new modules, including AI-powered features within a unified transaction-based platform that eliminates traditional hosting and seat fees. This commercial model provides logistics service providers with integrated capabilities spanning international forwarding, customs, warehousing, and land transport operations.

InPost's December 2023 strategic agreement with Capgemini to migrate to SAP S/4HANA Cloud, supported by Google Cloud infrastructure, demonstrates the operational imperative for cloud transformation. The initiative aims to enhance delivery speed, efficiency, and real-time decision-making through state-of-the-art analytics and live reporting capabilities.

These developments underscore how the Courier Software Market benefits from cloud infrastructure investments that enable courier companies to respond more quickly to market challenges, streamline operations across multiple European markets, and leverage advanced analytics to optimise operations. The convergence of cloud computing with logistics software creates scalable solutions that accommodate fluctuating delivery volumes while maintaining service quality and operational visibility.

Integration of Mobile Technology and Autonomous Data Capture Solutions

The proliferation of mobile-enabled delivery solutions and smart data capture technologies represents a critical advancement for courier operations, reducing capital expenditures while enhancing operational accuracy. Scandit's August 2015 launch of its mobile Proof of Delivery solution demonstrates this evolution, enabling logistics providers, express couriers, and postal carriers to utilise smartphones and wearable devices for delivery tracking, eliminating the need for costly dedicated barcode scanners.

The solution supports enterprise-grade barcode scanning, geotagged signature capture, and navigation, and integrates seamlessly with existing IT systems. Scandit's February 2022 completion of a $150 million Series D investment, bringing total funding to nearly $300 million, further validates market confidence in autonomous data capture technology.

The funding accelerates research and development in AI/ML capabilities and global expansion, particularly in APAC. The December 2025 partnership between Scandit, Hardis Supply Chain, and Dior showcases tangible operational benefits, achieving an 85 percent reduction in shipping control time through real-time insights and advanced barcode scanning integrated with warehouse management systems. For the Courier Software Market, these advances in mobile technology enable courier companies to equip their workforce with cost-effective, highly capable tools that improve delivery accuracy, customer communication, and operational visibility without substantial hardware investments.

Market Restraining Factors

Data Security, Compliance, and Regulatory Complexity

Security and compliance represent substantial operational expenses in courier software implementation, as data breach incidents accelerate regulatory scrutiny and liability exposure. Stringent international frameworks, including GDPR in Europe and HIPAA standards, impose non-compliance penalties that exceed the cost of financial software investments, obligating courier companies to implement encryption protocols, access control systems, audit trail mechanisms, and continuous security monitoring.

Courier software must accommodate evolving regulatory requirements across jurisdictions with varying data protection standards, customs procedures, and cross-border trade regulations, necessitating ongoing development investments and compliance certifications, including ISO 27001. The expenses associated with staff training, external audits, incident response protocols, and security-related features, including SSL certificates, data backups, and disaster recovery systems, constitute ongoing operational commitments throughout the software lifecycle duration, disproportionately impacting smaller logistics providers with constrained technology budgets.

Key Market Opportunities

Emerging Markets Penetration and Regional Digitalisation

Emerging economies across Asia, Latin America, and Africa present substantial market expansion opportunities, including rapid urbanisation, improved digital infrastructure, and rising e-commerce adoption, which create receptivity among previously underserved logistics providers for courier software platforms. India's National Logistics Policy targets reducing logistics costs to 8% of GDP by 2030 through digital integration initiatives, including the Unified Logistics Interface Platform (ULIP) and operational standardisation across 57 Central Ministries and 36 states, and establishing a governmental framework to support technology adoption within logistics ecosystems.

The government's Multi-Modal Logistics Park program designates 35 strategic locations, including Chennai, Bengaluru, Nagpur, and Indore, for integrated logistics facilities combining warehousing, customs, and transport coordination, creating institutional demand for courier software solutions capable of managing complex, multi-stakeholder operations. South Korea's courier service sector is projected to grow by 8% annually, driven by B2C e-commerce dominance and government infrastructure investments in smart logistics hubs, as well as smart mega-terminal projects reflecting institutional commitment to logistics modernisation.

Small and medium-sized enterprises in emerging markets represent particularly attractive opportunities, as cost-effective, cloud-based courier software solutions provide scalability and functionality previously accessible only to large enterprises, democratizing access to logistics technology and creating competitive parity for smaller operators navigating international supply chains.

Multimodal Freight Integration and Unified Platform Development

The convergence of air, ocean, and ground freight operations onto unified digital platforms represents a transformative opportunity for the Courier Software Market, addressing long-standing operational inefficiencies in logistics coordination. Freightos' April 2025 unveiling of its Freightos Enterprise suite exemplifies this opportunity, offering large importers and exporters a comprehensive global freight procurement platform that unifies air, ocean, and ground freight with automated RFQs, contract optimisation, and real-time market intelligence through the Freightos Baltic Index and Freightos Air Index. The platform achieves up to 90% reduction in procurement time while providing integrated modules for rate comparison, booking, and shipment tracking.

The November 2025 launch of WebCargo Rate & Quote Ocean further demonstrates market potential, enabling freight forwarders to manage air and ocean rates, quotes, and bookings on a single digital platform. Early adopters reported 75% faster quote times, significantly streamlining workflows and improving competitive positioning. For the Courier Software Market, this multimodal integration opportunity extends beyond freight forwarding to last-mile delivery coordination, enabling courier companies to offer end-to-end visibility across complex supply chains involving multiple transportation modes. The ability to seamlessly connect international shipping, customs clearance, warehousing, and final delivery through unified software platforms creates differentiation opportunities for courier service providers serving global e-commerce businesses and manufacturers with complex distribution requirements.

Category-wise Analysis

Solution Type Insights

The Software segment maintains dominant market positioning in the courier software market, capturing 65.4% market share in 2026, driven by fundamental requirements for core logistics functionality, including order management, route optimisation, tracking systems, and customer communication platforms. WiseTech Global's August 2025 acquisition of e2open Parent Holdings for $2.1 billion substantially enhances CargoWise's logistics execution capabilities, expanding market reach into global and domestic trade spanning demand planning, channel management, supply operations, and transportation logistics. The minimal product overlap between the entities strengthens end-to-end supply chain connectivity from order fulfilment through customs processing, promoting automation and digitisation across logistics operations.

The software segment's dominance reflects courier companies' prioritisation of platform investments that deliver immediate operational improvements through integrated functionality. Freightos' development of unified platforms combining air and ocean freight management demonstrates the centrality of software in addressing operational complexity, with early adopters achieving 75% faster quote times through consolidated rate management and booking capabilities. The segment benefits from recurring revenue models, continuous feature enhancements, and scalability advantages that enable courier operators to expand service offerings without proportional infrastructure investments.

The services segment is the fastest-growing component of the Courier Software Market, driven by rising customer demand for implementation support, customisation, training, and ongoing technical assistance as software platforms grow in complexity and breadth of functionality. WiseTech Global's inclusion of free training and certifications through WiseTech Academy within CargoWise Value Packs exemplifies the strategic importance of comprehensive service offerings in driving software adoption and maximising platform utilisation. The transition from traditional seat-based licensing to transaction-fee models creates heightened requirements for change management support, process optimisation consulting, and continuous performance monitoring services.

End User Insights

Courier & Logistics Companies constitute the leading end-user segment in the Courier Software Market, holding 40.3% market share in 2026, reflecting their core operational dependence on specialised software platforms to manage complex delivery networks, fleet operations, and customer service requirements.

The December 2025 partnership between Scandit, Hardis Supply Chain, and Dior demonstrates the potential for operational transformation in logistics, achieving an 85% reduction in shipping control time through the integration of advanced barcode-scanning technology with warehouse management systems. The solution enables warehouse teams to capture multiple barcodes simultaneously with instant augmented reality feedback, substantially improving accuracy and efficiency in both warehouse and in-store order preparation.

The segment's market leadership stems from courier companies' fundamental need for software platforms that manage high-volume transaction processing, real-time route optimisation, driver coordination, and customer communication across geographically dispersed service areas. InPost's record-breaking Q4 2024 results, featuring substantial growth across volumes, revenues, and Adjusted EBITDA alongside significant out-of-home network expansion, validate the commercial impact of technology-enabled logistics models. Courier operators increasingly recognise that competitive differentiation depends on software capabilities that enable faster delivery times, greater tracking visibility, and seamless customer experiences, rather than on traditional factors like fleet size or geographic coverage alone.

E-commerce businesses represent the fastest-growing segment within the Courier Software Market end-user classification, reflecting explosive growth in online retail and direct-to-consumer commerce models, driving unprecedented demand for courier software.

Regional Insights and Trends

North America Market Trend

North America commands 35.4% of the global courier software market in 2026, reflecting mature logistics infrastructure, widespread digital transformation implementation, and concentration of leading software providers. The region's sophisticated supply chain ecosystem, characterized by advanced warehouse automation, well-developed transportation networks, and mature e-commerce markets, creates demand for specialized courier software solutions that address complex operational requirements.

The North American regulatory environment reflects heightened compliance scrutiny, particularly following the August 2025 elimination of de minimis exemptions by U.S. Customs and Border Protection, which has fundamentally altered e-commerce logistics operations. This regulatory modification eliminated duty-free clearance for shipments valued at US$800 or less, necessitating formal customs entry and duty assessment for previously exempt shipments, creating substantial demand for courier software for automated customs documentation, tariff classification, and compliance management.

North American courier software adoption acceleration reflects converging demand vectors, including e-commerce delivery network expansion, last-mile logistics optimization, and supply chain visibility requirements. E-commerce delivery networks demonstrate particular pressure as peak season approaches and market conditions shift, with major retailers advancing promotional calendars and e-commerce shippers locking last-mile capacity early to manage peak surcharges and capacity constraints. FedEx's 2024 introduction of Roxo autonomous delivery robots, integrated with courier management software and IoT ecosystems and powered by artificial intelligence and real-time data analytics, demonstrates institutional commitment to autonomous last-mile delivery technologies requiring sophisticated courier software coordination

East Asia Market Trend

East Asia commanded 20% of the Global Courier Software Market in 2026 but is the fastest-growing region, driven by explosive e-commerce proliferation and governmental initiatives prioritizing logistics infrastructure modernization. China's dominance as the world's largest e-commerce market, coupled with rapid urbanization across Southeast Asia and the rise of middle-class consumer segments, is driving unprecedented demand for courier software.

China's government commitment to smart logistics and infrastructure development in urban centres accelerates courier software adoption among the dense network of logistics companies and courier services characterising the region. Government initiatives, including smart mega hub terminal development, exemplified by Hanjin's Daejeon Smart Mega Hub Terminal investment in South Korea, reflect institutional recognition that logistics infrastructure modernisation requires sophisticated digital coordination platforms. South Korea's "Guaranteed Delivery Date" service, a partnership between CJ Logistics and Naver, demonstrates technological innovation in courier software, where service guarantees depend on sophisticated software coordination to ensure predictable delivery performance despite variable operational conditions.

Europe Market Trend

Europe commands 30% of the Global Courier Software Market in 2026, with mature logistics infrastructure, established regulatory frameworks, and emphasis on sustainability and compliance, creating specialised courier software requirements. Germany's position as the leading European courier software reflects a highly developed logistics industry and a robust manufacturing sector, creating complex international supply chain requirements.

European courier software markets exhibit sophisticated competitive dynamics, with established providers, including SAP and PTV Group, delivering customized solutions that address complex routing and scheduling challenges inherent in densely populated regions with congested transportation networks. Germany's strategic location in Europe and strong trade linkages create demand for courier software to manage complex cross-border operations, customs procedures, and multi-modal transportation coordination. InPost's December 2023 strategic agreement with Capgemini and subsequent migration to SAP S/4HANA Cloud, supported by Google Cloud, exemplifies regional strategic positioning where logistics providers modernise technology infrastructure to enhance delivery speed, efficiency, and real-time decision-making capabilities.

Competitive Landscape

The global courier software market is moderately consolidated, with a few key players commanding a significant share while numerous smaller providers offer specialised solutions. Leading players such as WiseTech Global, Descartes Systems Group, Freightos, SAP, Oracle, and IBM dominate the market with comprehensive software suites that cater to large enterprises and global logistics providers. Despite the dominance of these established companies, the market remains fragmented at the niche level, with several emerging vendors offering specialised services like real-time tracking, proof of delivery, and route optimisation. This fragmentation is driven by technological advancements and the rise of cloud-based solutions, which lower entry barriers for smaller firms.

Key Industry Developments

- On June 19, 2025, Descartes Systems Group announced the acquisition of PackageRoute, a leading provider of final-mile carrier solutions. This acquisition strengthens Descartes’ final-mile carrier capabilities by integrating PackageRoute’s mobile and web-based platform that provides real-time package delivery visibility, route optimization, and fleet management. This acquisition aligns with Descartes' strategy to enhance end-to-end logistics operations and improve safety and compliance for final-mile carriers.

- On December 3, 2025, Scandit and Hardis Supply Chain partnered with Dior to enhance its warehouse logistics through real-time insights and advanced barcode scanning technology. By integrating Scandit’s MatrixScan Count with Hardis WMS, Dior optimised its warehouse workflows, reducing shipping control time by 85%. This collaboration exemplifies how courier software solutions, particularly those focused on barcode scanning and real-time insights, can streamline logistics operations, improve efficiency, and optimise order preparation processes.

Companies Covered in Courier Software Market

- WiseTech Global

- Descartes Systems Group

- Scandit

- Freightos

- InPost

- WebCargoNet

- CargoWise

- IBM Sterling

- SAP Logistics Suite

- Oracle Logistics

- Manhattan Associates

Frequently Asked Questions

The global Courier Software Market is projected to be valued at US$ 12.7 Bn in 2026.

The Courier & Logistics Companies segment is expected to account for approximately 71.2% of the Global Courier Software Market by End User in 2026.

The market is expected to witness a CAGR of 14.0% from 2026 to 2033.

The Courier Software Market growth is driven by e-commerce expansion, omnichannel logistics complexity, cloud-based platform adoption, and the integration of mobile technology and autonomous data capture solutions.

Key market opportunities in the Courier Software Market include emerging markets penetration, regional digitalisation, government infrastructure investments, multimodal freight integration, and scalable cloud-based solutions for small and medium enterprises.