- Communication Infrastructure & Services

- Composable Disaggregated Infrastructure Market

Composable Disaggregated Infrastructure Market Size, Share, and Growth Forecast 2026 - 2033

Composable Disaggregated Infrastructure Market by Component (Disaggregated Hardware, Composable Software, Services), by Application (BFSI, Manufacturing, Healthcare, IT & ITES, Utilities, Others), End-user (Cloud Providers, Colocation Providers, Enterprises), and Regional Analysis, 2026 - 2033

Composable Disaggregated Infrastructure Market Size and Trend Analysis

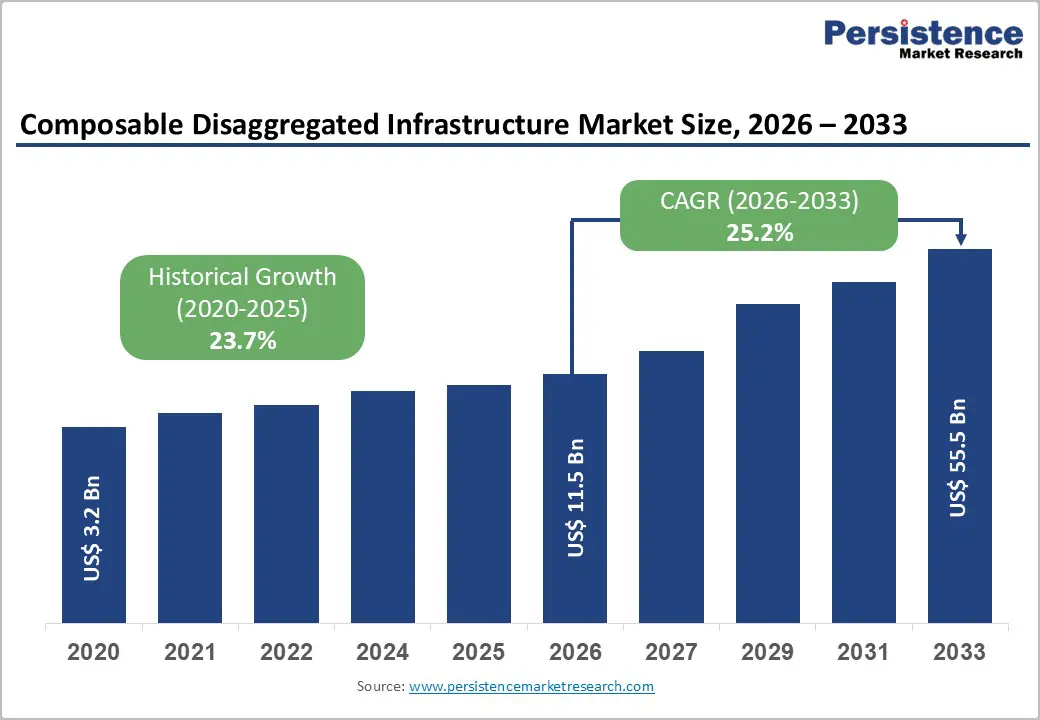

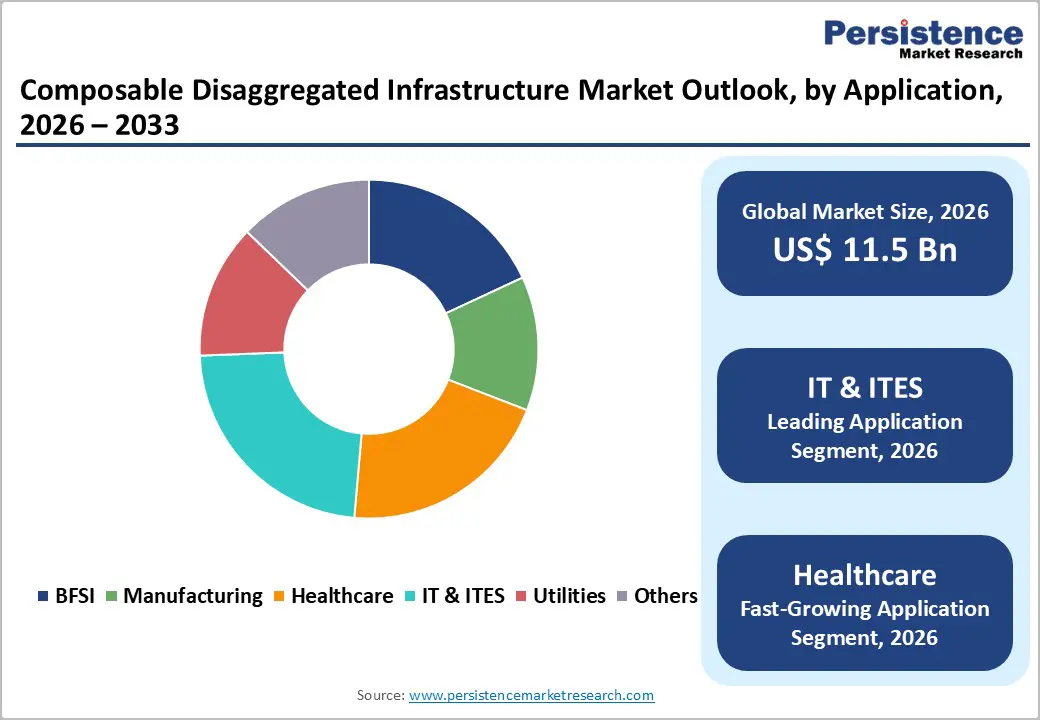

The global composable disaggregated infrastructure market size is expected to be valued at US$ 11.5 billion in 2026 and projected to reach US$ 55.5 billion by 2033, growing at a CAGR of 25.2% between 2026 and 2033.

The market is driven by surging demand for flexible IT architectures that support AI, cloud, and edge workloads through the dynamic allocation of compute, storage, and networking resources. Organizations are shifting toward hybrid environments to reduce overprovisioning and improve utilization rates from 15–20% to above 70%. Initiatives led by the Open Compute Project and rising hyperscale investments, alongside increasing data center power demand highlighted by the International Energy Agency, further accelerate adoption.

Key Industry Highlights:

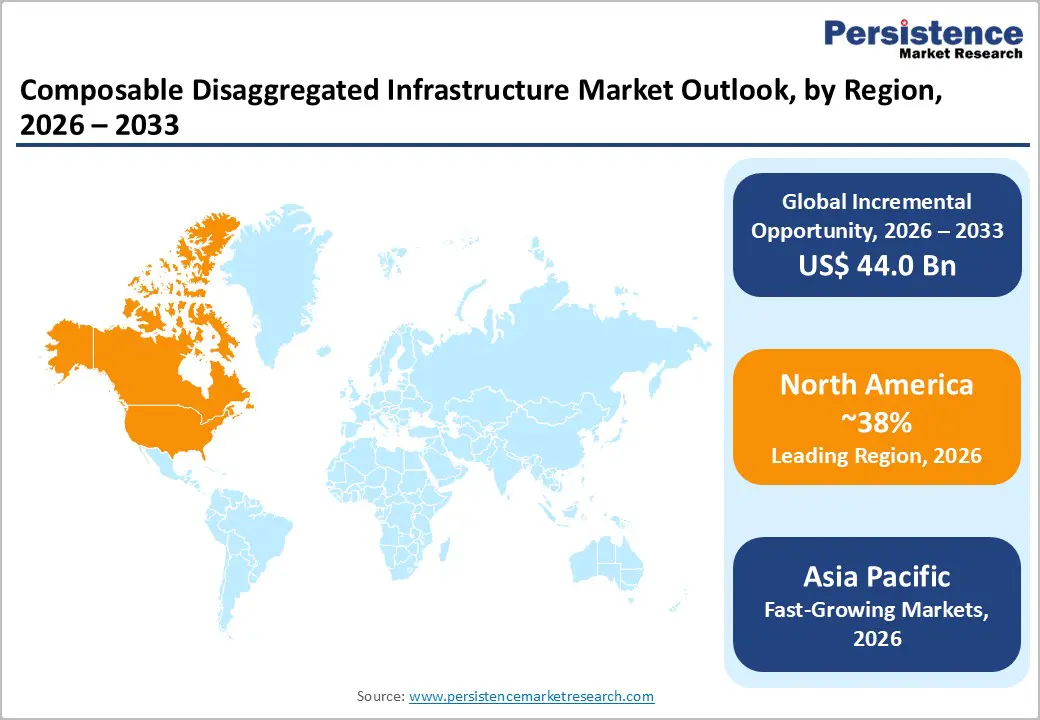

- Leading Region: North America dominates the Composable Disaggregated Infrastructure market with a 38% share in 2025, driven by strong U.S. hyperscale adoption and semiconductor investments.

- Fastest Growing Region: Asia Pacific, holding a 32% share in 2025, is the fastest-growing regional market, supported by rapid data center expansion across China, India, and Southeast Asia.

- Leading Component Category: Composable Software leads with a 42% share in 2025, driven by API-based orchestration, automation, and Infrastructure-as-Code enablement.

- Leading End-User Category: Cloud Providers account for 50% of the market share in 2025, fueled by scalable, multi-tenant cloud infrastructure requirements.

- Key Opportunity: The surge in edge computing and IoT deployments is creating major growth opportunities, as billions of connected devices require low-latency, dynamically disaggregated infrastructure.

| Key Insights | Details |

|---|---|

|

Composable Disaggregated Infrastructure Size (2026E) |

US$ 11.5 billion |

|

Market Value Forecast (2033F) |

US$ 55.5 billion |

|

Projected Growth CAGR (2026-2033) |

25.2% |

|

Historical Market Growth (2020-2025) |

23.7% |

Market Dynamics

Surging AI/ML and IoT-Driven Workloads Accelerating Demand for Dynamic, High-Performance Infrastructure

The explosive growth of AI and machine learning workloads is significantly driving demand for composable disaggregated infrastructure. Advanced AI training and inference require scalable GPU and CPU pooling beyond traditional fixed servers. With 75 billion IoT devices projected globally, massive real-time data generation necessitates low-latency, flexible resource allocation. Hyperscale data centers are increasingly adopting modular architectures to efficiently handle exaflop-scale AI training.

Composable infrastructure enables real-time recomposition of compute, storage, and networking resources, improving workload efficiency and reducing latency in performance-intensive environments. GPU disaggregation and dynamic scaling support AI clusters without hardware overprovisioning, lowering operational costs. As enterprises expand AI, analytics, and edge computing deployments, flexible infrastructure becomes critical for sustaining next-generation computing performance and scalability requirements.

Growing Emphasis on Energy Efficiency and Sustainable Data Center Operations

Rising sustainability mandates and power consumption concerns are further accelerating market adoption. Global data center electricity usage reached 460 TWh in 2022 and is projected to increase substantially, putting pressure on operators to improve energy efficiency. Composable disaggregation reduces stranded capacity by precisely matching resources to workloads, significantly lowering idle hardware consumption and improving power utilization effectiveness.

By optimizing hardware allocation, operators can reduce energy waste and carbon emissions while maintaining performance levels. Industry estimates indicate composable systems can reduce power usage by 25–40%, aligning with decarbonization targets and regulatory requirements. As energy costs rise and environmental policies tighten, sustainable, efficiency-focused infrastructure strategies are becoming a key driver for composable disaggregated infrastructure investments.

Restraints - Integration and Orchestration Complexity Limiting Enterprise-Scale Deployment of Disaggregated Architectures

High orchestration complexity remains a key restraint for the composable disaggregated infrastructure market. Managing dynamically pooled compute, storage, and networking resources requires advanced expertise in containerization and orchestration platforms such as Kubernetes. Many enterprises face internal skill gaps, which increase implementation timelines and raise integration risks, particularly when transitioning from legacy architectures.

The absence of universal standards for composable environments further complicates deployment, especially for non-hyperscale organizations. Integration with existing IT stacks can extend rollout cycles and inflate operational costs. Without mature automation frameworks and skilled personnel, enterprises may delay adoption, limiting near-term scalability benefits despite long-term efficiency gains.

Expanded Cybersecurity Risks in Highly Dynamic and Software-Defined Resource Pools

Dynamic recomposition of infrastructure resources increases cybersecurity exposure, acting as a significant adoption barrier. Disaggregated pools create broader attack surfaces, complicating zero-trust enforcement and micro-segmentation strategies. According to the National Institute of Standards and Technology, software-defined and distributed environments require enhanced monitoring and policy enforcement mechanisms.

The financial impact of breaches remains substantial, with the Ponemon Institute reporting average breach costs reaching $4.45 million in 2023. Highly regulated sectors operating under frameworks such as the General Data Protection Regulation remain cautious about adopting dynamic architectures, thereby slowing widespread enterprise deployment.

Opportunity - Rapid Expansion of Edge Computing and IoT Ecosystems Creating New Growth Avenues

The accelerating deployment of edge computing infrastructure presents strong growth opportunities for composable disaggregated systems. With billions of IoT connections generating real-time data, low-latency resource pooling at the edge becomes essential. Government initiatives such as the CHIPS and Science Act are allocating significant funding to strengthen advanced hardware ecosystems supporting distributed architectures.

Composable infrastructure enables localized scaling of compute and storage, reducing latency and improving workload efficiency at edge nodes. Performance benchmarks from Intel indicate substantial latency improvements through resource disaggregation. As cloud providers extend services closer to users, flexible edge-ready architectures are expected to command a premium growth trajectory through the forecast period.

Large-Scale Hyperscale Data Center Modernization Driving Retrofit and Service Demand

Ongoing hyperscale data center modernization initiatives offer significant service and integration opportunities. Major operators are transitioning toward modular rack-level disaggregation to enhance capacity utilization and scalability. The Open Compute Project, supported by companies such as Meta Platforms, promotes open, disaggregated rack designs to increase infrastructure efficiency.

Emerging digital transformation programs, including India’s Digital India, further accelerate demand for scalable architectures. According to projections from Gartner, a majority of new data centers are expected to adopt composable or software-defined designs, creating sustained long-term market expansion opportunities.

Category-wise Analysis

Component Insights

Composable Software leads the market with an estimated 42% share in 2025, driven by its central role in orchestration, automation, and API-enabled infrastructure control. Software platforms integrate with container ecosystems such as Kubernetes to enable Infrastructure-as-Code (IaC) and DevOps workflows. Deployments by companies such as Liqid and VMware show utilization rates of nearly 80%, highlighting the efficiency gains enabled by intelligent resource pooling.

Disaggregated Hardware is emerging as the fastest-growing segment, supported by increasing adoption of GPU pooling, CXL-enabled memory expansion, and high-speed fabric interconnects. As AI clusters and edge deployments expand, demand for modular compute and storage nodes is accelerating. Hardware innovation remains critical to unlocking the full performance benefits of composable environments.

Application Insights

IT & ITES dominates the application segment with a 35% share in 2025, fueled by cloud-native workloads and enterprise digital transformation initiatives. According to NASSCOM, India’s IT exports reached $194 billion in 2024, reflecting the scale of infrastructure demand. Composable systems help reduce downtime by nearly 50%, as highlighted by the Uptime Institute, making them attractive for service-driven enterprises.

Healthcare is projected to be the fastest-growing application segment, driven by rising adoption of AI diagnostics, telemedicine platforms, and data-intensive medical imaging systems. Hospitals and research institutions increasingly require flexible compute scaling to manage sensitive, high-volume datasets. The need for secure, low-latency infrastructure to support precision medicine and real-time analytics is accelerating adoption across healthcare ecosystems.

End-user Insights

Cloud providers lead the end-user segment with a 50% share in 2025, leveraging composable architectures to enhance scalability and multi-tenant efficiency. Major hyperscalers such as Amazon Web Services and Microsoft Azure use open hardware designs promoted by the Open Compute Project to achieve utilization rates of around 80%, compared to traditional averages of around 30%.

Enterprises represent the fastest-growing end-user category as organizations modernize legacy data centers to support hybrid and AI-driven workloads. The increasing demand for workload portability, automation, and cost optimization is encouraging enterprise IT teams to transition to composable environments. As digital transformation initiatives accelerate globally, enterprise adoption is expected to expand steadily.

Regional Insights

North America Composable Disaggregated Infrastructure Market Trends

North America leads the global market with an estimated 38% share in 2025, driven primarily by strong U.S. hyperscale adoption. Companies such as Microsoft and Google deploy disaggregated architectures aligned with Open Compute Project standards. Federal initiatives, including the CHIPS and Science Act, are strengthening semiconductor R&D and AI infrastructure investments.

Innovation ecosystems across Silicon Valley and other tech hubs are accelerating the development of AI-optimized racks, including collaborations between NVIDIA and Dell Technologies. Regulatory emphasis on energy efficiency, supported by agencies such as the Federal Communications Commission, further promotes sustainable, high-density data center modernization across the region.

Europe Composable Disaggregated Infrastructure Market Trends

Europe represents a technologically advanced market, projected to grow at a CAGR of approximately 22% through the forecast period. Germany leads regional adoption, supported by industrial digitalization initiatives from Siemens aligned with Industry 4.0 frameworks. Research institutions such as the Fraunhofer Society highlight efficiency gains from modular and automated infrastructure deployments.

Policy harmonization efforts, including the European Data Act and Gaia-X, promote interoperable cloud ecosystems. Cybersecurity guidance from the European Union Agency for Cybersecurity supports secure, energy-efficient data centers, with several operators achieving power usage effectiveness levels near 1.3 across advanced facilities.

Asia Pacific Composable Disaggregated Infrastructure Market Trends

Asia Pacific accounts for an estimated 32% market share in 2025 and represents the fastest-growing regional landscape. China drives large-scale deployments through hyperscalers such as Alibaba Group, supporting national digital expansion strategies. The Ministry of Industry and Information Technology continues to promote the growth of advanced data centers to support AI and cloud computing.

India and Japan are accelerating investments in edge and cloud infrastructure, with companies like NTT expanding regional data center footprints. Southeast Asian nations leverage manufacturing and smart city initiatives, while sustainability standards from Infocomm Media Development Authority encourage the adoption of green, energy-efficient composable architectures.

Competitive Landscape

The competitive landscape of the composable disaggregated infrastructure market is moderately consolidated, with leading vendors holding a significant portion of total revenue. Market leaders focus heavily on advanced R&D investments in ARM-based architectures, AI-optimized hardware, and high-speed interconnect technologies. Strategic collaboration with open hardware ecosystems and standards-based initiatives strengthens interoperability and accelerates large-scale deployments across hyperscale and enterprise environments. Key differentiation factors include open-source integration capabilities, software-defined orchestration strength, and infrastructure-as-a-service delivery models tailored for edge and hybrid deployments. Vendors are increasingly offering consumption-based and flexible financing options to attract enterprises seeking scalable, low-latency, and energy-efficient infrastructure solutions.

Key Developments:

- In April 2025, Dell Technologies unveiled disaggregated AI-optimized servers integrated with NVIDIA GB200 platforms at NVIDIA GTC, strengthening high-performance composable infrastructure portfolios designed for large-scale AI training and accelerated data center workloads.

- In February 2025, Hewlett Packard Enterprise introduced Gen12 ProLiant servers powered by Intel Xeon processors, enhancing modular compute performance, AI acceleration readiness, and energy-efficient architecture for enterprise and hyperscale composable deployments.

- In November 2024, Liqid launched the UltraStack L40S platform at SC23, integrating solutions from Dell Technologies and NVIDIA to deliver scalable GPU disaggregation for HPC and AI-driven environments.

Companies Covered in Composable Disaggregated Infrastructure Market

- Hewlett Packard Enterprise

- Dell Technologies

- Cisco Systems

- Lenovo

- IBM

- NetApp

- Super Micro Computer

- Liqid

- Western Digital

- Huawei Technologies

- Inspur

- Arista Networks

- NVIDIA

- Intel

- Quanta Cloud Technology

Frequently Asked Questions

US$ 11.5 billion in 2026, driven by accelerating AI, cloud, and hybrid infrastructure adoption.

Rising AI/ML workloads and sustainability goals, with composable systems improving utilization rates to over 70%.

North America leads with a 38% market share in 2025, supported by strong hyperscale and semiconductor investments.

Composable Software leads with a 42% share in 2025 due to orchestration and automation capabilities.

Major innovators include Hewlett Packard Enterprise, Intel, NVIDIA, VMware, Cisco Systems, and Dell Technologies.