- Medical Devices

- Compartment Syndrome Monitoring Market

Compartment Syndrome Monitoring Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Compartment Syndrome Monitoring Market, segmented by Device (Intra-Compartmental Pressure Monitoring Systems, Intramuscular Tissue Pressure Measuring (IMP) Catheters, Disposables/Accessories), Indication (Acute Compartment Syndrome, Chronic Compartment Syndrome, Abdominal Compartment Syndrome), Anatomy, End-user, and by Regional Analysis, 2025 - 2032

Compartment Syndrome Monitoring Market Share and Trends Analysis

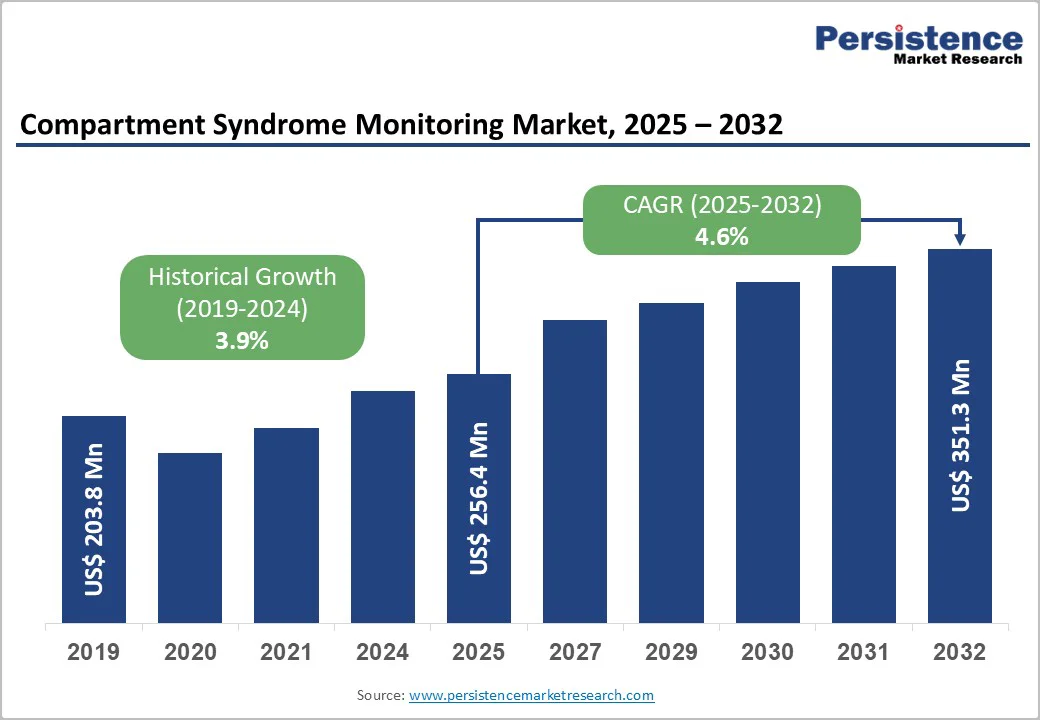

The global compartment syndrome monitoring market size is valued at US$ 256.4 million in 2025 and projected to reach US$ 351.3 million by 2032. The market is projected to record a CAGR of 4.6% during the forecast period from 2025 to 2032. Increasing burden of chronic illnesses needing ICU admissions, continuous monitoring, and mechanical ventilation are some of the key factors that lead to intra-abdominal hypertension and abdominal compartment syndrome. Incidence of chronic exertional compartment syndrome in patients suffering from leg pain was around 7.6% in the U.S., according to an article published in the PubMed journal.

Chronic compartment syndrome requires regular monitoring by healthcare professionals. It also affects people who regularly work out in the form of running, swimming, playing tennis, etc. Since many people around the world are opting to stay fit and exercise, the prevalence of this condition is increasing. Thus, it will positively impact compartment syndrome monitoring demand growth over the coming years.

Key Industry Highlights:

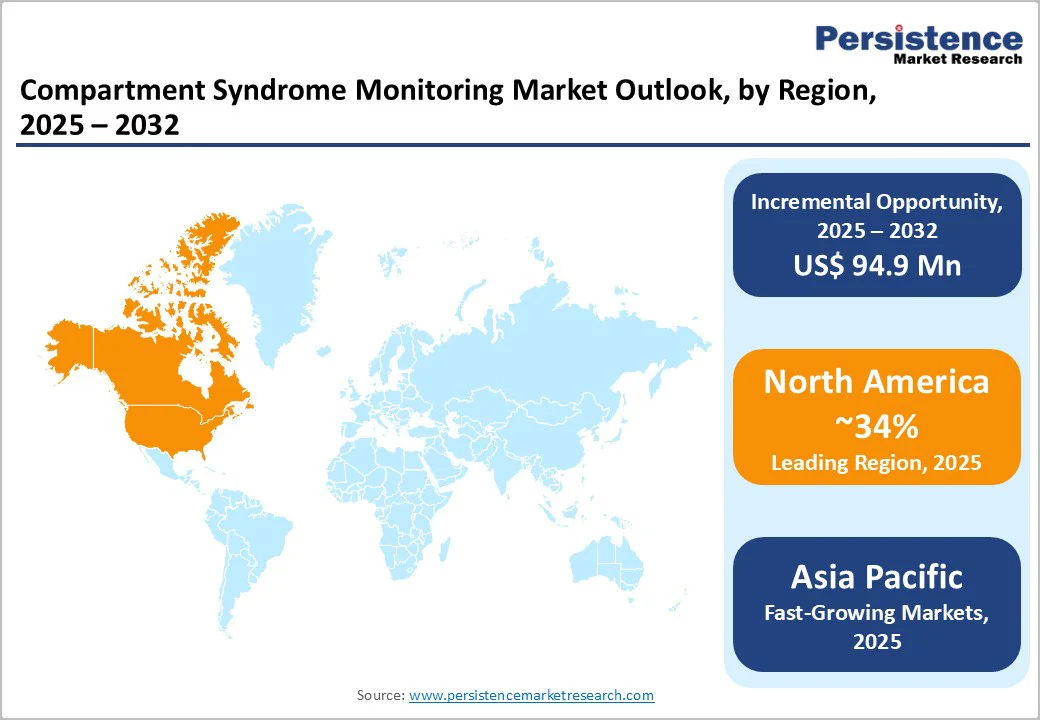

- Leading Region: North America remains the market leader, driven by well-established trauma care systems, high rates of orthopedic surgical procedures, and strong adoption of advanced pressure monitoring devices in hospitals and emergency centers.

- Fastest Growing Region: Asia Pacific is the fastest growing region, supported by rising trauma incidence, expanding orthopedic infrastructure, and increasing investments in emergency care technologies across China, India, and Southeast Asia.

- Dominant Segment: Intra-Compartmental Pressure Monitoring Systems dominate, owing to their critical role in early diagnosis and timely clinical decision-making to prevent irreversible tissue damage.

- Opportunity: Significant market opportunity lies in developing portable, minimally invasive, and user-friendly monitoring solutions designed for ambulatory surgical centers, sports medicine clinics, and remote care settings to broaden clinical access and adoption.

| Key Insights | Details |

|---|---|

|

Compartment Syndrome Monitoring Market Size (2025E) |

US$ 256.4 Mn |

|

Market Value Forecast (2032F) |

US$ 351.3 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

4.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.9% |

Market Dynamics

Driver - Rising Incidence of Acute Compartment Syndrome to Boost the Market

A key factor propelling growth in the compartment syndrome monitoring market is the rising incidence of acute compartment syndrome linked to trauma, high-impact injuries, and complex orthopedic procedures. Road accidents, industrial injuries, and sports-related fractures continue to increase worldwide, resulting in a larger patient pool at risk of developing compartment syndrome. As clinicians emphasize early identification to avoid irreversible muscle damage, nerve injury, or potential limb loss, the importance of precise intercompartmental pressure assessment has become more prominent in critical care and trauma settings.

Hospitals and emergency departments are recognizing that timely monitoring not only improves clinical outcomes but also reduces long-term rehabilitation costs. This growing awareness is encouraging healthcare providers to adopt accurate and reliable pressure-monitoring systems as part of their standard protocols. Technological progress has further strengthened market momentum, with modern devices becoming portable, user-friendly, and capable of providing continuous or near real-time pressure measurements. These improvements enable faster decision-making during emergencies and support broader utilization across orthopedic units, surgical centers, and sports medicine facilities. Collectively, the rise in injury-related cases and advancements that enhance diagnostic precision are driving sustained demand for compartment syndrome monitoring solutions.

Restraints - Limited Device Availability and Inadequate Reimbursement

A key restraint for the compartment syndrome monitoring market is the limited availability of specialized diagnostic devices. Only a few established systems, such as Stryker’s STIC pressure monitoring system, Centurion’s Compass Universal pressure transducer, innovative sensors from MY01, and Medline’s pressure monitoring solutions, are widely used. This narrow product portfolio limits clinical adoption, particularly in settings that seek diverse options or cost-effective alternatives. The medium pricing of these devices further restricts uptake in resource-constrained markets.

Additionally, compartment pressure monitoring is not recognized as a standalone procedure in many countries. It is often grouped under general critical care services, leading to a lack of dedicated reimbursement pathways. Insurance providers in several regions do not offer specific coverage for compartment syndrome monitoring, reducing hospitals’ willingness to invest in advanced systems. Inadequate reimbursement and limited device choices collectively hinder market expansion and may slow the adoption of modern monitoring technologies.

Opportunity - Growing Demand for Monitoring Solutions in Ambulatory and Office-Based Care Settings

The expanding adoption of compartment syndrome monitoring devices across ambulatory surgical centers (ASCs) and orthopedic office-based clinics presents a strong growth opportunity for the market. As the healthcare landscape shifts toward outpatient and same-day surgical procedures, clinicians increasingly require compact, easy-to-use monitoring systems that support early detection without relying solely on hospital-based equipment. This transition has opened a promising avenue for manufacturers to develop device portfolios specifically tailored for these decentralized care environments.

ASCs and orthopedic clinics are also placing greater emphasis on postoperative surveillance, especially for high-risk patients undergoing fracture fixation, tendon repairs, or sports injury interventions. By offering reliable and minimally invasive monitoring tools, suppliers can address these unmet needs and capture an expanding customer base. Additionally, ongoing awareness initiatives and hands-on training programs aimed at improving early clinical recognition of compartment syndrome are strengthening the role of monitoring in outpatient practices. As caregivers in these settings become more informed about the benefits of timely pressure assessment, demand for specialized devices is expected to rise steadily. Together, these trends create attractive opportunities for companies to broaden market penetration and generate new revenue streams outside traditional hospital systems.

Category-wise Analysis

By Product Insights

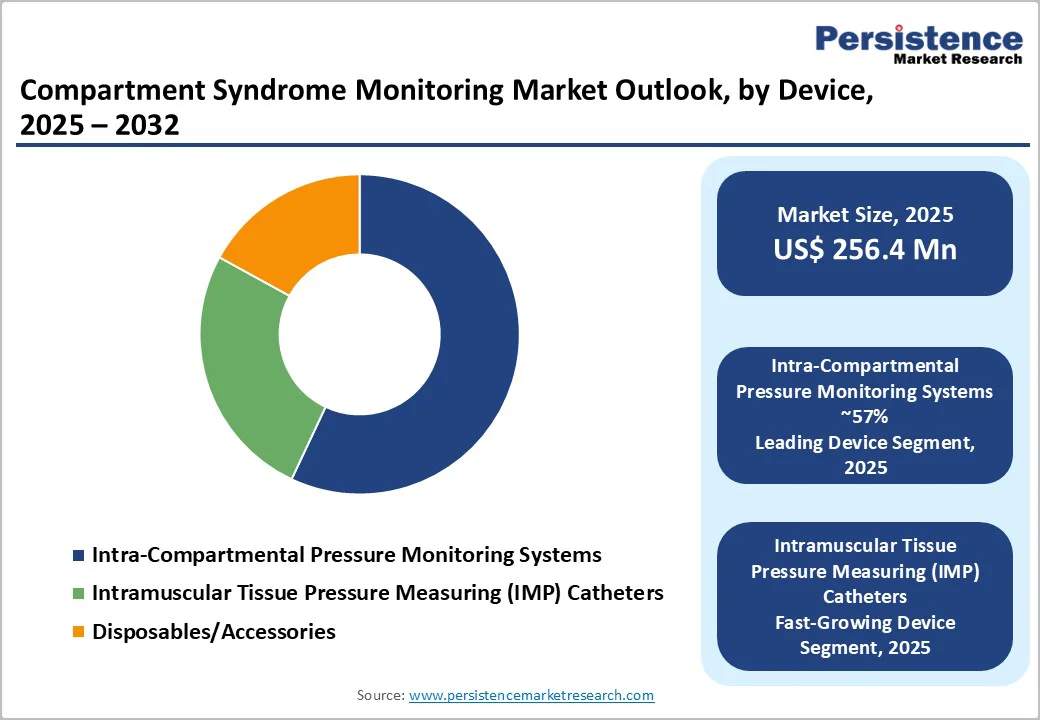

Intra-compartmental pressure monitoring systems hold a dominant 57% share of the market in 2024, reflecting their critical role in the timely and accurate diagnosis of compartment syndrome. These systems remain the preferred choice in emergency and orthopedic settings because they provide direct, reliable pressure measurements that help clinicians prevent irreversible tissue or nerve damage. Their strong adoption is further supported by continuous improvements in device accuracy, simplified handling, and compatibility with modern digital recording tools used across trauma centers and intensive care units. The growing burden of road traffic injuries and sports-related trauma also sustains the demand for these monitoring systems worldwide.

Among device categories, intramuscular tissue pressure measuring (IMP) catheters are emerging as the fastest-growing segment. Their minimally invasive nature, improved sensitivity, and suitability for continuous monitoring make them increasingly valuable in high-risk patients. Additionally, disposables and accessories used with pressure monitoring systems are gaining steady momentum, driven by repeated clinical use, infection-control requirements, and hospital preference for single-use components to ensure procedural safety and accuracy.

By Indication Insights

Acute compartment syndrome accounts for nearly 50% of the market share in 2025, placing it ahead of other indication types. Its dominance is closely tied to the urgent and high-risk nature of the condition, which can rapidly progress following fractures, crush injuries, and complex orthopedic surgeries. Because delays in diagnosis may lead to nerve impairment, muscle necrosis, or even limb loss, healthcare teams rely heavily on dedicated pressure monitoring systems to support early intervention. Hospitals, trauma centers, and emergency departments increasingly integrate these monitoring tools into standard trauma protocols, reinforcing the segment’s strong position.

The higher volume of trauma cases globally, combined with rising road accidents and sports-related injuries, further expands the demand for products tailored for acute presentations. The need for continuous and precise intracompartmental pressure assessment also encourages clinicians to adopt advanced monitoring systems that ensure timely decision-making. As a result, acute compartment syndrome continues to remain the primary clinical focus for device manufacturers, guiding product development and driving sustained market leadership in this segment.

Region-wise Insights

North America Compartment Syndrome Monitoring Market Trends

North America maintains a dominant position in the compartment syndrome monitoring market, largely driven by the U.S. Mature trauma systems, high healthcare spending, and an extensive network of trauma centers support widespread adoption of advanced monitoring devices. Severe traumatic injury remains a major public health concern: incidence of EMS-assessed severe trauma in selected North American regions has been reported at around 37 per 100,000 population annually. In the U.S., over 7 million patients were recorded in the National Trauma Data Bank (NTDB), highlighting the scale of trauma burden and the critical need for compartment monitoring.

Regulatory support from the FDA enables accelerated introduction of novel pressure-monitoring systems, reinforcing innovation. Moreover, regional adoption of digital and AI-driven monitoring tools is improving real-time diagnostic precision. Increasing awareness and training in trauma and orthopedic centers are helping integrate pressure monitoring into standard care pathways. As a result, North America’s leadership is reaffirmed by a confluence of clinical need, infrastructure, and a favourable regulatory framework.

Asia and Pacific Compartment Syndrome Monitoring Market Trends

Asia Pacific is emerging as the fastest-growing region in the compartment syndrome monitoring market, supported by rising trauma cases and expanding emergency care infrastructure across China, India, Japan, and ASEAN nations. Increasing road traffic accidents, industrial injuries, and sports-related trauma are creating a stronger need for timely intracompartmental pressure assessment. Governments across the region are investing in modernizing trauma centers and strengthening orthopedic care pathways, which is accelerating the adoption of monitoring devices.

Growing healthcare expenditure and broader access to advanced surgical procedures are further encouraging hospitals and specialty clinics to integrate reliable pressure-monitoring technologies into routine practice. Countries such as China and India also benefit from cost-effective manufacturing capabilities, enabling the development of locally produced devices tailored to regional budgets. Continued medical training programs, awareness initiatives on early detection, and partnerships between global device manufacturers and regional healthcare providers are collectively driving market expansion in Asia Pacific.

Competitive Landscape

The compartment syndrome monitoring market exhibits a moderately consolidated structure with a mix of established medical device companies and innovative startups. Leading players such as C2DX, MY01, Raumedic AG, ConvaTec Inc., Medline Industries, and Becton Dickinson & Company focus on product innovation, developing minimally invasive and connected monitoring systems. Competitive strategies include strategic partnerships, expanding geographic presence, and investment in research and development to enhance device accuracy and usability. Emerging business models emphasize integration with hospital IT systems and the introduction of AI-driven analytics for predictive diagnostics.

Key Industry Developments:

- In January 2024, C2Dx, in partnership with Shore Capital Partners, acquired Cook Medical’s full Otolaryngology/Head and Neck Surgery (OHNS) product portfolio.

- In December 2021, The MY01 Continuous Compartmental Pressure Monitor earned FDA approval for the Bluetooth-enabled MY01.

Companies Covered in Compartment Syndrome Monitoring Market

- C2DX

- MY01

- Raumedic AG

- ConvaTec Inc.

- Medline Industries

- Becton Dickinson & Company.

- Others

Frequently Asked Questions

The global compartment syndrome monitoring market is projected to be valued at US$ 256.4 Mn in 2025.

Key drivers include the rising incidence of acute compartment syndrome due to trauma and surgeries, technological advancements enabling minimally invasive.

The global market is expected to witness a CAGR of 4.6% between 2025 and 2032.

The expansion of minimally invasive and real-time continuous monitoring technologies and increased adoption in ambulatory surgical centers and orthopedic clinics present significant growth opportunities.

Leading companies include C2DX, MY01, Raumedic AG, ConvaTec Inc., Medline Industries, and Becton Dickinson & Company among others.