- Non-food Packaging

- Collation Shrink Film Market

Collation Shrink Film Market Size, Share, and Growth Forecast, 2026 - 2033

Collation Shrink Film Market by Material (Low-Density Polyethylene (LDPE), Linear Low-Density Polyethylene (LLDPE), Others), Thickness (25-50 microns, 50-100 microns, Others), Application, End-user, and Regional Analysis for 2026 - 2033

Collation Shrink Film Market Size and Trends Analysis

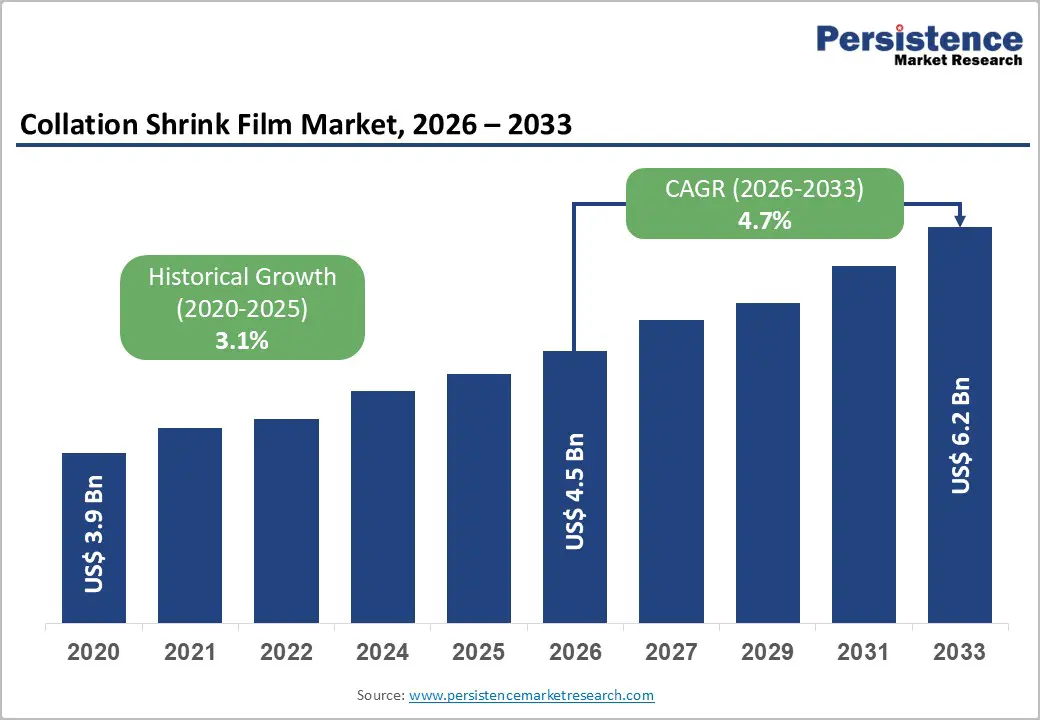

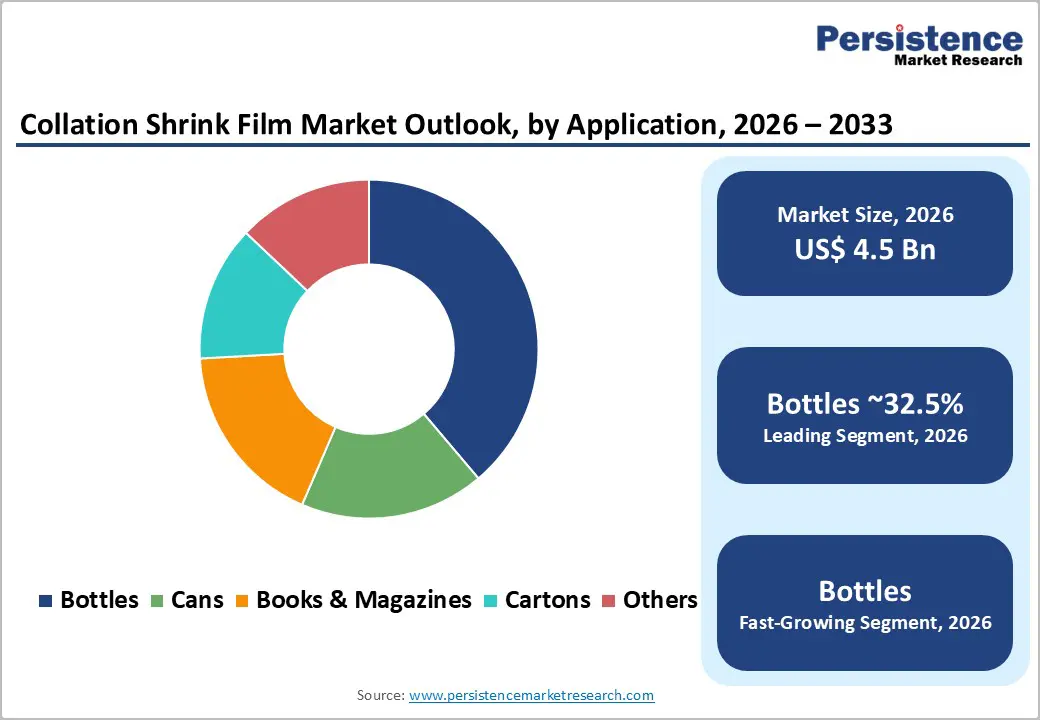

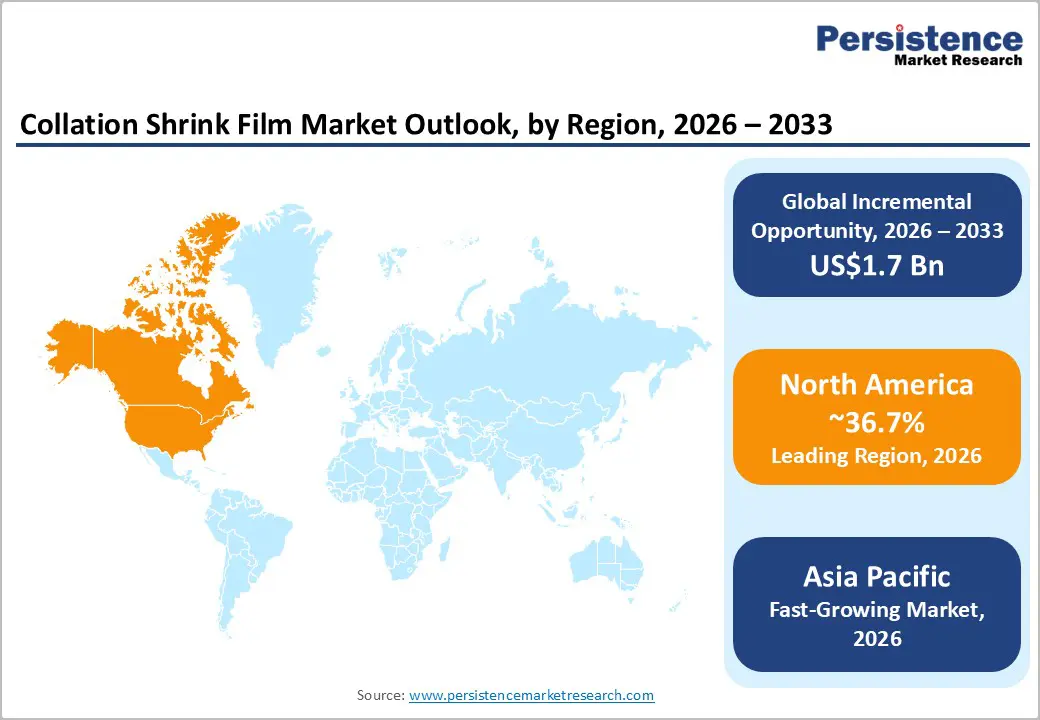

The global collation shrink film market size is likely to be valued at US$ 4.5 billion in 2026 and is expected to reach US$6.2 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033, driven by sustained multipack beverage consumption, automation in retail logistics, and rising regulatory emphasis on recyclable and recycled-content packaging.

Polyethylene-based films remain central due to strength-to-weight efficiency and compatibility with high-speed bundling lines. While raw-material volatility and recycled feedstock constraints present near-term margin pressure, the market outlook remains structurally stable. Strategic advantage will depend on downgauging innovation, validated food-grade PCR integration, and proximity to beverage production hubs.

Key Industry Highlights:

- Leading Region: North America is projected to hold approximately 36.7% of revenue share, driven by high beverage multipack penetration, automated bundling infrastructure, and strong retail logistics networks.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by expanding beverage production in China and high CAGR momentum in India due to urbanization and retail modernization.

- Investment Plans: Companies are prioritizing downgauging technologies, mono-PE recyclable film development, and PCR integration, alongside mechanical recycling capacity expansion across North America and Europe.

- Dominant Material: Low-Density Polyethylene (LDPE) is expected to lead with an anticipated 34.2% market share, supported by clarity, shrink consistency, and established global resin supply chains.

- Leading Application: Bottles are expected to dominate with an anticipated 32.5% of market share and are also the fastest-growing application segment due to rising beverage consumption in emerging economies, urbanization, and increasing demand for premium and functional beverages.

| Key Insights | Details |

|---|---|

| Collation Shrink Film Market Size (2026E) | US$4.5 Bn |

| Market Value Forecast (2033F) | US$6.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Multipack Beverage Demand and Retail Economics

The global beverage sector continues to anchor collation shrink film demand. Multipack formats such as six-pack bottled water, carbonated soft drinks, beer, and ready-to-drink beverages rely on shrink film for bundle stability and shelf presentation. Beverage producers increasingly substitute paperboard and corrugated secondary packaging with polyethylene shrink due to material efficiency and lower transport weight. High-volume beverage operations benefit from automated shrink bundling lines capable of maintaining consistent pack geometry at elevated throughput speeds. In mature retail markets, multipack formats represent a substantial portion of beverage sales, translating directly into recurring shrink film consumption. This structural reliance creates predictable volume growth aligned with packaged beverage demand and reinforces long-term supplier contracts with film converters.

E-commerce Growth and Logistics Automation

Retail transformation toward omnichannel fulfillment has increased demand for secure, tamper-resistant bundling formats. Shrink film provides consistent containment across distribution environments, including automated picking systems and palletized cross-border shipments. Automated shrink systems reduce dimensional variability compared with corrugate-based secondary packaging, optimizing cube efficiency in distribution centers. As grocery and consumer packaged goods companies modernize fulfillment operations, machine-applied collation film becomes integral to throughput and damage-reduction objectives. The business impact is structural rather than cyclical. Equipment investments in high-speed bundlers and shrink tunnels create long-term rollstock demand. Film suppliers offering validated performance testing, abuse-resistance optimization, and technical line integration services benefit from increased switching barriers and customer retention.

Regulatory and Corporate Sustainability Mandates

Packaging regulations across major economies increasingly require recyclability and minimum recycled content. Many jurisdictions mandate that packaging placed on the market meet recyclability thresholds by 2030. Corporate ESG commitments accelerate the adoption of post-consumer recycled (PCR) polyethylene within shrink film applications. Food-grade compliance requirements necessitate strict decontamination and validation processes, raising technical barriers but creating differentiated value propositions for certified suppliers. This dual push, regulatory and corporate, drives innovation in mono-material PE films compatible with existing recycling streams. The market effect is measurable: development pipelines prioritize downgauged mono-PE solutions and mechanically recycled blends designed to meet food-contact safety standards while preserving optical clarity and shrink performance.

Barrier Analysis - Recycled Feedstock Scarcity and Quality Variability

Food-grade PCR polyethylene remains constrained by collection inefficiencies and sorting limitations. Film waste streams are often contaminated, requiring advanced decontamination processes to achieve regulatory approval for food-contact use. Supply inconsistency leads to pricing premiums for certified PCR resins. These premiums compress converter margins and increase procurement complexity for brand owners with recycled-content commitments. In regions lacking advanced recycling infrastructure, film manufacturers face difficulty securing long-term, high-quality recycled feedstock at scale.

Polyolefin Price Volatility and Energy Costs

Collation shrink film production depends heavily on LDPE and LLDPE resins derived from ethylene feedstock. Resin prices fluctuate with crude oil markets and global supply-demand dynamics. Extrusion operations also consume substantial energy, exposing converters to electricity and natural gas price swings. Short-term price volatility reduces planning visibility and constrains capital allocation toward innovation. Firms without vertical integration or long-term resin contracts experience greater margin variability during commodity cycles.

Opportunity Analysis - Food-Grade PCR Commercialization

Scaling mechanically recycled polyethylene suitable for food-contact applications represents a high-impact growth avenue. Advancements in washing, deodorization, and melt filtration enable higher-quality recycled resin streams. Strategic partnerships between recyclers and converters provide traceability and certification assurance. Companies that secure offtake agreements for validated PCR resin gain supply predictability and regulatory compliance advantages. As beverage and FMCG brands set public recycled-content targets, demand for compliant shrink film grades will expand steadily through 2033.

Downgauging through LLDPE Blends

LLDPE-rich formulations enable enhanced tensile strength at lower thickness levels. Downgauging from heavier gauges to optimized 50-100 µm films reduces material consumption per bundle while maintaining load integrity. This transition lowers carbon intensity and shipping weight, aligning with corporate sustainability metrics. Technical validation across customer lines, especially beverage bottling facilities, reduces adoption friction. Over high-volume SKUs, small per-unit resin savings accumulate into significant cost reductions, creating compelling ROI for both converters and brand owners.

Retrofit and Line Optimization Services

Installed shrink bundling lines represent a large global asset base. Converters offering line diagnostics, tunnel optimization, and material compatibility testing can unlock incremental demand by facilitating transitions to downgauged or PCR-containing films. Bundled service contracts increase customer retention and generate recurring revenue streams. As throughput speeds rise, integrated technical support becomes a strategic differentiator.

Category-wise Analysis

Material Insights

Low-Density Polyethylene (LDPE) is anticipated to account for approximately 34.2% of market share in 2026, maintaining its leadership due to excellent clarity, balanced shrink performance, and a broad extrusion processing window. Beverage multipacks, particularly carbonated soft drinks and bottled water brands, prioritize optical transparency to enhance on-shelf branding visibility. LDPE’s consistent shrink behavior ensures tight pack formation around irregular bottle shapes, improving load stability during transport. Its low-temperature sealing characteristics reduce energy consumption in shrink tunnels, supporting cost-efficiency goals for large beverage bottlers. In practical applications, major beverage producers across North America and Europe commonly deploy LDPE-based shrink films for 6-pack and 12-pack bottled water formats. Blends incorporating minor Linear Low-Density Polyethylene (LLDPE) content further enhance puncture resistance while preserving shrink integrity. Well-established resin supply chains, especially in the U.S., the Middle East, and Western Europe, reinforce LDPE’s continued dominance across mature packaging markets.

Linear Low-Density Polyethylene (LLDPE) is projected to expand at a CAGR of 5.4%, emerging as the fastest-growing material category. Its superior tensile strength, puncture resistance, and load-bearing capacity make it ideal for downgauging initiatives, where film thickness is reduced without compromising mechanical performance. This aligns closely with global cost-optimization and sustainability strategies focused on reducing raw material consumption and transportation emissions. High-volume beverage programs increasingly shift toward LLDPE-forward blends to achieve measurable weight reductions while maintaining pack durability in high-speed automated bundling lines. For example, multinational beverage manufacturers are adopting 100% LLDPE shrink films for heavy multipacks such as 1.5-liter PET bottle bundles. Growth momentum is particularly strong in Asia Pacific and Latin America, where manufacturers prioritize material efficiency and carbon footprint reduction in line with evolving environmental regulations and corporate ESG targets.

Application Insights

Bottled beverages are anticipated to hold approximately 32.5% of the market share in 2026. Multipack shrink film remains the preferred secondary packaging solution for bottled water, carbonated soft drinks, juices, and ready-to-drink teas. Compared to corrugated trays, shrink film provides comparable load stability with significantly lower material weight and cost. Large-scale beverage production ensures consistent recurring demand. Major retailers and warehouse clubs frequently require palletized bottled multipacks, where shrink film provides both unitization and visual merchandising advantages. The growth of private-label bottled water brands across supermarket chains further strengthens this segment’s volume leadership.

The bottles segment is also projected to be the fastest-growing application. Rising beverage consumption in emerging economies, urbanization, and increasing demand for premium and functional beverages drive higher multipack volumes. Formats such as flavored sparkling water, energy drinks, and fortified beverages often launch in multipack configurations to improve shelf presence and sales velocity. Integration with automated high-speed bundling systems enhances production efficiency and supports large-scale retail distribution. Expanding modern trade networks in Asia Pacific and Latin America further accelerate adoption. Sustainability-driven initiatives, including lightweight PET bottle designs paired with downgauged shrink films, strengthen the long-term growth trajectory of bottled multipack applications.

Regional Insights

North America Collation Shrink Film Market Trends- High-Speed Beverage Multipacks and PCR Compliance

North America is projected to account for approximately 36.7% of revenue share in 2026, with the U.S. representing the largest share due to high beverage multipack penetration and a highly automated packaging infrastructure. Large beverage producers such as The Coca-Cola Company and PepsiCo operate extensive high-speed bottling networks that rely on LDPE- and LLDPE-based collation shrink films for 6-pack and 12-pack bottled water and carbonated soft drink formats. Warehouse retail formats led by Costco Wholesale and Walmart further reinforce demand for durable, load-stable multipacks designed for pallet display and club-store distribution.

Regulatory compliance remains a structural requirement. The U.S. Food and Drug Administration mandates strict food-contact documentation, particularly for films incorporating post-consumer recycled (PCR) content. This requirement has accelerated supplier validation programs and traceability investments. Material innovation is also visible at the converter level. For example, Berry Global has expanded recycled-content polyethylene film offerings, while Amcor continues investing in lightweight and recyclable flexible packaging solutions across North American beverage applications. Investments increasingly focus on downgauging technologies and resin-optimization strategies to mitigate price volatility tied to shale-based polyethylene production. Vertically integrated players with in-house extrusion capacity demonstrate stronger resilience during resin price cycles, strengthening long-term supplier consolidation in the region.

Europe Collation Shrink Film Market Trends - Circular Economy Mandates and Mono-PE Transition

Europe maintains a strong and structurally supported demand, shaped by regulatory harmonization that emphasizes recyclability and recycled content integration. Countries such as Germany, the United Kingdom, France, and Spain serve as primary consumption centers due to high beverage multipack penetration and advanced retail logistics networks. Pan-European sustainability frameworks, including Extended Producer Responsibility (EPR) systems, directly influence procurement decisions by beverage producers and retailers. Design-for-recycling principles are accelerating mono-material polyethylene film innovation. Under the broader framework of the European Commission Circular Economy Action Plan, packaging producers face rising pressure to ensure recyclability compatibility with mechanical recycling streams. As a result, converters are phasing out multi-material shrink structures in favor of mono-PE alternatives.

Industry collaborations illustrate this shift. Nestlé has publicly committed to increasing recycled plastic content across European packaging portfolios, influencing secondary packaging suppliers to develop compliant shrink films. Similarly, Carlsberg Group continues expanding sustainable multipack initiatives, including reduced-plastic and recyclable bundling formats in key European markets. Investment activity increasingly centers on mechanical recycling infrastructure expansion, particularly in Germany and the Netherlands, where new polyethylene recycling facilities are scaling output. These developments strengthen PCR availability for shrink film production, supporting regional circular economy objectives and stabilizing long-term supply chains.

Asia Pacific Collation Shrink Film Market Trends - Beverage Scale Expansion and Resin Cost Advantage

Asia Pacific is likely to be the fastest-growing regional market, supported by expanding beverage production capacity, urbanization, and retail modernization. China leads in absolute volume due to the scale of domestic beverage manufacturing, with major players such as China Resources Beverage and Tingyi Holding Corp operating high-output bottling networks that depend heavily on collation shrink films for water and ready-to-drink tea multipacks. India demonstrates one of the highest CAGRs in the region, supported by rising per capita packaged beverage consumption and the rapid expansion of modern retail chains. Global beverage brands, including Coca-Cola India and PepsiCo India continue expanding production lines and distribution networks, increasing demand for automated bundling systems and high-performance shrink films.

Manufacturing advantages, including competitive resin production in China and Southeast Asia, support lower conversion costs and export-oriented film production. Regional polymer producers such as Sinopec play a critical role in stabilizing polyethylene supply across Asia Pacific. Meanwhile, recycling infrastructure development remains uneven but shows measurable progress. Countries such as Japan and South Korea maintain advanced collection systems, while India and Southeast Asian markets are expanding mechanical recycling capacity through public-private partnerships. Strategic capacity expansion by local converters, often in collaboration with multinational beverage brands, strengthens regional self-sufficiency and positions Asia Pacific as both a high-growth consumption market and a competitive production hub for collation shrink films.

Competitive Landscape

The global collation shrink film market exhibits moderate concentration, with global packaging groups holding a significant share alongside numerous regional converters. Top players benefit from scale, integrated resin sourcing, and multinational beverage contracts. Regional specialists compete on cost efficiency and customer proximity.

Key strategies include material innovation, scale consolidation, vertical recycling partnerships, and line-integration services. Market leaders differentiate through certified food-contact compliance and validated downgauging performance guarantees.

Key Industry Developments

- In March 2025, SABIC partnered with Iyris and Napco National to use certified circular LLDPE from its TRUCIRCLE™ portfolio in greenhouse roofing films in Saudi Arabia, showcasing how circular PE resin can be used in durable film applications beyond food packaging while advancing regional sustainability and circularity initiatives.

Companies Covered in Collation Shrink Film Market

- Amcor

- Berry Global

- Sealed Air

- Coveris

- Winpak

- Clondalkin Group

- Clysar

- Polifilm

- RKW Group

- Intertape Polymer Group

- Sigma Plastics Group

- Charter Next Generation

- Scientex Berhad

- Jindal Poly Films

- Toray Plastics

- Dow Inc.

- ExxonMobil

- SABIC

Frequently Asked Questions

The global collation shrink film market is estimated to be valued at US$4.5 billion in 2026.

The collation shrink film market is projected to reach approximately US$6.2 billion by 2033.

Key trends include downgauging initiatives using LLDPE blends, integration of post-consumer recycled (PCR) content, mono-PE recyclable film development, automation-compatible high-performance films, and regional recycling infrastructure expansion across North America and Europe.

Low-Density Polyethylene (LDPE) is the leading material segment, holding an anticipated 34.2% market share, due to its clarity, shrink consistency, and established global supply chain availability.

The collation shrink film market is expected to grow at a CAGR of approximately 4.7% between 2026 and 2033.

Major players with strong product portfolios and global presence include Amcor, Berry Global, Sealed Air, RKW Group, and Dow Inc.