- Pharmaceuticals

- Collagen Skin Matrix Market

Collagen Skin Matrix Market Size, Share, and Growth Forecast, 2026-2033

Collagen Skin Matrix Market by Product (Animal-Derived, Synthetic, Hybrid), End-Use (Hospitals & Surgical Centers, Wound Care Clinics, Aesthetic Clinics), Use Case (Chronic Wounds, Burns, Surgical Reconstruction, Scar Revision, Cosmetic Use), and Regional Analysis for 2026-2033

Collagen Skin Matrix Market Share and Trends Analysis

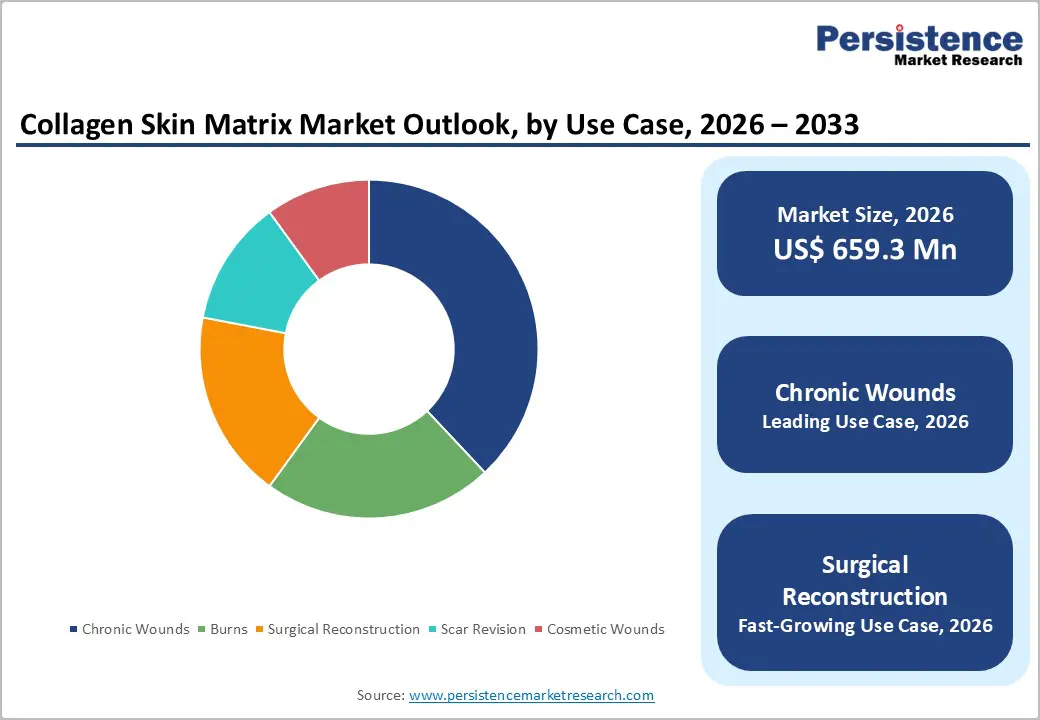

The global collagen skin matrix market size is likely to be valued at US$ 659.3 million in 2026, and is projected to reach US$ 976.1 million by 2033, growing at a CAGR of 5.8% during the forecast period 2026–2033.

Market growth is primarily driven by the increasing prevalence of chronic wounds, diabetic ulcers, and burn injuries, which have created a pressing need for advanced wound care solutions. Simultaneously, hospitals, surgical centers, and aesthetic clinics are adopting innovative collagen-based products at an accelerated pace to improve healing outcomes, reduce recovery times, and enhance patient satisfaction. Technological advancements in synthetic and hybrid collagen matrices, including bioengineered scaffolds and growth factor integration, have significantly enhanced product efficacy. Furthermore, government incentives, reimbursement support, and rising awareness of minimally invasive surgical reconstruction and scar revision procedures are fueling widespread adoption.

Key Industry Highlights

- Dominant Product: Animal-derived collagen is set to command around 45% revenue share in 2026, while hybrid matrices are likely to grow the fastest through 2033, driven by technological advancements in bioengineered scaffolds.

- Leading Use Case: Chronic wounds are anticipated to hold roughly 38% of the revenue share in 2026, while surgical reconstruction is set to record the highest 2026-2033 CAGR of 6.2%, driven by increasing burn incidents worldwide.

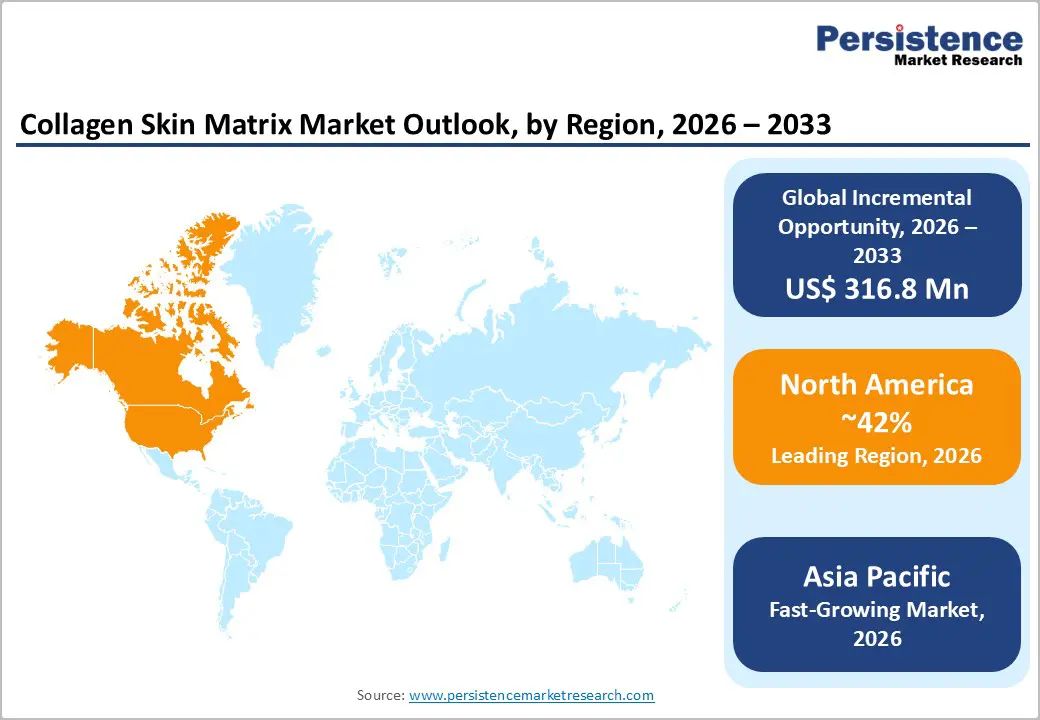

- Regional Leadership: North America is poised to dominate with an estimated 42% share in 2026, driven by advanced healthcare infrastructure and favorable reimbursement policies.

- Major Drivers: Market growth is primarily supported by rising chronic wounds and burns, technological innovations, and expanding adoption in cosmetic and aesthetic applications.

| Key Insights | Details |

|---|---|

| Collagen Skin Matrix Market Size (2026E) | US$ 659.3 Mn |

| Market Value Forecast (2033F) | US$ 976.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Incidence of Chronic Wounds and Burns

Globally, chronic wounds, including diabetic foot ulcers, venous leg ulcers, and pressure sores, continue to rise, with the World Health Organization (WHO) recognizing long-term wound care as a growing public health priority. Burn injuries remain prevalent due to industrial accidents, domestic hazards, and increasing urbanization, placing significant treatment demands on hospitals and healthcare systems. Hospitals and specialized wound care facilities increasingly adopt collagen skin matrix solutions to improve tissue regeneration, reduce infection risk, and minimize healing time. Adoption is further accelerated as clinicians seek to meet patient expectations for faster recovery and reduced complications.

In 2025, the U.S. Centers for Medicare & Medicaid Services (CMS) finalized updates to the Physician Fee Schedule, grouping skin substitutes and advanced wound products under adjusted reimbursement classifications for 2026. These changes are designed to streamline access in outpatient and clinic settings, thereby strengthening the economic case for advanced wound management products such as collagen matrices. With rising chronic disease prevalence, aging populations, and policy support for wound care reimbursement, demand for collagen-based matrices continues to accelerate across hospitals, wound care centers, and specialized clinics, highlighting a sustained growth trajectory.

Technological Advancements and Expanding Clinical Adoption

Technological innovation in collagen matrix design, including synthetic and hybrid matrices with enhanced biomechanical properties and optimized degradation profiles, has significantly improved clinical efficacy for both wound healing and reconstructive applications. These advanced matrices allow clinicians to manage complex wounds and surgical sites with greater confidence, consistent tissue integration, and reduced scarring. The improved performance has also increased adoption in aesthetic clinics for scar revision and cosmetic procedures, expanding market reach beyond traditional hospital settings.

The U.K. National Health Service (NHS) announced expanded evaluation programs for advanced wound care technologies, including next-generation bioactive matrices, to standardize care pathways for chronic wound treatment. Meanwhile, Canada’s Health Canada regulatory authority has streamlined review timelines for advanced biologic wound products, supporting faster clinical availability. These regulatory developments, coupled with enhanced product performance, enable hospitals, surgical centers, and outpatient clinics to adopt collagen matrices more rapidly, reinforcing their role as a critical component of modern wound management and reconstructive therapy.

Prohibitive Product Costs

Collagen skin matrices, particularly hybrid and synthetic variants, remain highly cost-intensive, with unit prices ranging from US$1,500 to US$3,000 per treatment. These elevated costs limit adoption in smaller wound care clinics and in developing regions where healthcare budgets are constrained. Cost sensitivity is further compounded by variable reimbursement policies across countries, making widespread procurement challenging even for mid-sized hospitals and outpatient facilities. Providers in price-conscious healthcare systems often opt for lower-cost traditional dressings despite superior outcomes with advanced products.

The reimbursement structures for advanced wound care products are under scrutiny by policy makers such as the U.S. CMS, which in late 2025 reported changes to the Calendar Year 2026 Medicare Physician Fee Schedule that adjust payment methodologies for skin substitutes. These shifts have the potential to limit profitability and reduce financial incentives for providers to adopt high-cost collagen matrices. In many regions, limited insurance coverage and reimbursement classifications that do not fully reflect clinical value continue to restrain product adoption, especially in low-income and underfunded healthcare settings.

Regulatory and Supply Chain Challenges

Collagen-based products must navigate stringent regulatory pathways from authorities such as the U.S. Food and Drug Administration (FDA), European Medicines Agency (EMA), and Japan’s PMDA, which can delay market entry by 12–18 months or more. These approvals require extensive clinical evidence and stringent safety validation, increasing compliance costs and development timelines. Even after FDA clearance is achieved, as with recent approvals for specific collagen matrices, the broader regulatory landscape remains a significant deterrent to rapid innovation and market entry across multiple countries.

In addition to regulatory hurdles, manufacturing and supply chain vulnerabilities heighten operational risks. For example, securing high-quality animal-derived collagen and maintaining sterile production environments involves specialized processes with long lead times. Despite recent expansions in U.S. collagen production capabilities, such as MPM Medical’s FDA 510(k)-cleared manufacturing platform in Texas, supply reliability remains a constraint for many manufacturers due to infrastructure and logistic challenges. These factors collectively limit immediate market scalability, requiring companies to carefully mitigate risks and plan for compliance to ensure consistent product availability across key geographies.

Expansion in Emerging Healthcare Markets

Emerging healthcare markets in the Asia Pacific and Latin America are increasingly prioritizing infrastructure investment and access to advanced care technologies. Governments are expanding public hospital networks and upgrading wound care facilities, enhancing the availability of modern treatments for chronic wounds and burns. In India, nationwide healthcare initiatives aim to expand access to primary and specialty care, thereby supporting the adoption of innovative wound management solutions. As clinical awareness grows, these regions present actionable avenues for manufacturers to establish early footholds in high-growth environments.

Several countries are strengthening public health programs that address diabetes and vascular disease, conditions directly linked to chronic wound prevalence. For example, India’s National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke (NPCDCS) has expanded its screening and management initiatives at primary and community health centers, increasing early detection and care of diabetes-related foot ulcers. Similarly, Australia’s National Strategic Framework for Chronic Conditions includes funding for integrated care pathways to reduce non-healing wounds among at-risk populations. Combined with expanding private hospital and aesthetic clinic chains, these developments position collagen matrices as essential tools in addressing treatment gaps, reflecting a sustainable and long-term opportunity for market expansion.

Policy Support and Clinical Innovation for Advanced Therapies

Policy and payment reforms in major healthcare systems are creating openings for broader clinical adoption of advanced wound care and regenerative technologies. In the U.S., the CMS finalized the 2026 Medicare Physician Fee Schedule, which includes expanded reimbursement for select skin substitutes and tissue-based products, enhancing access in both hospital and outpatient settings. This change standardizes payment for novel wound care technologies, supports broader utilization of advanced matrices across varied care settings, and encourages hospitals to prioritize innovation in patient treatment protocols.

Complementing reimbursement shifts, the FDA-recognized New Technology Add-On Payment (NTAP) designation for regenerative devices such as the RECELL System, which promotes improved wound healing and lower donor site burden, has been extended through 2026, encouraging hospitals to adopt next-generation approaches. Such incentives reduce cost barriers and align payer frameworks with clinical innovation, strengthening the case for advanced collagen-based matrices. As governments and health systems emphasize value-based care, outcomes-driven reimbursement, and innovative clinical practices, these policy movements provide a compelling catalyst for premium wound care solutions and drive long-term market adoption.

Category-wise Analysis

Product Type Insights

Animal-derived collagen matrices are expected to remain the leading product segment, capturing an estimated 45% of global revenue in 2026, driven by their proven clinical efficacy, high biocompatibility, and trusted performance in chronic wound and burn care. Widely adopted in hospitals and wound care centers, these matrices provide reliable structural support for complex tissue regeneration and integrate seamlessly into standardized treatment protocols.

In 2025, Yale New Haven Hospital’s wound care program reported expanded use of animal-derived collagen matrices for diabetic foot ulcer management, combining them with advanced therapies to improve healing outcomes. This real-world adoption reinforces steady demand, clinician familiarity, and consistent integration across care settings.

Synthetic collagen matrices are anticipated to be the fastest-growing product, projected to expand at a 6.5% CAGR through 2033, driven by superior mechanical strength, reduced immunogenicity, and integration with regenerative growth factors. These matrices are increasingly used in surgical reconstruction and cosmetic scar revision, where performance gains improve tissue healing and aesthetic outcomes. Mount Sinai Health System in New York incorporated hybrid collagen matrices into reconstructive burn surgeries, reporting faster recovery and reduced complications compared with traditional matrices.

Growing clinician confidence in these advanced materials is driving adoption across specialized surgical and aesthetic clinics, highlighting their role as a high-value, innovative product segment.

Use Case Insights

Chronic wounds are likely to dominate with an estimated 38% of the collagen skin matrix market revenue share in 2026, driven by the rising prevalence of diabetic foot ulcers, venous leg ulcers, and pressure sores. These wounds require long-term management, often involving multiple treatment modalities, where collagen matrices provide effective structural support to guide cellular repair and reduce infection risk. Their role in accelerated healing reinforces their leadership within wound care treatment protocols.

Supporting this, the expansion of specialized wound care clinics in 2026, such as the new Complete Wound Care LLC clinic in New Haven near Yale New Haven Hospital, which prioritizes chronic wound treatment with holistic care, including infection screening and advanced therapies, reflects sustained clinical focus on specialized chronic wound approaches. This indicates active investment in chronic wound care infrastructure and broadens the channels through which collagen products are utilized.

Surgical reconstruction emerges as the fastest-growing use cases with an approximate 6.2% CAGR, driven by technological improvements in hybrid and synthetic matrices that enhance regeneration in severe injury and surgical sites. These developments support faster integration into reconstructive procedures and complex burn care, where durable mechanical support and optimized healing responses are crucial for clinical success. Cosmetic applications are also expanding steadily due to patients’ growing interest in minimally invasive procedures and aesthetic outcomes.

Clinics offering aesthetic reconstruction and scar revision are increasingly incorporating performance-enhanced matrix products into service lines, reflecting broader acceptance beyond traditional therapeutic domains.

Regional Insights

North America Collagen Skin Matrix Market Trends

North America is anticipated to command around 42% of the collagen skin matrix market share in 2026. The United States leads due to its expansive healthcare infrastructure, advanced clinical practices, and a favorable reimbursement environment that encourages adoption of advanced wound care solutions in hospitals and outpatient facilities. Hospitals and surgical centers remain the dominant end users, with aesthetic and specialty clinics increasingly integrating collagen matrices into care protocols for scar revision and reconstructive procedures. The region also benefits from a mature R&D ecosystem, which fosters continuous innovation and new product development to meet evolving clinical needs.

In 2025, Convatec received regulatory approval for its ConvaNiox™ nitric oxide-based multimodal wound dressing, enhancing treatment effectiveness for diabetic foot ulcers, a chronic wound category with significant clinical burden; this product demonstrated up to 60% improved healing compared to standard care, reflecting real-world innovation in advanced wound care solutions. Such product approvals and strong clinical results are driving the adoption of cutting-edge wound therapies across North American medical institutions, further solidifying the region’s leadership role. Hospitals are increasingly using these advanced therapies as part of integrated care pathways to reduce hospital stays and improve patient outcomes.

Europe Collagen Skin Matrix Market Trends

The European market is anchored by demand from Germany, the U.K., France, and Spain. Strong healthcare systems with established chronic wound care protocols support widespread adoption, while regulatory harmonization via the European framework ensures consistent safety and quality standards. Hospitals remain the largest purchasers of advanced wound care products, while specialized clinics in aesthetic and reconstructive surgery progressively integrate innovative matrices into treatment regimens. Aging populations and higher chronic disease prevalence further sustain demand for collagen-based therapies in both hospital and outpatient settings.

A key industry development in 2025 was the 35th Conference of the European Wound Management Association (EWMA) held in Barcelona, which brought together clinicians, researchers, and industry leaders to share best practices and new wound care technologies. This event highlighted evidence-based approaches to managing chronic wounds and accelerated professional awareness and the integration of advanced products, including collagen matrices, across multiple European healthcare systems. Companies used the conference to showcase real-world clinical outcomes and new matrix formulations, promoting broader adoption and reinforcing market growth momentum.

Asia Pacific Collagen Skin Matrix Market Trends

Asia Pacific is projected to be the fastest-growing regional market, expanding at a 7.1% CAGR between 2026 and 2033, led by China, Japan, and India. Rising chronic disease incidence, expanding hospital and clinic infrastructure, and increasing uptake of aesthetic care contribute to accelerating demand for collagen matrices in therapeutic and cosmetic applications. Governments and healthcare providers across the region are prioritizing modernization of wound care services to address traumatic injuries, chronic ulcers, and surgical wound management. Growing awareness among clinicians and patients about advanced therapies is further boosting adoption rates in both urban and semi-urban centers.

Regional market data showed that advanced wound care products, including collagen matrices, held the largest share of the Asia Pacific wound care market, driven by investments in clinical effectiveness and technology adoption across major healthcare facilities in China, Japan, and India. This trend underscores the region’s improving access to modern wound care and increasing procurement of advanced therapies as healthcare systems mature and clinical awareness deepens. Regional healthcare conferences and government-led initiatives promoting best practices in wound care are further encouraging integration of collagen-based solutions into standard treatment pathways.

Competitive Landscape

The global collagen skin matrix market structure is moderately consolidated, with leading players such as Integra LifeSciences, 3M, Medtronic, Smith & Nephew, and CollPlant collectively controlling a significant portion of market revenue. These companies leverage their strong hospital and surgical center relationships, regulatory expertise, and integrated product portfolios spanning animal-derived, synthetic, and hybrid collagen matrices. Heavy investment in R&D enables leadership in advanced regenerative technologies, bioengineered scaffolds, and innovative wound care solutions that improve clinical outcomes and accelerate tissue regeneration.

Regional and niche competitors, including Acelity (part of 3M), Mölnlycke, and Terumo, focus on specialized therapeutic segments or local markets, often targeting chronic wounds, burns, and aesthetic procedures. Entry barriers, such as stringent regulatory approvals, complex manufacturing processes, and clinical validation requirements, limit new entrants. However, growing digitalization and adoption of data-driven wound care platforms allow software-supported clinical decision-making tools to complement collagen matrix therapies. Market consolidation is expected to increase gradually as leading companies acquire smaller players to expand geographically and technologically, while partnerships between regenerative therapy innovators and hospital networks enhance the adoption of advanced collagen solutions globally.

Key Industry Developments

- In March 2026, StimLabs launched Architect Fx, an advanced collagen matrix wound-care device derived from equine pericardium and cleared under the U.S. FDA 510(k) pathway. The product is designed to treat complex wounds, including diabetic ulcers, venous leg ulcers, pressure injuries, and surgical wounds.

- In September 2025, BioLab donated US$ 2.2 million to Arizona State University to fund the BioLab Sales and Innovation Lab, scholarships, and professional development, supporting biotech research and workforce training in advanced wound care.

- In May 2025, researchers at PASCH Hydrogel in India developed a silk fibroin–collagen-like hydrogel for chronic wounds, diabetic ulcers, and burns, accelerating tissue repair, reducing inflammation, and providing a biodegradable platform for next-generation wound healing.

Companies Covered in Collagen Skin Matrix Market

- Integra LifeSciences

- Organogenesis

- Smith & Nephew

- MTF Biologics

- BioTime

- AlloSource

- B.Braun Melsungen AG

- Coloplast A/S

- Terumo Corporation

- Medtronic plc

- Organica Biotech

- Hyland’s Biotech

- Cytomedix

Frequently Asked Questions

The global collagen skin matrix market is projected to reach US$ 659.3 million in 2026.

Growing chronic wounds and burns prevalence, technological advances in hybrid and synthetic matrices, and growing aesthetic and cosmetic applications drive the market.

The market is poised to witness a CAGR of 5.8% from 2026 to 2033.

Expansion into emerging markets and integration with regenerative medicine therapies represent key opportunities.

Integra LifeSciences, 3M, Medtronic, Smith & Nephew, and CollPlant are some of the key market players.