- Pharmaceuticals

- COPD Therapeutics Market

COPD Therapeutics Market Size, Share, and Growth Forecast, 2026 - 2033

COPD Therapeutics Market by Drug Class (Bronchodilators, Corticosteroids, Combination Therapies, Phosphodiesterase (PDE) Inhibitors, Biologics, Mucolytics & Adjunct Therapies), Route of Administration (Inhalation, Oral, Injectable/Parenteral), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Pharmacies), and Regional Analysis for 2026 - 2033

COPD Therapeutics Market Share and Trends Analysis

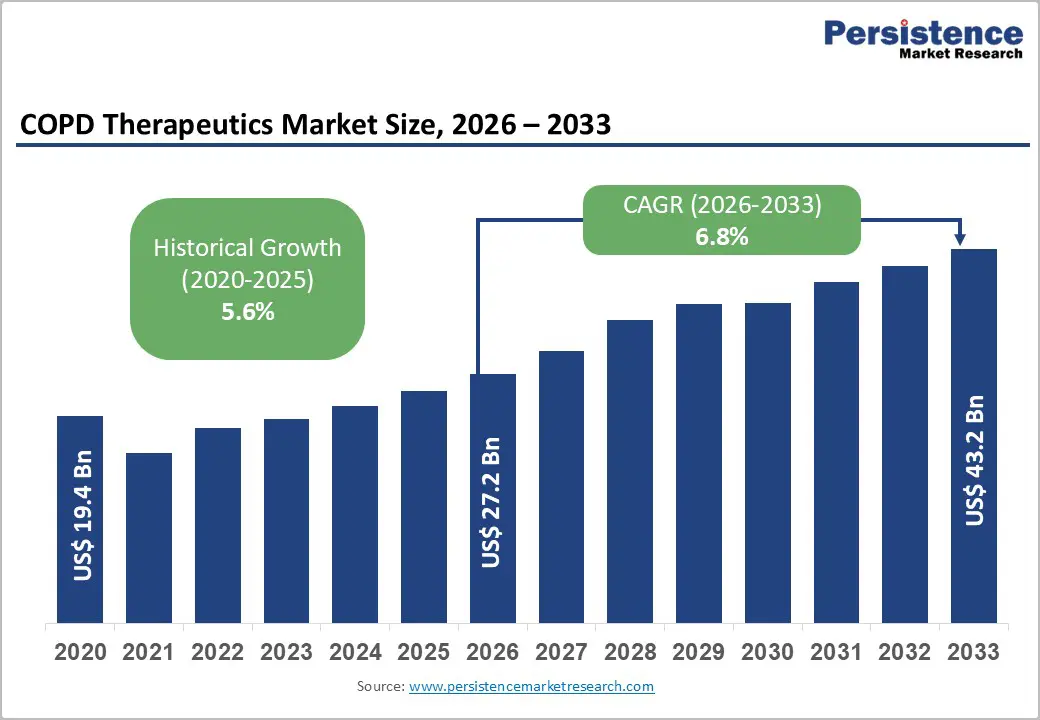

The global COPD therapeutics market size is likely to be valued at US$ 27.2 billion in 2026, and is estimated to reach US$ 43.2 billion by 2033, growing at a CAGR of 6.8% during the forecast period 2026 - 2033.

The market is expanding as demographic aging, improving diagnosis rates, and treatment innovation are increasing both patient volumes and therapy intensity. The disease burden is remaining substantial, with more than 390 million individuals affected globally according to the Global Burden of Disease Study, while the World Health Organization (WHO) continues to classify chronic obstructive pulmonary disease (COPD) among the leading causes of mortality. Aging populations across North America, Europe, and East Asia are driving higher treatment prevalence, as older adults are known to experience cumulative lung damage and comorbidities that require long-term pharmacological management. Emerging economies are reporting rising diagnosis rates as healthcare access is improving and environmental exposure risks such as urban air pollution and biomass fuel combustion are increasing disease incidence.

Clinical practice evolution is further accelerating market expansion, with treatment guidelines increasingly recommending earlier use of combination therapies and phenotype-specific interventions. The Global Initiative for Chronic Obstructive Lung Disease (GOLD) is promoting escalation toward dual and triple therapy regimens to reduce exacerbations and hospitalizations, which is increasing per-patient treatment costs. Novel drug classes such as dual phosphodiesterase (PDE) inhibitors and biologic monoclonal antibodies are entering treatment pathways for severe or inflammation-driven disease subsets, shifting revenue toward high-value specialty therapeutics.

Key Industry Highlights

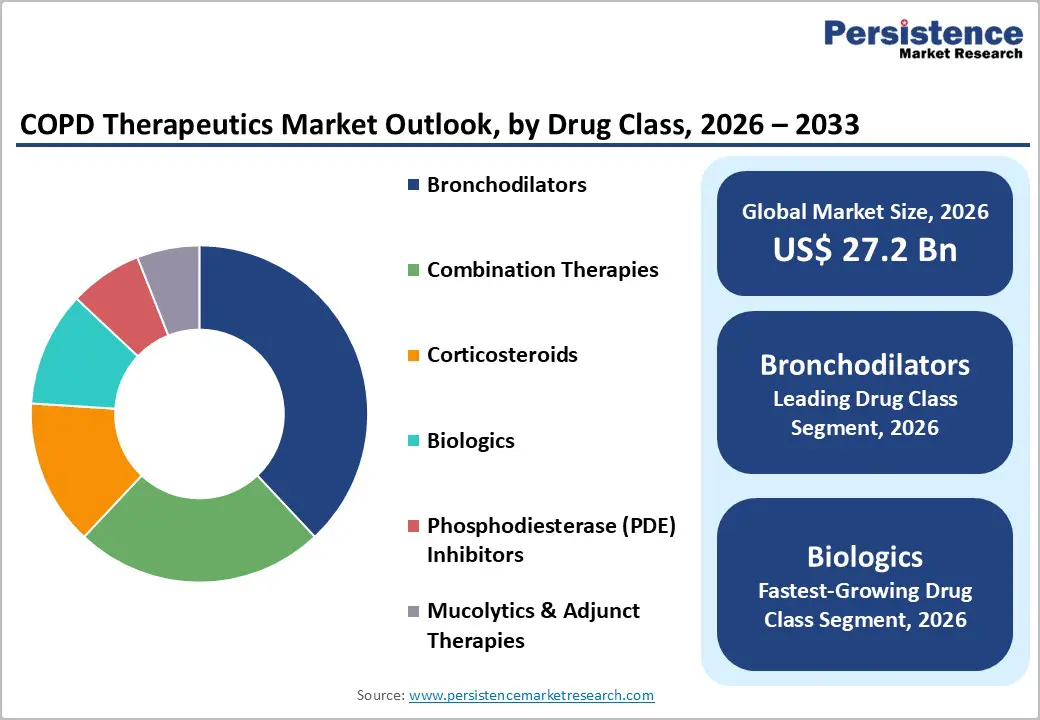

- Drug Class Leadership: Bronchodilators are expected to lead with nearly 38% market share in 2026 due to their first-line treatment role.

- Fastest-growing Drug Class: Biologic therapies are anticipated to record the fastest growth at an estimated 12.5% CAGR through 2033, driven by precision medicine adoption.

- Route of Administration Dominance: Inhalation therapies are projected to dominate with approximately 72% revenue share in 2026 owing to established clinical use and device familiarity

- Fastest-growing Administration Route: Injectable therapies are likely to expand the fastest at roughly 11.2% CAGR through 2033, as monoclonal antibody treatments gain traction.

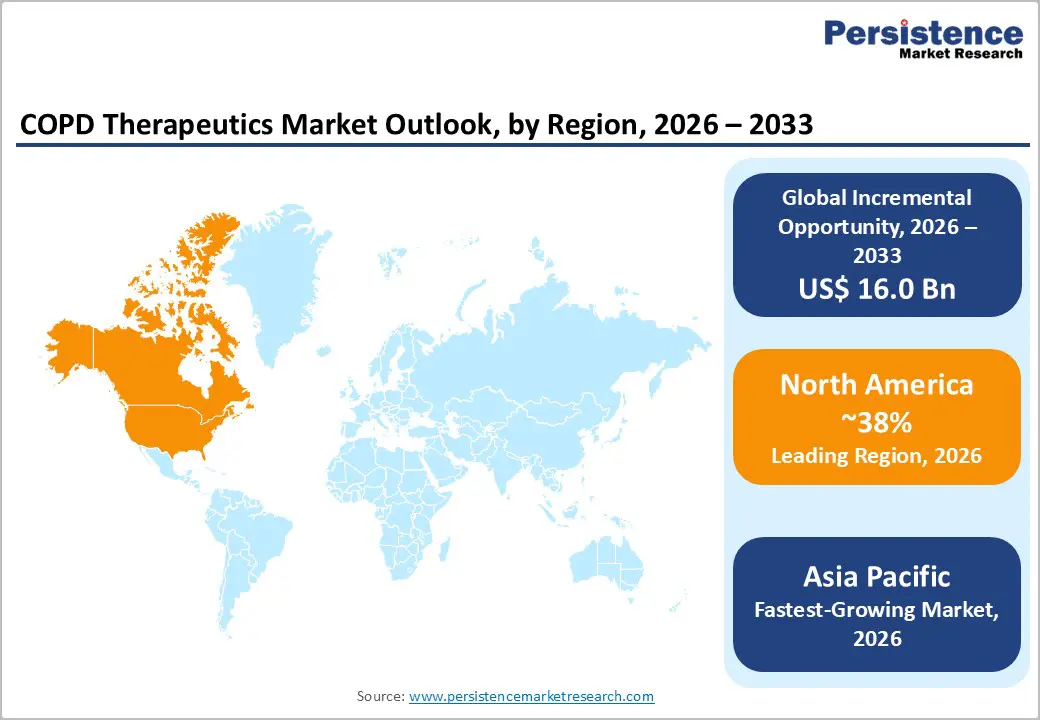

- Regional Landscape: North America is poised to account for about 38% market share in 2026 due to premium drug pricing, while Asia Pacific is expected to emerge as the fastest-growing market with an estimated 8.5% CAGR through 2033, supported by rising diagnosis rates and healthcare expansion.

- Investment Outlook: Pipeline diversification beyond legacy inhalers, including biologics, digital inhaler platforms, and emerging market expansion strategies, is expected to remain the primary determinant of competitive advantage through 2033.

| Key Insights | Details |

|---|---|

| COPD Therapeutics Market Size (2026E) | US$ 27.2 Bn |

| Market Value Forecast (2033F) | US$ 43.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Aging Population and Smoking Legacy Burden

The chronic obstructive pulmonary disease therapeutics market growth is gaining momentum as population aging and cumulative exposure to risk factors such as smoking are increasing disease prevalence across multiple regions. The United Nations (UN) is projecting that the global population aged 65 years and above will have doubled between 2020 and 2050, which is significantly increasing the incidence of chronic respiratory conditions. Older adults are experiencing progressive lung function decline, immune system weakening, and higher exposure history, spiking COPD diagnosis rates. The Organisation for Economic Co-operation and Development (OECD) is also reporting that chronic disease prevalence is rising faster than overall population growth in developed economies, which is reinforcing the long-term demand outlook for respiratory therapeutics.

This demographic transformation is increasing treatment penetration and extending therapy duration, which is strengthening revenue stability for pharmaceutical manufacturers. Earlier diagnosis is allowing patients to initiate maintenance therapy sooner, and they are remaining on treatment regimens for longer periods as disease progression continues over time. Pharmaceutical companies are responding by investing in long-acting inhalers, combination therapies, and disease-modifying research programs to address evolving clinical needs. The aging population trend is therefore structurally expanding the total addressable market and improving lifetime patient value, which is supporting predictable revenue growth.

Clinical Guideline Evolution toward Combination and Precision Therapy

Treatment strategies for COPD are evolving as clinical guidelines are increasingly recommending earlier use of combination inhaled therapies during disease progression. The GOLD initiative emphasizes symptom control and exacerbation prevention through dual and triple therapy regimens rather than gradual escalation from monotherapy. Physicians are adopting fixed-dose combinations more frequently because these therapies are improving adherence and delivering broader bronchodilation and anti-inflammatory effects. This transition is increasing the average cost of treatment per patient and is accelerating the adoption of combination inhalers across both moderate and severe disease populations. Pharmaceutical companies are benefiting from this shift because combination products often command higher pricing and provide stronger differentiation compared to single-agent therapies.

Biomarker-guided treatment approaches are emerging, particularly for patients with eosinophilic inflammation profiles. Regulatory agencies are approving biologic therapies that target inflammatory pathways such as interleukin signaling, which is creating new high-value therapeutic categories within COPD management. These specialty drugs are typically priced significantly higher than traditional inhaled bronchodilators due to their targeted mechanism and clinical benefits in reducing exacerbations. Pharmaceutical companies that invest in biomarker-driven research and specialty drug development are likely to achieve stronger competitive positioning.

Generic Inhaler Competition and Pricing Compression

The COPD therapeutics market growth faces pricing pressure as patents for several major inhaled therapies are expiring, which is allowing generic manufacturers to enter the market with lower-cost alternatives. Regulatory authorities in the U.S. and Europe are actively encouraging generic competition to reduce healthcare expenditure and improve patient affordability. The U.S. Food and Drug Administration (FDA) is implementing accelerated approval pathways for generic inhalers, which is increasing the number of competing products available. As a result, branded pharmaceutical companies are experiencing declining margins and reduced pricing power, particularly for long-established bronchodilator products. This regulatory environment is reshaping the competitive landscape by shifting value toward differentiated therapies and innovation-driven products.

This trend is creating significant revenue erosion risks for companies that rely heavily on legacy inhaler portfolios. Declining per-unit pricing is limiting revenue growth even as patient populations continue to expand globally. The financial impact is becoming more pronounced in publicly funded healthcare systems, where reimbursement authorities are negotiating aggressively to control costs and prioritize generic substitution. Pharmaceutical firms are therefore facing pressure to diversify their product offerings beyond traditional inhaled therapies to maintain profitability. Investors are increasingly favoring companies with strong specialty drug pipelines, biologics development programs, and advanced delivery technologies, as these segments are expected to provide more sustainable long-term growth compared to commoditized inhaler markets.

Underdiagnosis and Treatment Access Gaps in Emerging Markets

COPD is one of the most widely underdiagnosed conditions across low-income and middle-income countries due to limited access to diagnostic tools and disparities in healthcare infrastructure. Spirometry testing, which is the standard method for confirming COPD, is not easily accessible in several primary care settings, particularly in rural regions. The WHO estimates that a substantial proportion of COPD cases remain undetected globally, especially in populations exposed to biomass fuel smoke and environmental pollutants. Without formal diagnosis, patients are not entering pharmacological treatment pathways, which is restricting therapy adoption and delaying disease management. This diagnostic gap is limiting pharmaceutical demand growth despite rising disease prevalence across large populations.

Healthcare system constraints are also reducing the adoption of advanced therapies such as biologic treatments and specialty inhalers. High medication costs and limited reimbursement coverage are creating affordability barriers in regions such as Asia, Africa, and Latin America, where healthcare spending per capita is comparatively lower. Patients are often relying on symptomatic relief rather than long-term maintenance therapy due to cost considerations, which is reducing market penetration for premium treatments. These structural challenges are contributing to uneven regional growth patterns, with developed markets adopting advanced therapies more rapidly than emerging economies.

Biologic Therapies for Eosinophilic and Severe COPD

A substantial opportunity is developing in biologic therapies that target inflammatory pathways associated with severe COPD phenotypes. Clinical studies are identifying a subgroup of patients with eosinophilic inflammation patterns that resemble asthma-related immune responses, which is making them suitable candidates for monoclonal antibody treatments. These therapies are targeting cytokine pathways such as interleukin-5 (IL-5) and IL-4, which play a role in airway inflammation and exacerbation frequency. Biologic drugs are typically administered through injectable routes and are commanding premium pricing because they deliver targeted therapeutic effects and reduce hospitalization risk. In developed healthcare systems, annual treatment costs are often exceeding UUS$ 10,000 per patient, which is significantly higher than conventional inhaled therapies.

If biologics achieve penetration levels of approximately 5-10% globally within this patient segment, incremental market value could exceed US$ 8 billion by 2033. Pharmaceutical manufacturers are actively expanding research and development pipelines to capture this opportunity, with multiple clinical trials focusing on inflammatory biomarkers and targeted mechanisms of action. This emerging segment is representing one of the most attractive growth corridors within the market for COPD therapeutics, since it combines high pricing potential with unmet clinical need. Companies that establish early clinical leadership and regulatory approvals in biologic therapies are likely to secure strong competitive advantages in the coming decade.

Improving Diagnosis Rates in Developing Economies and Urban Pollution Exposure

Rapid urbanization and deteriorating air quality across Asia Pacific and parts of Latin America are increasing the incidence of chronic obstructive pulmonary disease among non-smoking populations. Exposure to environmental pollutants such as particulate matter, industrial emissions, and household biomass combustion is contributing to long-term respiratory damage. The World Bank (WB) and the WHO have already identified air pollution as a major driver of chronic respiratory disease burden, particularly in densely populated urban regions. Governments in countries such as China and India are investing in respiratory healthcare programs, expanding diagnostic capacity, and strengthening public health awareness initiatives. These efforts are improving disease detection and are gradually integrating COPD management into primary healthcare systems, which is supporting pharmaceutical market development.

Improving healthcare access is expected to increase treatment penetration significantly across large patient populations. Expanded insurance coverage, infrastructure development, and local pharmaceutical manufacturing are reducing barriers to therapy adoption. This volume-driven expansion in emerging economies is complementing the value-driven growth generated by biologic therapies and specialty treatments in developed markets. Companies that adopt localized pricing strategies, establish regional partnerships, and invest in distribution networks are likely to capture long-term growth opportunities as healthcare systems continue to mature.

Category-wise Analysis

Drug Class Insights

In 2026, bronchodilators are expected to account for approximately 38% of the COPD therapeutics market revenue share, on account of their central role in treatment protocols. These medications are improving airway function and symptom control, which is making them essential in clinical management. Long-acting beta agonists and muscarinic antagonists are being prescribed widely due to strong efficacy and established safety profiles. High patient volumes and chronic therapy use are sustaining revenue leadership despite increasing generic competition. Pharmaceutical companies are maintaining competitiveness through fixed-dose combinations and improved inhaler devices.

Biologic therapies are projected to grow the fastest between 2026 and 2033, at an estimated CAGR of 12.5%, since precision medicine approaches are expanding treatment options for severe disease populations. Injectable monoclonal antibodies targeting inflammatory pathways are showing promising clinical outcomes in reducing exacerbations and hospitalizations. These therapies are commanding significantly higher pricing compared to inhaled medications, which is amplifying revenue growth potential. Pharmaceutical companies are investing heavily in research and development to capture this segment.

Route of Administration Insights

Inhalation therapy is poised to maintain leadership in the market for COPD therapeutics in 2026. This is mainly attributable to the superior efficacy of direct drug delivery to the lungs while minimizing systemic side effects. Metered dose inhalers, dry powder inhalers, and nebulized therapies are being widely adopted across all disease severity levels. Physicians and patients are familiar with inhalation devices, which is supporting adherence and sustained usage. Pharmaceutical companies are enhancing product differentiation through device innovation and connected inhaler technologies that monitor patient adherence. As a result, inhalation therapies are projected to hold approximately 72% of the COPD therapeutics market share in 2026, powered by their established clinical acceptance and high treatment volumes.

Injectable therapies are expected to register the highest CAGR of around 11.2% during the 2026-2033 forecast period, owing to the entry of biologic treatments in COPD management pathways for specific patient groups. Subcutaneous administration is enabling targeted treatment with prolonged dosing intervals, which is improving patient convenience. Specialty pharmacies and hospital-based care systems are facilitating adoption of injectable treatments. As clinical guidelines increasingly incorporate phenotype-based therapy selection, injectable biologics are likely to gain market share.

Regional Insights

North America COPD Therapeutics Market Trends

North America is anticipated to command an estimated 38% of the COPD therapeutics market share in 2026, supported by strong diagnosis rates, advanced healthcare infrastructure, and broad pharmaceutical adoption. The U.S. is contributing the majority of regional revenue because medication pricing levels remain higher than in most other regions and insurance coverage is facilitating access to advanced therapies. Public programs such as Medicare and private health insurers are covering combination inhalers and specialty medications, which is increasing treatment utilization across different disease stages. High physician awareness and widespread availability of pulmonary diagnostics are also enabling early disease identification, which is expanding the treated patient population and strengthening long-term demand for maintenance therapies.

Biologic therapy adoption is increasing as specialty respiratory clinics and integrated care networks are expanding across the region. The U.S. FDA is bolstering innovation through regulatory pathways that accelerate approval of novel therapeutics, which is encouraging pharmaceutical investment. Digital health technologies such as remote patient monitoring and connected inhaler platforms are improving treatment adherence and clinical outcomes, which is reinforcing therapy uptake. Although the market is relatively mature, premium-priced therapies and ongoing innovation are sustaining growth momentum. Given these factors, the North America market is projected to expand at a 2026-2033 CAGR of about 6.2%.

Europe COPD Therapeutics Market Trends

Europe is a major market for COPD therapeutics, backed by aging populations and comprehensive healthcare coverage across many countries. Germany, the U.K., and France are maintaining strong treatment adoption through structured respiratory care programs and established clinical pathways. Universal healthcare systems are ensuring patient access to maintenance therapies, including inhaled medications and combination treatments. The European Medicines Agency (EMA) is facilitating regulatory approvals for innovative therapies such as biologics, which is supporting gradual advancement in treatment standards. However, centralized pricing negotiations and health technology assessment processes are limiting revenue expansion compared to North America by prioritizing cost-effectiveness and budget sustainability.

Government healthcare authorities are continuing to emphasize value-based procurement, which is encouraging the adoption of generic inhalers and cost-efficient therapeutic options. Despite pricing constraints, rising disease prevalence and demographic aging are sustaining overall treatment demand across the region. Western European countries are maintaining stable markets, while Eastern Europe is presenting emerging growth opportunities due to improving diagnostic capacity and expanding healthcare access. Pharmaceutical companies are increasingly focusing on market access strategies and regional partnerships to strengthen their presence within cost-regulated environments.

Asia Pacific COPD Therapeutics Market Trends

Asia Pacific is poised to become the fastest-growing market for COPD therapeutics, with a projected CAGR of about 8.5% between 2026 and 2033. Rapid urbanization, increasing exposure to environmental pollutants, and persistent smoking prevalence are contributing to rising disease incidence across the region. Countries such as China and India are representing the largest growth contributors due to their substantial population sizes and ongoing expansion of healthcare infrastructure. Industrial development and worsening air quality are increasing respiratory disease burden among both smokers and non-smokers, which is expanding the potential patient pool requiring pharmacological management.

Government healthcare reforms are improving diagnostic capacity and treatment accessibility across several Asia Pacific countries. Public insurance programs, hospital infrastructure investment, and physician training initiatives are increasing the number of diagnosed patients entering therapy pathways. Domestic pharmaceutical manufacturing is also enhancing affordability by reducing dependence on imported medications and enabling competitive pricing. Multinational pharmaceutical companies are forming regional partnerships and establishing local production facilities to strengthen market presence and supply chain efficiency. As healthcare systems continue to mature and treatment awareness improves, Asia Pacific is expected to become a major revenue contributor to the global market for COPD therapeutics by 2033, offering significant long-term growth opportunities for industry stakeholders.

Competitive Landscape

The global COPD therapeutics market structure is moderately consolidated, with the top five pharmaceutical companies controlling nearly 60% of revenues. Leading manufacturers are strengthening their market positions by expanding combination inhaler portfolios, advancing biologic drug pipelines, and investing in drug delivery device innovation. Competition is intensifying as generic inhaler producers are entering the market, particularly across Europe and Asia, where regulatory policies are encouraging cost-effective treatment alternatives. This influx of lower-priced products is increasing pricing pressure on established brands and is reshaping competitive dynamics across both developed and emerging markets.

Organizations with diversified respiratory portfolios are maintaining stronger competitive advantage because they are balancing legacy inhaler revenue with innovation-driven products such as biologics and advanced delivery systems. Strategic positioning is increasingly depending on research and development capability, clinical differentiation, and regulatory execution rather than reliance on established bronchodilator franchises. Partnerships between pharmaceutical companies and digital health providers are also emerging to enhance patient adherence and disease monitoring through connected inhaler platforms and remote care technologies.

Key Industry Developments

- In January 2026, the U.K. National Institute for Health and Care Excellence (NICE) recommended dupilumab as an add-on maintenance therapy for adults with uncontrolled COPD and elevated eosinophil levels, potentially benefiting up to 30,000 patients in England. The biologic, administered via self-injection every two weeks, has demonstrated around a 30% reduction in exacerbations in clinical trials.

- In November 2025, Glenmark Pharmaceuticals launched the world’s first nebulized fixed-dose triple therapy for COPD, combining glycopyrronium, formoterol, and budesonide into a single treatment to simplify administration and improve symptom control. Clinical studies in India showed rapid improvement in lung function and breathlessness with a favorable safety profile.

- In July 2025, Merck Sharp & Dohme (MSD) agreed to acquire Verona Pharma for approximately US$ 10 billion to strengthen its respiratory portfolio with Ohtuvayre (ensifentrine), a first-in-class inhaled COPD therapy that combines bronchodilator and anti-inflammatory effects. The drug, approved by the U.S. FDA in 2024, represents the first novel inhaled COPD mechanism in over two decades.

Companies Covered in COPD Therapeutics Market

- GlaxoSmithKline plc

- AstraZeneca PLC

- Boehringer Ingelheim International GmbH

- Novartis AG

- Merck & Co., Inc.

- F. Hoffmann-La Roche Ltd

- Sanofi S.A.

- Regeneron Pharmaceuticals, Inc.

- Teva Pharmaceutical Industries Ltd.

- Chiesi Farmaceutici S.p.A.

- Verona Pharma plc

- Pfizer Inc.

- Cipla Limited

- Sun Pharmaceutical Industries Limited

- Viatris Inc.

Frequently Asked Questions

The global COPD therapeutics market is projected to reach US$ 27.2 billion in 2026.

Increasing number of aging individuals, surging prevalence of chronic respiratory conditions worldwide, improving diagnosis rates, and treatment innovation are driving the market.

The market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Rising exposure to urban air pollution, clinical practice evolution toward dual and triple therapy regimens to reduce exacerbations and hospitalizations, and development of novel drug classes such as dual PDE inhibitors and biologic monoclonal antibodies are key market opportunities.

GlaxoSmithKline plc, AstraZeneca PLC, Boehringer Ingelheim International GmbH, and Novartis AG are some of the key players in the market.