- Specialty & Fine Chemicals

- Chloroacetyl Chloride Market

Chloroacetyl Chloride Market Size, Share, and Growth Forecast 2026 - 2033

Chloroacetyl Chloride Market by Product Grade (Technical Grade, Industrial Grade, Laboratory/Reagent Grade), Purity Level (≥98%, 95-97%, <95%), End-user (Pharmaceuticals, Agrochemicals, Chemical Manufacturing, Specialty Chemicals, Research & Laboratories), Regional Analysis for 2026 - 2033

Chloroacetyl Chloride Market Size and Trend Analysis

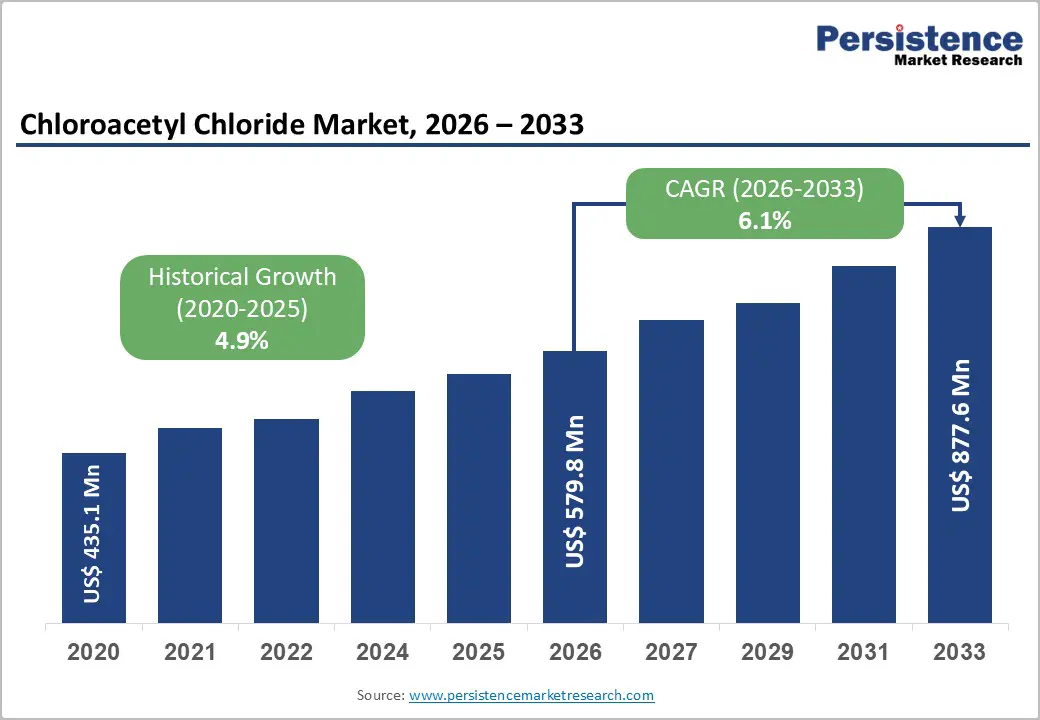

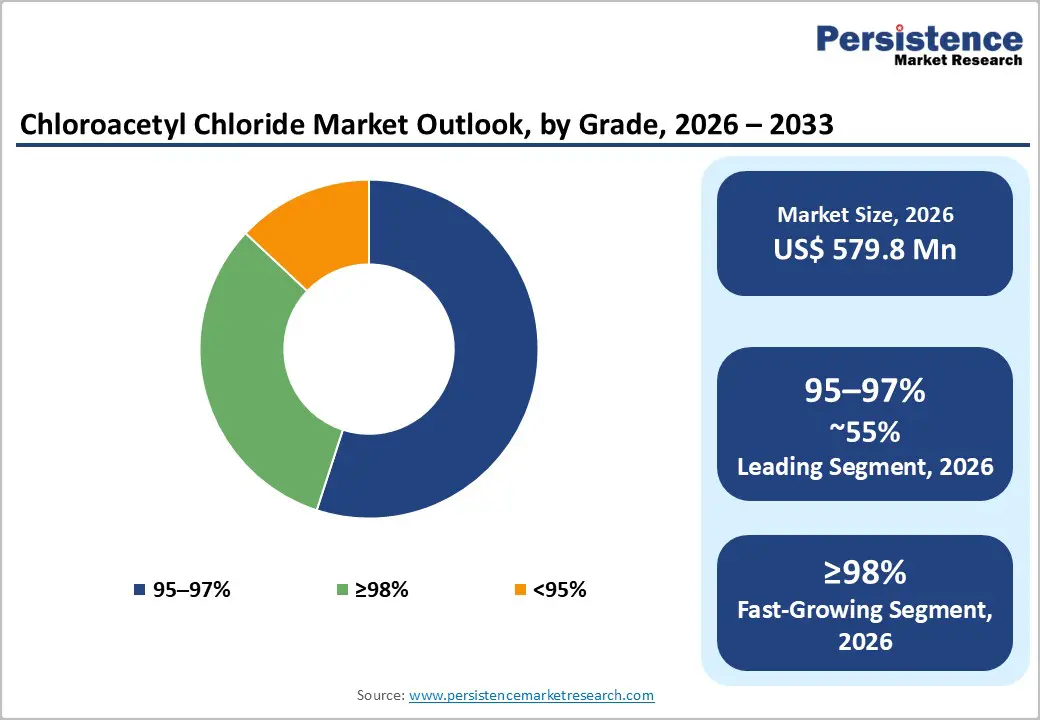

The global chloroacetyl chloride market size is likely to be valued at US$ 579.8 million in 2026 and is expected to reach US$ 877.6 million by 2033, growing at a CAGR of 6.1% during the forecast period from 2026 to 2033.

Market growth is fundamentally driven by escalating pharmaceutical intermediates demand across global drug synthesis pathways and expanding agrochemical production, particularly in emerging Asian economies.

Key Industry Highlights:

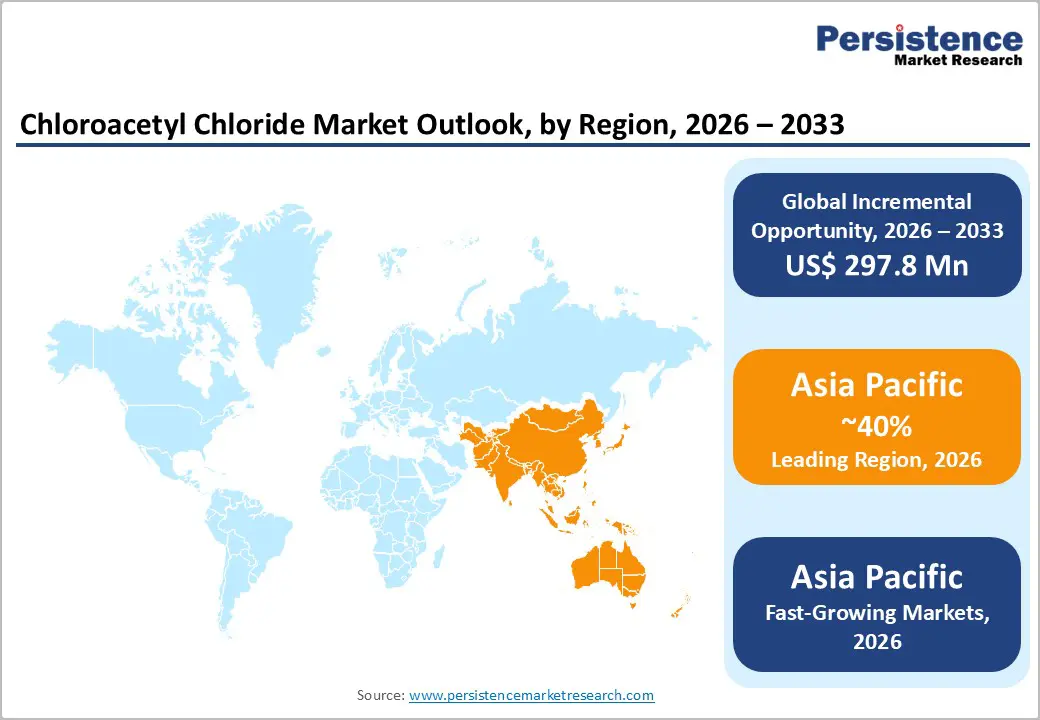

- Leading Region: Asia Pacific commands the largest chloroacetyl chloride market share with approximately 40% of global volume, driven by pharmaceutical manufacturing concentration in China and India, extensive agricultural operations requiring crop protection chemicals, and government industrial development initiatives supporting chemical sector expansion.

- Dominant Segment: Industrial Grade chloroacetyl chloride with 95-99% purity commands approximately 55% market share, leveraging cost-effectiveness, established supply chains, and adequate performance for bulk chemical synthesis applications in agrochemical and specialty chemical production.

- Fastest Growing Segment: High-Purity Grade chloroacetyl chloride (≥98% purity) experiences accelerated 7.8% annual growth, driven by expanding pharmaceutical manufacturing demand, stricter regulatory requirements, and premium pricing supporting specialized production investments.

- Key Market Opportunity: Asia Pacific pharmaceutical and agrochemical expansion, with India's projected 9% chemical industry growth toward US$ 304 billion by FY25 and China's agricultural intensification, creates substantial demand for cost-effective, region-optimized chloroacetyl chloride formulations supporting API synthesis and herbicide production.

| Key Insights | Details |

|---|---|

| Chloroacetyl Chloride Market Size (2026E) | US$ 579.8 Million |

| Market Value Forecast (2033F) | US$ 877.6 Million |

| Projected Growth CAGR (2026 - 2033) | 6.1% |

| Historical Market Growth (2020 - 2025) | 4.9% |

Market Dynamics

Drivers - Rising global pharmaceutical production is driving strong demand for chloroacetyl chloride as a key API intermediate

The rapid expansion of the global pharmaceutical industry is a major driver of demand for chloroacetyl chloride. Factors such as an aging population, rising healthcare expenditure, and ongoing drug innovation are significantly increasing demand for specialized chemical intermediates. Leading pharmaceutical companies, including Pfizer, GlaxoSmithKline, and growing generic manufacturers, rely on chloroacetyl chloride as an essential building block for active pharmaceutical ingredient synthesis. The compound plays a critical role in acylation reactions used to manufacture antibiotics, anti-inflammatory drugs, antivirals, and anticancer therapies.

Its importance is evident in the production of widely used medicines such as Diclofenac and Aceclofenac. As the global API market continues to expand, specialty chemical consumption is growing steadily as part of complex manufacturing processes. Currently, pharmaceuticals account for nearly 40% of total chloroacetyl chloride demand. With annual growth exceeding 7%, this segment is outperforming commodity chemicals, highlighting the long-term strength and resilience of healthcare-driven demand.

Growing agricultural intensification and herbicide usage continue to boost chloroacetyl chloride consumption worldwide

Growing pressure on global food systems is strongly driving demand for modern agrochemicals, creating significant growth opportunities for chloroacetyl chloride. Rapid population growth, declining arable land per capita, and the need to improve crop productivity have increased reliance on advanced herbicides and crop protection solutions. Chloroacetyl chloride serves as a vital intermediate in the manufacture of dichloroacetanilide herbicides and crop safeners. According to the U.S. Environmental Protection Agency, the global pesticide market is expected to reach US$ 92.7 billion by 2027, reflecting strong long-term demand.

Asia Pacific countries, especially China, India, and ASEAN nations, are witnessing rising agricultural intensification and higher chemical usage. Regional agrochemical producers increasingly depend on secure chloroacetyl chloride supply to maintain uninterrupted production. Agrochemicals currently represent about 35% of total market consumption. Growth rates above 8% in Asian markets are supported by improving farmer incomes, expanding commercial farming, and regulatory focus on effective crop protection practices.

Restraints - Strict safety regulations and hazardous handling requirements significantly increase operational and compliance costs

The hazardous nature of chloroacetyl chloride presents a major restraint for market growth. The compound is highly reactive, corrosive, and toxic, requiring strict safety protocols across production, storage, transportation, and end-use handling. Regulatory authorities such as OSHA mandate low exposure limits and compulsory protective systems, while transportation regulations impose strict hazardous material guidelines. In Europe, REACH regulations introduce complex authorization and documentation requirements, significantly increasing compliance costs. The NIOSH recommended exposure limit of just 0.05 ppm necessitates advanced monitoring systems and costly emission controls.

Differences in regulatory standards across regions further complicate global operations, forcing manufacturers to manage multiple compliance frameworks simultaneously. These regulatory obligations increase operational expenses, reduce profit margins, and discourage new market entrants. Smaller and regional manufacturers are particularly impacted, as they often lack the financial capacity and technical expertise needed to meet international safety and compliance standards consistently.

Fluctuating raw material prices and supply chain instability create pricing uncertainty and production challenges

Chloroacetyl chloride production is highly dependent on chlorine gas and acetic acid derivatives, both of which experience frequent price volatility. Chlorine supply is closely linked to chlor-alkali plant operations, making availability regionally sensitive. Energy-intensive manufacturing processes further expose producers to fluctuations in electricity and natural gas prices. Global supply chain disruptions, port congestion, and transportation cost inflation have historically increased procurement expenses and delayed deliveries.

Managing hazardous raw materials also limits inventory flexibility, as long-term stockpiling involves regulatory approvals and high warehousing costs. These constraints reduce manufacturers’ ability to buffer supply shocks effectively. As a result, pricing instability often transfers to downstream customers, particularly affecting cost-sensitive agrochemical and chemical manufacturers. Unpredictable raw material pricing complicates long-term planning, contract negotiations, and margin stability. This volatility restricts market expansion in regions where end users operate under tight cost structures and demand consistent input pricing.

Opportunities - Rapid industrial growth and expanding chemical manufacturing in Asia Pacific present major market expansion opportunities

Asia Pacific represents the most attractive growth opportunity for the chloroacetyl chloride market, currently accounting for nearly 40% of global consumption. The region benefits from rapid pharmaceutical manufacturing expansion, rising agrochemical output, and strong government support for chemical industry development. China continues to increase production capacity, particularly for pharmaceutical intermediates and crop protection chemicals. India’s chemical sector, projected to reach US$ 304 billion by FY25, is expanding at nearly 9% annually, drawing global manufacturers seeking cost efficiency and skilled labour.

Countries such as Indonesia are also witnessing increased herbicide usage due to agricultural expansion. Establishing local manufacturing facilities allows suppliers to reduce logistics costs and improve responsiveness to customers. Rising foreign direct investment, favorable policies, and infrastructure development further strengthen regional growth potential. Manufacturers that form strategic partnerships with local pharmaceutical and agrochemical companies are well-positioned to capture long-term demand while improving supply reliability and market penetration.

Adoption of green chemistry and advanced manufacturing technologies is opening new pathways for sustainable growth

Increasing regulatory focus on sustainability is creating strong opportunities for manufacturers investing in greener production technologies. Customers and governments alike are demanding environmentally responsible chemical manufacturing processes, encouraging innovation across the value chain. Process intensification, continuous manufacturing systems, and waste minimization technologies are helping producers reduce emissions while improving operational efficiency. Advances in catalytic optimization and alternative raw material use are lowering production costs and enhancing yield consistency.

Digital tools such as artificial intelligence, predictive analytics, and real-time monitoring enable precise control over reaction conditions and reduce by-product formation. These improvements support both sustainability goals and margin expansion. Companies that successfully commercialize green production methods gain strong competitive differentiation and premium customer positioning. Early adopters benefit from regulatory incentives, improved brand reputation, and long-term customer loyalty. Collaborative R&D efforts between chemical producers, academic institutions, and technology firms further accelerate innovation cycles, enabling faster commercialization of next-generation sustainable manufacturing solutions.

Category-wise Analysis

Product Grade Insights

Industrial-grade chloroacetyl chloride, with typical purity levels between 95% and 99%, holds the largest market share at approximately 55%. Its dominance is driven by cost efficiency and suitability for large-scale chemical and agrochemical synthesis. Many downstream users accept moderate impurity levels, allowing manufacturers to optimize production economics. Industrial-grade material is widely used in herbicide intermediates and bulk specialty chemicals where ultra-high purity is not essential. Producers benefit from integrated manufacturing setups, particularly those located near chlor-alkali plants that enable on-site chlorine availability.

Continuous process upgrades have improved production efficiency and output consistency. The segment grows steadily at around 4.5% annually, supported mainly by agrochemical demand. Market leadership remains concentrated among established suppliers such as CABB, ALTIVIA, and Daicel, whose vertical integration and economies of scale provide strong cost advantages. These players continue to dominate price-sensitive, high-volume applications worldwide.

Purity Level Insights

High-purity chloroacetyl chloride, generally exceeding 98% purity, accounts for nearly 30% of the total market and shows faster growth of 7.8% annually. This segment is driven primarily by pharmaceutical manufacturers requiring stringent impurity control for API synthesis. Even trace contaminants can impact drug yields and regulatory compliance, making premium quality non-negotiable. Compliance with FDA CGMP guidelines demands extensive documentation, traceability, and consistent manufacturing performance. High-purity suppliers, therefore, invest heavily in advanced analytical testing and process control systems.

These capabilities allow them to command premium pricing and maintain strong customer loyalty. Daicel Corporation leads this segment through long-standing R&D investments and a strong reputation for reliability among pharmaceutical clients. Demand remains stable even during economic downturns, as drug manufacturing continues regardless of market cycles. This resilience supports long-term investment in specialized facilities and reinforces the segment’s high-margin growth profile.

End-use Insights

Laboratory and reagent-grade chloroacetyl chloride represents a smaller but specialized segment, accounting for approximately 15% of total demand. This grade is primarily used by research institutions, universities, contract research organizations, and specialty chemical laboratories. The focus is on ultra-high purity, precise specifications, and complete quality documentation rather than cost efficiency. These products are supplied in small volumes and require specialized packaging and rigorous analytical validation. Academic research, pharmaceutical discovery, and synthetic chemistry development rely on consistent reagent quality to ensure reproducible results.

Global distributors such as Sigma-Aldrich and Fisher Scientific dominate this segment through extensive catalog offerings and efficient logistics networks. The segment grows at around 5-6% annually, supported by increasing pharmaceutical R&D investment and outsourcing trends. However, high compliance costs and limited order volumes restrict profitability for new entrants, reinforcing strong incumbent dominance within laboratory-grade distribution channels.

Regional Insights

North America Chloroacetyl Chloride Market Trends

North America accounts for approximately 25% of global market share, supported by strong pharmaceutical and agrochemical manufacturing infrastructure. The United States leads regional demand due to major pharmaceutical companies and specialized API producers. Strict EPA, OSHA, and DOT regulations encourage high-quality and compliance-focused production models. Recent policy initiatives emphasize domestic manufacturing and supply chain resilience. Regional suppliers are investing in facility upgrades and automation to improve efficiency and reduce import dependence.

Companies increasingly adopt advanced analytics, robotics, and AI-based monitoring to enhance consistency and safety. Pharmaceutical innovation and complex drug synthesis continue to support long-term demand. Agrochemical consumption remains stable despite competition from bio-based alternatives. Strategic partnerships between suppliers and customers strengthen long-term supply agreements. Overall, North America prioritizes reliability, compliance, and technology-driven manufacturing as key competitive differentiators.

Europe Chloroacetyl Chloride Market Trends

Europe holds around 20% of the global market share and operates under one of the most stringent regulatory environments worldwide. REACH regulations, Seveso III directives, and strict waste management rules significantly influence production strategies. Germany, the UK, and France remain major demand centers due to advanced pharmaceutical and specialty chemical industries. European manufacturers focus heavily on safety, sustainability, and documentation compliance. CABB Group maintains strong regional leadership through advanced infrastructure and long-standing customer relationships.

Sustainability plays a critical role in purchasing decisions, with customers prioritizing environmentally responsible suppliers. Manufacturers investing in green chemistry and low-risk processes gain pricing advantages and stronger market preference. While overall growth is moderate due to market maturity, stable demand from established industries ensures consistent revenue streams. Europe remains a premium-focused, compliance-driven market emphasizing quality and environmental responsibility.

Asia Pacific Chloroacetyl Chloride Trends

Asia Pacific is the fastest-growing region, accounting for nearly 40% of global volume with growth rates exceeding 8% annually. China dominates regional consumption, supported by massive pharmaceutical and agrochemical production capacity. Government-backed chemical industry modernization continues to drive capacity expansion. India’s rapidly growing pharmaceutical sector and rising API exports significantly increase chloroacetyl chloride demand. Regional manufacturers benefit from cost advantages, skilled labor, and integrated infrastructure.

Companies such as Taixing Shenlong and Transpek Industry have expanded production to meet domestic and export requirements. Strong agricultural activity and increasing herbicide adoption further support market growth. International companies are establishing manufacturing hubs in the region to improve cost efficiency and supply security. Strategic partnerships, competitive pricing, and large-scale capacity investments make Asia Pacific the most attractive region for long-term market expansion.

Competitive Landscape

The global chloroacetyl chloride market shows moderate concentration, led by multinational chemical companies with integrated production capabilities. Market leaders benefit from advanced chlorination technology, regulatory expertise, and global distribution networks. CABB Group leads in Europe, while Daicel dominates the high-purity pharmaceutical segment. ALTIVIA differentiates through customized manufacturing solutions and application-specific support. Competitive positioning increasingly depends on product purity, compliance infrastructure, and technical service capabilities.

Sustainability and digital transformation are emerging as key differentiators. Companies are investing in process automation, emissions reduction, and supply chain resilience following recent global disruptions. Strategic partnerships with technology providers and regional producers support innovation and capacity expansion. Regional players compete through cost efficiency, local market knowledge, and flexible service models. Overall, competition is shifting from volume-based strategies toward quality, reliability, and long-term customer collaboration.

Key Developments:

- In June 2024: CABB Group expanded production capacity for high-purity chloroacetyl chloride at its Gersthofen, Germany facility to strengthen supply for pharmaceutical and specialty chemical markets amid rising European demand and reinforce its strategic market position.

- In December 2024: Daicel Corporation advanced greener production processes focusing on waste reduction, enhanced energy efficiency, and environmental sustainability, aligning with broader industry trends toward eco-friendly synthesis technologies in chloroacetyl chloride manufacturing.

- In January 2025: Shiva Pharmachem Ltd secured a strategic supply partnership with major Indian pharmaceutical manufacturers, reinforcing its market presence in Asia and expanding regional integration for critical chemical intermediates including chloroacetyl chloride.

Companies Covered in Chloroacetyl Chloride Market

- Daicel Corporation

- ALTIVIA Petrochemicals Corporation

- CABB Group GmbH

- Shiva Pharmachem Ltd

- Transpek Industry Limited

- Triveni Chemicals

- Taixing Shenlong Chemical Co., Ltd

- Chengwu Chenhui Environmental Protection Technology Co., Ltd.

- Zouping Qili Additives Co. Ltd

- YiDu Jovian Industry CO., LTD

- Tokyo Chemical Industry Co., Ltd.

- Shandong Xinhua Pharma

- Hefei TNJ Chemical Industry Co., Ltd.

- Kerry Group

- Aceto Chemical Companies

Frequently Asked Questions

The global chloroacetyl chloride market is expected to reach US$ 877.6 million by 2033, growing at a 6.1% CAGR driven by pharmaceutical and agrochemical demand.

Demand is driven by rising pharmaceutical API production, expanding agrochemical manufacturing, Asia Pacific industrial growth, and increasing healthcare and food security needs.

Industrial-grade chloroacetyl chloride leads the market with around 55% share, supported by cost efficiency and high usage in bulk chemical and agrochemical synthesis.

Asia Pacific dominates the market, supported by strong pharmaceutical manufacturing, agrochemical expansion, government incentives, and large-scale chemical production in China and India.

The biggest opportunity lies in Asia Pacific’s rapidly expanding pharmaceutical and agrochemical industries, supported by regional manufacturing investments and strategic partnerships.

Key players include CABB Group, Daicel Corporation, ALTIVIA Petrochemicals, Shiva Pharmachem Ltd, Transpek Industry Limited, and major Chinese manufacturers.