- Pharmaceuticals

- Chemotherapy-Induced Alopecia Treatment Market

Chemotherapy-Induced Alopecia Treatment Market Size, Share, and Growth Forecast, 2025 - 2032

Chemotherapy-Induced Alopecia Treatment Market by Drug Type (Minoxidil, Deuruxolitinib, Ritlecitinib, Others), End-user (Hospitals, Cancer Centers, Outpatient Clinics), Form (Tablet, Capsule, Foam, Solution), and Regional Analysis for 2025 - 2032

Chemotherapy-Induced Alopecia Treatment Market Size and Trends Analysis

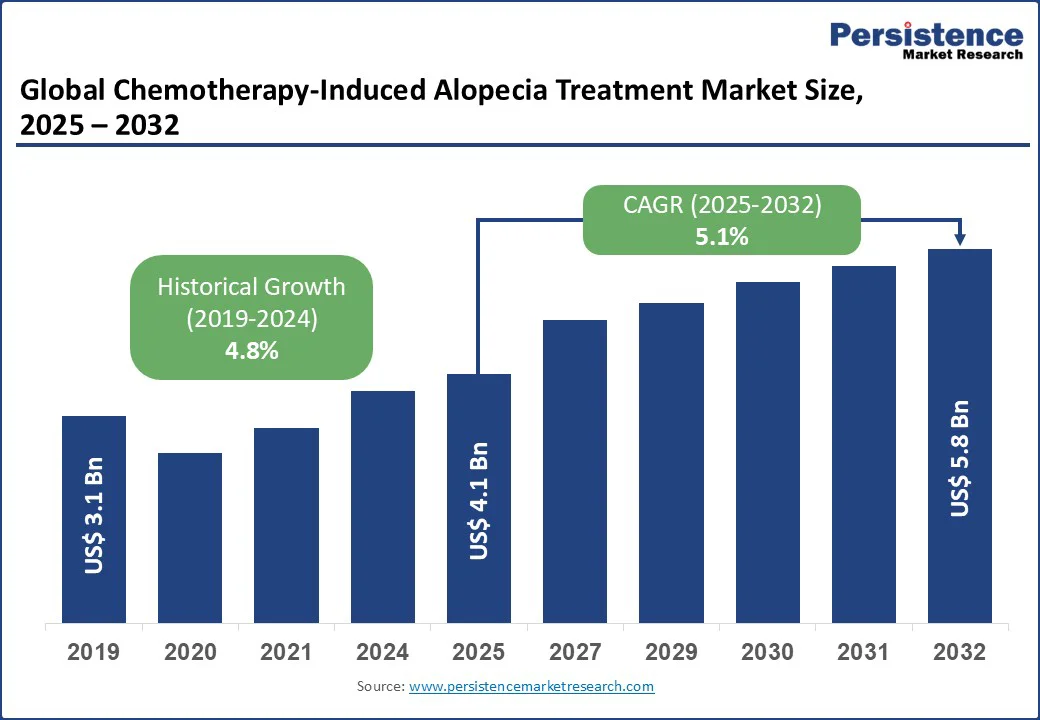

The global chemotherapy-induced alopecia treatment market size is likely to value at US$4.1 Bn in 2025 and is expected to reach US$5.8 Bn by 2032, registering a CAGR of 5.1% during the forecast period from 2025 to 2032.

The chemotherapy-induced alopecia treatment market has experienced steady growth, driven by increasing awareness of chemotherapy side effects, expansion in oncology care, and rising demand for hair loss prevention and treatment solutions. Innovations in targeted therapies and supportive care products further propel market expansion across hospitals, cancer centers, and outpatient settings.

Key Industry Highlights:

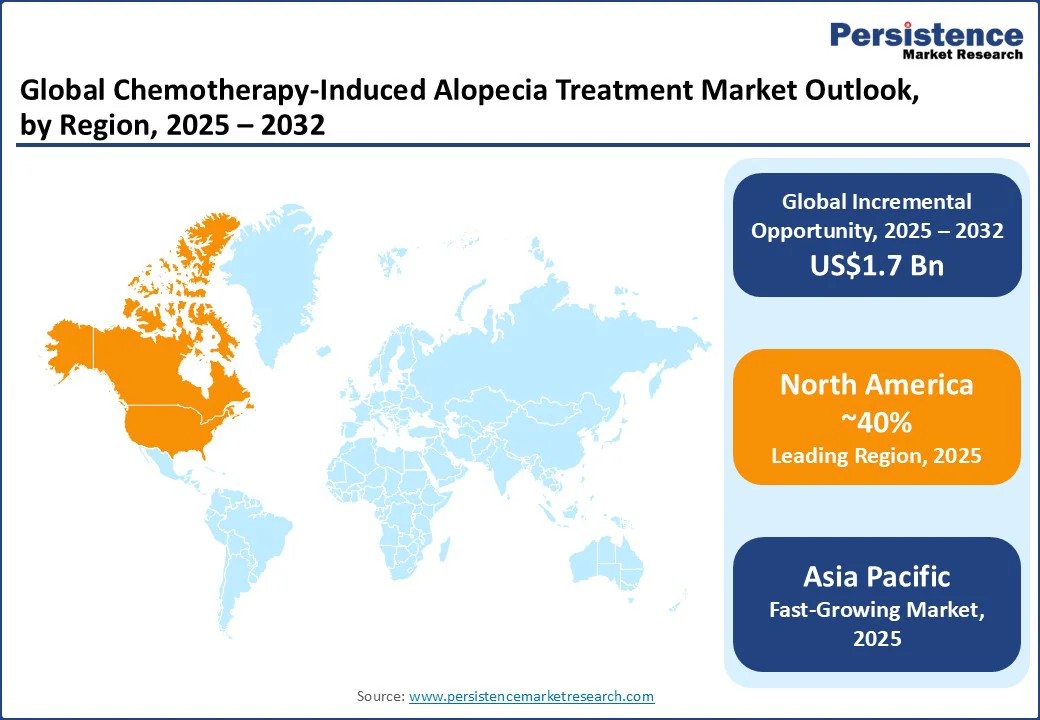

- Leading Region: North America holds a 40% market share in 2025, driven by advanced oncology infrastructure, high cancer prevalence, and established pharmaceutical industries.

- Fastest-growing Region: Asia Pacific, fueled by booming oncology sectors, increasing health consciousness, and expanding cancer treatment facilities in countries such as China and India.

- Dominant Drug Type: Minoxidil accounts for nearly 45% of the chemotherapy-induced alopecia treatment market share, driven by its proven efficacy and widespread availability for alopecia management.

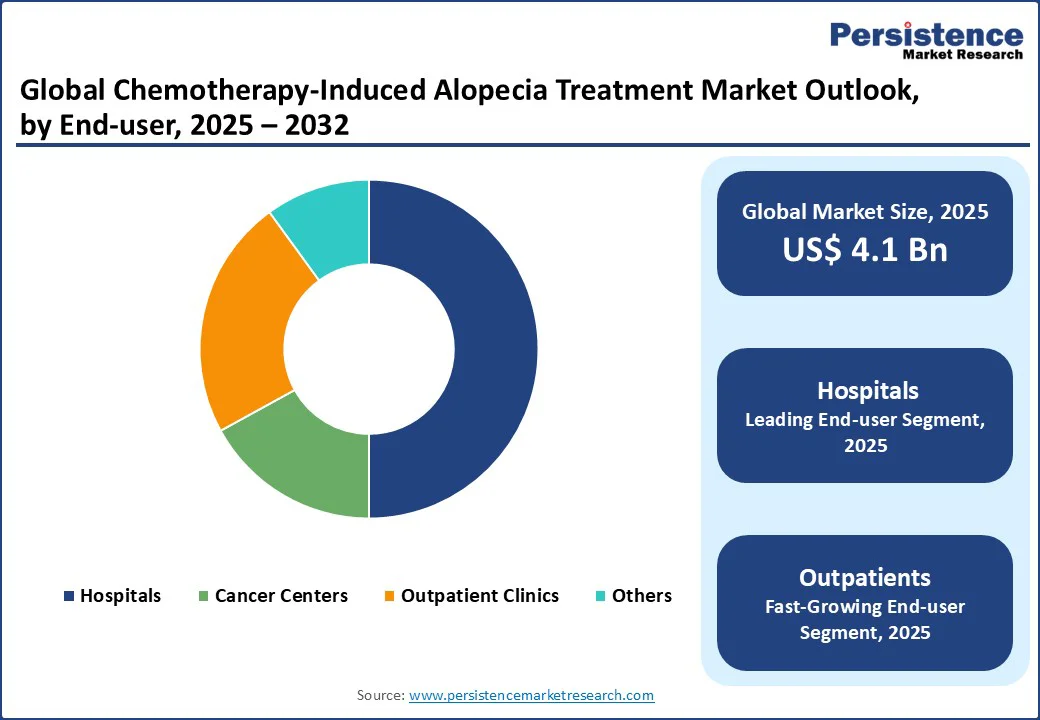

- Leading End-user: Hospitals lead with a 50% share, reflecting their high usage in integrated cancer care.

|

Global Market Attribute |

Key Insights |

|

Chemotherapy-Induced Alopecia Treatment Market Size (2025E) |

US$4.1 Bn |

|

Market Value Forecast (2032F) |

US$5.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.8% |

Market Dynamics

Driver - Rising Cancer Prevalence and Awareness of Supportive Care Push Demand

The global surge in awareness of chemotherapy-induced alopecia (CIA) and its impact on patient quality of life is a primary driver of the chemotherapy-induced alopecia treatment market. According to the World Health Organization, cancer cases are projected to rise by 60% over the next two decades, with chemotherapy remaining a cornerstone treatment, leading to alopecia in patients. The rising incidence of these conditions, particularly among breast and lung cancer patients, drives demand for effective treatments such as minoxidil and JAK inhibitors. In North America, a significant share of cancer survivors report psychological distress from hair loss, necessitating advanced therapies to improve adherence to chemotherapy regimens.

Technological advancements in drug formulations and delivery systems are propelling market growth. Modern treatments, such as Eli Lilly’s ritlecitinib, offer targeted inhibition of hair follicle damage, with clinical studies showing a notable reduction in alopecia severity. A recent trial published in the Journal of Clinical Oncology found that JAK inhibitors such as deuruxolitinib improve hair regrowth rates compared to placebo, boosting consumer confidence. The integration of supportive care protocols in oncology guidelines, such as those from the American Society of Clinical Oncology (ASCO), supports adoption in combination therapies.

Government health initiatives and increased funding for cancer care also drive market expansion. In India, national cancer control programs such as the National Cancer Grid have expanded access to alopecia treatments, increasing demand for affordable options. In Europe, favorable regulatory policies, such as the European Medicines Agency’s (EMA) approval of new JAK inhibitors, incentivize manufacturers to invest in high-quality drugs, further fueling market growth.

Restraint - High Costs and Limited Efficacy Concerns Restrict Adoption

High costs associated with advanced chemotherapy-induced alopecia treatments continue to hinder widespread adoption, particularly in emerging markets. Treatments such as JAK inhibitors, such as ritlecitinib, often require premium pricing due to extensive R&D, with annual costs that can be prohibitively high for patients. Beyond the initial purchase cost, ongoing expenses for monitoring side effects and combination therapies add to the total cost. For patients in resource-limited regions, such as parts of Latin America and Southeast Asia, these financial burdens are difficult to justify, even with growing demand for supportive care. Premium drugs are often priced significantly higher than generic options such as minoxidil, limiting accessibility.

The need for robust clinical evidence and regulatory compliance also restricts market growth. Concerns over variable efficacy, with some treatments showing limited success rates in preventing alopecia, lead to hesitation among oncologists. Industry reports highlight shortages of specialized suppliers in the Asia Pacific region. This supply gap, combined with high distribution costs, further limits the adoption of innovative products in developing regions, where reimbursement policies are inconsistent.

Opportunity - Innovation in Targeted Therapies and Personalized Medicine Boosts Consumption

The development of targeted therapies and personalized medicine presents significant growth opportunities, particularly by enabling tailored treatments for chemotherapy-induced alopecia. JAK inhibitors such as deuruxolitinib and ritlecitinib offer precision targeting of inflammatory pathways, reducing reliance on broad-spectrum options. These innovations address patient-specific needs and appeal to the growing demand for non-invasive solutions, particularly in North America and Europe. For instance, Pfizer’s ritlecitinib is gaining traction in clinical trials, exemplifying the shift toward personalized care.

The rise of outpatient and home-based treatments offers another growth avenue. Topical formulations, rich in growth factors, are increasingly used to enhance patient compliance and reduce hospital visits. Recent market studies highlight steady global growth in supportive care sales, driving demand for high-quality alopecia treatments. Companies such as Sun Pharmaceutical are capitalizing on this trend by offering tailored drug forms for cancer patients. The growing adoption of digital health platforms and AI for treatment monitoring also enhances market potential. Companies such as Johnson & Johnson are integrating app-based tracking systems, ensuring efficacy and regulatory compliance. This trend supports market expansion by addressing patient concerns about side effects and improving treatment outcomes.

Segmental Insights

Drug Insights

The global chemotherapy-induced alopecia treatment market is segmented into Minoxidil, Deuruxolitinib, Ritlecitinib, and Others. Minoxidil dominates, holding approximately 45% of the chemotherapy-induced alopecia treatment market share in 2025, due to its abundant availability and proven track record in promoting hair regrowth. It is widely used for its vasodilatory effects, making it a cost-effective choice for post-chemotherapy care. On the other hand, ritlecitinib is the fastest-growing segment, driven by increasing demand for targeted JAK inhibitors in alopecia management. Its high efficacy in clinical trials, particularly in North America and Europe, boosts its adoption in high-value markets.

End-user Insights

The chemotherapy-induced alopecia treatment market is divided into hospitals, cancer centers, and outpatient clinics. Hospitals lead with a 50% share in 2025, driven by their high usage in integrated oncology care for chemotherapy patients. They are critical for administering treatments alongside cancer therapies, with over 60% of global CIA cases managed in this setting.

Outpatient clinics are the fastest-growing segment, fueled by rising patient preference for convenient, non-hospital care. The increasing use of topical and oral treatments in outpatient settings, particularly in Europe and North America, drives demand for flexible solutions.

Form Insights

The chemotherapy-induced alopecia treatment market is segmented into tablet, capsule, foam, and solution. Solution dominates with a 40% share in 2025, driven by its ease of application and rapid absorption for topical use in alopecia treatment.

Foam is the fastest-growing segment, propelled by innovations in user-friendly formulations for home use. Enhanced foam products from companies such as Taro Pharmaceutical support this growth by offering better patient compliance.

Regional Insights

North America Chemotherapy-Induced Alopecia Treatment Market Trends

In North America, the U.S. is a significant market, driven by high cancer prevalence and the presence of a robust oncology industry. In the U.S., demand for targeted alopecia treatments is rising, fueled by increasing consumption of JAK inhibitors and supportive care products. Leading brands such as Pfizer Inc. and Eli Lilly and Company continue to offer innovative, high-efficacy solutions to meet the patient needs.

Consumer preferences are shifting toward personalized and non-invasive treatments, with companies such as Legacy Healthcare incorporating patient-centric formulations to enhance credibility. Health consciousness remains a priority, and stringent FDA regulations encourage the adoption of high-quality drugs. Additionally, favorable policies for cancer supportive care claims further incentivize manufacturers to invest in advanced therapies, supporting market growth.

Europe Chemotherapy-Induced Alopecia Treatment Market Trends

Europe holds a significant share in the global chemotherapy-induced alopecia treatment market, led by Germany, the U.K., and France, driven by regulatory support and high adoption of supportive oncology products. Germany accounts for the largest share within Europe, supported by strong sales from leading brands such as Cosmo Pharmaceuticals. The EU’s strict regulations on drug safety, such as EMA guidelines, foster innovation, compliance, and encourage the adoption of targeted therapies and topical solutions across major markets.

In the U.K., market growth is driven by the rising preference for JAK inhibitors in cancer care. Products such as Sun Pharmaceutical’s minoxidil formulations are gaining popularity for their efficacy and bioavailability. France is witnessing increased demand for outpatient applications, with companies such as Johnson & Johnson offering specialized drug forms. Regulatory support for innovative production practices across Europe further enhances market prospects.

Asia Pacific Chemotherapy-Induced Alopecia Treatment Market Trends

Asia Pacific remains the fastest-growing region for the chemotherapy-induced alopecia treatment market, with China, India, and Japan emerging as key contributors. In India, heightened health awareness and supportive government oncology programs, such as the National Cancer Control Programme, are fueling demand for affordable treatments, with companies such as Sun Pharmaceutical Industries Ltd. leading the supply of cost-effective, generic options. China’s growth is underpinned by extensive cancer treatment expansion, where brands such as Pfizer Inc. provide high-quality drugs for supportive care.

Japan is carving a niche in premium-grade treatments for breast cancer patients, with Eli Lilly and Company gaining prominence. Rising healthcare investments and digital procurement platforms further bolster regional market expansion.

Competitive Landscape

The global chemotherapy-induced alopecia treatment market is highly competitive, with global and regional players competing on innovation, efficacy, and pricing. The rise of JAK inhibitors and personalized therapies intensifies competition, as companies aim to meet stringent regulatory and quality standards. Strategic partnerships, clinical trials, and investments in R&D are key differentiators.

Key Developments

- In July 2024, The U.S. Food and Drug Administration (FDA) approved Sun Pharmaceutical Industries Ltd.’s Leqselvi (deuruxolitinib) for treating severe alopecia areata. This milestone expands therapeutic options, offering patients an advanced JAK inhibitor that targets underlying immune pathways, improving hair regrowth outcomes and addressing unmet clinical needs.

- In May 2024, new positive topline results from a randomized, placebo-controlled, multi-dose, phase 2 clinical trial assessing STS-01 for the treatment of mild to moderate alopecia areata were released by Soterios Pharma, a clinical-stage life sciences company based in the United Kingdom.

Companies Covered in Chemotherapy-Induced Alopecia Treatment Market

- Sun Pharmaceutical Industries Ltd.

- Pfizer Inc.

- Eli Lilly and Company

- Taro Pharmaceutical Industries Ltd.

- Legacy Healthcare

- BPGbio, Inc.

- Johnson & Johnson Services, Inc.

- Cosmo Pharmaceuticals

Frequently Asked Questions

The chemotherapy-induced alopecia treatment market is projected to reach US$4.1 Bn in 2025.

Rising cancer prevalence, awareness of supportive care, and government oncology initiatives are key drivers.

The chemotherapy-induced alopecia treatment market is poised to witness a CAGR of 5.1% from 2025 to 2032.

Innovation in targeted therapies and personalized medicine forms the base for opportunities in Chemotherapy-Induced Alopecia Treatment.

Sun Pharmaceutical Industries Ltd., Pfizer Inc., and Eli Lilly and Company are among the key players.