- Industrial Machinery

- Centrifugal Industrial Dryer Market

Centrifugal Industrial Dryer Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Centrifugal Industrial Dryer by Dryer Type (Batch, Continuous, Semi-continuous, Custom-built), by Capacity (Low Capacity, Medium Capacity, High Capacity), Power Source (Electric, Steam, Gas-fired, Hybrid), Distribution Channel (Direct Sales, Distributors, OEM Partnerships, Aftermarket Services), Industry, and Regional Analysis, 20262033

Centrifugal Industrial Dryer Market Size and Trend Analysis

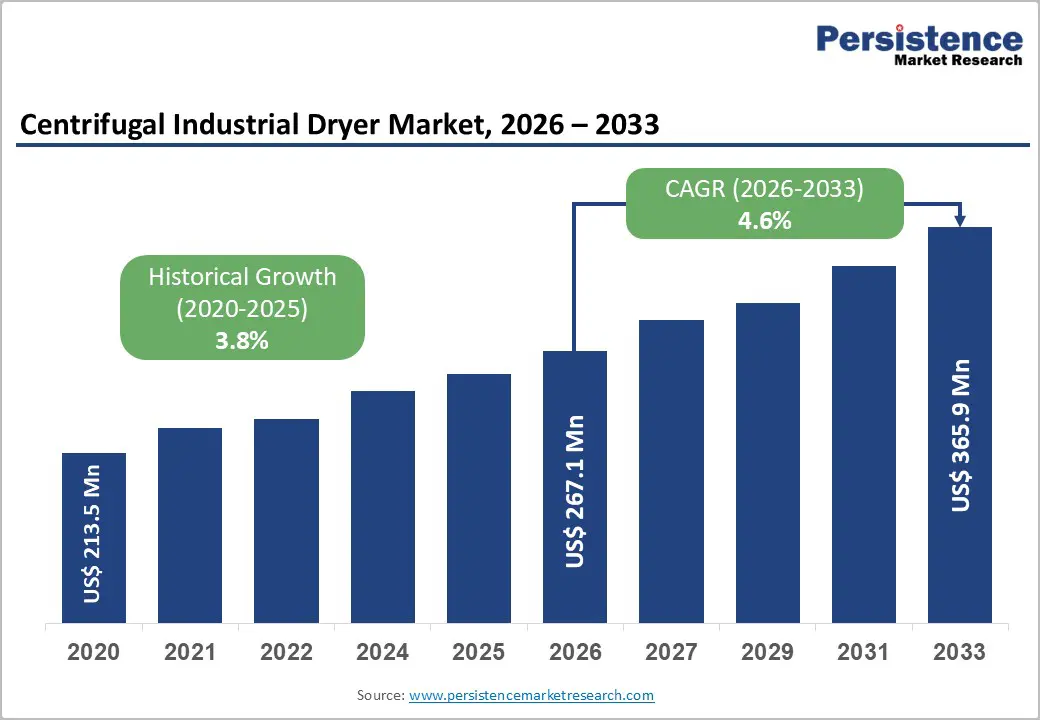

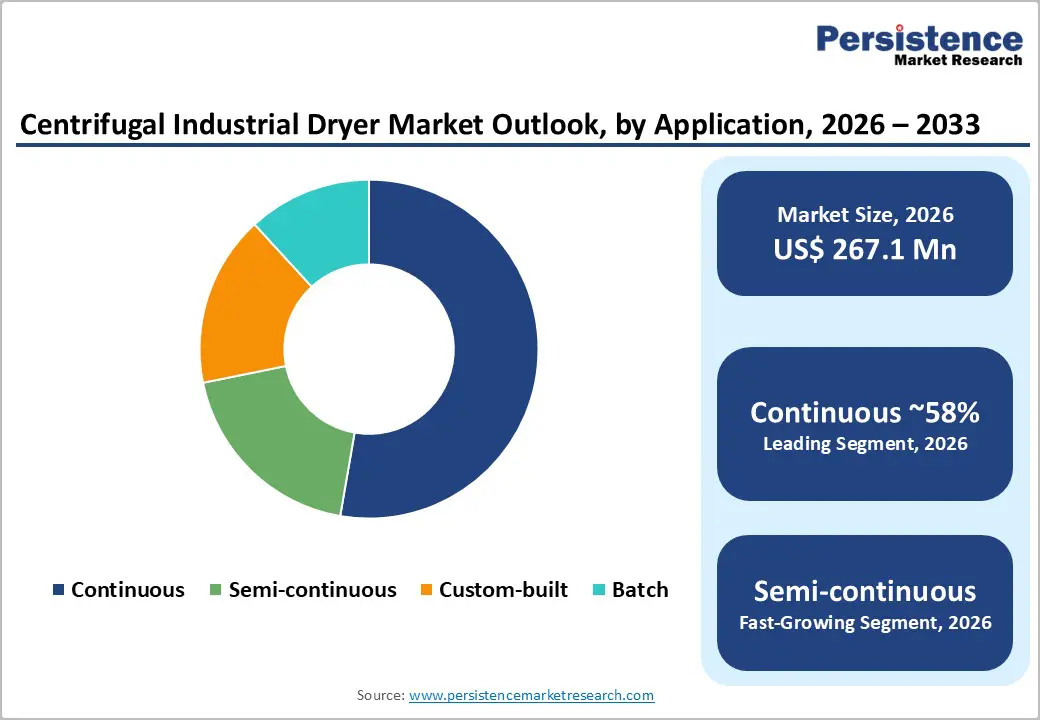

The global centrifugal industrial dryer market is projected to reach US$ 267.1 million in 2026 and US$ 365.9 million by 2033, growing at a CAGR of 4.6% over the forecast period.

Market growth is driven by Asia-Pacific industrialization, rising pharmaceutical API drying needs under GMP standards, and Industry 4.0 integration, which is transforming centrifugal dryers into smart, energy-efficient systems.

Key Market Highlights

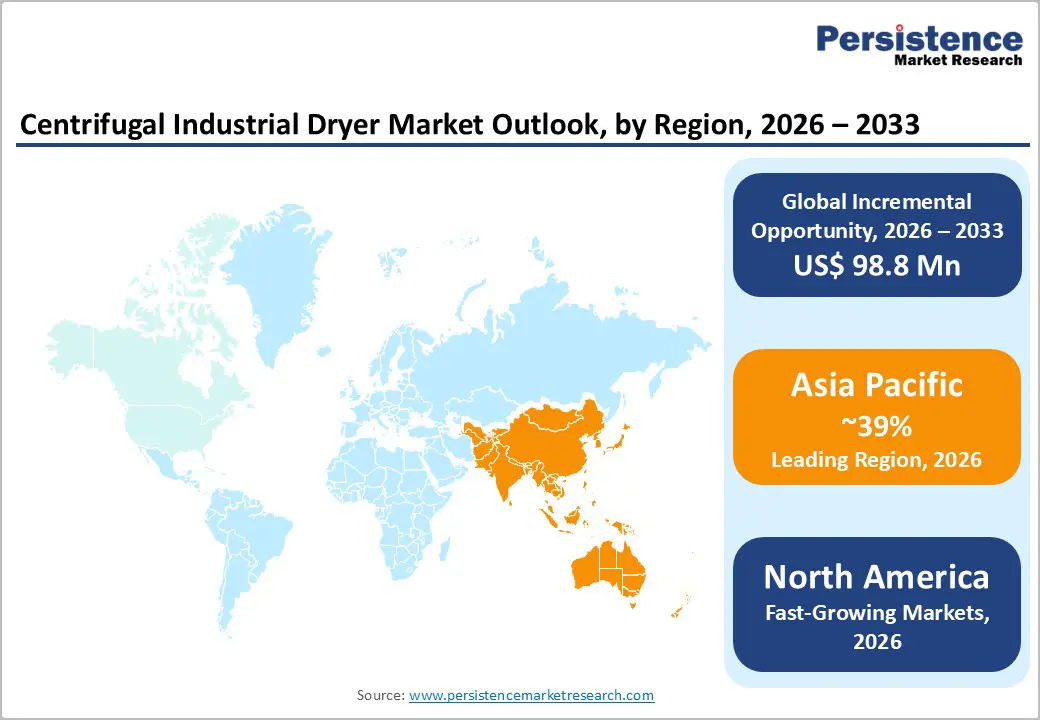

- Leading Region: Asia-Pacific dominates the global centrifugal industrial dryer market, holding a 39% share, driven by rapid industrialization in China and India, the expansion of pharmaceutical manufacturing, and large-scale food-processing operations that require efficient drying solutions to optimize production.

- Fastest Growing Region: North America maintains a strong market position with established manufacturing infrastructure, stringent regulatory frameworks, and advanced technology adoption, and is growing steadily through semiconductor manufacturing, pharmaceutical production, and food processing expansion.

- Leading Segment: Continuous centrifugal dryer systems account for approximately 58% of the market, and are preferred for high-volume production environments that require efficient, uninterrupted drying operations to support large-scale manufacturing and optimize production efficiency.

- Fastest-Growing Segment: Electric-powered centrifugal dryers exhibit a 7.8% CAGR, driven by precise temperature control, superior Industry 4.0 compatibility, and widespread electrical infrastructure that supports adoption across pharmaceutical and specialty applications.

- Key Opportunity: Pharmaceutical active pharmaceutical ingredient (API) drying and GMP-compliant drying solutions represent the fastest-growing segment, with expanding pharmaceutical manufacturing across the Asia-Pacific region and stringent regulatory requirements driving demand for specialized, precision-engineered centrifugal drying systems.

| Key Insights | Details |

|---|---|

| Centrifugal Industrial Dryer Market Size (2026E) | US$267.1 Mn |

| Market Value Forecast (2033F) | US$ 365.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.8% |

Market Dynamics

Drivers - Rapid industrial growth in Asia Pacific is accelerating demand for advanced centrifugal dryers across food and pharmaceutical manufacturing sectors

Rapid industrial growth across the Asia Pacific region, especially in China and India, is strongly increasing demand for advanced centrifugal drying solutions across multiple manufacturing industries. The food processing sector remains the leading application area, valued at around US$ 1,050 million in 2024 and expected to reach nearly US$ 1,540 million by 2035.

The growth is supported by continuous demand for efficient drying systems that help preserve flavour, extend shelf life, and ensure food safety through accurate moisture control. At the same time, the pharmaceutical industry is witnessing rapid expansion due to the rising production of active pharmaceutical ingredients (APIs).

Manufacturers increasingly require high-performance centrifugal dryers that operate in GMP-compliant environments and deliver precise temperature and moisture control for heat-sensitive compounds. Additionally, rising urbanization, expanding middle-class populations, and growing industrial infrastructure across emerging economies are creating sustained demand for efficient manufacturing equipment that improves productivity, reduces operational costs, and supports long-term industrial growth.

Industry 4.0 integration is transforming centrifugal dryers into intelligent, data-driven systems, enabling efficiency, predictive maintenance, and process optimization

The integration of Industry 4.0 technologies such as artificial intelligence, the Internet of Things, and predictive analytics is transforming centrifugal dryers into intelligent, connected production assets. By 2025, more than half of industrial companies are expected to adopt Industry 4.0 solutions, driving strong demand for smart drying systems with real-time monitoring and automated process optimization. Modern centrifugal dryers now offer AI-enabled predictive maintenance that reduces unexpected downtime, improves energy efficiency, and maintains consistent product quality.

Cloud-based connectivity enables manufacturers to track equipment performance across multiple facilities, identify inefficiencies, and anticipate component failures. This digital transformation is also creating new opportunities for waste reduction, energy optimization, and resource efficiency.

As a result, manufacturers are increasingly willing to pay premium prices for advanced drying systems that deliver long-term operational savings, higher reliability, and improved sustainability performance.

Restraints - High upfront costs, complex retrofitting requirements, and regulatory compliance challenges limit centrifugal dryer adoption, particularly for small manufacturers

Centrifugal dryer systems require significant upfront capital investment, particularly for advanced models that include automation, specialized materials, and customized engineering designs. These costs can be challenging for small and mid-sized manufacturers with limited budgets. Integration becomes even more complex when upgrading or retrofitting existing production facilities, as it often requires major structural modifications, utility upgrades, and extensive operator training. Such requirements extend project timelines and increase overall ownership costs.

In addition, stringent environmental regulations require the installation of wastewater treatment units, emission control systems, and energy-efficient components, thereby increasing capital and compliance costs. Market growth is also affected by supply chain disruptions, fluctuations in raw material prices, and dependence on specialized components. These factors increase lead times for customized equipment and limit access for manufacturers that lack strong technical expertise or financial flexibility.

Rising energy costs and strict environmental regulations are increasing compliance burdens and pushing demand toward more sustainable drying technologies

Industrial drying processes consume substantial amounts of energy, making centrifugal dryers a key focus area for cost control and sustainability initiatives. Rising energy prices and increasing pressure to reduce carbon emissions are creating challenges for both equipment manufacturers and end users. Environmental regulations governing air emissions, wastewater discharges, and waste handling require continuous monitoring and additional pollution-control systems, thereby increasing operational complexity and compliance costs.

Many governments are introducing stricter policies to promote energy efficiency, low-emission manufacturing, and circular-economy practices. These policies encourage companies to explore alternative technologies or upgrade to more energy-efficient systems. As a result, conventional centrifugal dryer providers face increasing competition from innovative solutions that promise lower energy consumption and reduced environmental impact, thereby exerting pressure on pricing and accelerating the need for technological advancements.

Opportunity - Growing wastewater treatment investments are creating strong demand for centrifugal dryers supporting sludge reduction, resource recovery, and environmental compliance

The water and wastewater treatment sector offers strong growth potential for centrifugal dryer manufacturers, driven by rising demand for efficient sludge dehydration and solids handling solutions. Municipal treatment plants and industrial facilities are increasingly focused on reducing sludge volume, lowering disposal costs, and meeting strict discharge regulations.

Centrifugal dryers play a critical role in the treatment of mineralized mine water and in zero-waste processes by enabling water recovery and the extraction of valuable mineral salts.

Rapid investment in water infrastructure across the Asia-Pacific and emerging regions is further increasing demand for advanced dehydration systems. Wastewater treatment operators are prioritizing technologies that improve operational efficiency while supporting environmental compliance. As regulations become more stringent and disposal costs rise, demand for reliable centrifugal drying equipment that enables resource recovery and long-term cost savings is expected to grow steadily.

AI-enabled smart dryers with predictive maintenance capabilities are improving reliability, reducing downtime, and unlocking premium market opportunities

Technological advancements in artificial intelligence and IoT are creating significant opportunities for next-generation centrifugal dryers. Smart dryers equipped with advanced sensors and analytics enable real-time performance monitoring, predictive maintenance, and automated process optimization. These features help reduce unplanned downtime, extend equipment life, and lower maintenance costs by shifting from fixed schedules to condition-based servicing. Remote monitoring capabilities allow manufacturers to manage equipment across multiple sites and respond quickly to performance issues.

Companies investing in intelligent process control and AI-driven optimization are gaining access to premium customer segments by offering lower total cost of ownership and higher operational reliability. The adoption of edge computing and high-speed connectivity further enhances system responsiveness, making smart centrifugal dryers highly attractive for pharmaceutical, chemical, and food processing industries seeking efficiency and consistent quality.

Category-wise Analysis

Dryer Type Insights

Continuous centrifugal dryers account for approximately 58% of the total share, supported by their strong performance in high-volume, uninterrupted production environments. These systems are widely used in industries that require consistent throughput and minimal downtime, allowing manufacturers to maximize productivity and equipment utilization. Continuous dryers are particularly well-suited for large-scale food processing, chemical, and pharmaceutical operations where stable moisture control and predictable output are essential. Their dominance reflects growing preference for automation and streamlined production workflows.

Batch centrifugal dryers hold around 32% market share and continue to grow steadily, especially among manufacturers that require greater flexibility. These systems allow precise control over processing parameters and are ideal for handling varying batch sizes and specialized products. Manual and automated batch options make them attractive for niche and high-value applications.

Power Source Insights

Electric-powered centrifugal dryers lead the market with approximately 52% share, driven by their wide availability, precise temperature control, and easy integration with automated production systems. These systems are especially favored in pharmaceutical and specialty chemical industries where strict process control is critical. Electric dryers also align well with Industry 4.0 technologies, enabling real-time monitoring and digital optimization.

Steam-powered systems account for around 28% of market demand and are valued for their indirect heating capability, which reduces contamination risks. They are commonly used in food and pharmaceutical applications where product purity is essential. Gas-fired and hybrid dryers make up the remaining share, offering flexibility and cost advantages for large-scale operations. These systems allow manufacturers to optimize energy use through fuel switching and support long-term operational efficiency.

Capacity Insights

Medium-capacity centrifugal dryers represent nearly 48% of total market demand, offering an ideal balance between investment cost and production efficiency. With processing capacities ranging from 5,000 to 15,000 kg per hour, these systems meet the needs of most mid-sized manufacturing facilities across the food, chemical, and pharmaceutical sectors. They provide operational flexibility while maintaining favorable economics.

High-capacity dryers account for about 35% of the market, reflecting increasing consolidation toward large-scale manufacturing facilities that benefit from economies of scale and lower per-unit processing costs. These systems are commonly used in large industrial plants with continuous production requirements. Low-capacity dryers serve specialized and small-scale applications, representing approximately 17% of demand. They are typically used for niche products and customized processing needs.

Distribution Channel Insights

Direct sales dominate the market with around 54% share, as large and customized centrifugal dryer systems require close collaboration between manufacturers and end users. This channel allows suppliers to provide tailored engineering support, installation services, and long-term maintenance solutions. Distributor networks account for approximately 28% of market demand and play an important role in expanding regional reach and improving equipment accessibility.

OEM partnerships represent about 12% of the market, with centrifugal dryers integrated into complete processing systems supplied by equipment manufacturers. Aftermarket services contribute roughly 6% of total market value, including spare parts, maintenance contracts, and system upgrades. These services strengthen customer relationships, ensure equipment longevity, and generate recurring revenue for manufacturers.

Regional Insights

North America Centrifugal Industrial Dryer Market Trends

North America is a mature and well-established market. Growth is supported by strong demand for advanced, high-performance drying solutions across pharmaceutical, food processing, and water treatment sectors. The region benefits from robust industrial infrastructure and strict regulatory standards related to product quality and environmental compliance.

The United States remains a global leader in pharmaceutical manufacturing, with strong domestic API and formulation production driving demand for GMP-compliant centrifugal dryers. Additionally, growth in the food processing industry and increasing focus on extended shelf life are supporting the adoption of modern drying technologies. Investments in water treatment infrastructure and Industry 4.0 adoption further accelerate demand for smart, connected centrifugal dryers with predictive maintenance capabilities.

Europe Centrifugal Industrial Dryer Trends

Europe represents a significant market. Strong pharmaceutical manufacturing, advanced food processing industries, and strict environmental regulations support steady demand for centrifugal dryers. Countries such as Germany, the United Kingdom, France, and Spain play a key role due to their established industrial base. European manufacturers are increasingly focused on sustainability, energy efficiency, and circular economy practices.

As a result, drying technologies that support waste reduction, sludge treatment, and resource recovery are gaining traction. Regulatory frameworks related to emissions control and energy efficiency are driving the modernization of industrial equipment. These factors allow manufacturers offering advanced, energy-efficient systems to achieve premium pricing and long-term customer loyalty.

Asia Pacific Centrifugal Industrial Dryer Trends

Asia Pacific leads the global centrifugal industrial dryer market, supported by rapid industrialization and expanding manufacturing sectors. China dominates regional demand due to its strong chemical, pharmaceutical, and food processing industries, creating a consistent need for high-capacity drying solutions. India is experiencing rapid growth in pharmaceutical manufacturing, particularly in API production, driving demand for GMP-compliant centrifugal dryers.

Southeast Asian countries are benefiting from urbanization, industrial expansion, and infrastructure development, further supporting market growth. Japan continues to demand high-end, technologically advanced dryers for specialty chemical and pharmaceutical applications. Government-led industrial initiatives and supportive investment policies across the region are accelerating equipment adoption.

Competitive Landscape

The global centrifugal industrial dryer market is moderately consolidated, with approximately 15–20 major global manufacturers holding strong technological and market positions. Gala Industries, founded in 1959, is the largest manufacturer, holding an estimated 18% global market share. The company offers a broad product range from 500 kg/hr to 150,000 kg/hr and has delivered over 8,000 units worldwide.

Other key players, including ZIRBUS technology GmbH, Rösler Oberflächentechnik GmbH, Wave Power Equipment, and Sukup Manufacturing Co., collectively hold an additional 35–40% share. Competition from Chinese manufacturers is increasing due to cost advantages and application-specific solutions. Market differentiation is driven by energy efficiency, digital integration, customization capabilities, and long-term service support.

Key Market Developments

- In September 2025: Gala Industries strengthened its technology leadership by integrating AI-driven IoT and predictive maintenance into centrifugal dryers, enabling real-time monitoring, proactive failure detection, and automated process optimization, significantly reducing downtime and improving efficiency for pharmaceutical and food manufacturers.

- In May 2025: Rösler Oberflächentechnik GmbH introduced closed-loop water recycling solutions combined with centrifugal drying technology, helping industrial users lower water consumption, reduce operating costs, and achieve sustainability goals through efficient waste minimization and process water reuse.

- In January 2025: ZIRBUS technology GmbH launched a modular centrifugal dryer platform tailored for pharmaceutical API drying, offering scalable capacity, strict GMP compliance, enhanced contamination control, and seamless integration with existing production lines to improve operational flexibility.

Companies Covered in Centrifugal Industrial Dryer Market

- Gala Industries, Inc.

- ZIRBUS technology GmbH

- Gostol TST d.d.

- Genox Recycling Tech Co., Ltd.

- Firex s.r.l.

- Sukup Manufacturing Co.

- Auto Technology Company

- BelAir Finishing Supply Corp.

- Rösler Oberflächentechnik GmbH

- Wave Power Equipment

- Sino-alloy Machinery Inc.

- Greco Brothers Incorporated

- Brüel Systems A/S

- Delcra Chemicals

- FLS

- MAAG Group

- Kerone

- Sunkaier Industrial Technology

Frequently Asked Questions

The global centrifugal industrial dryer market is expected to reach US$ 365.9 million by 2033, growing at a 4.6% CAGR.

Market growth is driven by Asia Pacific industrialization, expanding pharmaceutical API production, and rapid adoption of AI- and IoT-enabled smart dryers.

Continuous centrifugal dryers lead the market with about 58% share, supported by high-volume, uninterrupted industrial production requirements.

Pacific dominates the global market due to rapid industrial growth, while North America remains strong in premium and advanced systems.

Major opportunities lie in pharmaceutical API drying, GMP-compliant systems, and wastewater sludge dehydration applications.

The market is led by Gala Industries, ZIRBUS technology GmbH, Rösler Oberflächentechnik GmbH, Wave Power Equipment, and Sukup Manufacturing Co.