- Home Appliances

- Ceiling Fan Market

Ceiling Fan Market Size, Share, and Growth Forecast 2026 - 2033

Ceiling Fan Market by Fan Type (Standard Ceiling Fans, Decorative Ceiling Fans, Energy Efficient Ceiling Fans, Smart Ceiling Fans, Industrial Ceiling Fans, Ceiling Fans with Integrated Light, Misc.), Technology (AC Motor Technology, DC Motor Technology, BLDC Motor Technology), End-user (Residential, Commercial, Industrial), by Distribution Channel (Offline Retail, Online Retail), and Regional Analysis, 2026-2033

Global Ceiling Fan Market Size and Trend Analysis

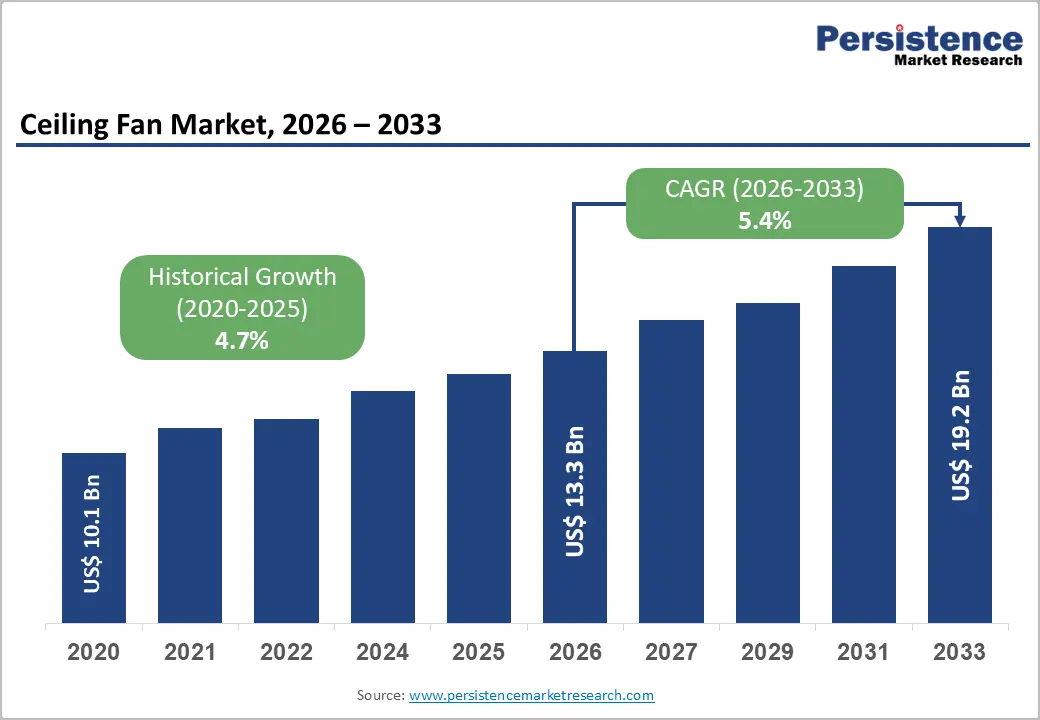

The global ceiling fan market size is expected to be valued at US$ 13.3 billion in 2026 and projected to reach US$ 19.2 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033. Shift toward energy-efficient cooling appliances, accelerated adoption of BLDC motor technology, and the integration of smart-home features such as voice control and IoT connectivity.

Government-led efficiency mandates, including the Bureau of Energy Efficiency (BEE) star labelling in India, the U.S. Department of Energy (DOE) efficiency standards, and the EU Ecodesign Directive, are pushing manufacturers to redesign product portfolios. Rapid urban housing construction across the Asia Pacific and replacement-led demand in mature markets are reinforcing volume growth.

Key Industry Highlights:

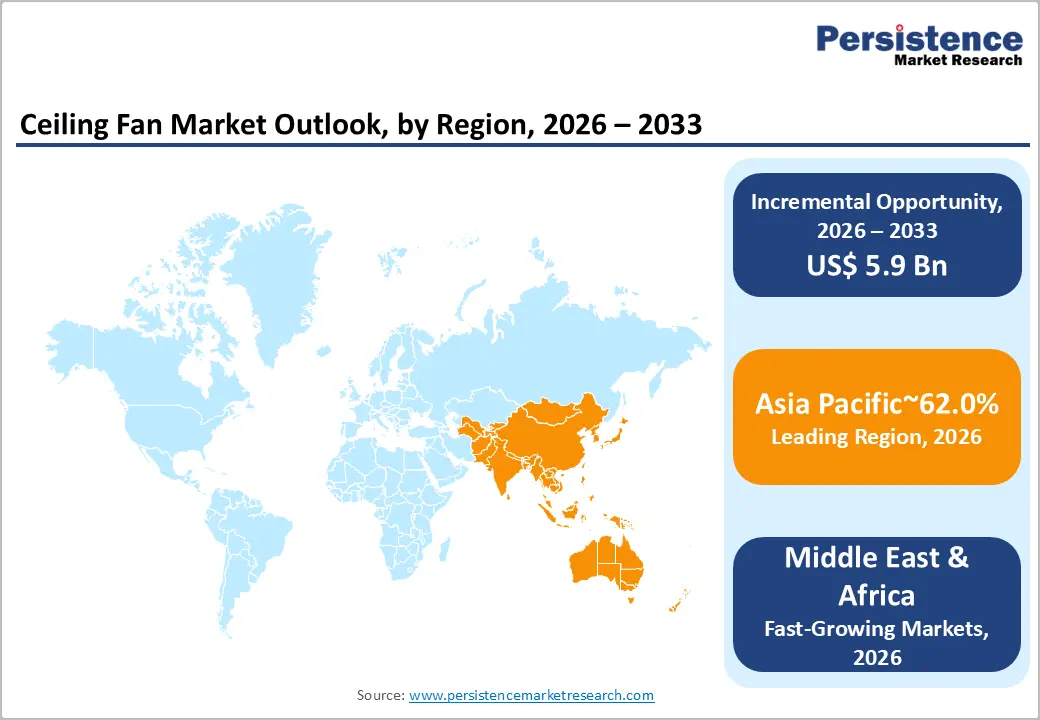

- Leading Region: Asia Pacific leads the global ceiling fan market with a 62% share in 2025, driven by tropical climate, mass housing construction, and dominant manufacturing capacity in China and India.

- Fast-Growing Region: Asia Pacific is also the fastest-growing region, propelled by BEE mandates in India, MEPS enforcement in China, and rapid BLDC and smart-fan adoption across emerging Southeast Asian markets.

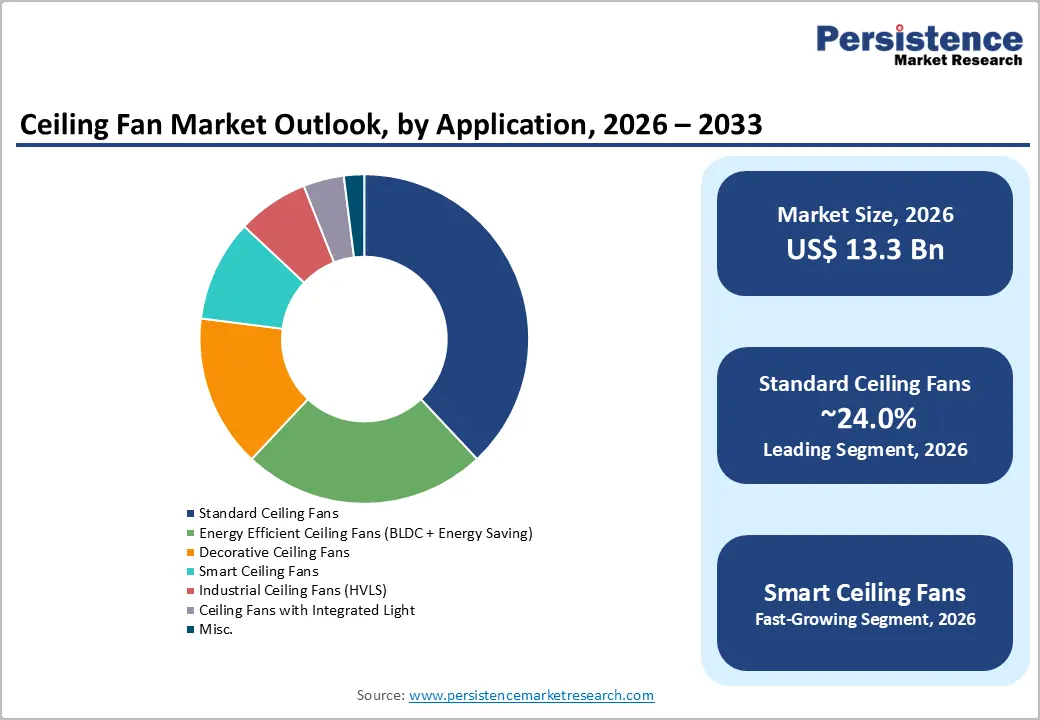

- Leading Category: Standard ceiling fans dominate the fan-type category with 38% share in 2025, reflecting universal affordability and entrenched demand across mass-market residential housing in emerging economies.

- Fast-growing Category: Smart ceiling fans are the fastest-growing fan type, expanding at over 5% CAGR through 2033, driven by IoT, voice-assistant integration, and rising premium-residential adoption.

- Opportunity: A key opportunity lies in BLDC ceiling fans linked to green-building certifications such as LEED, GRIHA, and CII Green-Pro, unlocking institutional and commercial procurement demand.

DRO Analysis

Drivers - Energy Efficiency Mandates and BLDC Motor Adoption Reshape Product Demand

Stringent energy-efficiency regulations are fundamentally restructuring global ceiling fan demand toward high-efficiency variants. The Bureau of Energy Efficiency (BEE) in India revised its star-labelling program for ceiling fans effective January 2023, mandating minimum service value benchmarks that effectively pushed legacy induction-motor fans out of higher star bands.

BLDC motor fans consume nearly 50% less electricity than conventional AC induction fans, with Havells India Limited's ECOACTIV range delivering estimated household savings of up to INR 1,900 annually. The U.S. Department of Energy ceiling fan conservation standards under 10 CFR Part 430 and the EU Ecodesign Regulation 327/2011 are similarly accelerating premiumization, with manufacturers reporting double-digit volume growth in efficient SKUs.

Construction Boom and Housing Completions Anchor Volume Demand

Sustained construction activity across emerging and developed economies is generating substantial first-fit demand for ceiling fans. The U.S. Census Bureau reported total construction spending of US$ 2.16 trillion in January 2024, with private residential spending at US$ 912.8 billion, while Statistics Canada recorded residential building permits worth CAD 8,013.3 million in December 2025, with multi-unit dwellings contributing US$ 5,528.9 million.

In India, the real estate sector contributes nearly 13% to GDP and is projected to reach US$ 1 trillion by 2030, according to IBEF. Each new housing unit typically requires 3 to 5 ceiling fans, directly translating sectoral construction strength into appliance demand.

Restraints - Volatility in Copper and Steel Input Costs Compresses Margins

Ceiling fan manufacturing is highly exposed to copper and electrical steel pricing, with these inputs accounting for 30 to 40% of the bill of materials. London Metal Exchange (LME) copper prices traded above US$ 9,500 per tonne through much of 2024, well above the five-year average.

Indian manufacturer Crompton Greaves Consumer Electricals and Orient Electric have publicly flagged input-cost pressure in investor disclosures, with several brands implementing price hikes of 3 to 6% to protect operating margins. This volatility complicates entry-level fan pricing, where consumers remain highly price-sensitive and sustained inflation can defer replacement-cycle purchases.

Air-Conditioner Substitution in Affluent Urban Households

Falling room-air-conditioner prices and improving inverter efficiency are eroding ceiling fan share in higher-income urban households. According to the International Energy Agency (IEA), global air-conditioner stock surpassed 2 billion units in 2024 and is projected to reach 5.6 billion by 2050. In tier-1 Indian cities and Southeast Asian metros, AC penetration in new apartments now exceeds 45%, partially displacing ceiling fans as primary cooling devices. While ceiling fans remain complementary, the diversion of cooling-appliance budgets toward ACs constrains average selling price uplift in premium ceiling fan categories within affluent consumer segments.

Opportunities - Smart Ceiling Fan Adoption Powered by IoT-Enabled Home Ecosystems

Smart ceiling fans, the fastest-growing fan type expanding at a CAGR above 5% through 2033, present a substantial value-creation opportunity for manufacturers. Integration with Amazon Alexa, Google Home, and Apple HomeKit is becoming a baseline expectation in premium segments. Hunter Fan Company unveiled its HunterSMART™ portfolio and ZenTech smart ceiling fan series at PepCom's Digital Experience 2026 in Las Vegas in January 2026, while its Techne model with SIMPLEconnect® technology launched in June 2023.

With global smart-home device shipments forecast by IDC to surpass 1.4 billion units annually by 2027, ceiling fans are positioned as a high-utility, low-friction entry point into connected living, supported by adjacent traction in the smart home appliances market.

Sustainability-Linked Procurement and Green Building Codes

Green-building certification frameworks are creating procurement pull for certified energy-efficient ceiling fans in commercial and institutional projects. Crompton Greaves Consumer Electricals secured CII Green-Pro Certification for its ceiling fan portfolio at the Annual Green-Pro Summit 2024, validating life-cycle sustainability across resource use, emissions, and end-of-life management.

Globally, LEED-certified projects exceeded 195,000 by 2024 per U.S. Green Building Council data, while India's GRIHA and IGBC ratings now cover over 9 billion sq. ft. of registered footprint. Specification of certified BLDC fans in offices, hospitals, schools, and hospitality projects represents a structural opportunity, particularly aligned with the broader energy efficient appliances market trajectory.

Category-wise Analysis

Fan Type Insights

Standard ceiling fans retained category leadership with approximately 38% market share in 2025, driven by entrenched affordability and the sheer scale of replacement demand in mid-income households across Asia Pacific, Latin America, and Africa.

Despite the rise of premium variants, standard fans remain the default choice for new low- and mid-rise housing in India, Indonesia, Vietnam, and the Philippines, where typical retail prices range between US$ 25 and US$ 60. Mass-market manufacturers, including Crompton, Orient Electric, Havells, and Usha International, sustain this dominance through dense distribution networks spanning over 100,000 retail touchpoints in India alone, while OEM supply contracts with builders for affordable housing under schemes such as PMAY continue to anchor first-fit volumes.

Technology Insights

AC motor technology continues to lead the technology segment with an estimated 62% share in 2025, anchored by lower upfront cost and well-established global manufacturing ecosystems. AC induction motors remain the workhorse for entry-level and mid-tier fans, particularly in price-sensitive markets across South Asia, Sub-Saharan Africa, and parts of Latin America, where retail price points below US$ 40 dominate household purchases.

The segment faces structural pressure as BEE star-labeling in India and DOE efficiency rules in the U.S. progressively raise minimum performance thresholds. The displacement is gradual: legacy AC fans still account for the majority of the installed base, supported by extensive after-sales spare-parts availability and consumer familiarity, even as BLDC captures incremental demand.

End-user Insights

The residential end-user segment dominated the market with approximately 74% share in 2025, reflecting the universal role of ceiling fans as a fundamental household cooling appliance. Demand is reinforced by United Nations Department of Economic and Social Affairs projections that 68% of the world population will be urban by 2050, with most growth concentrated in housing-deficient economies.

India alone faces an urban housing shortage exceeding 10 million units per the Ministry of Housing and Urban Affairs estimates, while annual housing completions in China, Indonesia, and Vietnam continue to absorb large fan volumes. Replacement cycles of 8 to 12 years in mature markets such as the U.S. and Australia further sustain residential demand, with Energy Star-rated and BLDC variants gaining mainstream household acceptance.

Regional Insights

Asia Pacific Ceiling Fan Market Trends and Insights

Asia Pacific dominated the global ceiling fan market with approximately 62% share in 2025, anchored by the region's role as both the largest manufacturing hub and the largest consumption base. Tropical climates, vast housing-construction pipelines, and government-backed electrification drive sustained volume demand, while regulatory pushes on BLDC adoption in India and minimum energy performance standards (MEPS) in China are accelerating premium-segment growth. Trends include rapid e-commerce penetration, smart fan launches, and aggressive capacity additions by domestic majors.

China Ceiling Fan Market Size

In 2025, China ceiling fan market size touched US$ 3.5 billion. Massive residential-construction pipeline, MEPS enforcement under GB 12021 standards, and the role of Guangdong-based manufacturers such as Aerodynamic and Guangzhou-based OEMs as global export hubs have fuelled the market growth here.

India Ceiling Fan Market Size

India ceiling fan market size was US$ 2.7 billion in 2025, positioning as the fast-growing market in Asia. Growth is propelled by the BEE star-labelling overhaul effective January 2023, the shift to BLDC technology championed by Crompton, Havells ECOACTIV, Orient Aeroslim, and Atomberg, and the housing push under Pradhan Mantri Awas Yojana, which sanctioned over 12 million urban units.

North America Ceiling Fan Market Trends and Insights

North America holds a 13% share of the global ceiling fan market in 2025, characterized by replacement-led demand, premiumization, and strong adoption of smart, Energy Star-rated fans. Trends include integration with Alexa, Google Home, and Apple HomeKit, retrofit demand tied to single-family housing turnover, and a steady shift to DC and BLDC variants under tightening DOE efficiency standards.

U.S. Ceiling Fan Market Size

The U.S. ceiling fan market valuation in 2025 stood at US$ 1,408.7 million, supported by U.S. Census Bureau private residential construction spending of US$ 912.8 billion in January 2024 and total construction spending of US$ 2.16 trillion. Replacement demand from the existing housing stock of over 140 million units, combined with Hunter Fan Company's HunterSMART™ and ZenTech launches at PepCom 2026, anchors premium-segment growth.

Europe Ceiling Fan Market Trends and Insights

Europe holds a 10% share of the global ceiling fan market in 2025, with demand concentrated in southern Mediterranean economies and rising in northern markets due to extended summer heatwaves. Trends include EU Ecodesign Regulation 327/2011 compliance, surging interest in DC ceiling fans as low-energy alternatives to air conditioning, and design-led decorative variants serving hospitality and premium residential refurbishment.

Germany Ceiling Fan Market Size

Germany ceiling fan market was valued at US$ 302.4 million in 2025, the largest within Europe, driven by record summer temperatures recorded by the Deutscher Wetterdienst (DWD), growing aversion to fixed air-conditioning installations in residential apartments, and strong consumer affinity for premium DC fans from brands such as CasaFan and Westinghouse. Energy-efficiency-conscious purchasing aligned with EU efficiency labels reinforces premium-tier demand.

U.K. Ceiling Fan Market Size

The U.K. ceiling fan market is valued at US$ 214.2 million in 2025, supported by repeated heatwave seasons recorded by the UK Met Office, increasing retrofit demand in Victorian-era housing stock where central air conditioning is impractical, and rising hospitality-sector specifications across London and southeast England. Online channels, including Amazon UK and specialist retailers such as Fantasia Distribution, have widened consumer access to decorative and DC-motor variants.

Competitive Landscape

The global ceiling fan market is moderately fragmented, with the top 10 manufacturers collectively accounting for an estimated 40 to 45% of global revenues. Leadership is regionally segmented: Crompton, Havells, Orient Electric, Usha, and Atomberg dominate India; Hunter Fan, Hampton Bay, Casablanca, and Minka Aire lead North America; while Panasonic, KDK, and Chinese OEMs anchor Asia Pacific.

Strategic priorities include BLDC R&D, smart-home integration, expansion of D2C e-commerce, design-led decorative SKUs, and ESG-aligned manufacturing certifications such as CII Green-Pro. M&A and brand-licensing partnerships with smart-home ecosystems are emerging differentiators.

Key Developments:

- In Jan 2026, Hunter Fan Company, a leading global manufacturer of ceiling fans and smart home comfort solutions, showcased its latest innovations at PepCom’s Digital Experience 2026 in Las Vegas, unveiling its new HunterSMART™ portfolio and ZenTech smart ceiling fan series, marking a major advancement in connected ceiling fan technology.

- In June 2023, Hunter Fan Company introduced the Techne smart ceiling fan, which integrates SIMPLEconnect® smart technology, enabling seamless connectivity with major smart home ecosystems, including Alexa, Apple HomeKit, and Google Home. This allows users to control fan speed, lighting, and scheduling through voice commands or mobile applications, reflecting the growing demand for IoT-enabled ceiling fan solutions in residential environments.

Companies Covered in Ceiling Fan Market

- Hunter Fan Company

- Crompton Greaves Consumer Electricals Ltd

- Orient Electric Ltd

- Havells India Ltd

- Emerson Electric Co

- Panasonic Corporation

- Midea Group

- Haier Group

- Usha International

- Bajaj Electricals Ltd

- LG Electronics Inc

Frequently Asked Questions

The global ceiling fan market is expected to be valued at US$ 13.3 billion in 2026 and is projected to reach US$ 19.2 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033.

Demand is driven by stringent energy-efficiency mandates such as BEE star-labelling in India and DOE standards in the U.S., the rapid shift to BLDC motor technology, and sustained residential and commercial construction activity globally.

Asia Pacific leads the global ceiling fan market with approximately 62% share in 2025, anchored by China's US$ 3.5 billion and India's US$ 2.7 billion country markets, supported by tropical climate and large housing pipelines.

The key opportunity lies in smart ceiling fans integrated with IoT and voice-assistant ecosystems such as Alexa, Google Home, and Apple HomeKit, alongside BLDC adoption tied to green-building certifications.

Leading players include Hunter Fan Company, Crompton Greaves Consumer Electricals Ltd, Havells India Limited, Orient Electric Limited, Usha International Limited, Atomberg Technologies, Panasonic Corporation, Emerson Electric Co., and Big Ass Fans.