- Off-Road Equipment & Machinery

- Bolter Miner Market

Bolter Miner Market Size, Share, and Growth Forecast 2026 – 2033

Bolter Miner Market by Mining Technique (Room and Pillar, Longwall, Others), Power Source (Hydraulically Powered, Electrically Powered), Product Type (Bolter Miners, Others), Application (Coal Mining, Others), and Regional Analysis 2026 – 2033

Bolter Miner Market Share, Size, and Trends Analysis

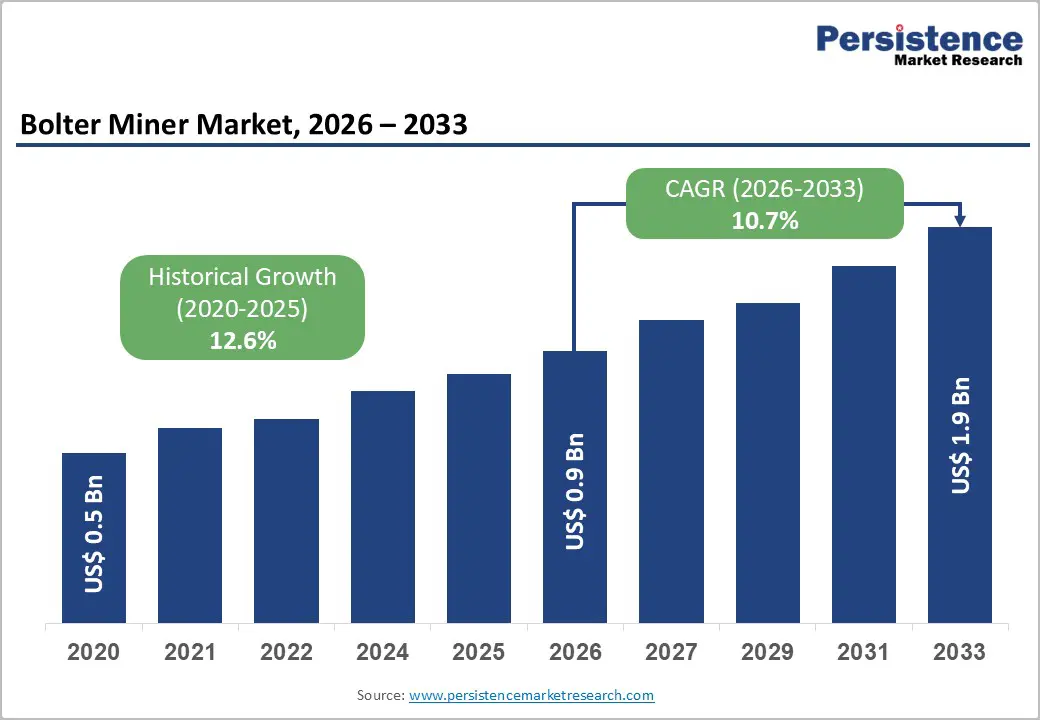

The global bolter miner market size is projected to be valued at US$0.9 billion in 2026 and is projected to reach US$1.9 billion by 2033, growing at a CAGR of 10.7% during the forecast period from 2026 to 2033, driven by the dual imperatives of enhanced underground safety standards and the automation of mineral extraction processes. Rising underground mining activities, driven by global mineral demand, support expansion alongside safety regulations mandating mechanized equipment.

Key Industry Highlights:

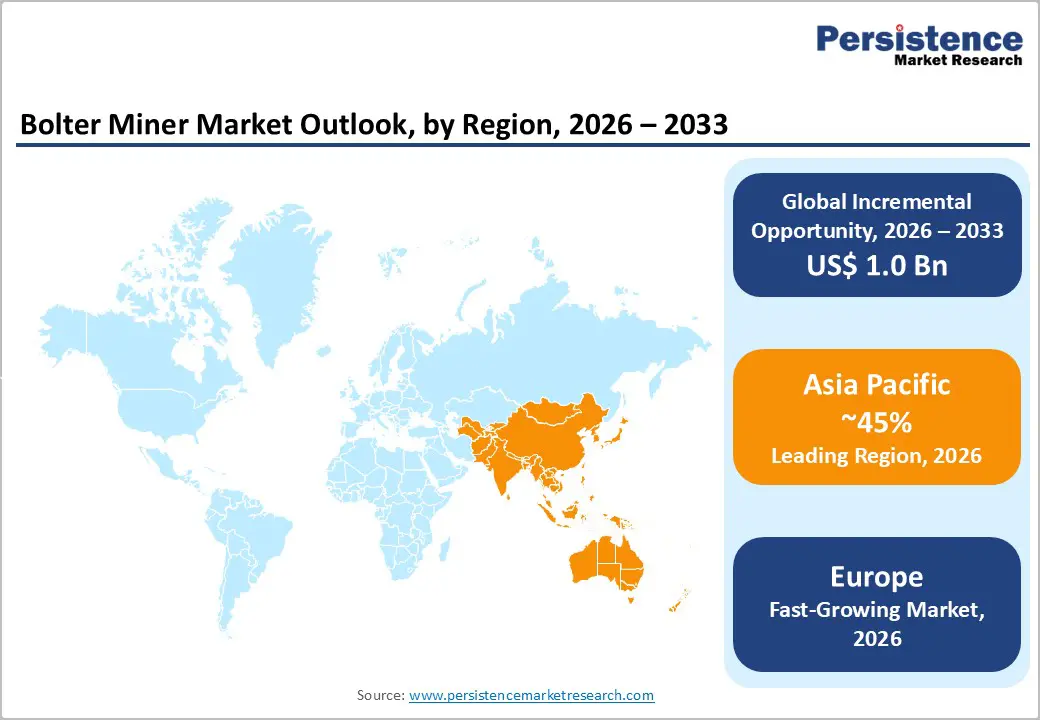

- Leading Region: Asia Pacific is expected to lead the global mining equipment market with around 45% share, supported by high coal and metal production volumes, expanding mining infrastructure in China and India, and large-scale industrial demand.

- Leading Mining Technique: Longwall mining is anticipated to remain the leading mining technique in the global mining equipment market, holding around 47.4% share, as it offers higher productivity, mechanization, and safety benefits for large-scale underground operations.

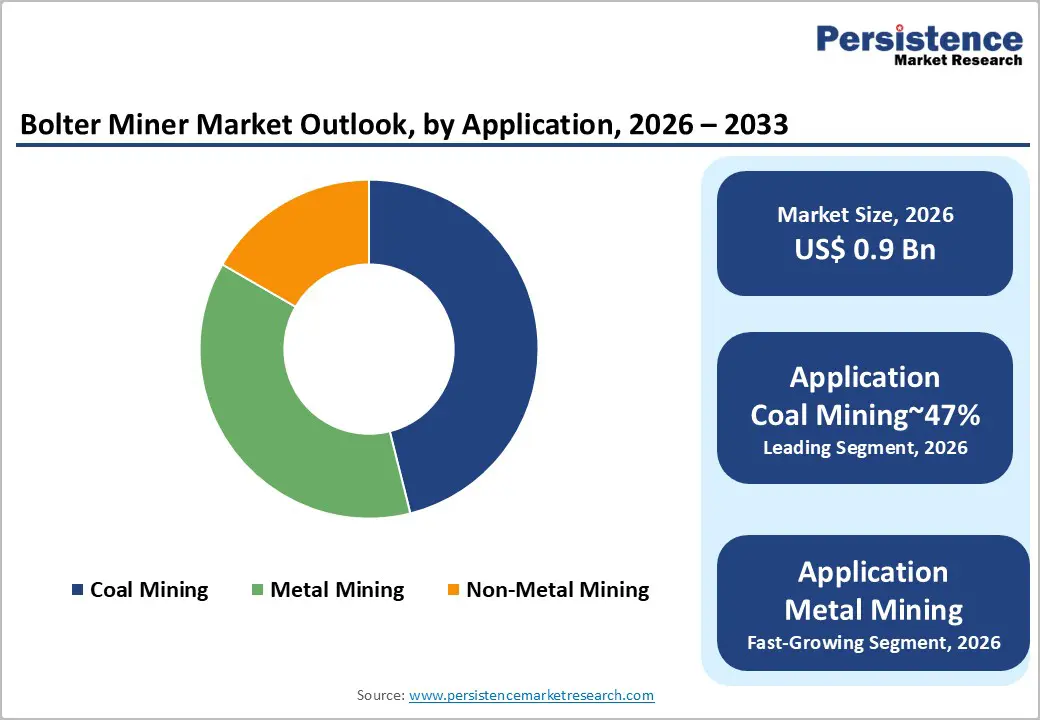

- Leading Application: Coal mining is expected to stay the dominant application, accounting for approximately 47%share of this segment.

- Key Industry Developments: Electrification of bolter miners accelerated, with increased use in longwall and metal mining. In November 2025, Sandvik launched the DS422iE, the industry’s first battery-powered cable bolter. This zero-emission rig offered up to four hours of operation, tele-remote control, and automated features, enhancing environmental compliance, reducing health risks, and integrating with digital systems for real-time sustainability monitoring.

| Key Insights | Details |

|---|---|

| Bolter Miner Market Size (2026E) | US$0.9 Bn |

| Market Value Forecast (2033F) | US$1.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Ongoing Growth in Underground Mining Driven by Energy Security and Critical Mineral Demand

The bolter miner market is structurally driven by the continued expansion of underground mining across both energy and metal segments, despite ongoing energy transition narratives. Thermal coal demand remains resilient in developing economies where baseload power reliability and industrial growth priorities outweigh short-term decarbonization targets. In parallel, metallurgical coal consumption continues to be anchored by global steel production, while accelerating demand for battery metals is pushing rapid development of new underground hard-rock mines. These mining environments require fast, continuous roadway development with immediate roof stabilization, making bolter miners indispensable for maintaining production schedules and workforce safety.

This dual demand profile creates a balanced growth dynamic for bolter miners. Coal mining applications provide consistent equipment volumes through sustained replacement and capacity expansion cycles, while metal mining operations offer structurally higher growth as deeper, more geologically complex projects come online. Bolter miners uniquely address this requirement by enabling simultaneous excavation and roof bolting, reducing exposure time in unsupported headings, and improving operational continuity. This combination positions bolter miners as critical productivity and safety assets across evolving underground mining portfolios.

Skilled Operator Shortages and Training Constraints Limiting Bolter Miner Adoption

A critical structural barrier for the bolter miner market is the persistent shortage of skilled operators capable of handling mechanized bolting systems. Bolter miners require specialized technical competence across roof bolting mechanics, hydraulic systems, and underground safety protocols, typically supported by mandatory MSHA-certified training programs and recurring refresher requirements. As the global mining industry faces a widening skills gap, the availability of experienced operators has not kept pace with increasing mechanization. This mismatch is particularly pronounced as aging workforces retire faster than new talent can be trained, creating operational risk for mines seeking to deploy advanced bolter miner fleets.

The challenge is more acute in emerging mining regions, where formalized training infrastructure and mechanized mining exposure remain limited. High operator vacancy rates in markets such as India and parts of Southeast Asia reflect the inability of existing vocational and in-house training programs to scale at the same speed as mine development plans. As a result, bolter miner penetration remains structurally constrained in high-growth coal and metal mining regions, slowing the transition toward safer, more productive underground development despite strong underlying demand drivers.

Electric Bolter Miners for Sustainable Underground Development

The accelerating push toward green mining and stricter controls on diesel particulate matter is creating a clear, technology-driven opportunity for electrically powered bolter miners. As underground mines move deeper, ventilation becomes a dominant operating cost and a critical safety constraint. Electrified bolter miners directly address this challenge by eliminating diesel emissions at the face, reducing heat load, noise levels, and airflow requirements in development headings. While tethered electric bolters are already established, the next phase of opportunity lies in battery-electric and hybrid mobility solutions that enable emission-free tramming, relocation, and auxiliary movements without reliance on trailing cables.

Electrification shifts bolter miners from productivity-focused assets to strategic cost-reduction tools. Lower ventilation demand improves mine energy efficiency, simplifies regulatory compliance, and enhances ESG performance reporting, making electric bolters attractive for both new developments and fleet retrofits. Manufacturers that offer modular battery systems, retrofit kits, or hybrid electric architectures can accelerate adoption by allowing operators to electrify incrementally rather than through full fleet replacement. In June 2024, Epiroc deployed the first battery-electric Boltec M10 bolter at Leeville mine in the US. The rig improves the operator's work environment with reduced noise and a smaller environmental footprint, offering perks such as optimized operational efficiency and enhanced sustainability metrics for reports on underground gold mining transitions to electrification.

Category–wise Analysis

Mining Technique Insights

The room and pillar mining segment is anticipated to lead, accounting for 40% of total demand in 2026, as its operational structure is structurally aligned with continuous development requirements where bolter miners are mission-critical assets. The technique’s reliance on systematic roof support, continuous haulage, and flexibility in navigating irregular ore geometries positions it as the preferred method across mature coal markets, particularly in North America and Australia. Stable pillar layouts reduce geotechnical risks while enabling steady production rates, reinforcing capital efficiency, and sustaining long-term equipment utilization.

Longwall mining represents the fastest-growing technique, driven by scale-driven productivity optimization rather than extraction flexibility. While bolter miners are not deployed at the coal face, they are indispensable for gate road development, which increasingly dictates longwall panel throughput as panel dimensions expand. Accelerated tunnel development requirements, combined with automation-led productivity gains, elevate demand for high-capacity bolter miners. Blast mining and other niche techniques collectively account for the remaining share, serving selective geological conditions where mechanized continuous development offers limited operational advantage.

Application Insights

Coal mining is expected to lead, accounting for approximately 47% market share in 2026, supported by the industry’s massive global production scale and the shift toward underground extraction as surface reserves decline. India’s push to nearly double annual output, combined with the resumption of regulated mining in regions such as Meghalaya, is driving demand for mechanized, high-capacity bolting systems. Safety imperatives, particularly roof and rib fall mitigation, make integrated bolter miners essential, while deeper seams increase the need for dense anchorage to maintain operational speed and stability.

Key market drivers include thermal power demand in emerging economies, labor shortages prompting automation, and continuous-operation efficiencies compared to traditional drill-blast-bolt cycles. Recent industrial trends include methane drainage integration, 3D digital twin mapping for bolting optimization, and a rapid shift to battery-electric fleets to reduce ventilation costs and emissions. Regulatory pressure from MSHA, DGMS, and ESG-focused investors reinforces mechanized bolting adoption. Equipment such as Sandvik’s MB600 bolter miner illustrates the move toward autonomous, high-efficiency coal mining operations.

Metal mining is projected to be the fastest-growing segment, driven by the global critical minerals push for EV batteries and renewable energy infrastructure. Deep underground deposits of copper, nickel, and rare earth elements require automated bolting for stability in narrow, high-pressure tunnels. High-value metals enable operators to invest in advanced fleets, while ESG and zero-emission mandates accelerate the adoption of battery-electric systems.

Recent developments include large-scale fleet orders from Hindustan Zinc and digital integration of autonomy software through acquisitions such as Caterpillar’s RPMGlobal. Trends such as AI-guided real-time rock monitoring, digital twin-assisted anchorage adjustment, and brownfield retrofitting of existing mines are shaping deployment strategies. Policy support, including India’s mining budget and the EU’s Critical Raw Materials Act, is expediting underground development. Leading solutions, exemplified by Epiroc’s zero-emission bolters and Sandvik’s autonomous i-series rigs, highlight the emphasis on safety, efficiency, and regulatory compliance in the expanding metal mining market.

Regional Insights

Asia Pacific Bolter Miner Market Trends

Asia Pacific is estimated to lead, commanding approximately 45% of global share in 2026, driven by large-scale mechanization and high-capacity mining operations. Growth is underpinned by government-led initiatives promoting intelligent and safe mining, consolidation of smaller mines into larger state-owned enterprises, and the rising demand for coal and other industrial minerals. Investments focus on mechanization, automation, and safety upgrades, creating a competitive landscape where both global majors and domestic manufacturers compete aggressively.

China is the primary growth engine within the region, accounting for the majority of mining mechanization efforts. National policies under the "Intelligent Mining" initiative promote large-scale, high-efficiency bolter miners and enforce rigorous safety standards. Chinese manufacturers such as SANY and CRCHI leverage local production advantages and regulatory alignment to deliver cost-effective solutions, positioning China as the central hub in Asia Pacific’s leading mining machinery market.

Europe Bolter Miner Market Trends

Europe is expected to be the fastest-growing regional market, driven by investments in non-metal mining and specialized tunneling projects. Growth is fueled by regulatory mandates enforcing low-emission and electric-hybrid bolter miners, creating demand for advanced, energy-efficient machinery. The region serves as a strategic testbed for "Green Mining" technologies, with manufacturers deploying low-emission prototypes before global rollout. EU harmonization directives and aging mine infrastructure further accelerate adoption, while the market remains fragmented with the key players driving M&A activity and technological innovation.

Germany leads regional activity, reflecting both coal and potash mining modernization. German regulations on emissions and environmental compliance incentivize electric-hybrid machinery adoption, while technological sophistication in German mining equipment firms ensures high operational efficiency. Poland also contributes steady demand, particularly from copper mines operated by KGHM, but Germany’s combination of regulatory pressure and industrial expertise positions it as the central hub in Europe’s fastest-growing mining machinery market.

North America Bolter Miner Market Trends

North America is expected to represent a mature and stagnant market, with limited growth due to established mining operations and replacement-focused equipment cycles. Market dynamics are shaped by regulatory compliance requirements, aging fleet modernization, and the adoption of safety-focused machinery, which sustain consistent demand but constrain expansion. Investments are directed toward retrofitting existing fleets with IoT-enabled diagnostics, automated temporary roof support systems, and proximity detection technologies, reinforcing operational reliability rather than rapid market growth.

The U.S. dominates regional activity, driven by Appalachian and Illinois basin operations. MSHA regulations heavily influence equipment design, mandating remote bolting and safety automation, which reduces operational incidents. U.S.-based manufacturers such as Caterpillar lead innovation in automation and compliance-focused machinery, capitalizing on regulatory-driven replacement demand rather than new production expansion. This combination of stringent safety requirements, fleet modernization, and regulatory enforcement positions the U.S. as the central hub within a mature North American mining equipment market.

Competitive Landscape

The global bolter miner market is moderately consolidated, with the top five players, Sandvik, Epiroc, Caterpillar, Komatsu, and Joy Global, holding approximately 65–70% of the market share. Tier 1 leaders, including Sandvik and Komatsu, leverage proprietary digital ecosystems, extensive service networks, and automation capabilities to maintain dominance. Tier 2 challengers such as Epiroc and J.H. Fletcher focus on niche segments such as hard rock bolting and highly customized engineering solutions, while emerging Chinese manufacturers, including SANY and CRCHI, gain traction in Asia through competitive pricing and improved reliability. Competitive differentiation is achieved through automation, safety innovations, cost efficiency, and integration of digital planning and IoT-enabled monitoring systems.

Key strategic developments highlight technological expansion and regional growth. Sandvik secured a SEK 500 million intelligent fleet order in Southeast Asia, addressing demand for automated bolting solutions. Komatsu integrated iVolve fleet management into its underground mining systems, enhancing real-time analytics capabilities. Epiroc updated its Boltec and PowerROC series with fuel-efficient, automated features to reduce operational costs and skill dependency. Leaders pursue digital ecosystem lock-in, Power-by-the-Hour service models, and local manufacturing in APAC to mitigate supply chain risks and capture high-growth regional markets.

Key Industry Developments:

- In May 2024, Komatsu launched its second-generation Z2 bolter line, featuring the battery-electric ZB21 model. This upgrade introduced zero-emission battery options and a pumpable resin system, reducing bolt costs and enhancing mine sustainability by cutting heat, noise, and fuel consumption in small-class underground operations.

- In September 2024, Komatsu debuted the Z3 series with the ZB31 bolter for medium-sized hard rock applications. The modular platform and advanced resin installation improved bolting cycles, extended equipment life, reduced service costs, and simplified operator training, supporting operational efficiency in expanding underground mines.

- In September 2024, Epiroc showcased the Boltec E10 S ABR at MINExpo 2024. This automation-focused rig featured auto bolt reload, minimizing operator exposure to hazards and increasing installation speed, boosting safety and efficiency in underground tunneling and mining.

Companies Covered in Bolter Miner Market

- Sandvik AB

- Komatsu Ltd.

- Epiroc AB

- Caterpillar Inc.

- J.H. Fletcher & Co.

- MacLean Engineering

- SANY Heavy Industry Co., Ltd

- China Railway Construction Heavy Industry (CRCHI)

- Famur S.A.

- Eickhoff Bergbautechnik GmbH

- RDH-Scharf

- XCMG Group

- China Coal Technology

- Herrenknecht AG

- Gainwell Engineering

Frequently Asked Questions

The global bolter miner market is projected to be valued at US$0.9 billion in 2026 and is expected to reach US$1.9 billion by 2033, driven by rising underground mining activity and stricter safety compliance requirements.

Adoption is increasing due to tightening mine safety regulations, replacement of manual and semi-mechanized systems, and growing emphasis on automation to improve roof control, worker safety, and operational productivity.

The bolter miner market is expected to grow at a CAGR of 10.7% between 2026 and 2033, supported by mine modernization programs and the accelerating electrification of underground equipment.

The strongest growth opportunities are emerging in Asia Pacific, led by large-scale underground coal operations in China, expanding mine capacity in India, and sustained investments in productivity and safety upgrades.

Key players include Sandvik AB, Komatsu Ltd., Epiroc AB, Caterpillar Inc., J.H. Fletcher & Co., MacLean Engineering, SANY Heavy Industry, China Railway Construction Heavy Industry, Famur S.A., Eickhoff Bergbautechnik, RDH-Scharf, XCMG Group, and China Coal Technology.