- Specialty & Fine Chemicals

- Blowing Agents Market

Blowing Agents Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Blowing Agents Market by Product Type (Hydrochlorofluorocarbons (HCFCs), Hydrofluorocarbons (HFCs), Hydrocarbons (HCs), Hydrofluoroolefin (HFO), Others), Foam Type, Application, and Regional Analysis for 2025 - 2032

Blowing Agents Market Size and Trend Analysis

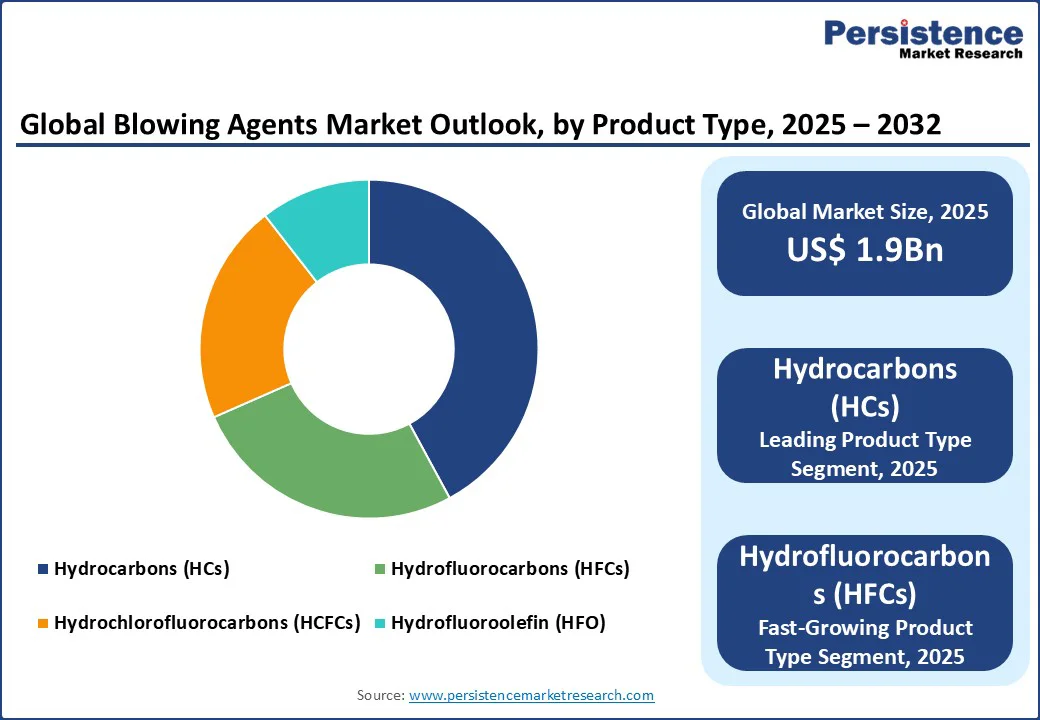

The global blowing agents market size is likely to be valued at US$1.9 Bn in 2025 and reach US$2.8 Bn by 2032, growing at a CAGR of 5.51% during the forecast period from 2025 to 2032, driven by increasing demand for lightweight, energy-efficient, and sustainable materials across industries such as construction, automotive, and packaging. Blowing agents, critical for producing cellular structures in foams, enhance insulation, reduce material density, and improve product durability.

Key Industry Highlights:

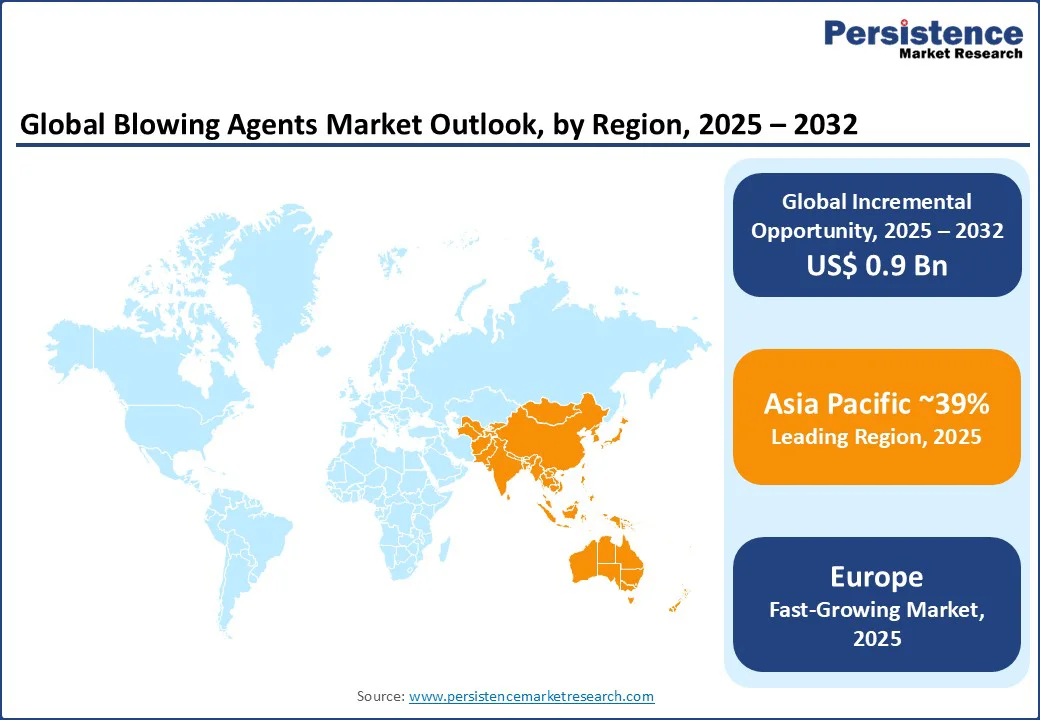

- Leading Region: Asia Pacific is projected to account for a 39% share in 2025, driven by rapid industrialization, urbanization, and construction activities in countries such as China and India.

- Fastest-Growing Region: Europe is the fastest-growing region, driven by stringent environmental regulations and the growing demand for sustainable insulation materials in construction.

- Investment Plans: Arkema announced plans to expand its hydrofluoroalkene (HFO) production capacity in China and the United States to meet the growing demand for low-GWP blowing agents. In 2021, the company committed to investing USD 60 billion to add 15 kilotons per year of HFO capacity in Calvert City, Kentucky, and five kilotons per year in China through a partnership with Aofan.

- Dominant Product Type: Hydrocarbons (HCs), accounting for nearly 40% of the blowing agents market share, due to their low cost, zero ozone depletion potential, and widespread use in polyurethane foams.

- Leading Application: Building and construction, contributing over 35% of market revenue, driven by global infrastructure development and energy efficiency mandates.

| Key Insights | Details |

|---|---|

|

Blowing Agents Market Size (2025E) |

US$ 1.9Bn |

|

Market Value Forecast (2032F) |

US$ 2.8Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.51% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.8% |

Market Dynamics

Driver - Growing Demand for Energy-Efficient Insulation in Construction Fuels Market Expansion

The global blowing agents market is experiencing significant growth due to the rising demand for energy-efficient insulation materials in the construction industry. Blowing agents are critical in producing polyurethane and polystyrene foams, which are widely used for thermal insulation in buildings, reducing energy consumption and greenhouse gas emissions. According to the International Energy Agency, global energy demand for heating and cooling in buildings is expected to rise by 40% by 2040, necessitating advanced insulation solutions.

In the Asia Pacific, China’s 14th Five-Year Plan prioritizes green building initiatives, driving demand for eco-friendly blowing agents, such as HFOs. In the U.S., the Department of Energy reported that energy-efficient insulation could reduce building energy costs by up to 11%. Companies such as Honeywell and Arkema have seen increased sales of low-GWP blowing agents in 2024, reflecting the construction sector’s shift toward sustainability. Government-led energy efficiency mandates and rising urbanization ensure sustained demand, positioning construction as a key driver for market growth through 2032.

Restraint - Stringent Environmental Regulations and High Development Costs

The blowing agents market faces challenges due to stringent environmental regulations and high costs associated with developing eco-friendly alternatives. Regulations such as the Kigali Amendment to the Montreal Protocol mandate the phase-out of high-GWP blowing agents such as HFCs, pushing manufacturers to invest in costly R&D for low-GWP alternatives such as HFOs. In 2023, the cost of transitioning to HFO-based formulations increased production expenses for smaller players, limiting their competitiveness.

Additionally, the complexity of ensuring compatibility with existing foam production processes adds to development costs. Competition from alternative insulation materials, such as mineral wool, also poses a threat in cost-sensitive markets. These regulatory and cost-related challenges, particularly in developing regions with limited infrastructure, restrain overall market growth.

Opportunity - Rising Demand in Renewable Energy and Automotive Sectors

The increasing focus on renewable energy and electric vehicles (EVs) presents significant opportunities for the blowing agents market. Blowing agents are essential in producing lightweight foams for insulation and cushioning in EV battery systems and renewable energy infrastructure, such as wind turbine insulation.

The International Energy Agency projects global renewable energy capacity to increase by 2.7 times by 2030, with wind and solar projects driving demand for polyurethane foams. In the EV sector, blowing agents are used in manufacturing lightweight components to improve fuel efficiency.

Companies such as Solvay and The Chemours Company are innovating with HFO-based blowing agents for automotive applications, aligning with sustainability trends. The EU’s Green Deal and similar global initiatives encourage investments in green technologies, creating opportunities for manufacturers to develop advanced, eco-friendly blowing agents to meet industry needs through 2032.

Category-wise Analysis

By Product Type

- Hydrocarbons dominate the blowing agents market, holding approximately 40% share in 2025, due to their cost-effectiveness, zero ozone depletion potential (ODP), and low global warming potential (GWP). Widely used in polyurethane and polystyrene foam production, HCs are favored in construction and appliance applications for their thermal insulation properties. Companies such as Exxon Mobil and Solvay lead with extensive HC-based portfolios, catering to demand in the Asia Pacific and North America.

- HFOs are the fastest-growing product type, driven by their ultra-low GWP and compliance with stringent environmental regulations. Ideal for high-performance insulation in automotive and construction sectors, HFOs are gaining traction in Europe and North America. Brands such as Honeywell and Arkema are expanding HFO offerings, supported by rising demand for sustainable, energy-efficient solutions in green building projects.

By Foam Type

- Polyurethane foam accounts for over 41% revenue in 2025, driven by its widespread use in construction, automotive, and appliance industries. Its excellent insulation and cushioning properties make it ideal for energy-efficient buildings and lightweight vehicle components. Major players, such as BASF and Dow, supply rigid polyurethane foam blowing agents, meeting global demand for high-performance insulation.

- Polystyrene foam is the fastest-growing foam type, propelled by its increasing use in packaging and construction applications. Its lightweight and durable properties make it suitable for protective packaging and insulation panels. Companies such as Arkema and Huntsman are innovating with polystyrene foam blowing agents, particularly in the Asia Pacific, where urbanization drives demand for cost-effective insulation materials.

By Application

- The building and construction sector accounts for over 35% of market revenue in 2025, driven by global infrastructure projects and energy efficiency mandates. Blowing agents are critical for producing polyurethane and polystyrene foams used in insulation, roofing, and wall panels. Major players, such as The Chemours Company and Solvay, supply high-performance blowing agents for construction projects in China and the U.S.

- The automotive sector is the fastest-growing application, fueled by the rising production of electric vehicles and lightweight components. Blowing agents are used in foam production for interior cushioning and battery insulation, enhancing vehicle efficiency. Companies such as Honeywell and Daikin are innovating with low-GWP blowing agents, supporting growth in Europe and the Asia Pacific, driven by EV adoption.

Regional Insights

Asia Pacific Blowing Agents Market Trends

Asia Pacific is set to dominate in 2025, capturing a substantial 39% share due to its rapid industrialization, urbanization, and booming construction sector, particularly in China and India. China, recognized as a global manufacturing powerhouse, plays a pivotal role in foam production, fueled by government initiatives such as the 14th Five-Year Plan that prioritize energy-efficient buildings and sustainable development. This plan encourages the widespread adoption of advanced insulation materials, such as polyurethane foam, which relies heavily on blowing agents.

Similarly, India’s Smart Cities Mission promotes urban modernization with an emphasis on green infrastructure, driving significant demand for high-performance insulation solutions. Beyond construction, the packaging and automotive sectors in the Asia Pacific contribute notably to blowing agents consumption. Major companies such as Daikin and Arkema are expanding operations and investments in the region to meet growing demand. Additionally, heightened consumer awareness around environmental sustainability, coupled with supportive government policies and incentives for green technologies, reinforces Asia Pacific’s position as a leader through 2032.

Europe Blowing Agents Market Trends

Europe is emerging as the fastest-growing region, largely driven by stringent environmental regulations and an increasing demand for sustainable insulation materials in the construction sector. The European construction industry, valued at €1,683 billion in 2023 according to the European Construction Industry Federation, plays a critical role in this growth. As energy efficiency becomes a top priority, blowing agents are essential for producing high-performance insulation materials that reduce energy consumption and greenhouse gas emissions in buildings.

Germany and France are at the forefront of this demand, propelled by rigorous green building standards and ambitious renewable energy projects such as offshore wind farms. Leading chemical companies such as Solvay and BASF are innovating with hydrofluoroolefin (HFO)-based blowing agents, which have low global warming potential and comply with strict EU regulations such as the European Green Deal. These developments are expected to sustain robust market growth across Europe through 2032, as the region transitions towards a greener and more energy-efficient built environment.

North America Blowing Agents Market Trends

North America stands as the second fastest-growing region, fueled primarily by strong demand from the construction and automotive industries in the U.S. and Canada. In July 2025, the region’s total construction spending reached an estimated $2,139.1 billion, reflecting sustained investments in both commercial and residential projects. Blowing agents play a crucial role in producing high-quality insulation materials that enhance energy efficiency and meet stringent building codes. In Canada, the automotive sector significantly contributes to market growth by driving demand for lightweight foam materials used in electric vehicle (EV) production, aligning with global efforts to reduce vehicle emissions.

Leading companies such as Honeywell and The Chemours Company dominate the market with extensive distribution networks and innovative product offerings. Their focus on low-global-warming-potential blowing agents caters to increasing energy efficiency mandates and growing consumer preference for sustainable materials.

Competitive Landscape

The global blowing agents market is highly competitive and fragmented, with a mix of global and regional players. Leading companies, including The Chemours Company, Honeywell International Inc., Solvay, and Arkema, dominate through extensive product portfolios and global distribution networks. Regional players, such as CHEMSPEC Ltd., focus on localized offerings in the Asia Pacific. Companies are investing in eco-friendly blowing agents, such as HFOs, and advanced manufacturing technologies to enhance market share, driven by demand for sustainable foams in construction and automotive sectors.

Key Industry Developments:

- March 2025: Honeywell introduced Solstice LBA, a next-generation HFO-based blowing agent with ultra-low GWP, designed for polyurethane foam insulation in construction, strengthening its position in Europe and North America. This innovation aligns with Honeywell's broader sustainability efforts, as the company plans to spin off its Advanced Materials business into an independent entity named Solstice Advanced Materials by late 2025 or early 2026

- July 2024: Arkema launched Forane 1233zd, a high-performance HFO blowing agent for automotive and appliance applications, aligning with sustainability trends in the Asia Pacific and Europe. Forane 1233zd boasts a GWP of 1, zero ozone depletion potential (ODP), and is non-flammable, making it compliant with stringent environmental regulations like the EU F-Gas Regulation and the U.S. AIM Act.

Companies Covered in Blowing Agents Market

- The Chemours Company

- Honeywell International Inc.

- Solvay

- Huntsman International LLC

- Akzo Nobel N.V

- BASF SE

- 3M

- Exxon Mobil Corporation

- DAIKIN INDUSTRIES Ltd.

- Arkema

- CHEMSPEC Ltd.

- Dow

- Others

Frequently Asked Questions

The Blowing Agents market is projected to reach US$1.9 Bn in 2025.

Growing demand for energy-efficient insulation in construction and expanding applications in renewable energy and automotive sectors are key market drivers.

The Blowing Agents market is poised to witness a CAGR of 5.51% from 2025 to 2032.

Rising demand in the renewable energy and electric vehicle sectors is the key market opportunity.

The Chemours Company, Honeywell International Inc., Solvay, and Arkema are key market players.