- Medical Devices

- Global Bariatric Surgery Devices Market

Global Bariatric Surgery Devices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Bariatric Surgery Devices Market by Product (Minimally Invasive Surgical Devices and Non-invasive Surgical Devices), by Procedure (Sleeve Gastrectomy, Gastric Bypass, Revision Bariatric Surgery, Non-invasive Bariatric Surgery, Adjustable Gastric Banding, and Others), by End User (Hospitals, Specialty Clinics, and Ambulatory Surgery Centers), and Regional Analysis from 2026 to 2033.

Bariatric Surgery Devices Market Size and Trend Analysis

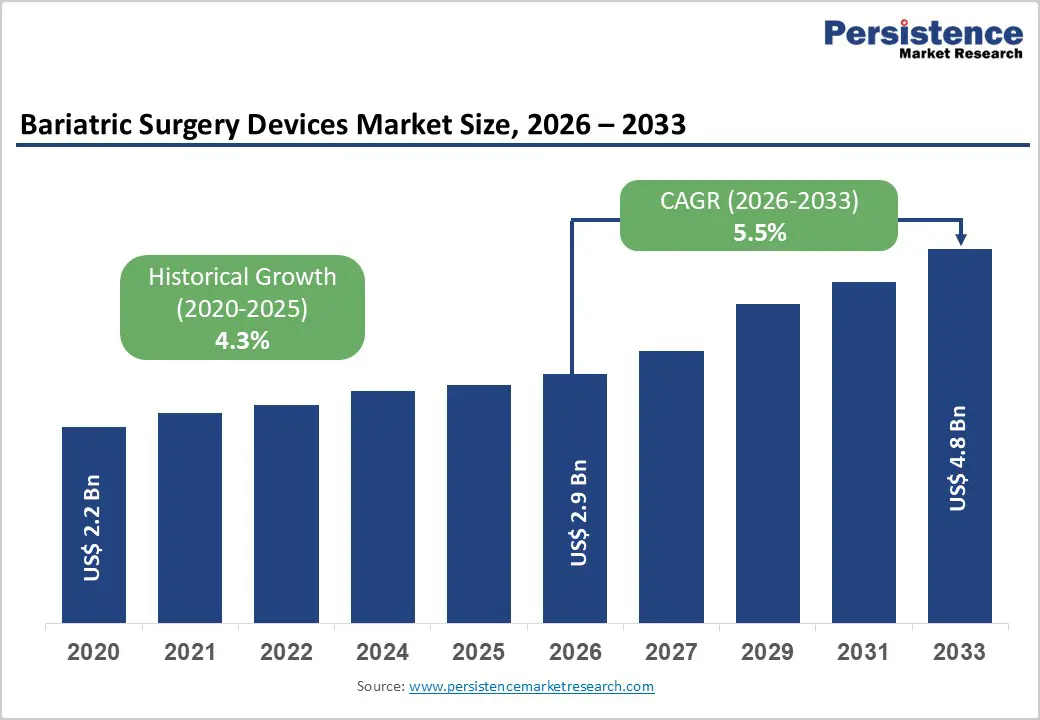

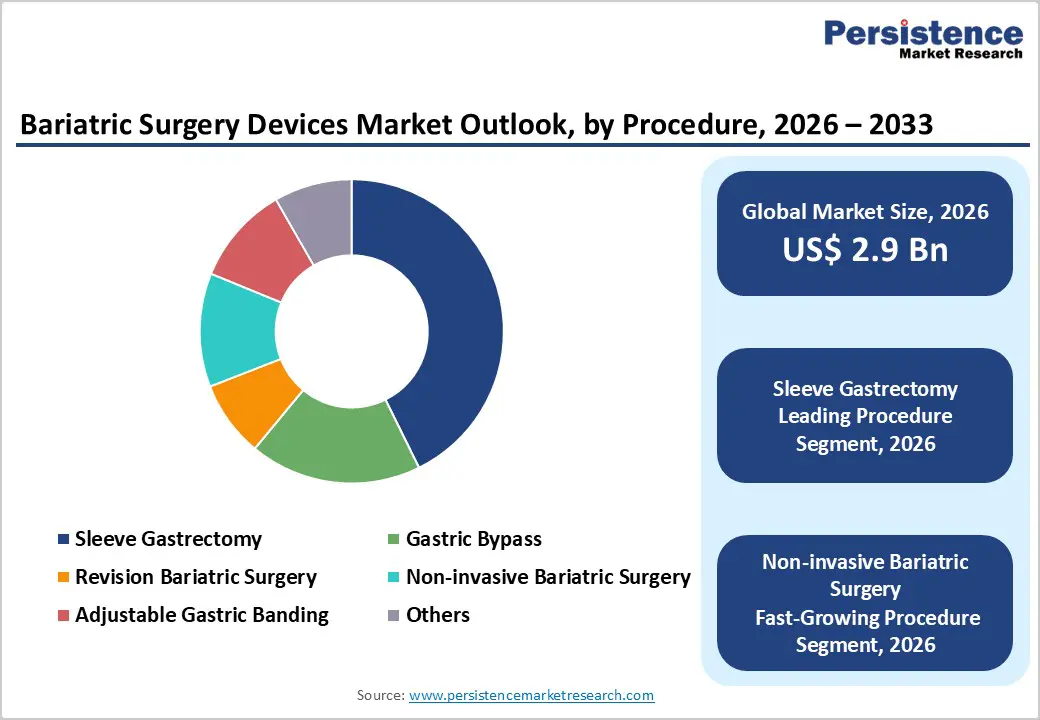

The global bariatric surgery devices market size is estimated to grow from US$ 2.9 Bn in 2026 to US$ 4.8 Bn by 2033. The market is projected to record a CAGR of 5.5% during the forecast period from 2026 to 2033.

Global demand for bariatric surgery devices is increasing steadily, driven by the rising prevalence of obesity, metabolic disorders, and associated comorbidities such as type 2 diabetes, hypertension, and cardiovascular disease. Growing awareness of obesity as a chronic, life-impacting condition, along with improvements in diagnostic protocols, patient screening, and obesity management programs, is supporting sustained market growth. Increasing adoption of advanced minimally invasive surgical devices, robotic-assisted platforms, stapling and vessel-sealing tools, and endoscopic weight-loss solutions is further accelerating demand. Higher procedure volumes across hospitals, specialty clinics, and ambulatory surgery centers, rising healthcare expenditure, and expanding access to bariatric-focused care are strengthening market expansion. Continuous innovation in device design, surgical precision, digital integration, and patient-centric postoperative management solutions is improving procedural outcomes, reducing complications, and enhancing long-term patient adherence. In addition, increasing focus on non-invasive and endoscopic treatment options, customized surgical planning, and integration of telemedicine and remote monitoring platforms is further propelling the global bariatric surgery devices market.

Key Industry Highlights

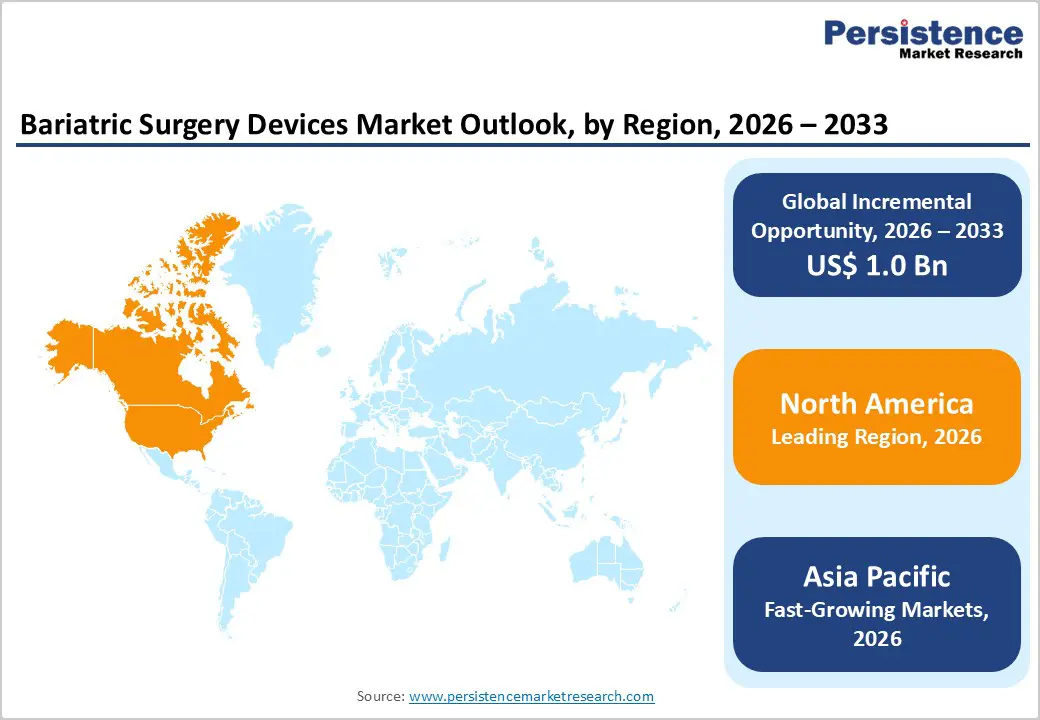

- Leading Region: : North America holds the largest share at 47.9%, supported by advanced healthcare infrastructure, high procedure volumes, early adoption of minimally invasive and robotic bariatric technologies, and the strong presence of leading manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a large untreated obesity population, increasing awareness of surgical interventions, rising screening programs, improving healthcare infrastructure, and growing investments in specialty bariatric centers.

- Leading Product Segment: Minimally invasive surgical devices dominate the market due to their broad applicability across bariatric procedures, including sleeve gastrectomy, gastric bypass, and revision surgeries.

- Fastest-Growing Product Segment: Non-invasive surgical devices are expanding rapidly as clinicians increasingly adopt endoscopic and intragastric balloon solutions for patients seeking less invasive treatment alternatives.

- Leading End User Segment: Hospitals remain the top end user, driven by high volumes of complex bariatric procedures, specialized surgical infrastructure, and access to experienced surgical teams.

- Fastest-Growing End User Segment: Specialty clinics are scaling quickly as demand rises for focused bariatric evaluation, device-based procedures, outpatient interventions, and post-operative follow-up care.

| Global Market Attributes | Key Insights |

|---|---|

| Bariatric Surgery Devices Market Size (2026E) | US$ 2.9 Bn |

| Market Value Forecast (2033F) | US$ 4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5 % |

Market Dynamics

Driver – Rising Obesity Prevalence and Advancements in Minimally Invasive and Robotic Bariatric Surgery Driving Market Growth

The global bariatric surgery devices market is witnessing sustained growth, primarily driven by the escalating prevalence of obesity and associated comorbidities such as type 2 diabetes, cardiovascular disease, and metabolic syndrome across both developed and developing regions. According to the World Health Organization, over 650 million adults globally were classified as obese in 2023, with projections indicating continued growth through 2030. Increasing awareness of obesity-related health risks and the proven clinical effectiveness of bariatric procedures in long-term weight reduction and metabolic improvement are contributing to higher patient demand. Minimally invasive and robotic-assisted surgical technologies, including advanced stapling systems, vessel-sealing devices, suturing instruments, and laparoscopic platforms, are facilitating safer, faster, and more precise bariatric procedures.

Technological innovations, such as AI-assisted surgical planning, enhanced 3D visualization, and energy-efficient vessel-sealing tools, are improving procedural outcomes, reducing complication rates, and increasing patient satisfaction. Moreover, growing adoption of endoscopic and non-invasive weight-loss devices, including intragastric balloons and endoluminal suturing systems, is expanding treatment accessibility to patients seeking less invasive alternatives. The combined effect of rising obesity prevalence, patient preference for minimally invasive interventions, and continuous device innovation is driving significant growth in the global bariatric surgery devices market.

Restraints – High Procedural Costs, Limited Specialist Availability, and Surgical Complexity Constraining Market Adoption

the bariatric surgery devices market faces several structural and economic challenges that limit broader adoption. One of the key restraints is the high cost associated with advanced surgical interventions, encompassing device acquisition, robotic or laparoscopic equipment, preoperative assessments, hospital stays, and postoperative follow-up care. In many regions, particularly in low- and middle-income countries, limited insurance coverage or inconsistent reimbursement policies increases out-of-pocket expenditure, deterring potential patients. Access to trained bariatric surgeons, anesthesiologists, and multidisciplinary care teams remains unevenly distributed, with a concentration in urban tertiary-care centers, leaving rural and semi-urban populations underserved.

The technical complexity of procedures such as sleeve gastrectomy, gastric bypass, or revision surgeries necessitates specialized surgical expertise, precise intraoperative management, and structured post-operative monitoring, creating barriers for healthcare facilities lacking adequate infrastructure. Additionally, variability in patient response to surgical or non-invasive interventions, along with potential device-related complications or intolerance, can reduce clinician confidence and patient willingness. These economic, clinical, and logistical factors collectively slow procedure adoption, limit market penetration in cost-sensitive regions, and pose challenges to scaling bariatric surgical solutions globally.

Opportunity – Emerging Market Expansion and Integration of Digital and Personalized Treatment Technologies

The global bariatric surgery devices market offers substantial growth opportunities, particularly in emerging regions such as Asia Pacific, Latin America, the Middle East, and Africa, where obesity prevalence is rapidly increasing but access to advanced surgical solutions remains limited. Expanding healthcare infrastructure, rising patient awareness, government health initiatives, and gradual expansion of insurance coverage are improving access to bariatric interventions in these high-potential markets. In parallel, technological innovation is transforming the delivery of bariatric care. The development of next-generation robotic platforms, advanced laparoscopic tools, endoscopic weight-loss devices, and energy-efficient stapling and vessel-sealing systems is enabling safer, more precise, and personalized procedures.

Digital health integration, including telemedicine for preoperative consultation, remote post-operative monitoring, patient adherence tracking, and AI-driven surgical planning, is enhancing procedural efficiency, reducing hospital stays, and increasing patient satisfaction. Manufacturers focusing on cost-effective, user-friendly, and patient-centric device designs are further improving accessibility in underserved regions. Collectively, these trends represent a significant opportunity to expand market reach, enhance treatment outcomes, and create new revenue streams in both developed and emerging markets, driving long-term growth for the bariatric surgery devices industry.

Category-wise Analysis

By Product, Minimally Invasive Surgical Devices Lead Adoption Owing to Broad Clinical Use and Patient Preference

The minimally invasive surgical devices segment is projected to maintain its leading position in the global bariatric surgery devices market in 2026, accounting for a revenue share of 72.1%. This dominance is largely driven by the wide clinical applicability of laparoscopic and robotic instruments, including stapling devices, vessel sealing tools, and suturing systems, which are preferred for most bariatric procedures due to their reduced invasiveness, faster recovery, and lower complication rates. Non-invasive treatment options, such as endoscopic intragastric balloons, are gaining traction among patients seeking weight-loss interventions without surgery. Continuous technological enhancements, including improved stapling accuracy, advanced suturing devices, and energy-efficient vessel-sealing systems, have enhanced procedural safety and efficacy. Additionally, growing patient awareness, expanding access through hospitals and specialty clinics, and favorable reimbursement policies in developed markets, coupled with increasing affordability in emerging regions, are further driving adoption. These factors collectively reinforce the leadership of minimally invasive devices within the overall bariatric surgery devices landscape.

By Procedure, Sleeve Gastrectomy Retains Dominance Due to High Prevalence and Broad Eligibility

The sleeve gastrectomy segment is expected to dominate the global bariatric surgery devices market in 2026, capturing a revenue share of 42.7%. This leadership stems from the procedure’s broad clinical eligibility and high adoption among patients with obesity or overweight conditions requiring surgical intervention. Sleeve gastrectomy is increasingly preferred due to its relatively lower complication rates, effectiveness in substantial weight reduction, and suitability for a wide range of age groups and comorbid conditions. Growing patient awareness of obesity-related health risks, improved pre- and post-operative care protocols, and enhanced surgical precision through robotic and laparoscopic assistance further reinforce its market position. In addition, increasing insurance coverage and reimbursement support, alongside the expansion of specialized bariatric surgery centers, are facilitating greater patient access. Continuous innovation in surgical instruments, stapling technologies, and post-operative management solutions ensures optimal outcomes, sustaining sleeve gastrectomy’s leadership in global bariatric surgery procedures.

By End User, Hospitals Maintain Leading Role Due to Specialized Infrastructure and Surgical Expertise

Hospitals are projected to account for the largest share of the global bariatric surgery devices market in 2026, representing 47.3% of total revenue. This dominance is driven by the concentration of advanced surgical, diagnostic, and post-operative care facilities in hospital settings, which are essential for complex bariatric procedures such as sleeve gastrectomy, gastric bypass, and revision surgeries. Hospitals offer specialized operating rooms, experienced surgical teams, advanced laparoscopic and robotic systems, and structured rehabilitation programs, ensuring high-quality patient care. Complex cases, including patients with comorbidities or those requiring revision surgery, are predominantly managed in hospitals. Centralized procurement systems, long-term partnerships with device manufacturers, and access to premium bariatric devices also contribute to higher procedural volumes and revenue. Furthermore, hospitals are increasingly adopting digitally integrated surgical platforms, data-driven patient monitoring systems, and comprehensive pre- and post-operative management services, which enhance patient outcomes and procedural efficiency, reinforcing their leading position among end users in the bariatric surgery devices market.

Region-wise Insights

North America Bariatric Surgery Devices Market Trends

North America is expected to dominate the global bariatric surgery devices market in 2026, with a value share of 47.9%, led primarily by the United States. The region benefits from a mature healthcare ecosystem, high patient awareness of obesity and associated comorbidities, and strong adoption of minimally invasive and robotic bariatric procedures. Favorable reimbursement policies under both public and private insurance programs enhance patient access to advanced devices, including staplers, vessel-sealing systems, and endoscopic solutions. Early adoption of technologically advanced surgical platforms, such as robotic-assisted sleeve gastrectomy systems and digitally integrated laparoscopic tools, further drives market growth.

A strong presence of leading global manufacturers, robust research and development initiatives, and comprehensive surgeon training programs strengthen procedural quality and patient outcomes. The increasing use of telehealth and remote patient monitoring platforms supports pre- and post-operative care, improving adherence and long-term effectiveness. In addition, high investment in outpatient bariatric centers and ambulatory surgery units is facilitating treatment scalability, reinforcing North America’s leadership position in the global bariatric surgery devices landscape.

Europe Bariatric Surgery Devices Market Trends

The Europe bariatric surgery devices market is projected to witness steady growth in 2026, supported by a rising prevalence of obesity and related comorbidities, as well as an aging population. Countries such as Germany, the U.K., France, Italy, and the Nordic nations demonstrate consistent procedural volumes due to well-established healthcare systems, structured referral pathways, and specialized bariatric surgery programs. Universal healthcare coverage and reimbursement for minimally invasive and endoscopic bariatric interventions improve patient accessibility across multiple markets. Growing awareness of obesity-related health risks and the importance of early intervention is driving increased demand for sleeve gastrectomy, gastric bypass, and non-invasive procedures.

Technological adoption, including robotic surgical platforms, advanced stapling systems, and high-precision vessel-sealing devices, enhances procedural safety and outcomes. Strong collaboration among hospitals, academic institutions, and device manufacturers is fostering clinical innovation. The integration of digital surgical planning, standardized treatment protocols, and post-operative monitoring systems is further improving efficiency, patient adherence, and long-term success rates across the European bariatric surgery devices market.

Asia Pacific Bariatric Surgery Devices Market Trends

The Asia Pacific bariatric surgery devices market is expected to register a comparatively higher CAGR of approximately 7.4% between 2026 and 2033, fueled by expanding healthcare infrastructure and a rapidly increasing patient population. Rising obesity prevalence, growing awareness of surgical weight-loss options, and limited early intervention in many regions are driving demand in China, India, Japan, South Korea, and Southeast Asia. The proliferation of private hospitals and specialized bariatric centers, coupled with improvements in laparoscopic and robotic surgical capabilities, is accelerating adoption. Medical tourism is also contributing to increased procedural volumes, particularly in India and Southeast Asia, where cost-competitive yet high-quality treatments attract international patients.

Government-supported health initiatives, gradual expansion of insurance coverage, and local manufacturing of bariatric devices are improving affordability and accessibility. Global manufacturers are actively investing in clinician training, distribution networks, and digitally integrated surgical platforms, further strengthening long-term growth. Enhanced patient education, growing urban middle-class populations, and increasing focus on minimally invasive and non-invasive bariatric procedures collectively support sustained market expansion in the Asia Pacific region.

Market Competitive Landscape

The global bariatric surgery devices market is highly competitive, with key players including Medtronic, Johnson & Johnson, Boston Scientific Corporation, Intuitive Surgical, and B.Braun SE. These companies benefit from strong global distribution networks, established brand presence, and continuous innovation in minimally invasive and robotic surgical technologies.

Growing demand for effective obesity management and improved patient outcomes is driving focus on advanced stapling, suturing, vessel-sealing devices, and non-invasive bariatric solutions such as intragastric balloons and endoscopic systems. Strategic priorities include clinician training, expansion in emerging markets, and strengthening partnerships with hospitals, specialty clinics, and ambulatory surgery centers to maintain competitive advantage and support long-term market growth.

Key Industry Developments:

- In January 2026, innovators at VCU developed a device designed to replicate real blood flow in surgical training simulations. The recent invention disclosure highlights a specialized pump that has the potential to enhance training for physicians, military medics, and medical educators, ultimately improving patient outcomes by providing more realistic and effective surgical practice scenarios.

- In February 2024, BariaTek successfully implanted its first device designed to replicate the effects of weight-loss surgery. The BariTon implant is engineered to mimic the outcomes of sleeve gastrectomy and gastric bypass procedures, offering a less invasive alternative for patients seeking effective obesity management.

Companies Covered in Global Bariatric Surgery Devices Market

- Medtronic

- Johnson & Johnson

- Boston Scientific Corporation

- Intuitive Surgical

- B. Braun SE

- Asensus Surgical

- AbbVie Inc.

- ReShape Lifesciences Inc.

- Entero Medica, Inc.

- CONMED Corporation

- Olympus Corporation

- Allurion Technologies

- Spatz FGIA

- Apollo Endosurgery Inc

- Others

Frequently Asked Questions

The global bariatric surgery devices market is projected to be valued at US$ 2.9 Bn in 2026.

Rising obesity prevalence, increasing demand for minimally invasive procedures, growing adoption of advanced surgical devices, supportive healthcare infrastructure expansion, and technological advancements in robotic and laparoscopic systems.

The global bariatric surgery devices market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Expansion of non-invasive and endoscopic bariatric treatment technologies, rising outpatient and ambulatory surgery center adoption, and emerging markets with increasing healthcare accessibility.

Medtronic, Johnson & Johnson, Boston Scientific Corporation, Intuitive Surgical, and B. Braun SE are some of the key players in the bariatric surgery devices market.