- Medical Devices

- Atherectomy and Thrombectomy Devices Market

Atherectomy and Thrombectomy Devices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Atherectomy and Thrombectomy Devices Market by Product (Atherectomy Devices and Thrombectomy Devices), by Application (Peripheral Artery Disease (PAD), Coronary Artery Disease (CAD), and Neurovascular Conditions), by End User (Hospitals, Specialty Clinics, Ambulatory Surgical Center, and Others), and Regional Analysis from 2026 to 2033.

Atherectomy and Thrombectomy Devices Market Share and Trend Analysis

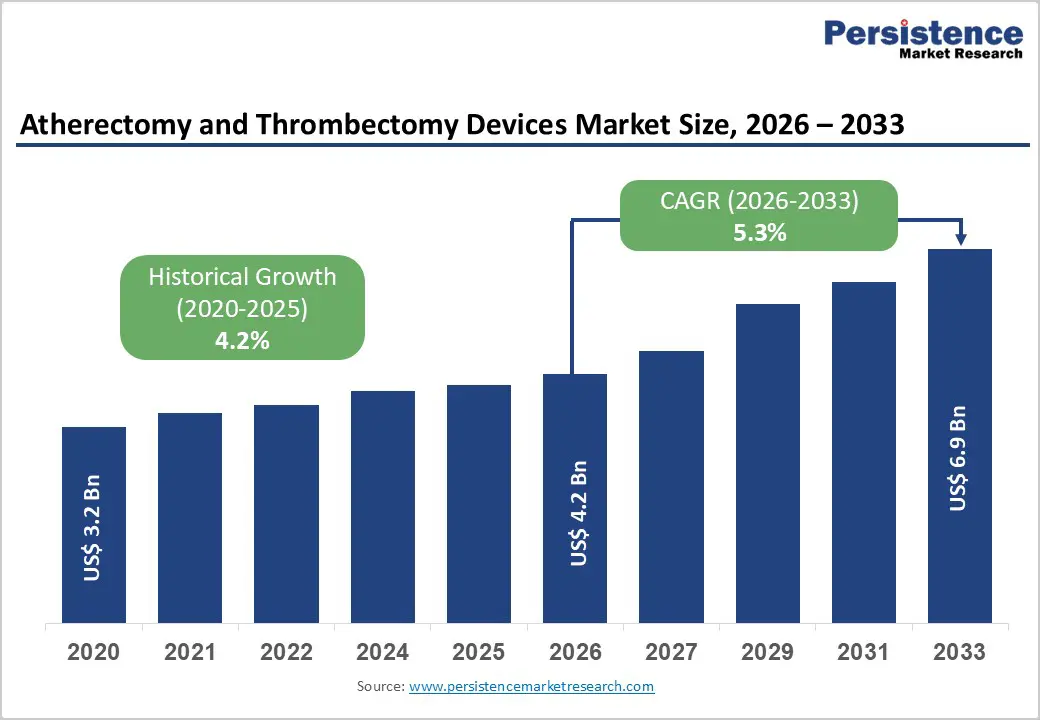

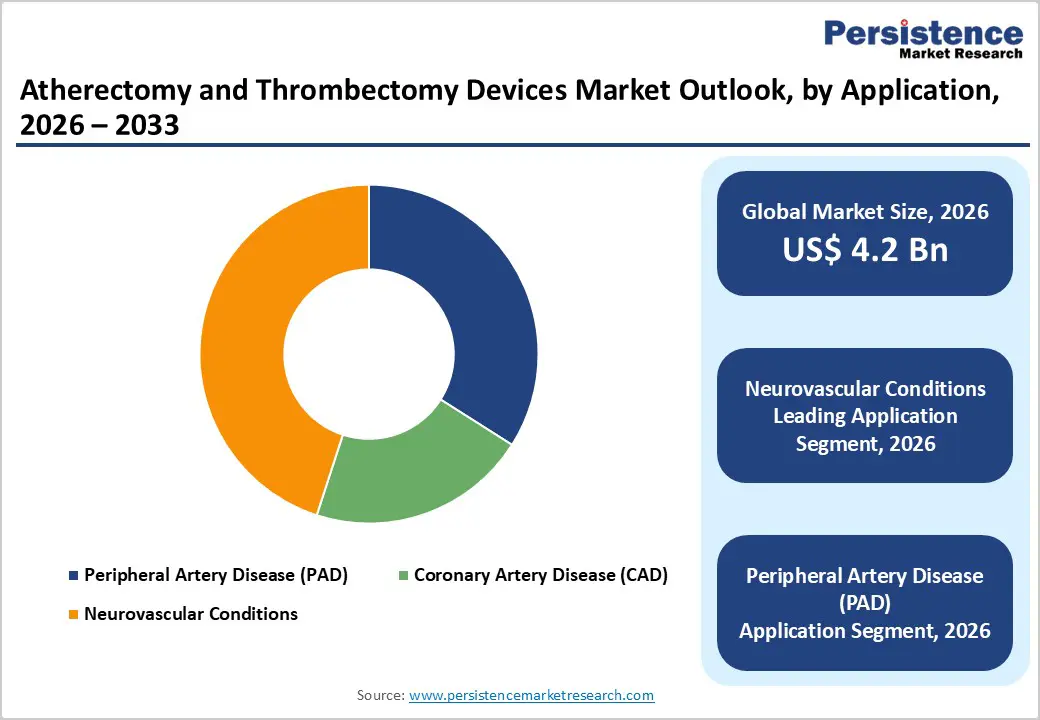

The global atherectomy and thrombectomy devices market size is estimated to grow from US$ 4.2 Bn in 2026 to US$ 6.9 Bn by 2033. The market is projected to record a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for atherectomy and thrombectomy devices is rising steadily, driven by the increasing prevalence of cardiovascular and neurovascular disorders such as peripheral artery disease (PAD), coronary artery disease (CAD), ischemic stroke, and venous thromboembolism. Aging populations, growing incidence of lifestyle-related risk factors including diabetes, obesity, hypertension, and smoking, and higher rates of vascular interventions are expanding the target patient pool requiring endovascular treatment. Atherectomy and thrombectomy devices are widely utilized across hospitals, comprehensive stroke centers, specialty cardiovascular clinics, and ambulatory surgical centers to restore blood flow, remove plaque or thrombus, and manage acute and chronic vascular conditions through minimally invasive procedures. Rising preference for catheter-based interventions that offer reduced procedural risk, shorter hospital stays, and faster recovery is accelerating adoption. Improved awareness of early diagnosis, expansion of stroke care pathways, and increased access to advanced imaging and interventional facilities further support demand. Continuous technological advancements including enhanced clot-retrieval mechanisms, improved catheter trackability, aspiration efficiency, and single-use device designs are improving safety, procedural success, and clinical outcomes. Additionally, strengthening healthcare infrastructure in emerging markets and rising investments in cardiovascular and neurovascular care are reinforcing long-term global demand for atherectomy and thrombectomy devices.

Key Industry Highlights

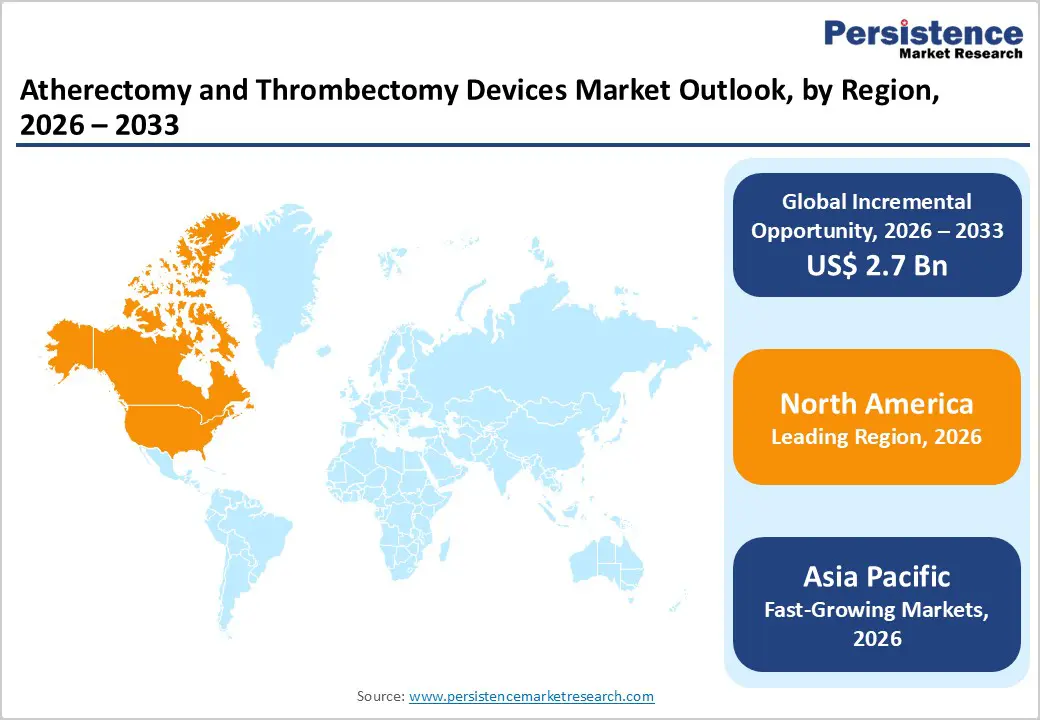

- Leading Region: North America holds the largest share at 47.3%, supported by advanced interventional infrastructure, high prevalence of cardiovascular and neurovascular diseases, strong hospital procurement systems, favorable reimbursement, and early adoption of innovative endovascular devices.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to improving healthcare access, rising burden of stroke and peripheral vascular diseases, aging populations, rapid expansion of private hospitals, and growing medical tourism.

- Leading Application Segment: Neurovascular conditions dominate the market due to high global incidence of ischemic stroke, urgent treatment requirements, strong clinical evidence supporting mechanical thrombectomy, and high procedural volumes in comprehensive stroke centers.

- Fastest-Growing Application Segment: Peripheral artery disease (PAD) is growing rapidly as minimally invasive endovascular interventions gain preference and treatment volumes increase in outpatient and ambulatory care settings.

- Leading End User Segment: Hospitals remain the top segment, driven by high patient volumes, availability of specialized interventional cardiologists and neuro-interventionists, and management of complex and acute vascular cases.

- Fastest-Growing End User Segment: Ambulatory surgical centers are scaling quickly as selected peripheral vascular interventions shift toward outpatient care, supported by shorter recovery times, lower costs, and improving procedural capabilities.

| Global Market Attributes | Key Insights |

|---|---|

| Atherectomy and Thrombectomy Devices Market Size (2026E) | US$ 4.2 Bn |

| Market Value Forecast (2033F) | US$ 6.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Driver – Rising Burden of Cardiovascular and Neurovascular Diseases and Shift Toward Catheter-Based Interventions

Market growth is strongly driven by the rising global incidence of cardiovascular and neurovascular conditions, including peripheral artery disease (PAD), coronary artery disease (CAD), ischemic stroke, and venous thromboembolism. Aging populations and increasing prevalence of lifestyle-related risk factors such as diabetes, obesity, hypertension, and smoking are significantly expanding the patient base requiring endovascular intervention. Atherectomy and thrombectomy procedures are increasingly preferred due to their minimally invasive nature, ability to rapidly restore blood flow, and reduced recovery times compared to open surgical alternatives.

Advancements in catheter design, imaging guidance, and device precision have improved procedural safety and clinical outcomes, supporting broader physician adoption. Mechanical thrombectomy has become a standard of care for large-vessel occlusion stroke, further accelerating demand.

Rising awareness of early diagnosis and timely intervention is increasing procedure volumes across both developed and emerging markets. Additionally, expanding availability of interventional cardiology and neuro-interventional services in hospitals and specialty centers is strengthening utilization. Favorable clinical evidence, guideline support, and growing investment in stroke and vascular care infrastructure continue to reinforce sustained market momentum.

Restraints – High Device Costs, Procedural Risks, and Infrastructure Limitations in Resource-Constrained Settings

The adoption is constrained by several clinical and economic challenges. Atherectomy and thrombectomy devices are often associated with high upfront costs, which can limit accessibility in price-sensitive healthcare systems. Advanced procedures require specialized catheterization laboratories, imaging equipment, and highly trained interventional specialists, restricting use in smaller hospitals and rural settings. In developing regions, limited availability of skilled clinicians and uneven distribution of vascular care infrastructure remain key barriers.

Procedural risks such as vessel perforation, distal embolization, bleeding, and contrast-related complications can impact physician and patient confidence, particularly in complex or repeat interventions. Outcomes may vary depending on operator experience, patient anatomy, and disease severity, contributing to cautious adoption in certain care settings. Reimbursement variability across countries and procedures can further influence utilization rates, especially for advanced atherectomy technologies.

Additionally, alternative treatment options such as pharmacological thrombolysis, balloon angioplasty, or surgical bypass may reduce reliance on device-based intervention in selected patient groups. Regulatory approval processes, clinical evidence requirements, and compliance with stringent quality standards can also increase time-to-market and cost burdens for manufacturers.

Opportunity – Expansion of Stroke Care Networks, Technological Innovation, and Rapid Growth in Emerging Economies

Significant growth opportunities are emerging from the global expansion of organized stroke care networks and increasing investment in rapid-response neurovascular treatment pathways. As mechanical thrombectomy adoption continues to expand beyond tertiary centers into regional hospitals, demand for advanced, easy-to-use devices is expected to rise. Ongoing innovation in aspiration systems, clot-retrieval mechanisms, and plaque-modification technologies is improving procedural efficiency and expanding treatable patient populations.

Emerging markets across Asia Pacific, Latin America, and the Middle East present substantial untapped potential due to improving healthcare infrastructure, rising awareness of cardiovascular disease, and increasing access to diagnostic imaging. Expansion of private hospitals, multispecialty cardiac centers, and ambulatory intervention facilities is accelerating market penetration. Growing focus on minimally invasive care, reduced hospital stays, and cost-effective treatment pathways aligns well with catheter-based solutions.

Strategic partnerships between device manufacturers, hospitals, and training institutions are strengthening clinical expertise and standardizing procedural adoption. Additionally, development of next-generation devices optimized for complex anatomy and faster intervention is expected to unlock new application areas, supporting long-term market expansion.

Category-wise Analysis

By Product, Thrombectomy Devices Lead Due to Single-Use Design, Rapid Clot Removal, and Lower Infection Risk

Thrombectomy devices are projected to dominate the global atherectomy and thrombectomy devices market in 2026, accounting for a revenue share of 58.0%. Their leadership is driven by increasing adoption of single-use, disposable thrombectomy systems, which significantly reduce infection risk and eliminate cross-contamination concerns associated with reusable devices. These devices enable rapid thrombus extraction, shortening procedure times and improving clinical outcomes, particularly in time-sensitive conditions such as acute ischemic stroke and venous thromboembolism.

Mechanical and aspiration thrombectomy systems are widely preferred across hospitals and ambulatory settings due to simplified workflows, reduced need for reprocessing, and compatibility with minimally invasive catheter-based interventions. Growing emphasis on infection control protocols, patient safety, and operational efficiency further supports adoption. Additionally, technological advancements improving trackability, clot engagement efficiency, and vessel safety are reinforcing clinician confidence. As procedural volumes rise globally, thrombectomy devices are expected to maintain their dominant position throughout the forecast period.

By Application, Neurovascular Conditions Lead Due to High Stroke Incidence and Urgent Intervention Requirements

The neurovascular conditions segment is expected to dominate the global atherectomy and thrombectomy devices market in 2026, capturing a revenue share of 45.0%. This dominance is primarily driven by the high global burden of ischemic stroke and the critical need for rapid mechanical intervention to restore cerebral blood flow. Mechanical thrombectomy has become a standard of care for large vessel occlusion strokes, supported by strong clinical evidence and guideline endorsements.

Rising awareness of stroke symptoms, improved emergency response systems, and expanding availability of comprehensive stroke centers are increasing procedural volumes worldwide. Advancements in neurovascular imaging and catheter technology have improved procedural success rates, encouraging broader adoption. Additionally, aging populations and higher prevalence of cardiovascular risk factors such as hypertension, diabetes, and atrial fibrillation continue to elevate stroke incidence. As neuro-interventional capabilities expand globally, this application segment is expected to retain its leading share.

By End User, Hospitals Lead Due to High Procedural Complexity and Availability of Advanced Interventional Infrastructure

Hospitals are projected to dominate the global atherectomy and thrombectomy devices market in 2026, accounting for a revenue share of 72.0%. This dominance is attributed to their ability to manage high-acuity and complex vascular cases, including acute stroke, severe peripheral arterial disease, and coronary interventions. Hospitals are equipped with advanced catheterization laboratories, neuro-interventional suites, and multidisciplinary clinical teams essential for atherectomy and thrombectomy procedures.

High patient inflow, 24/7 emergency care capabilities, and adherence to standardized treatment protocols further support sustained device utilization. Hospitals also serve as primary centers for training, clinical trials, and adoption of newly approved technologies. While ambulatory surgical centers and specialty clinics are gradually expanding their role in elective peripheral interventions, hospitals continue to lead due to their capacity to handle critical cases, post-procedural monitoring, and complication management.

Region-wise Insights

North America Atherectomy and Thrombectomy Devices Market Trends

North America is expected to dominate the global atherectomy and thrombectomy devices market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from a highly developed cardiovascular and neurovascular care ecosystem, characterized by widespread access to advanced interventional facilities and skilled specialists. High prevalence of ischemic stroke, peripheral artery disease, and coronary artery disease continues to drive strong procedural demand. Early adoption of innovative thrombectomy and atherectomy technologies, supported by robust clinical evidence and regulatory approvals, reinforces market leadership.

Favorable reimbursement policies for endovascular procedures encourage consistent utilization across hospital systems. Additionally, strong emphasis on patient safety, infection prevention, and single-use device adoption aligns well with advanced thrombectomy platforms. Presence of leading manufacturers, continuous product innovation, and large-scale hospital procurement networks further strengthen the market. Growing investment in stroke centers and emergency response infrastructure ensures sustained regional dominance.

Europe Atherectomy and Thrombectomy Devices Market Trends

The Europe atherectomy and thrombectomy devices market is expected to grow steadily, supported by strong regulatory frameworks, standardized clinical guidelines, and broad access to vascular and neuro-interventional care across countries such as Germany, the U.K., France, Italy, and Spain. An aging population, combined with rising incidence of cardiovascular and cerebrovascular diseases, is driving demand for minimally invasive endovascular procedures.

European healthcare systems emphasize early diagnosis and evidence-based treatment, supporting adoption of atherectomy and thrombectomy devices in both acute and elective settings. Strict compliance with medical device safety, material quality, and performance standards favors high-quality, clinically validated products. Expansion of specialized stroke units and vascular centers is improving procedural accessibility. Additionally, increasing outpatient intervention capacity and cross-border healthcare within the EU are contributing to rising treatment volumes. These factors collectively support stable, long-term market growth across the region.

Asia Pacific Atherectomy and Thrombectomy Devices Market Trends

The Asia Pacific atherectomy and thrombectomy devices market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by improving healthcare infrastructure, rising disease burden, and expanding access to advanced medical technologies. Countries such as China, India, Japan, South Korea, and Australia are witnessing increasing diagnosis of stroke and peripheral vascular diseases due to better awareness and improved imaging capabilities.

Rapid urbanization, aging populations, and growing prevalence of lifestyle-related risk factors are accelerating procedural demand. Expansion of private hospitals, specialty cardiovascular centers, and neuro-interventional units is enhancing market penetration.

Entry of regional manufacturers and increasing affordability of thrombectomy devices are improving accessibility in cost-sensitive markets. Government initiatives to strengthen stroke care networks and rising medical tourism further support growth. As clinical capacity and interventional expertise expand, Asia Pacific is expected to emerge as the fastest-growing regional market.

Market Competitive Landscape

The global atherectomy and thrombectomy devices market is highly competitive, with strong participation from companies such as Medtronic, Boston Scientific Corporation, Philips Healthcare, Abbott, and Argon Medical Devices. These players leverage extensive global distribution networks, strong brand recognition, and diversified endovascular and interventional cardiovascular product portfolios to address the growing demand for safe, effective, and minimally invasive solutions for arterial plaque and thrombus removal.

Their offerings emphasize device reliability, procedural precision, rapid clot or plaque removal, physician ease of use, and compatibility across multiple clinical applications, including peripheral artery disease (PAD), coronary artery disease (CAD), acute ischemic stroke, and venous thromboembolic interventions. Continuous technological innovation, regulatory approvals, clinical evidence generation, adherence to sterilization protocols, and compliance with international quality and manufacturing standards remain critical for maintaining competitive positioning in the global atherectomy and thrombectomy devices market.

Key Industry Developments:

- In December 2025, Medtronic announced the first commercial deployment of its Liberant™ thrombectomy system, designed for the removal of fresh, soft emboli and thrombi from peripheral arterial and venous vasculature. The company highlighted that Liberant broadens its treatment portfolio for peripheral arterial and venous diseases by adding a mechanical aspiration thrombectomy solution.

- In May 2025, BD (Becton, Dickinson and Company), a global medical technology leader, announced its plan to launch a patient data registry for the Rotarex™ Atherectomy System aimed at evaluating real-world clinical outcomes in patients with peripheral artery disease (PAD). The registry is expected to support evidence-based adoption, inform clinical best practices, and strengthen long-term post-market performance validation of the system.

- In March 2025, Inari Medical, now part of Stryker, announced the launch of the Artix Thrombectomy System, a purpose-built solution for the peripheral arterial system that combines aspiration and mechanical thrombectomy to enhance procedural control, versatility, and performance in arterial clot removal.

- In April 2022, Cardiovascular Systems Inc. (CSI) partnered with Innova Vascular Inc. to develop and commercialize thrombectomy devices for peripheral vascular diseases, including DVT and PE, complementing CSI’s cardiovascular technology portfolio.

Companies Covered in Atherectomy and Thrombectomy Devices Market

- Medtronic

- Boston Scientific Corporation

- Philips Healthcare

- Abbott

- Argon Medical Devices.

- BD

- Teleflex Incorporated.

- Inari Medical, Inc.

- Terumo Corporation

- Vascumed (Pty) Ltd

- plusmedica.de

- Rex Medical

- Others

Frequently Asked Questions

The global atherectomy and thrombectomy devices market is projected to be valued at US$ 4.2 Bn in 2026.

The market is driven by the rising prevalence of cardiovascular diseases (PAD, CAD, and stroke) and the growing adoption of minimally invasive interventional procedures with advanced device technologies.

The global atherectomy and thrombectomy devices market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Key opportunities lie in technological innovations such as AI/robotics, enhanced imaging, and next-generation device design to improve procedural precision and expand clinical applications.

Medtronic, Boston Scientific Corporation, Philips Healthcare, Abbott, and Argon Medical Devices are some of the key players in the body atherectomy and thrombectomy devices market.