- Smart Packaging

- Aseptic Packaging Market

Aseptic Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Aseptic Packaging Market by Material (Paper & Paperboard, Plastic, Others), Packaging Type (Cartons, Bottles & Cans, Others), Application, and Regional Analysis for 2026 - 2033

Aseptic Packaging Market Size and Trends Analysis

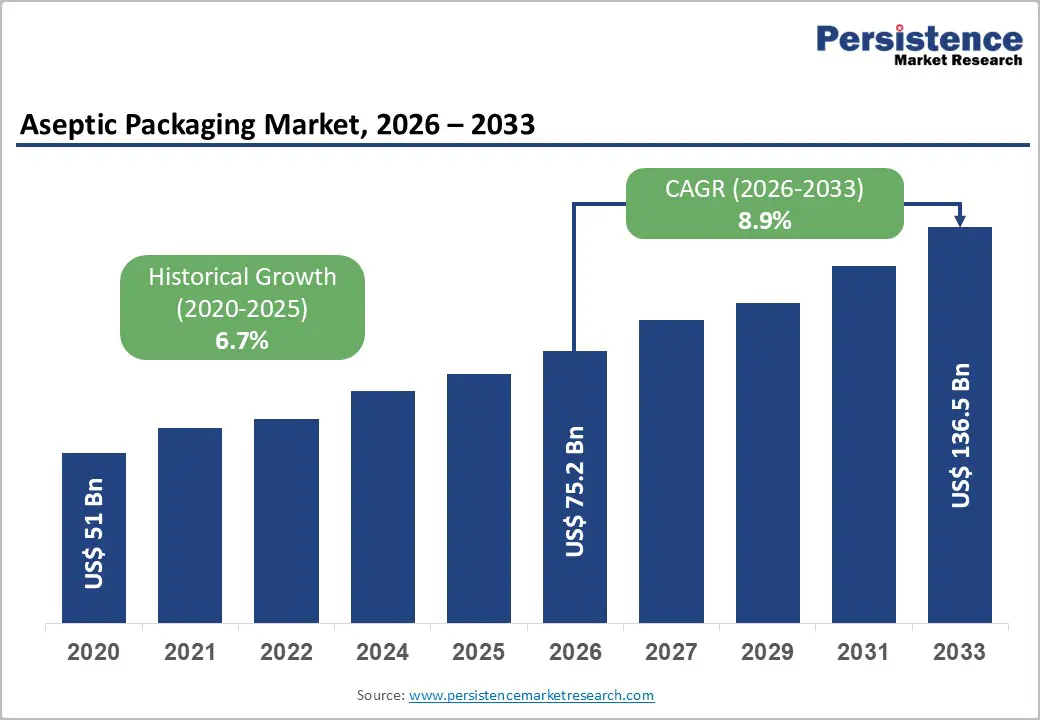

The global aseptic packaging market size is likely to be valued at US$75.2 billion in 2026 and is expected to reach US$136.5 billion by 2033, growing at a CAGR of 8.9% between 2026 and 2033, driven by rising consumption of shelf-stable beverages and liquid foods, increasing pharmaceutical demand for sterile primary packaging, and sustained investments in recyclable cartons and mono-material packaging solutions. Structural cost pressures in cold-chain logistics, tightening food-contact regulations, and the capital intensity of aseptic filling lines influence adoption timelines.

Key Industry Highlights

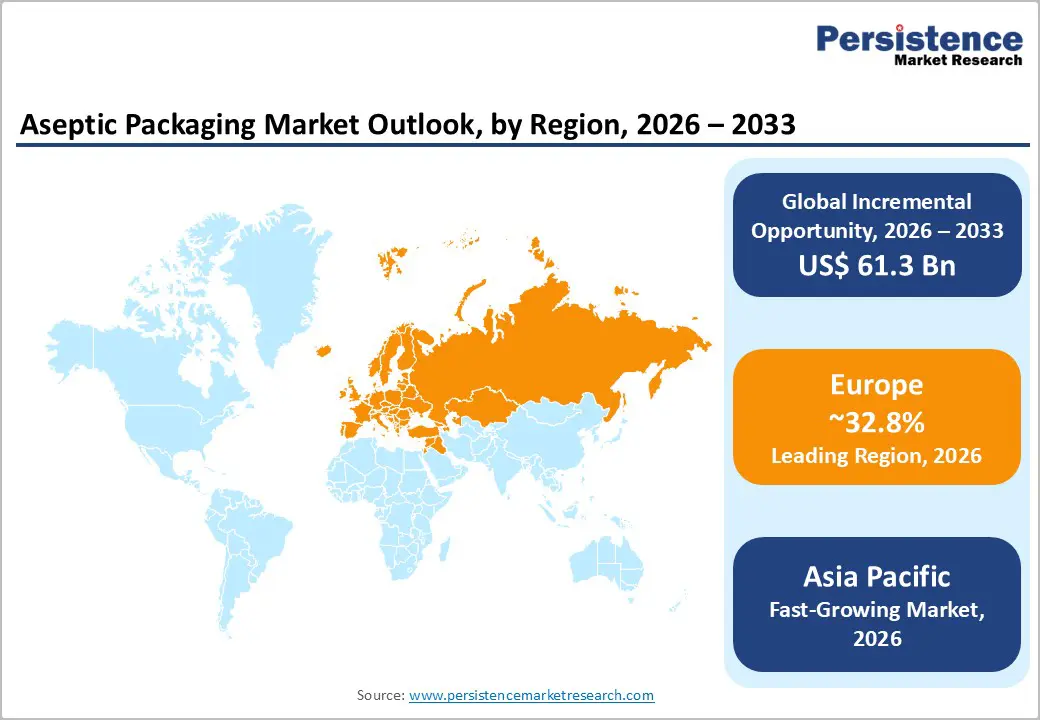

- Leading Region: Europe is projected to lead the market, accounting for approximately 32.8% of market share, supported by strong dairy and beverage consumption, regulatory harmonization, and early adoption of recyclable high-barrier carton solutions.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rising packaged dairy and beverage demand in China and India, expanding middle-class populations, and increased investments in localized aseptic manufacturing.

- Investment Plans: Major investments are focused on automation, digital aseptic monitoring, and modular filling systems, with North America and Asia Pacific accounting for a growing share of capital deployment in contract aseptic filling, pharmaceutical fill-finish capacity, and sustainable packaging innovation.

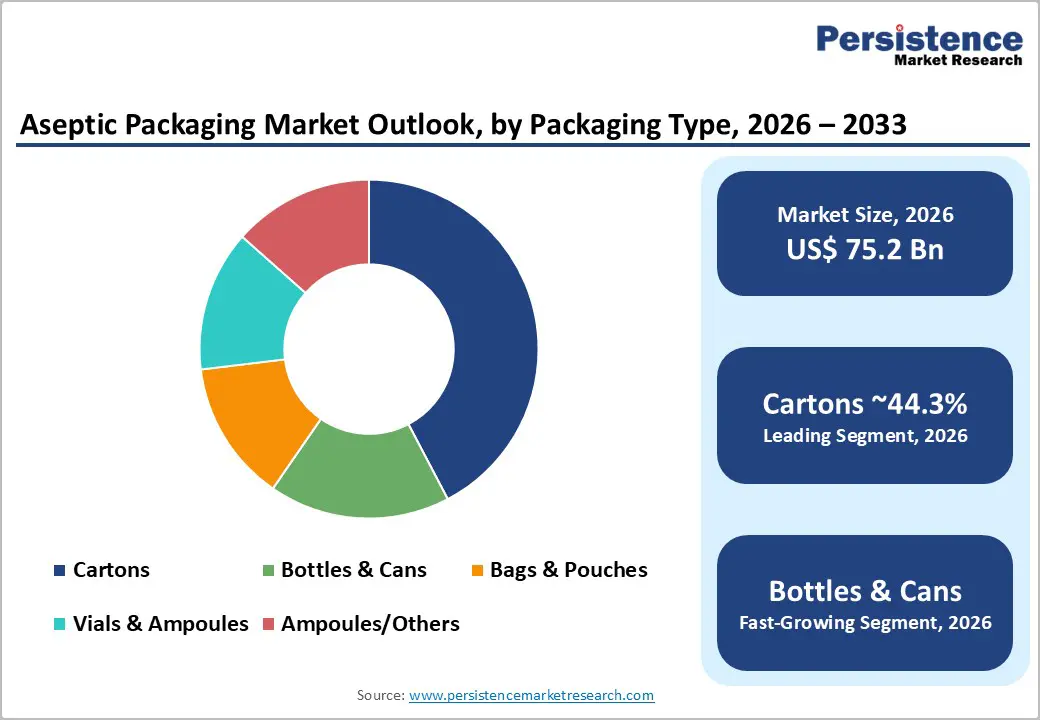

- Dominant Packaging Type: Cartons are anticipated to dominate the packaging type segment, holding an anticipated 44.3% market share, driven by their extensive use in UHT milk, juices, and plant-based beverages, along with integrated packaging-equipment systems that enhance operational efficiency and customer retention.

- Leading Application: Beverages are likely to be the largest application segment, contributing over 50.8% of the market share, supported by strong consumption of dairy, ready-to-drink beverages, and juices requiring ambient distribution and extended shelf life.

| Key Insights | Details |

|---|---|

| Aseptic Packaging Market Size (2026E) | US$75.2 Bn |

| Market Value Forecast (2033F) | US$136.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growth in Shelf-Stable Liquid and Ready-to-Drink Beverages

Aseptic packaging enables ambient storage and transportation while maintaining product safety and quality without preservatives. This capability significantly reduces reliance on refrigerated logistics, which often account for a single-digit to low double-digit percentage of finished-goods costs. Beverage manufacturers are increasingly shifting from chilled to ambient ready-to-drink formats, particularly for dairy alternatives, juices, and functional beverages. High-volume SKUs benefit from improved distribution reach and longer shelf life, creating measurable returns on investment for aseptic lines, especially in regions with extended supply chains and limited cold-storage infrastructure.

Rising Pharmaceutical and Biotechnology Sterile Packaging Demand

The growth of biologics, injectable therapies, and pre-filled drug delivery systems continues to elevate demand for aseptic vials, ampoules, and containers. Regulatory frameworks governing aseptic processing and good manufacturing practices impose stringent sterility requirements, favoring validated aseptic systems and qualified suppliers. Pharmaceutical aseptic packaging carries a higher per-unit value compared to food and beverage applications, increasing overall market value even at lower volumes. Capital investment in cleanrooms, validated filling equipment, and environmental monitoring systems reinforces long-term demand stability.

Sustainability and Material Innovation

Packaging suppliers are commercializing high-fiber cartons, paper-based barriers, and recyclable mono-material structures to reduce fossil-based polymer usage. These innovations align with circular-economy objectives and retailer sustainability commitments. Commercial-scale rollouts of paper-barrier aseptic cartons demonstrate that sustainability and performance requirements can coexist. Regulatory mandates in developed markets further accelerate adoption, enabling aseptic cartons to defend and expand their share relative to alternative packaging formats.

Barrier Analysis - High Capital Intensity and Operational Complexity

Aseptic filling and sterilization systems require substantial upfront investments in cleanroom infrastructure, validated equipment, and skilled labor. Qualification and commissioning cycles are lengthy, extending payback periods to multiple years. The adoption remains concentrated among large food, beverage, and pharmaceutical manufacturers. For mid-sized processors, greenfield aseptic investments and validation expenses can represent a high single-digit to low double-digit percentage of annual revenue, limiting penetration across fragmented supply chains and smaller product lines.

Regulatory and Compliance Complexity

Food-contact material regulations and aseptic processing requirements increase compliance costs and extend product development timelines. Updates to food-contact standards introduce transitional challenges, including additional testing, documentation, and material reformulation. Non-compliance risks include product recalls and restricted market access. Compliance-related expenditures typically add low single-digit percentage increases to per-unit packaging costs, particularly in highly regulated markets.

Opportunity Analysis - Emerging Markets in Asia Pacific and Africa

Urbanization, rising disposable incomes, and increasing consumption of shelf-stable dairy and beverages are driving aseptic packaging demand across Asia Pacific and parts of Africa. Manufacturers can unlock significant volume growth through modular, lower-capital aseptic solutions such as contract filling and compact sterilization units. Domestic dairy and juice markets in these regions represent multi-billion-dollar addressable opportunities, with regional contributions expected to increase materially toward 2030.

Sustainable Materials and Recycling Integration

Transitioning to recyclable fiber-based barriers and mono-polymer laminates allows brand owners to meet sustainability commitments while reducing end-of-life cost exposure. As national recycling infrastructures mature, particularly in Europe, value creation increasingly favors suppliers capable of integrating packaging design with recovery and recycling systems. Early adopters securing co-processing arrangements can monetize recovered materials and strengthen long-term customer relationships.

Category-wise Analysis

Packaging Type Insights

Cartons are expected to dominate, accounting for approximately 44.3% of the market share in 2026, primarily due to their widespread use in ambient liquid foods such as milk, flavored dairy drinks, fruit juices, and plant-based beverages. Their lightweight structure, excellent stackability, and longer shelf life significantly reduce transportation and warehousing costs across extended distribution networks. Integrated carton systems, where packaging materials, filling machines, and technical services are bundled, create high switching costs and reinforce long-term customer retention. These systems are particularly prevalent in large-scale dairy and beverage operations supplying national and export markets.

Bottles and cans are likely to be the fastest-growing segment, driven by the rising demand for ready-to-drink beverages, functional nutrition drinks, sports beverages, and premium single-serve offerings. Metal cans benefit from high barrier performance and carbonation compatibility, making them suitable for energy drinks and flavored sparkling beverages. Aseptic PET bottles are increasingly used for juices, dairy alternatives, and nutritional drinks, offering design flexibility and consumer convenience. Growth in contract aseptic filling facilities and smaller-batch production lines is accelerating adoption among new beverage brands and private-label manufacturers.

Application Insights

Beverages are expected to be the largest application segment, contributing over 50.8% of market share, supported by strong consumption of dairy products, fruit juices, flavored milk, and ready-to-drink beverages. Aseptic technology enables manufacturers to distribute products across wide geographic regions without refrigeration, lowering cold-chain dependency and improving cost efficiency. This advantage is particularly critical for exports and for serving markets with limited refrigerated infrastructure. Both multinational beverage brands and regional dairy processors continue to rely heavily on aseptic formats to scale distribution while maintaining product safety and quality.

The food segment is likely to witness rapid growth, as consumers increasingly favor shelf-stable, convenient meal solutions such as soups, sauces, purees, processed fruits, and baby food. Aseptic food packaging supports longer shelf life without preservatives while preserving taste and nutritional value. Growth is further reinforced by the expansion of e-commerce grocery platforms and modern retail formats, which prioritize ambient products due to lower storage and handling costs. Manufacturers are also adopting aseptic packaging to extend product reach into export and institutional foodservice channels.

Regional Insights

North America Aseptic Packaging Market Trends - Regulation-Driven Growth Anchored by Beverage, Dairy, and Pharmaceutical Aseptic Capacity

North America remains a significant revenue contributor to the global aseptic packaging market, underpinned by a strong demand from the beverage, dairy, and pharmaceutical sectors. The U.S. leads the region in installed aseptic filling capacity, supported by large dairy processors, multinational beverage brands, and a well-established contract aseptic filling ecosystem. Major beverage companies such as Coca-Cola and PepsiCo are steadily broadening their ready-to-drink juice, dairy-alternative, and functional beverage offerings, with many of these products packaged in aseptic cartons and bottles that enable nationwide distribution without the need for refrigeration.

The pharmaceutical sector further reinforces regional demand, particularly for aseptic vials, ampoules, and injectable packaging used in biologics, vaccines, and sterile injectables. The U.S. FDA regulations governing aseptic processing, validation, and sterility assurance impose high compliance requirements, creating structural entry barriers while maintaining consistent quality standards. These regulatory conditions favor established packaging suppliers and contract fill-finish providers with validated cleanroom infrastructure and proven compliance track records.

Investment trends across North America increasingly emphasize automation, digital process monitoring, and outsourced aseptic services. Packaging suppliers and equipment manufacturers are integrating Industry 4.0 capabilities, such as real-time sterility monitoring, predictive maintenance, and data-driven quality control, to improve uptime and reduce contamination risks. Pharmaceutical companies are expanding partnerships with specialized contract development and manufacturing organizations (CDMOs) to manage capital intensity and capacity constraints. Together, these factors position North America as a technologically advanced, regulation-driven aseptic packaging market with stable, high-value demand.

Europe Aseptic Packaging Market Trends - Sustainability-Led Market Leadership Supported by EU Regulation and Carton Recycling Infrastructure

Europe is expected to lead the global aseptic packaging market, accounting for an estimated 32.8% of total market share, supported by advanced recycling systems, strong regulatory frameworks, and early adoption of sustainable packaging technologies. Germany, the U.K., France, and Spain represent core demand centers across food, beverage, and pharmaceutical applications, with long-standing reliance on aseptic cartons for milk, juices, soups, and liquid nutrition products. European dairy and food multinationals such as Nestlé, Danone, and Arla Foods have historically driven large-scale adoption of aseptic packaging to support cross-border distribution and export-oriented supply chains.

Regulatory harmonization across the European Union plays a critical role in shaping market dynamics. EU packaging waste directives, circular economy action plans, and recycling targets have accelerated the shift toward recyclable, paper-based aseptic cartons and bio-based polymers. Packaging suppliers have hence intensified innovation in high-barrier materials that reduce aluminum content while maintaining shelf-life performance. These regulatory pressures favor suppliers with advanced material science capabilities and strong compliance infrastructure. Sustainability-driven investment is a defining regional trend. Packaging manufacturers and brand owners are collaborating to improve carton recycling rates, invest in collection infrastructure, and scale renewable material usage. Pharmaceutical demand also remains stable, supported by Europe’s strong generic drug manufacturing base and vaccine production capacity. Overall, Europe’s leadership reflects a combination of regulatory clarity, sustainability alignment, and mature end-user adoption across multiple aseptic applications.

Asia Pacific Aseptic Packaging Market Trends - High-Volume Expansion Fueled by Urbanization, UHT Dairy Adoption, and Modular Aseptic Systems

Asia Pacific is likely to be the fastest-growing regional market for aseptic packaging, driven by population growth, rising urbanization, and increasing consumption of packaged dairy, beverages, and shelf-stable foods. China and India account for a substantial share of volume growth, supported by expanding middle-class populations and improved access to packaged nutrition products. In these markets, aseptic cartons remain essential for distributing milk, flavored dairy drinks, and juices in regions where cold-chain infrastructure is limited or cost-prohibitive.

China continues to invest heavily in domestic beverage and dairy processing capacity, with local and multinational brands expanding aseptic filling lines to support national distribution. India shows similar momentum, where UHT milk and aseptic juice products are gaining traction due to longer shelf life and reduced wastage. Japan, while a more mature market, maintains a strong demand for aseptic pharmaceutical packaging, particularly for injectable drugs and aging-population healthcare needs.

A key regional trend is the expansion of localized manufacturing and modular aseptic systems. Packaging suppliers and equipment providers are increasingly offering scalable, lower-capacity aseptic lines tailored to regional brands, private-label producers, and contract manufacturers. This approach lowers capital barriers and enables faster market entry for emerging beverage and food companies. Collectively, these dynamics position Asia Pacific as a high-growth, volume-driven aseptic packaging market with increasing technological sophistication and expanding end-use diversity.

Competitive Landscape

The global aseptic packaging market is competitive, led by a small group of integrated players that provide both packaging materials and filling systems, supported by a broader ecosystem of converters and contract fillers. Competitive differentiation is driven by sustainability innovation, validated aseptic performance, and geographic reach. Key developments include the commercialization of paper-based barrier cartons, increased investment in recyclable mono-material solutions, and capacity expansions across Asia Pacific to support beverage and dairy growth. These initiatives enhance supply-chain resilience, reduce environmental impact, and strengthen regional market access. Market leaders prioritize vertical integration, sustainability-driven innovation, regionalized production, and service-oriented business models. Validated aseptic expertise and long-term customer partnerships serve as core competitive advantages.

Key Industry Developments

- In February 2025, Nissha Metallizing Solutions partnered with Tetra Pak to introduce a paper-based aseptic carton for milk featuring a recyclable barrier layer, reducing reliance on non-renewable materials and enhancing recyclability.

- In March 2025, Syntegon unveiled a new aseptic filling system for ready-to-use syringes at INTERPHEX 2025, expanding its sterile production portfolio and enhancing pharmaceutical aseptic processing capabilities.

Companies Covered in Aseptic Packaging Market

- Tetra Pak

- SIG Combibloc

- Elopak

- Amcor

- Greatview Aseptic Packaging

- Scholle IPN

- Uflex

- Schott

- IMA Group

- Ecolean

- Mondi Group

- Stora Enso

- DS Smith

- Nippon Paper Industries

- Goglio

- Wipak Group

- Printpack

- Sealed Air

Frequently Asked Questions

The aseptic packaging market is estimated to be US$75.2 billion in 2026.

The market is projected to reach US$136.5 billion by 2033, reflecting robust long-term growth.

Key trends include rising demand for shelf-stable beverages and liquid foods, increased pharmaceutical aseptic vial usage, commercialization of recyclable paper-based cartons, adoption of mono-material packaging, and capacity expansions in Asia Pacific.

By application, beverages (dairy, juices, RTD drinks) remain the leading segment, contributing over 50.8% of market demand.

The aseptic packaging market is expected to grow at a CAGR of 8.9% between 2026 and 2033, driven by expanding beverage and pharmaceutical applications and sustainability-focused innovations.

Major players include Tetra Pak, SIG Combibloc, Elopak, Amcor plc, Greatview Aseptic Packaging Co., Ltd.