- Electrical Equipment & Services

- Artillery Fire Control System Market

Artillery Fire Control System Market Size, Share, and Growth Forecast 2025 – 2032

Artillery Fire Control System Market by System Type (Command and Control Systems, Targeting Systems, Others), Component (Hardware, Software, Services), Application (Military, Defense, Commercial), and Regional Analysis for 2025-2032

Artillery Fire Control System Market Size and Trend Analysis

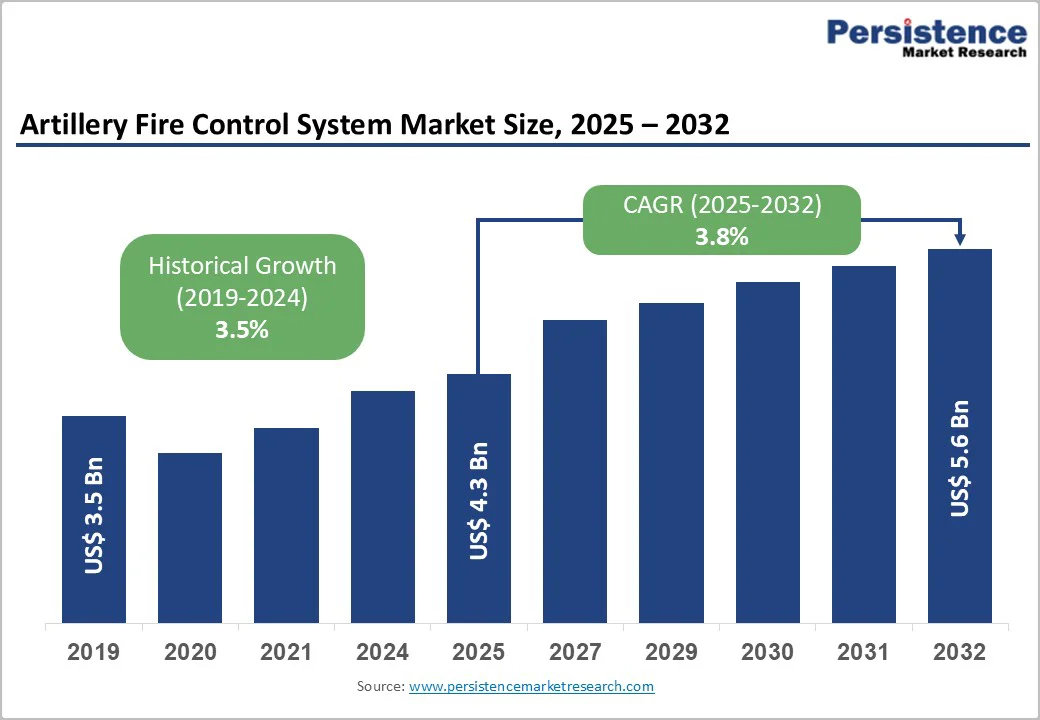

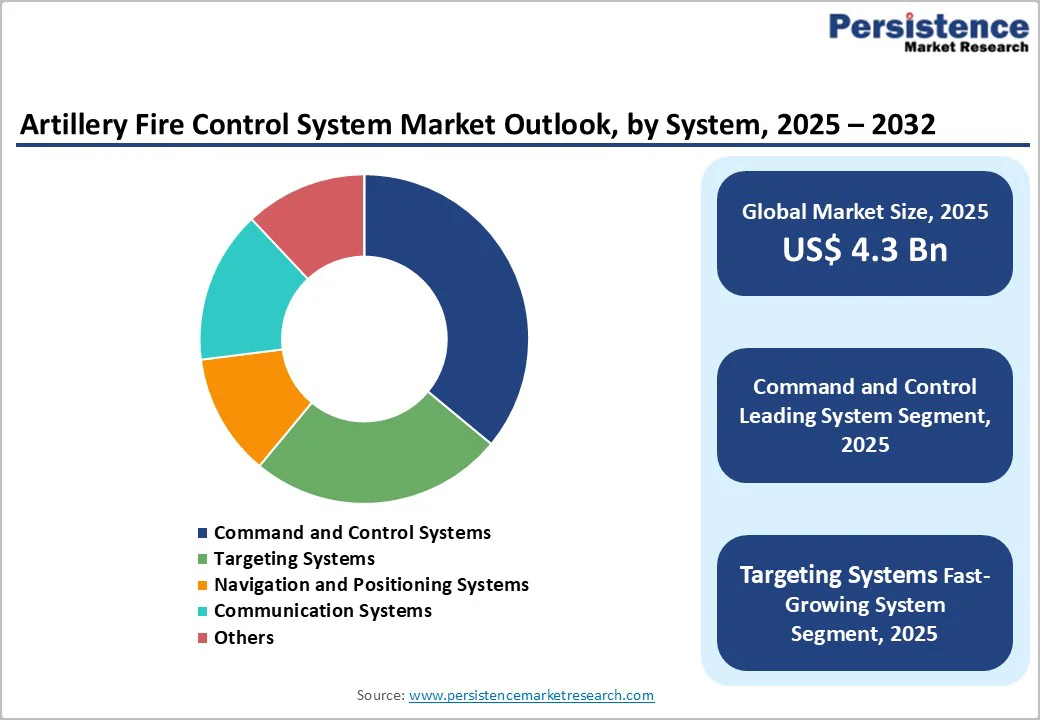

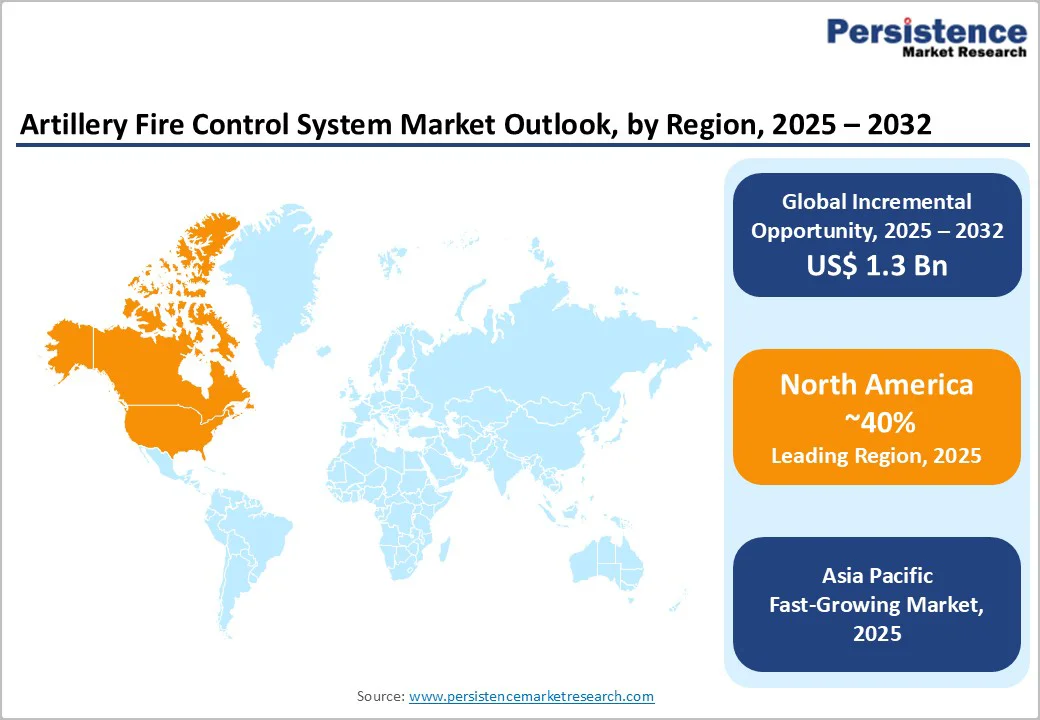

The global artillery fire control system market size is likely to be valued at US$4.3 billion in 2025 and is expected to reach US$5.6 billion by 2032, growing at a CAGR of 3.8% during the forecast period from 2025 to 2032, driven by large-scale artillery modernization programs aimed at enhancing precision, automation, and real-time battlefield responsiveness. Modern AFCS leverages AI-driven decision support, sensor fusion, and digital C2 architectures to boost accuracy and cut response times. Growing geopolitical tensions are driving defense spending across North America, Europe, and Asia Pacific, accelerating the adoption of advanced fire control systems. Militaries increasingly prioritize network-centric operations, C4ISR interoperability, and automated targeting to enhance counter-battery and long-range strike capabilities.

Key Industry Highlights

- Leading Region: North America leads the market with around 40% share, driven by U.S. defense modernization programs, strong R&D investments, and public-private partnerships advancing AI-enabled, network-centric fire control technologies.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rising defense budgets, modernization programs in China, India, Japan, and ASEAN nations, and increasing investment in indigenous, AI-enabled, networked fire control technologies.

- Leading System Type: The command and control systems segment leads the market with about 35% share, reflecting its vital role in real-time coordination and battlefield decision-making.

- Leading Component: Hardware component leads the market with over 50% share in 2025, driven by strong demand for sensors, control units, and communication modules.

- Leading Application Type: The military application segment leads the market with about 60% share, driven by extensive battlefield deployment requirements.

| Report Attribute | Details |

|---|---|

|

Artillery Fire Control System Market Size (2025E) |

US$4.3 Bn |

|

Market Value Forecast (2032F) |

US$5.6 Bn |

|

Projected Growth CAGR (2025-2032) |

3.8% |

|

Historical Market Growth (2019-2024) |

3.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements in Automation and AI

Advancements in artificial intelligence (AI), automation, and sensor fusion are transforming the operational capabilities of artillery fire control systems. Modern AFCS platforms now integrate AI-driven algorithms for target recognition, trajectory calculation, and fire mission optimization, enabling faster and more precise responses in dynamic combat scenarios. Automation minimizes human error and accelerates coordination between command centers, sensors, and firing units. Real-time data fusion also improves situational awareness, allowing forces to react swiftly to evolving threats and conduct effective counter-battery operations. Automated fire control enhances ammunition efficiency and reduces operational costs during sustained missions.

Leading defense manufacturers such as Raytheon Technologies, Lockheed Martin, BAE Systems, and Rheinmetall are actively incorporating AI-based decision-support and autonomous engagement functionalities into their artillery systems. Continuous R&D investment focuses on adaptive learning models capable of processing vast battlefield data from radar, drones, and satellite feeds. These innovations enhance targeting precision and enable seamless integration with multi-domain defense networks. Artillery units are increasingly connected with broader C4ISR frameworks, supporting joint-force operations. This technological evolution is driving the transition toward intelligent, network-centric artillery systems worldwide.

High Development and Maintenance Costs

The artillery fire control system (AFCS) market faces significant restraint due to the high costs associated with system development, integration, and long-term maintenance. Developing and testing these systems requires extensive R&D, compliance with defense standards, and integration with diverse artillery platforms. Ongoing maintenance, periodic software upgrades, cybersecurity enhancements, and calibration of sophisticated sensors and computing modules increase the total lifecycle costs. Customization requirements for different artillery platforms and terrain conditions elevate development expenses.

Many developing nations face budgetary constraints that limit their ability to adopt next-generation AFCS solutions, leading to reliance on legacy or semi-automated systems. The high financial burden also affects smaller defense contractors, reducing competition and innovation in the market. While technological sophistication drives operational superiority, it also creates a financial barrier to widespread adoption, particularly in regions with limited defense modernization budgets. Ongoing maintenance, periodic software upgrades, cybersecurity enhancements, and calibration of sophisticated sensors and computing modules further increase the total lifecycle costs. Customization requirements for different artillery platforms and terrain conditions further elevate development expenses.

Technological Convergence and Modular Systems

The convergence of AI, IoT, cloud computing, and advanced sensors offers a major growth opportunity in the artillery fire control system market. Integrating these technologies enables real-time data exchange, predictive analytics, and enhanced interoperability across platforms, transforming traditional fire control operations into intelligent, networked ecosystems. This convergence enables faster decisions, greater accuracy, and seamless coordination across artillery units and command centers. It also enhances situational awareness by integrating data from UAVs, radars, and satellite systems. Artillery forces can respond more effectively to dynamic and complex battlefield environments.

The shift toward modular system design amplifies this opportunity. Modular architectures allow defense forces to upgrade or customize individual components such as sensors, processors, or software without replacing entire systems, reducing lifecycle costs and enhancing flexibility. Leading manufacturers are increasingly adopting open-architecture and plug-and-play designs to enable interoperability across allied defense networks. As nations pursue adaptable defense systems, digital and modular integration will drive innovation and long-term growth in the AFCS market. This approach accelerates system deployment and simplifies future technology integration. As countries prioritize flexible and adaptable defense capabilities, digital convergence and modularization will continue to drive innovation.

Category-wise Insights

System Type Analysis

Command & control systems lead the artillery fire control system market, capturing around 35% of the total revenue share. These systems are critical as they enable real-time coordination, decision-making, and direct control of artillery assets linking firing units, sensors, and command centers into integrated operational networks, thereby delivering battlefield responsiveness and improved mission effectiveness. Their importance has increased with the shift toward network-centric warfare and joint-force operations, where rapid data exchange is essential. Modern C2 systems also support interoperability across allied forces and legacy platforms. For example, Rheinmetall’s ADLER fire control system is used across NATO forces, and Lockheed Martin’s digital command-and-control solutions are integrated into advanced artillery platforms.

The targeting systems segment is the fastest-growing category, driven by advances in precision targeting, AI-assisted detection, and sensor fusion. Capabilities such as automated target recognition, multi-sensor fusion, and decision-support software are raising demand steadily, positioning targeting systems as a major growth engine ahead of navigation, positioning, or communications subsystems. Growing reliance on UAVs, counter-battery radars, and satellite inputs accelerates the adoption of advanced targeting solutions. This positions targeting systems as a key growth engine ahead of navigation, positioning, and communication subsystems. For example, Elbit Systems’ digital targeting solutions are integrated into self-propelled artillery, and Raytheon’s sensor-enabled targeting modules support precision fire missions.

Component Type Analysis

Hardware component leads the market, accounting for over 50% share. This leadership is driven by the high demand for advanced sensors, control processors, and secure communication devices that form the backbone of modern fire control architectures. Continuous investments in network-compatible and battlefield-hardened hardware improve system reliability, targeting accuracy, and operational responsiveness across harsh environments. Hardware dominance is supported by artillery modernization and platform upgrades across land and naval forces. Retrofitting legacy artillery with modern hardware components sustains long-term demand. For example, the BAE Systems M109A7 Paladin self-propelled howitzer incorporates a state-of-the-art digital backbone and an onboard digital fire control system as a core part of its design.

The software segment is the fastest-growing segment, and the surge is fueled by innovations in AI-driven algorithms, real-time data analytics, and autonomous control capabilities that enhance targeting precision and decision-making. Cloud-enabled platforms and open-architecture software frameworks are increasingly adopted to ensure interoperability across multi-domain defense networks. Software upgrades offer cost-effective performance enhancement without full system replacement, accelerating adoption. This growth is complemented by services such as system integration, maintenance, and operator training, which ensure sustained system performance and generate stable recurring revenue.

Application Type Analysis

The military application segment leads the market, capturing around 60% of the total revenue share due to its direct use in battlefield operations. AFCS solutions are essential for precision targeting, real-time coordination, and mission adaptability, enabling effective artillery deployment in complex and high-threat combat environments. Ongoing modernization programs across major defense forces reinforce this segment’s dominance, supported by advances in secure communications, automation, and AI-driven decision support. For example, the U.S. Army’s integration of digital fire control systems in the M109A7 Paladin and India’s deployment of advanced AFCS in the K9 Vajra-T self-propelled howitzers.

Defense applications such as border security and strategic artillery placement are growing rapidly, driven by rising geopolitical tensions and the need for enhanced national security infrastructure. These systems support enhanced situational awareness and rapid response in sensitive regions. For example, Israel’s use of networked fire control systems for border defense and European NATO countries deploying digital artillery control systems for territorial security. The commercial segment, though smaller, is emerging in areas such as emergency response, disaster management, and infrastructure monitoring. The increasing adoption of integrated surveillance and command systems enhances border monitoring efficiency.

Regional Insights

North America Artillery Fire Control System Market Trends

North America holds a dominant position in the artillery fire control system (AFCS) market, capturing nearly 40% share, largely due to the U.S.’s extensive defense modernization efforts. The region is supported by a strong innovation ecosystem, with major defense players such as Raytheon Technologies, Lockheed Martin, and Northrop Grumman integrating AI, automation, and network-centric capabilities into advanced fire control solutions. Long-term procurement programs and consistent defense budgets sustain demand for next-generation AFCS, while ongoing upgrades of legacy artillery systems with digital fire control technologies continue to drive market growth.

Strong investments in R&D and public-private partnerships are fostering continuous advancements in AI-based targeting, sensor fusion, and digital command networks. The rising demand for interoperable and automated fire control solutions aligned with modern network-centric warfare strategies is a key growth driver. Integration of C4ISR systems (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) with the concept of multi-domain operations (MDO) significantly enhances real-time battlefield coordination. Enabling faster decision-making and synchronized operations across land, air, sea, cyber, and space domains.

Europe Artillery Fire Control System Market Trends

Europe remains a significant market for artillery fire control systems, fueled by large-scale modernization programs across NATO member states, aimed at improving precision, interoperability, and rapid-response capabilities. EU defense harmonization policies and cross-border cooperation have enabled extensive joint ventures and collaborative R&D efforts, strengthening the region’s defense ecosystem. Rising regional security concerns have accelerated artillery upgrades and the procurement of advanced fire control technologies. Coordinated defense spending across member states supports long-term demand for next-generation AFCS solutions.

Europe is embracing digitalization, and network-centric operations fire control suites now increasingly incorporate sensor-fusion technologies, ballistic computation, and integration with C4ISR systems. European defense industries are also reinforcing supply-chain resilience and supporting indigenous production of key components, enabling faster adoption of modular, upgradeable architectures. This strategy strengthens domestic manufacturing capabilities and improves long-term system reliability. It also supports the integration of digital targeting, automated decision support, and multi-sensor networks across NATO artillery units.

Asia Pacific Artillery Fire Control System Market Trends

Asia Pacific is the fastest growing region, driven by rising defense budgets, regional border and maritime tensions, and a pronounced shift toward indigenous manufacturing. Major regional powers are investing heavily in advanced fire-control technologies to enhance precision and battlefield coordination. Regional initiatives promoting indigenous production and technology transfer are strengthening local manufacturing capabilities and reducing reliance on imports. Programs such as India’s K9 Vajra-T procurement and China’s modernization of self-propelled artillery highlight the region’s commitment to upgrading fire control capabilities. Regional initiatives promoting technology transfer and domestic production are strengthening local defense industries and reducing dependence on imports.

A major trend driving the market is the swift shift toward digital and modular fire control systems. Modern AFCS platforms in Asia Pacific increasingly feature sensor fusion, automated targeting, and integrated C4ISR connectivity, enabling faster and more accurate response capabilities. Nations are also emphasizing interoperability and automation to support multi-domain operations across land and maritime borders. Integration of UAVs, counter-battery radars, and satellite feeds enhances targeting precision and situational awareness. These advancements also facilitate real-time data sharing between units, improving coordinated strikes and overall battlefield effectiveness.

Competitive Landscape

The global artillery fire control system (AFCS) market exhibits a moderately consolidated structure, driven by technological differentiation, strategic alliances, and long?term defense contracts among major defense and security suppliers. Established players compete intensely on the basis of innovation, product integration, and regional presence as countries modernize artillery capabilities and invest in network?centric warfare technologies. With key leaders including Lockheed Martin Corporation, BAE Systems plc, Rheinmetall AG, Elbit Systems Ltd., and Raytheon Technologies Corporation, the market reflects diverse portfolios across command and control, targeting, sensor fusion, and integrated AFCS modules.

These players compete through continuous R&D investment, strategic partnerships, localized production, and tailored solutions to meet specific defense procurement requirements. Many firms incorporate advanced AI, automation, and multi?domain interoperability into their fire control suites to differentiate offerings. Regional collaborations, joint ventures, and offset agreements also enhance competitiveness, particularly in fast?growing markets such as Asia Pacific. Smaller and regional manufacturers such as Bharat Electronics Limited (BEL), Hanwha Aerospace, and ASELSAN are entering niche segments or subsystem supply, intensifying competition.

Key Industry Developments:

- In December 2025, Lithuania signed a contract to acquire 30 CAESAR MkII 6×6 artillery systems, expanding its fleet to 48 units. The upgraded CAESAR MkII features enhanced engine power, an armored cabin for improved crew protection, and a redesigned digital architecture to boost interoperability, cybersecurity, and integration with modern fire control systems.

- In July 2025, DRDO’s 155mm/52-calibre ‘shoot-and-scoot’ mounted gun system was cleared for Indian Army trials. Built on an 8×8 high-mobility platform with around 85% indigenous content, the system enables rapid deployment, firing, and relocation within 85 seconds, enhancing battlefield survivability. It has completed internal testing, validating its reliability and operational performance across diverse terrains.

Companies Covered in Artillery Fire Control System Market

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- BAE Systems

- Thales Group

- Elbit Systems

- General Dynamics

- Leonardo

- Rheinmetall

Frequently Asked Questions

The artillery fire control system market is valued at US$4.3 billion in 2025 and expected to reach US$ 5.6 billion by 2032, reflecting robust growth.

Major drivers include increased defense budgets amid geopolitical tensions, technological advancements in AI and automation, and rising demand for networked warfare capabilities.

The command and control systems segment leads with a 35% market share, driven by its critical role in real-time coordination and battlefield decision-making.

North America dominates, capturing over 40% driven by robust defense investments and technological innovation.

Expansion into emerging markets such as Asia Pacific and the development of modular, upgradeable system architectures present significant growth opportunities.