- Industrial Goods & Service

- Anti-Riot Equipment Market

Anti-Riot Equipment Market Size, Share, and Growth Forecast 2025 - 2032

Anti-Riot Equipment Market by Equipment Type (Protective Gear, Non-lethal Weapons, Others), Application (Crowd Control, Public Safety Operations, Others), End-user (Law Enforcement Agencies, Others), and Regional Analysis for 2025 - 2032

Anti-Riot Equipment Market Size and Trends Analysis

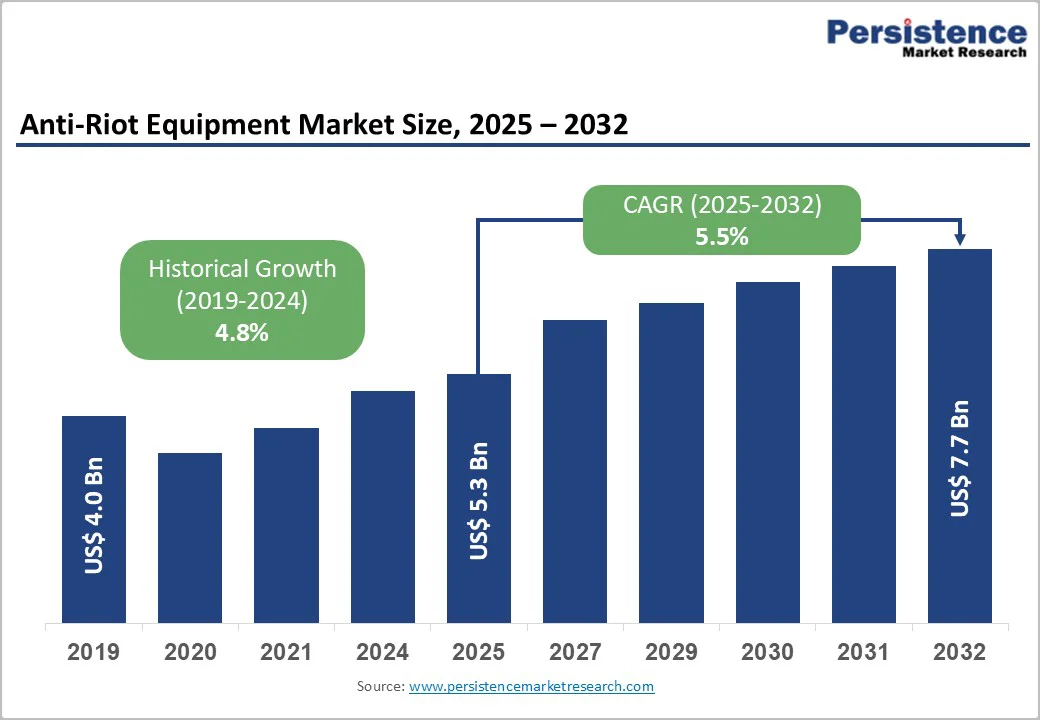

The global anti-riot equipment market size is likely to be valued at US$5.3 billion in 2025 and is expected to reach US$7.7 billion by 2032, growing at a CAGR of 5.5% during the forecast period from 2025 and 2032, driven by the rising frequency of public demonstrations and crowd-management events, political protests, and public demonstrations across both developed and developing regions.

Governments are increasingly prioritizing modernization of law enforcement and internal security forces, leading to higher procurement of protective gear, non-lethal weapons, surveillance systems, and crowd-control barriers. The integration of technologies such as AI-enabled surveillance, drones, real-time communication systems, and smart protective equipment is reshaping operational effectiveness and response strategies.

Key Market highlights:

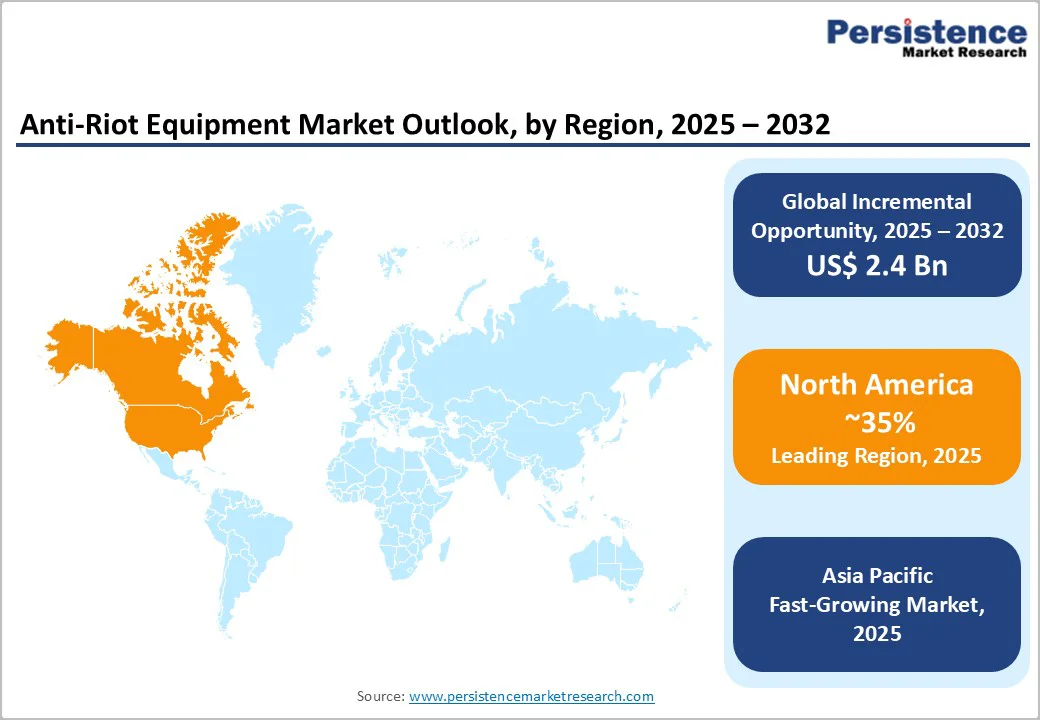

- Leading Region: North America leads the market with around 35% share, driven by U.S. innovation, strong law enforcement modernization, and high investments in advanced non-lethal and smart protective equipment.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rapid urbanization, rising security budgets, and increasing socio-political unrest across China, India, Japan, and ASEAN countries, supported by cost-effective local manufacturing and expanding domestic–international collaborations.

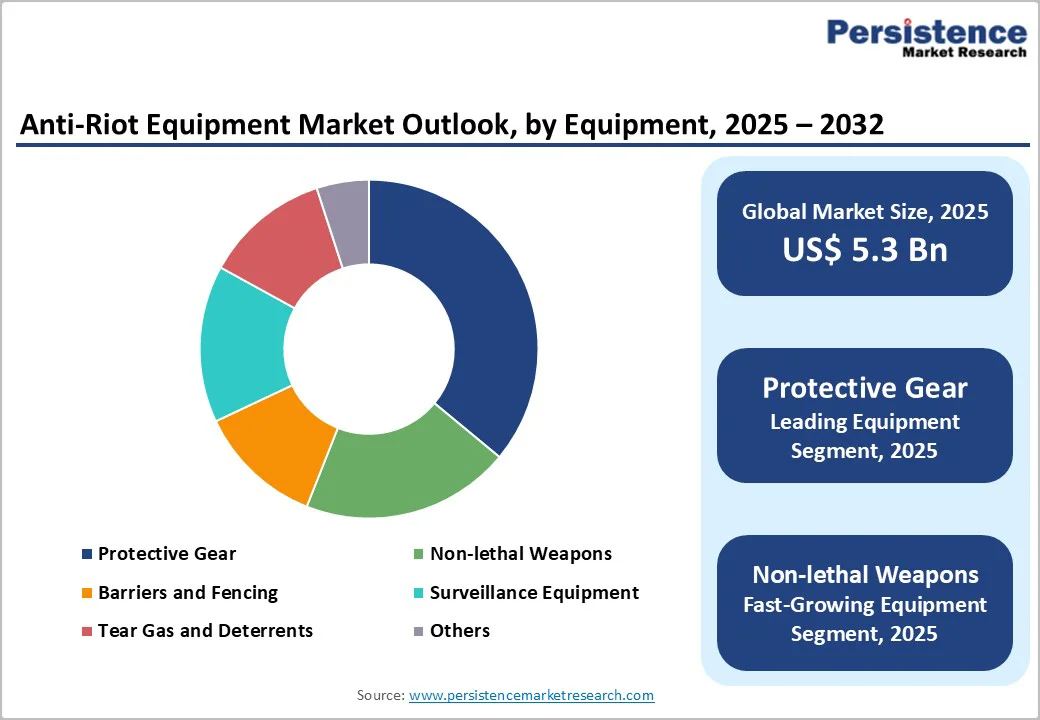

- Leading Equipment Type: Protective gear leads the market with nearly 42% share in 2025, driven by its vital role in officer safety and continuous innovations in lightweight, high-impact-resistant materials, enhancing comfort and durability.

- Leading Application: Crowd control leads the market with over 45% share as increasing protests and public unrest drive strong demand for advanced and diversified riot management solutions.

- Leading End-user: Law enforcement agencies are the leading segment in the market with about 72% share, driven by extensive adoption of riot control equipment by police and federal forces to maintain public order and safety.

| Key Insights | Details |

|---|---|

|

Anti-Riot Equipment Market Size (2025E) |

US$5.3 Bn |

|

Market Value Forecast (2032F) |

US$7.7 Bn |

|

Projected Growth CAGR (2025-2032) |

5.5% |

|

Historical Market Growth (2019-2024) |

4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Government Security Expenditure

Increasing government security expenditure has become a key growth driver in the anti-riot equipment market. Governments worldwide are prioritizing the modernization of law enforcement and internal security agencies to address the rising civil unrest, public demonstrations, and evolving security threats. Substantial portions of national budgets are now directed toward upgrading protective gear, surveillance systems, and non-lethal weaponry to ensure safer, more efficient crowd control operations. Many countries are also strengthening domestic manufacturing and procurement programs to reduce import dependence and accelerate equipment deployment. This focus on readiness and rapid response is increasing demand for standardized, high-performance anti-riot solutions.

In developed regions such as North America and Europe, rising security budgets support the integration of next-generation non-lethal technologies and smart protective equipment. The U.S., in particular, continues to lead in R&D investments for public safety, focusing on enhanced officer protection and improved situational awareness systems. European nations are investing in human-rights-compliant riot control tools and technology-enabled surveillance to balance security needs with regulatory requirements. These government-led initiatives collectively reinforce consistent demand and long-term growth for the anti-riot equipment industry.

High Equipment Costs and Budget Constraints

High equipment costs and budget limitations remain critical restraints to the growth of the market. Advanced systems such as smart protective gear, non-lethal weapons, and integrated surveillance tools demand high R&D and production investments. These innovations, while improving safety and effectiveness, significantly raise acquisition costs for law enforcement and security agencies. Expenses related to training, maintenance, and periodic upgrades further increase the total cost of ownership, making adoption challenging for budget-constrained agencies.

Many developing economies and smaller law enforcement agencies struggle to allocate sufficient funds for large-scale procurement, leading to delayed modernization cycles. These fiscal limitations hinder the ability of agencies to replace outdated equipment with advanced alternatives, slowing overall market growth. Economic uncertainties and shifting government priorities toward social welfare and infrastructure also impact security spending consistency. Manufacturers are increasingly focusing on cost-optimized solutions, modular designs, and local production to enhance affordability and improve market penetration in emerging regions.

Expansion in Civil Protection and Private Security Sectors

The expansion of civil protection and private security sectors presents a significant growth opportunity in the anti-riot equipment market. As public safety responsibilities increasingly extend beyond traditional law enforcement, private security agencies and civil protection units are emerging as major consumers of riot-control and protective equipment. Rapid urbanization, frequent large-scale public events, and rising security risks at commercial, industrial, and political venues are driving demand for protective gear, non-lethal weapons, surveillance systems, and crowd-control barriers. Private security firms are increasingly required to deploy professional-grade equipment comparable to that used by public agencies.

Governments are also strengthening civil protection units for rapid response to emergencies, protests, and public disorder, which rely on the same category of anti-riot tools. The growing adoption of public–private partnerships (PPPs) in security operations across Asia Pacific, the Middle East, and Latin America supports market expansion. Regulatory reforms mandating standardized training, certification, and approved equipment for private security personnel are accelerating adoption. These developments are broadening the customer base, diversifying revenue streams, and creating long-term growth opportunities for anti-riot equipment manufacturers.

Category-wise Insights

Equipment Type Analysis

Protective gear dominates the anti-riot equipment market, accounting for roughly 42% of total revenue, driven by its critical role in protecting personnel during protests, riots, and crowd-control operations. Law enforcement agencies worldwide are prioritizing advanced helmets, shields, and body armor made from lightweight, high-impact-resistant materials such as aramid fibers and composite polymers to enhance mobility and comfort. Continuous innovation in ergonomic design and material science further supports the adoption. For example, India’s DRDO introduced a lightweight bulletproof jacket using advanced ceramic plate technology, improving ballistic protection while reducing weight.

The non-lethal weapons segment is the fastest-growing category, driven by the increasing preference for less-lethal crowd control solutions to minimize injuries and fatalities. Technologies such as directed-energy weapons, tasers, acoustic deterrent devices, and chemical agents are gaining traction among military, police, and private security forces. Governments are investing heavily in non-lethal weapon R&D to balance effective threat neutralization with human-rights compliance. For example, Haryana Police became the first in India to deploy indigenously developed tear gas drones for crowd dispersal, highlighting technological advancements in this segment.

Application Type Analysis

Crowd control leads the market, accounting for over 45% share, driven by the rising frequency of mass protests, demonstrations, and public unrest across both developed and developing nations. Law enforcement agencies are increasingly investing in advanced protective gear, barriers, and surveillance systems to ensure effective crowd management and minimize casualties. For instance, several European countries have expanded the use of AI-enabled surveillance and crowd-monitoring drones to enhance real-time situational awareness during public demonstrations. Rising investments in integrated command-and-control systems that combine video analytics, communication networks, and field equipment are strengthening crowd control capabilities.

The terrorism and riot response segment is the fastest-growing application area. Heightened security threats and frequent terror-related incidents are compelling governments to invest in specialized anti-riot and counter-terror equipment. This includes advanced non-lethal weapons, tactical armor, and mobile defense systems designed for high-risk operations. Rising defense budgets and expanded funding through counter-terrorism initiatives, especially in Asia Pacific and the Middle East, are accelerating adoption. For instance, Punjab, Pakistan, has established a dedicated Riot Management Police force trained in less-lethal tactics and negotiation, underscoring growing investment in specialized crowd-control and response units.

End-user Type Analysis

Law enforcement agencies dominate the market, capturing around 72% of the total market share. This dominance stems from the critical role of police, paramilitary, and federal forces in maintaining civil order, managing protests, and responding to emergencies. Continuous government investments in modernizing police infrastructure and providing advanced non-lethal weapons, protective gear, and surveillance tools are fueling a steady demand. For example, Delhi Police inducted advanced anti-riot vehicles equipped with water cannons and surveillance systems, reflecting growing emphasis on preparedness. Police forces across North America and Europe are increasingly deploying smart protective gear, body-worn cameras, and AI-enabled monitoring systems to enhance situational awareness and accountability during crowd-control operations.

Private security firms represent the fastest-growing end-user segment, supported by the rising trend of outsourcing security responsibilities for events, commercial establishments, and private properties. Increasing urbanization, corporate sector expansion, and a surge in large-scale public gatherings are driving greater reliance on professional security services. Regulatory frameworks mandating standardized training and certified equipment use have improved operational efficiency and boosted product demand. In regions such as Asia Pacific and the Middle East, private firms are increasingly equipped with non-lethal crowd-control tools and protective gear comparable to law enforcement standards. Regulatory frameworks mandating standardized training and certified equipment use are improving operational efficiency and accelerating product adoption in this segment.

Regional Insights

North America Anti-Riot Equipment Market Trends

North America is emerging as the leading region, accounting for a 35% share, driven by the U.S. The region’s dominance is supported by extensive government spending on law enforcement modernization and public safety initiatives. Agencies are increasingly adopting modern protective gear, barriers, and surveillance technologies designed to enhance operational efficiency while minimizing injury risks. For example, U.S. police departments have upgraded riot shields and body armor with lightweight composite materials to improve mobility during protests.

North America is experiencing a shift toward technology-driven and ethically compliant riot-control solutions, reflecting growing emphasis on transparency and responsible use of force in law enforcement operations. Manufacturers are increasingly developing smart protective gear featuring embedded sensors, AI-enabled threat monitoring, and body-worn cameras to enhance situational awareness and accountability. For example, Axon’s expansion of integrated body-worn cameras and evidence-management systems across U.S. police forces reflects this trend. In parallel, partnerships between defense suppliers and law enforcement agencies are accelerating innovation in non-lethal technologies, including acoustic devices and chemical deterrents.

Europe Anti-Riot Equipment Market Trends

Europe remains a significant market for anti-riot equipment, driven by frequent civil demonstrations, political protests, and large public gatherings across major economies such as Germany, France, the U.K., and Italy. Governments across the region are steadily investing in the modernization of police and internal security forces, with a strong emphasis on equipment that balances operational effectiveness with strict human-rights and safety compliance. For example, French law enforcement has expanded the use of advanced protective gear and crowd-control vehicles during large-scale protests.

Europe is witnessing a rapid shift toward technology-driven and non-lethal riot control solutions. Law enforcement agencies are increasingly adopting AI-enabled surveillance systems, drones, and communication-integrated protective gear to enhance real-time situational awareness and coordination. The growing preference for less-lethal options such as acoustic deterrents, pepper sprays, and electric shock devices reflects a strong regulatory focus on minimizing harm during crowd management. For example, Germany and the Netherlands have increased the deployment of less-lethal tools such as pepper spray, acoustic deterrents, and electric shock devices.

Asia Pacific Anti-Riot Equipment Market Trends

Asia Pacific is the fastest-growing region in the market, driven by urbanization and socio-political unrest becoming more frequent. Governments across countries such as India, China, Indonesia, and Thailand are increasing their investments in law-enforcement modernization, crowd-control measures, and non-lethal technologies. Demand is particularly strong for protective gear such as helmets, shields, and body armor, along with non-lethal weapons, including rubber bullets, water cannons, and tear gas systems. For example, Indian police forces have expanded procurement of modern riot-control vehicles and protective equipment.

Technological integration is reshaping the market landscape. Authorities are incorporating smart surveillance systems, drones, wearable sensors, and AI-powered crowd-analysis tools into their riot-control arsenals. Local manufacturing capabilities are also improving, giving cost advantages and faster deployment in emerging markets. Asia Pacific region is emerging as not just a high-growth market, but also a center for innovation in the anti-riot equipment space. Improving local manufacturing capabilities in countries such as India and China is providing cost advantages and faster deployment.

Competitive Landscape

The global anti-riot equipment market is moderately fragmented, supported by rising demand from law enforcement, military, and private security agencies worldwide. It comprises a mix of large defense manufacturers and specialized public-safety equipment providers offering protective gear, non-lethal weapons, surveillance systems, and crowd-control solutions.

Leading companies such as Safariland Group, Rheinmetall AG, BAE Systems, Condor Non-Lethal Technologies, FN Herstal, and Axon Enterprise compete across developed and emerging markets. Competition is driven by broad, integrated product portfolios, innovation in smart protective equipment and AI-enabled monitoring systems, and value-added services such as training, customization, and long-term after-sales support.

Key Market Developments:

- In 2025, Punjab, Pakistan, established its first Riot Management Police unit, equipped with advanced gear and trained in less-lethal crowd-control and negotiation tactics.

- In 2025, Delhi Police introduced 10 advanced “Vajra Vahans,” featuring insulated water systems, two-way communication, first aid kits, and drone and CCTV mounts for improved awareness and safety.

Companies Covered in Anti-Riot Equipment Market

- Lamperd

- Combined Systems

- Axon

- Hagor Industries

- AMTEC Less-Lethal Systems

- LRAD Corporation

- Security Devices International

- Deenside

- Compass International Corp

- Senken Group

- Paulson Manufacturing Corporation

- Beijing Anlong Group

Frequently Asked Questions

The anti-riot equipment market is valued at US$5.3 billion in 2025 and expected to reach US$7.7 billion by 2032, reflecting robust growth.

Drivers include increasing government security expenditure, rising civil unrest, technological advancements in less-lethal equipment, and expanding application areas such as terrorism response.

Protective gear leads with a 42% share, due to its vital role in officer safety and continuous innovations in lightweight, high-impact-resistant materials, enhancing comfort and durability.

North America dominates, capturing over 35% driven by strong government investments, innovation, and established manufacturing.

Emerging markets in Asia Pacific present significant growth opportunities, supported by increasing governmental spending and local manufacturing strengths.