- Pharmaceuticals

- Anabolic Steroids Market

Anabolic Steroids Market Size, Share and Growth Forecast, 2026-2033

Anabolic Steroids Market by Compound Type (Testosterone, Oxandrolone, Methyl Testosterone, Stanozolol/Boldenone, Others), Route of Administration (Oral, Injectable, Transdermal Delivery Systems, Others), End-Use (Medical, Non-Medical, Veterinary, Others), and Regional Forecast for 2026-2033

Anabolic Steroids Market Share and Trends Analysis

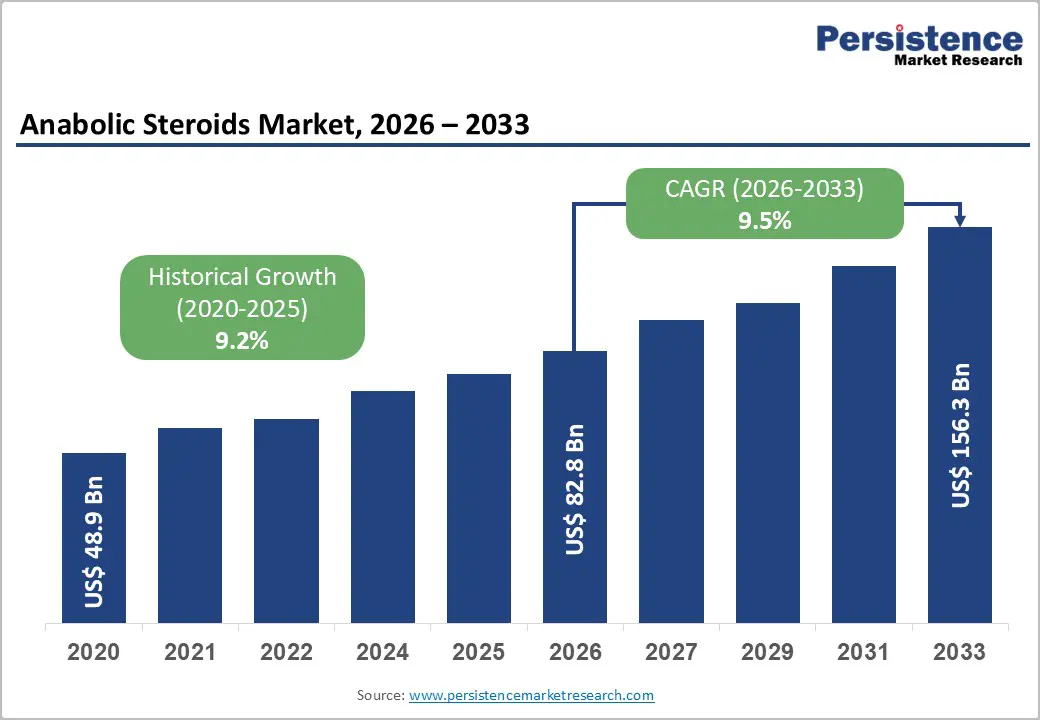

The global anabolic steroids market size is likely to be valued at US$ 82.8 billion in 2026, and is projected to reach US$ 156.3 billion by 2033, growing at a CAGR of 9.5% during the forecast period 2026 - 2033. Rising clinical diagnosis rates of testosterone deficiency have driven significant expansion of this market. Healthcare providers have increasingly prescribed these therapies to treat muscle-wasting disorders, while sustained demand persists from fitness enthusiasts seeking performance enhancement. Regulatory agencies have enhanced product standardization and traceability, which bolsters physician trust in legitimate anabolic prescriptions (APs).

Innovations in transdermal patches and long-acting injectable formulations have improved patient adherence and treatment efficacy. These developments minimize side effects and simplify dosing regimens, positioning anabolic steroids for broader clinical adoption. Pharmaceutical companies continue to invest in safer delivery systems, which will sustain market growth amid evolving healthcare needs.

Key Industry Highlights

- Dominant End-Use: Medical applications are expected to lead with 55% market share in 2026, aided by the increased adoption of physician-supervised hormone replacement therapies.

- Leading Compound Type: Testosterone-based compounds are likely to lead with about 48% in 2026, driven by strong clinical validation, broad regulatory approvals, and first-line use in endocrine treatments.

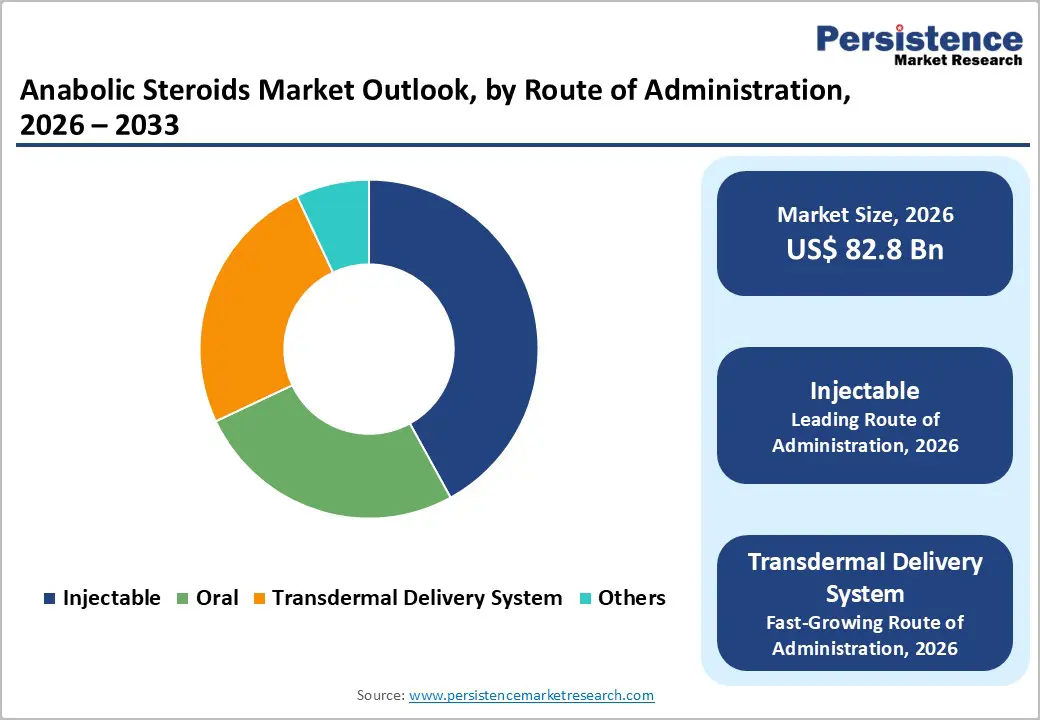

- Dominant Route of Administration: Injectable anabolic steroids are expected to account for 42% of revenues in 2026, owing to their superior bioavailability and strong physician preference for chronic therapy.

- Fastest-Growing Administration Route: Transdermal systems are projected to grow at roughly 10.5% CAGR from 2026 to 2033, supported by their non-invasive nature, leading to improved adherence among patients.

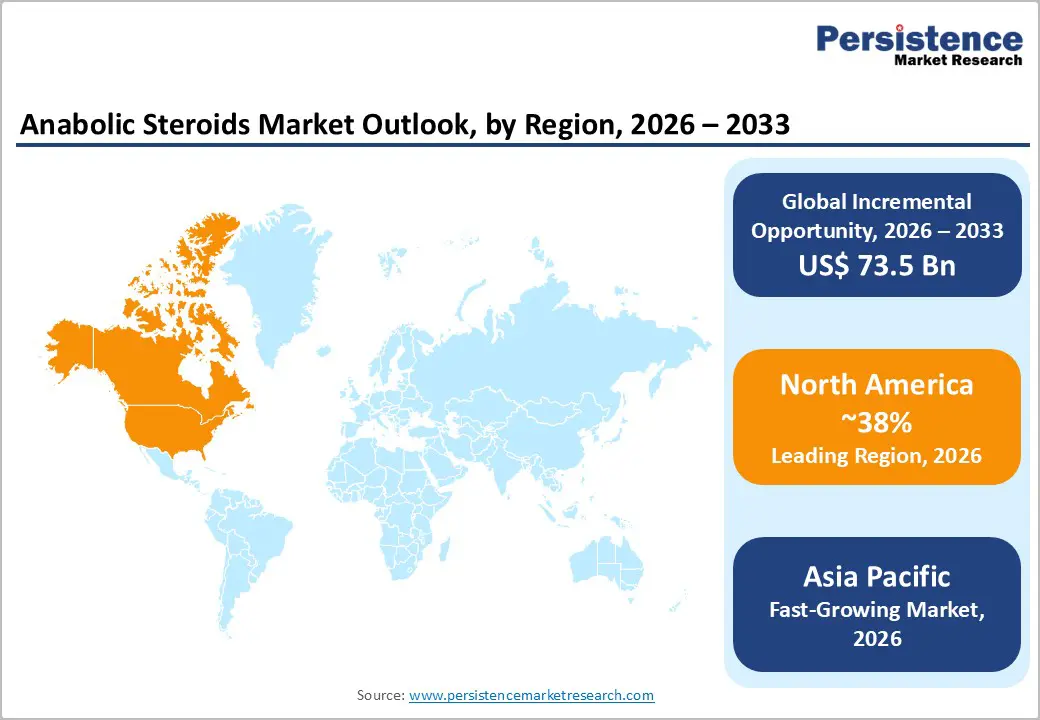

- Regional Leadership: North America is expected to lead with 38% market share in 2026, while the Asia Pacific market is set to grow the fastest at a 10.8% CAGR, owing to expanding healthcare access and manufacturing scale.

- Competitive Environment: Top players are deepening their market presence through regulatory-compliant innovation and geographic expansion, with an increasing focus on advanced delivery technologies.

| Key Insights | Details |

|---|---|

| Anabolic Steroids Market Size (2026E) | US$ 82.8 Bn |

| Market Value Forecast (2033F) | US$ 156.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Clinical Demand and Sustained Performance-Oriented Usage

The growing prevalence of testosterone deficiency and muscle-wasting disorders is a key structural driver of the anabolic steroids market. According to the U.S. National Institutes of Health (NIH), clinically significant hypogonadism affects approximately 20–25% of men over 60, while sarcopenia prevalence exceeds 10% among adults above 65, directly increasing demand for testosterone-based therapies in regulated healthcare systems. Rising physician awareness, improved diagnostic protocols, and broader insurance coverage for hormone replacement therapy have strengthened prescription volumes. In parallel, the U.S. Food and Drug Administration (FDA) and European Medicines Agency (EMA) have approved multiple next-generation testosterone formulations since 2020, improving pharmacokinetic consistency and supporting wider adoption across elderly and chronic care patient groups.

Alongside medical use, non-medical demand continues to contribute meaningfully to overall market volumes. The World Anti-Doping Agency (WADA) reports that anabolic steroids account for over 45% of detected doping violations globally, underscoring their widespread use across bodybuilding and recreational fitness segments. Expansion of organized fitness infrastructure, growth of online supplementation platforms, and continued activity within informal distribution channels are sustaining consumption, particularly in emerging economies where regulatory enforcement remains inconsistent. While this segment faces legal and ethical scrutiny, its scale reinforces overall market momentum, complementing medically driven growth and supporting the long-term expansion of the anabolic steroids market.

Regulatory Stringency and Heightened Public Health Scrutiny

Anabolic steroids are classified as controlled substances across developed markets such as the U.S., Canada, and the European Union (EU), creating a highly restrictive operating environment. Prescription-only mandates, import–export controls, and criminal penalties for misuse limit commercial scalability. The U.S. Drug Enforcement Administration (DEA) enforces Controlled Substances Act compliance through manufacturing quotas, audits, and distributor licensing. Similarly, the EMA mandates stringent pharmacovigilance and manufacturing authorizations. These requirements increase compliance costs and extend approval timelines. Smaller manufacturers are disproportionately impacted, restricting new entrants and cross-border expansion despite sustained demand.

Public health scrutiny further intensifies regulatory pressure on the market. The World Health Organization (WHO) and the Centers for Disease Control and Prevention (CDC) continue to issue advisories highlighting cardiovascular, endocrine, and psychiatric risks associated with non-therapeutic use. Several national health authorities have strengthened enforcement actions against illicit online and gym-based distribution networks. Increased media attention and litigation risk elevate reputational exposure for manufacturers. This environment discourages aggressive promotion beyond clinical settings. As a result, companies adopt conservative, evidence-based commercialization strategies that moderate overall market penetration.

Emerging Markets and Diversified Therapeutic Applications

The expansion of regulated hormone therapies in emerging markets presents a significant growth opportunity for the anabolic steroids industry. Rapid development of private healthcare infrastructure and endocrinology services across Asia Pacific and Latin America is increasing access to testosterone replacement therapy. The Organisation for Economic Co-operation and Development (OECD) reports that healthcare expenditure in middle-income economies is outpacing GDP growth by 2–3 percentage points annually, indicating rising affordability and service capacity. As diagnostic penetration improves, these regions could contribute over one-third of incremental global revenue by 2033, making geographic expansion a high-impact strategic lever. Companies that establish robust distribution and clinical partnerships are positioned to capture long-term market share in these high-growth markets.

Additional opportunity arises from specialized hormonal optimization services and veterinary applications. Precision medicine approaches, such as biomarker-based dosing and digital patient engagement, are transforming hormone therapy delivery, expanding premium clinical channels. The Food and Agriculture Organization (FAO) highlights increasing demand for veterinary performance enhancers in regulated animal healthcare systems, reflecting growth in animal hormone therapies as livestock production and animal health investment rise. The global veterinary hormones market continues to expand, offering stable revenue streams and diversification potential.

Category-wise Analysis

Compound Type Insights

Testosterone-based compounds are expected to remain dominant in 2026, accounting for nearly 48% of the anabolic steroids market revenue share due to broad clinical applicability and widespread regulatory approvals. These compounds are the first-line therapy for hypogonadism and are commonly prescribed across healthcare systems in North America and Europe. Availability in injectable, gel, and patch formulations further strengthens adoption and clinical flexibility. Over the past few years, the FDA has been approving next-generation long-acting injectable formulations, improving pharmacokinetic consistency and patient adherence. Healthcare providers in Canada and Germany have increasingly integrated these therapies into standard endocrine care protocols, reinforcing market leadership.

Oxandrolone is projected to expand at a 10.8% CAGR through 2033, driven by its favorable safety profile and growing use in muscle-wasting disorders and post-surgical recovery. Clinicians prefer it for its lower hepatotoxic risk, especially in hospital and rehabilitation settings. Hikma Pharmaceuticals plc launched enhanced oxandrolone formulations targeted at geriatric muscle support protocols. Government hospitals in Canada and the U.K.’s National Health Service (NHS) have begun pilot dosing studies to evaluate broader applicability. These developments reinforce clinician confidence and support a stronger growth trajectory for oxandrolone, increasing clinical exposure. Expanded research into pediatric and chronic care applications further supports its adoption.

Route of Administration Insights

Injectable anabolic steroids are projected to hold the largest revenue share at around 42% in 2026, primarily due to superior bioavailability, controlled dosing, and longer therapeutic duration. Long-acting injectables are widely used in chronic testosterone replacement therapy, particularly in North America and Europe, where physician preference favors predictable pharmacokinetics. For instance, Pfizer Inc. expanded its testosterone enanthate injectable distribution network across the U.S. and Canada, improving market access. Recent approvals by the EMA for advanced injectable testosterone esters have supported broader clinical adoption. The combination of regulatory support, physician familiarity, and insurance coverage continues to secure injectables as the leading route of administration.

Transdermal delivery systems, including gels and patches, are anticipated to be the fastest-growing route, projected to grow at a 10.5% CAGR from 2026 to 2033. The growth is driven by patient preference for non-invasive, convenient administration and steady hormone release profiles. Bayer AG received expanded regulatory approval in the EU for its testosterone gel, broadening market availability. Meanwhile, AbbVie Inc. introduced a novel patch system in the U.S. with enhanced skin adhesion technology. These innovations are expanding transdermal adoption and accelerating segment growth. These delivery systems are increasingly integrated into telemedicine and outpatient care programs, further supporting their rapid market growth and long-term potential.

End-Use Insights

Medical applications are likely to dominate the market, contributing approximately 55% to global revenue generation in 2026, driven by rising diagnoses of endocrine disorders, muscle degeneration, and chronic hormone deficiencies. Hospital pharmacies and specialty clinics remain the primary channels, with structured insurance reimbursement enhancing patient access. Cipla Ltd. partnered with several Indian state health agencies to expand testosterone replacement therapy programs in tertiary care centers, broadening clinical reach. The U.S. Centers for Medicare & Medicaid Services (CMS) updated reimbursement codes to support hormone optimization services, adding financial incentives for providers. These programs, combined with physician education on safe anabolic use, reinforce medical applications as the core market driver.

Non?medical use of anabolic steroids in bodybuilding, athletics, and recreational fitness is projected to be the fastest-growing end?use category, expected to expand at about 11% CAGR from 2026 to 2033. Growth is supported by increasing penetration of fitness culture and enhanced digital access to performance-enhancing products, particularly in emerging economies. Despite regulatory and ethical risks, consumer demand persists, especially through online channels and informal supply networks. Law enforcement agencies in the U.S. and U.K. have increased crackdowns on illicit anabolic distribution in gym ecosystems and e-commerce platforms. Even as enforcement tightens, robust participation in global fitness communities and rising competitive amateur sports contribute to ongoing volume growth. This demand dynamic supports above-average expansion relative to structured clinical usage.

Regional Insights

North America Anabolic Steroids Market Trends

North America is expected to hold approximately 38% of the anabolic steroids market share in 2026, led by the United States. The region’s advanced diagnostic infrastructure and high clinical awareness of hormonal disorders support robust demand for testosterone replacement and related therapies. Comprehensive insurance coverage and established endocrinology practice standards enhance patient access to regulated anabolic treatments. For instance, Merck & Co. expanded its endocrinology outreach programs in partnership with major U.S. health systems, increasing clinician engagement on hormone therapy protocols. The FDA continues to provide clear regulatory pathways that support innovation in delivery formats. Health systems and specialty clinics are increasingly integrating data-enabled patient monitoring, reinforcing North America’s leadership in revenue and clinical sophistication.

The collaborations between the U.S. Department of Veterans Affairs (VA) and private endocrine specialists have advanced screening and treatment programs for age-related testosterone deficiency among older adults. These initiatives have broadened patient pools and supported real-world evidence generation that informs clinical practice. Venture capital investment remains strong in digital health platforms focusing on hormonal health, accelerating the adoption of remote monitoring tools. Competitive dynamics in North America emphasize quality, compliance, and outcomes, driving sustained medical demand. Continued alignment of payer coverage and clinical guidelines is expected to fortify the region’s dominant market position through 2033.

Europe Anabolic Steroids Market Trends

Europe is a key regional market for anabolic steroids, led by Germany, the U.K., France, and Spain, driven by well-established endocrinology services and structured healthcare coverage. The European Medicines Agency harmonizes approvals across member states, reducing fragmentation and supporting cross?border commercialization of hormone therapies. Public healthcare systems ensure broad patient access to clinically supervised testosterone and related anabolic treatments. Regulatory focus on formulation safety and provider training reinforces consistent prescription practices. In the past year, France’s national health authority updated endocrine clinical guidelines, streamlining access to hormone-optimization programs across hospital networks.

Germany’s federal healthcare institutes have strengthened pharmacovigilance requirements for hormone therapies, boosting clinician confidence in long-term treatment protocols. The U.K.’s NHS introduced new patient education modules to improve adherence to approved anabolic regimens. Pharmaceutical manufacturers in Europe are emphasizing bioequivalent transdermal platforms and expanded dosing options to meet regional healthcare priorities. Cross-national endocrinology societies continue to advance evidence-based practice, consolidating Europe’s influential role in global anabolic steroid therapy.

Asia Pacific Anabolic Steroids Market Trends

Asia Pacific is projected to be the fastest-growing regional market for anabolic steroids, with a projected 10.8% CAGR during the 2026-2033 forecast period, driven by rising healthcare access, urbanization, and growing middle-class demand. The economies of China, Japan, India, and ASEAN are major contributors to this growth. Cost-efficient pharmaceutical manufacturing in India and China supports both domestic supply and export potential, while Japan leads in regulatory quality and clinical adoption of advanced hormonal therapies. In China, the National Health Commission’s Key Laboratory of Endocrinology has strengthened frameworks for early diagnosis and precision intervention in endocrine and metabolic diseases, enhancing clinical capacity for hormone management and related conditions.

Rapid expansion of private healthcare networks across ASEAN markets is broadening access to hormone therapies, particularly among middle-income urban populations. In the past year, the Ministry of Health and Family Welfare (MoHFW) in India expanded endocrinology training programs to target early diagnosis of testosterone deficiency in tertiary care centers, thereby increasing clinical demand. The proliferation of fitness culture in urban centers also contributes to rising demand for anabolic products in both clinical and non-clinical segments. As insurance penetration improves and regulatory pathways mature, Asia Pacific’s deepening healthcare infrastructure and rising patient awareness are expected to drive the region’s share of global anabolic steroids revenue to grow through 2033.

Competitive Landscape

The global anabolic steroids market is moderately consolidated, with leading pharmaceutical players such as Endo International plc, Pfizer Inc., AbbVie Inc., and Bayer AG collectively accounting for a significant share of global revenue. These established companies leverage their strong relationships with healthcare providers, regulatory expertise, and diversified product portfolios across injectables, gels, patches, and oral formulations. They continue to invest in R&D for advanced delivery systems, long-acting formulations, and digital patient adherence tools to maintain clinical and technological leadership.

Regional and niche manufacturers, including Hikma Pharmaceuticals and select Indian and Chinese pharmaceutical firms, focus on specific therapeutic indications, emerging markets, and cost-efficient production. Regulatory compliance, controlled substance laws, and complex clinical adoption requirements pose high entry barriers for new players. Market consolidation is expected to increase gradually as leading companies expand geographically through acquisitions, while smaller manufacturers and service providers collaborate through clinical and distribution partnerships to broaden market access and product reach.

Key Industry Developments

- In November 2025, Health Canada authorized KYZATREX® (testosterone undecanoate) CIII capsules, the first oral TRT in softgel form in Canada, offering a safer alternative that bypasses liver metabolism via the lymphatic system. Manufactured by Marius Pharmaceuticals, the therapy targets adult men with hypogonadism and is expected to be available through traditional providers and telehealth platforms in early 2026.

- In October 2025, Hims & Hers expanded its access to testosterone therapy through subscription-based telehealth models. By integrating virtual consultations, home lab testing, and recurring medication delivery, including FDA-approved oral and injectable options, they reduce geographic and social barriers, streamline patient care, and enhance adherence in a convenient, end-to-end digital ecosystem.

- In July 2025, CrazyBulk strengthened its position as a leading provider of natural, non-hormonal muscle-support supplements across the U.S. and globally. Responding to a 41% growth in consumer interest for legal hypertrophy aids, the company emphasizes FDA-registered, GMP-compliant manufacturing, third-party testing, and direct-to-consumer sales to ensure safety, transparency, and accessibility.

Companies Covered in Anabolic Steroids Market

- Pfizer Inc.

- Bayer AG

- AbbVie Inc.

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Industries

- Cipla Ltd.

- Hikma Pharmaceuticals

- Mylan

- Aspen Pharmacare

- Lupin Ltd.

- Zydus Lifesciences

- Ferring Pharmaceuticals

- Endo International

- Perrigo Company

Frequently Asked Questions

The global anabolic steroids market is projected to reach US$ 82.8 billion in 2026

Rising testosterone deficiency and muscle-wasting disorders, greater adoption of regulated hormone therapies, innovations in long-acting injectables and transdermal systems, and steady demand from fitness and performance use are driving the market.

The market is poised to witness a CAGR of 9.5% between 2026 and 2033

The expansion of regulated hormone therapy access in emerging markets, growth of personalized medicine and hormonal optimization clinics, and veterinary/adjacent therapeutic applications provide significant opportunities.

Endo International plc, Pfizer Inc., AbbVie Inc., Bayer AG, Hikma Pharmaceuticals, and Teva Pharmaceuticals are among the leading players in the market.