- Display Technologies

- Adaptive Optics Market

Adaptive Optics Market Size, Share, and Growth Forecast 2026 - 2033

Adaptive Optics Market by Component (Wavefront Sensor, Wavefront Modulator, Control System, Others), End-use (Ophthalmology, Microscopy, Laser Application, Manufacturing, Communications, Military & Défense, Others), and Regional Analysis for 2026 - 2033

Adaptive Optics Market Size and Trend Analysis

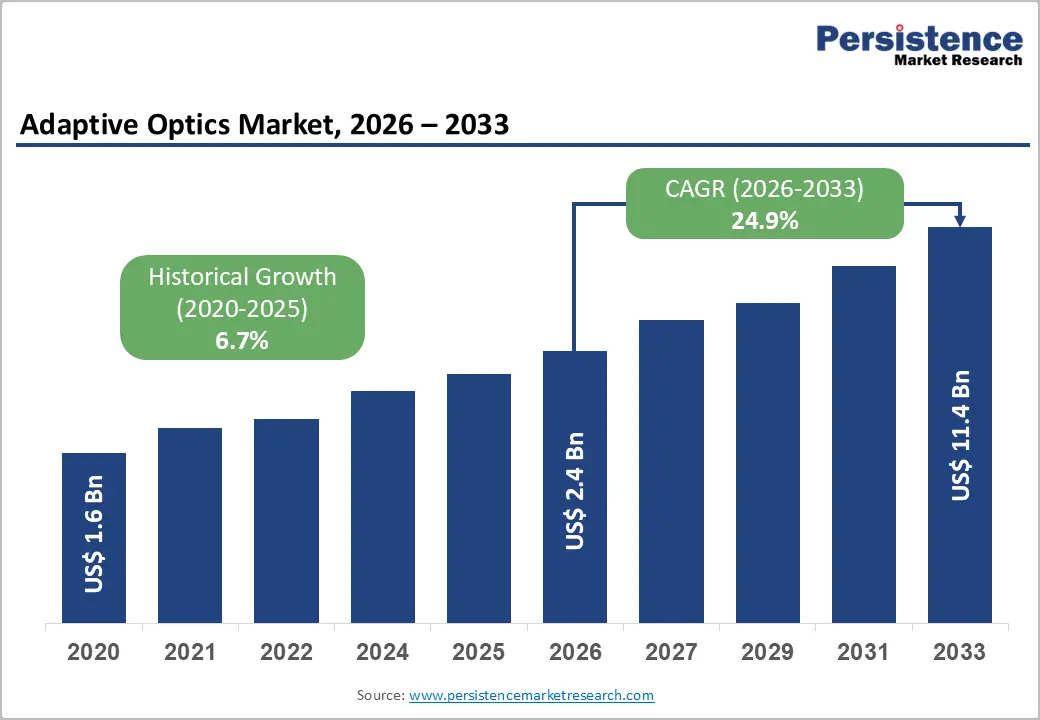

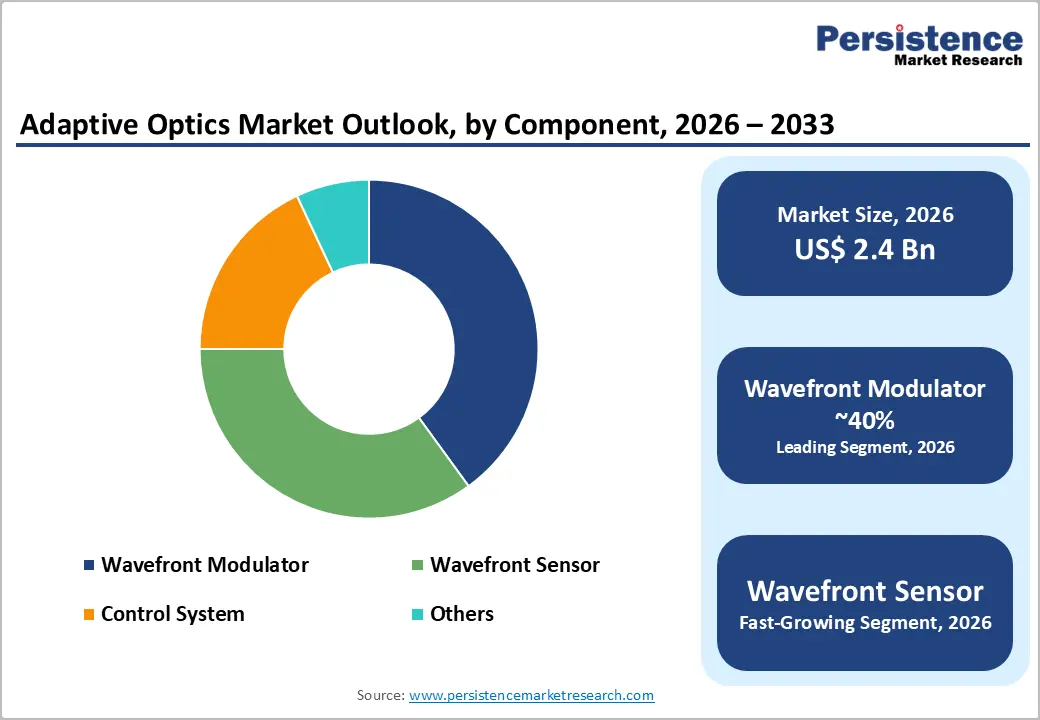

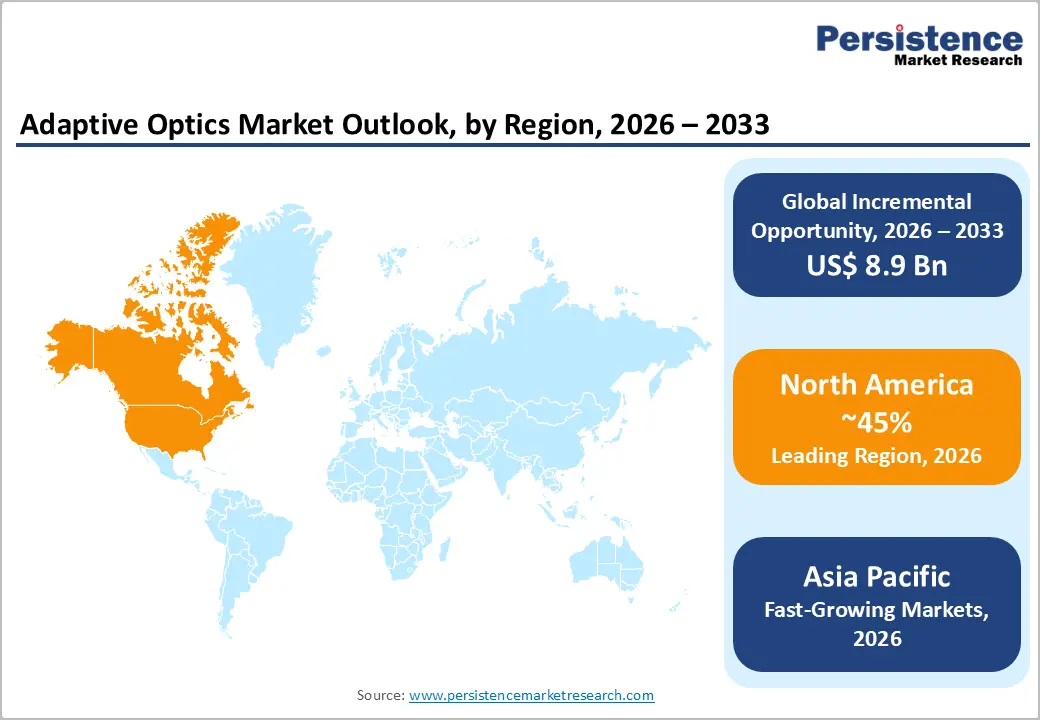

The global adaptive optics market size is expected to be valued at approximately US$ 2.4 Bn in 2026 and is projected to reach US$ 11.4 Bn by 2033, growing at an exceptional CAGR of 24.9% between 2026 and 2033.

The growth trajectory is driven by the convergence of free-space optical communications for satellite and 5G backhaul, the proliferation of adaptive optics in ophthalmic retinal imaging diagnostics, and unprecedented Defence investment in directed energy weapons. High-energy laser systems requiring precision wavefront correction are a central pillar of this demand expansion.

Key Industry Highlights:

- Leading Region - North America commands approximately 44% of the global adaptive optics market in 2025. This position is anchored by the U.S. Department of Defense’s directed energy program investments exceeding USD 1 billion annually and DARPA free-space optical communications programs.

- Fast-Growing Market - Asia Pacific is projected to register substantial market growth by 2033. China is likely to witness a leading CAGR driven by the Defence directed energy and satellite optical communications program scaling.

- Leading Component - Wavefront modulators lead the component segment with approximately 38% market share in 2025. They are entrenched as the most technically complex and highest-cost adaptive optics component in any system configuration.

- Fastest Growing Application - The laser application is the fastest-growing end-use category. Industrial laser material processing precision requirements, semiconductor photolithography beam quality, and free-space optical communications are each creating new adaptive optics integration opportunities.

- Opportunity: Ophthalmology AO-OCT clinical adoption represents the market’s largest long-term volume opportunity. The WHO documents over one billion people globally with preventable vision impairment, creating a massive potential patient population for advanced retinal diagnostics.

DRO Analysis

Drivers - Défense Directed Energy Weapons and Military Laser System Programs Are Creating the Market's Highest-Value Procurement Demand for Advanced Adaptive Optics

The United States and allied nation Defence establishments’ accelerating investment in high-energy laser (HEL) and directed energy weapon (DEW) systems represents the single most consequential near-term demand driver for advanced adaptive optics. Deformable mirror wavefront modulators, Shack-Hartmann wavefront sensors, and high-bandwidth control systems are non-negotiable enabling components for operational DEW platforms.

The U.S. Army awarded the High-Energy Laser Tactical Vehicle Demonstrator (HEL TVD) program to Raytheon and has multiple subsequent directed energy programs in active procurement. Each program requires high-speed adaptive optics control systems operating at kilohertz-range correction bandwidths to compensate for atmospheric turbulence between laser systems and aerial targets.

Free-Space Optical Communications for Satellite Constellations Is Opening a Structurally New and Rapidly Growing Adaptive Optics Application Domain

The proliferation of low-earth-orbit (LEO) satellite mega-constellations including SpaceX Starlink, Amazon Project Kuiper, and ESA programs is driving rapid adoption of free-space optical (FSO) inter-satellite links. These optical communications architectures require adaptive optics systems to compensate for atmospheric turbulence and beam distortion across atmospheric propagation paths.

SpaceX has publicly confirmed deployment of optical inter-satellite links in its Starlink V2 Mini constellation. Amazon’s Project Kuiper specifications include ISL optical communications as a key architectural feature, and these programs collectively require thousands of optical terminal units per constellation with integrated wavefront sensing and correction capability.

This application domain is structurally new it did not exist as a commercial adaptive optics procurement category a decade ago. Its rapid scaling from research prototype to production procurement status creates a parallel demand channel alongside the established Defence and scientific instrument markets.

Market Restraints

Extremely High System Cost Restricts Adoption to Institutional Buyers

Complete adaptive optics systems comprising a wavefront sensor, deformable mirror wavefront modulator, real-time control computer, and optical bench integration carry price points of USD 50,000-500,000+ for scientific and medical research configurations. Military-grade high-energy laser wavefront correction systems rise to USD 1-10 million+.

This cost profile restricts the addressable market to national Defence agencies, premium academic research institutions, high-technology manufacturers, and large ophthalmology research centres. While these buyers generate high per-transaction revenue, the inherently limited account density constrains market breadth compared with commodity photonics component markets.

Manufacturing Complexity Creates Supply Chain Bottlenecks

High-performance Shack-Hartmann wavefront sensors with large lenslet array counts and deformable mirrors with hundreds to thousands of actuators require specialized fabrication processes. These include precision micro-optics lenslet fabrication, piezoelectric or MEMS actuator manufacturing, and integrated circuit control electronics produced by a small number of specialist manufacturers globally.

This supply concentration creates long lead times during demand surge periods, a structural vulnerability that Defence procurement programs and satellite constellation build-outs have already begun to expose. The National Academies of Sciences, Engineering, and Medicine has identified the optical component manufacturing workforce and supply chain depth as a systemic U.S. photonics industrial vulnerability.

Opportunities - Ophthalmology Retinal Imaging Transitioning to Clinical Deployment

Adaptive optics ophthalmology, encompassing adaptive optics scanning laser ophthalmoscopes (AOSLO) and adaptive optics optical coherence tomography (AO-OCT), is transitioning from specialized research laboratory instrumentation toward clinically deployed diagnostic tools. Technology maturation, component cost reduction, and accumulating clinical evidence are combining to create a compelling commercial opportunity.

The National Eye Institute (NEI) at the U.S. NIH has funded multiple adaptive optics retinal imaging research programs and published clinical efficacy evidence supporting the technology’s regulatory pathway. An FDA 510(k) medical device clearance milestone will unlock hospital and clinic procurement channels representing orders of magnitude larger addressable markets than the current research institution installed base.

Ground Station Infrastructure for Satellite Optical Communications

The ground station and optical terminal infrastructure required to support LEO satellite optical communications networks represents a structurally new and rapidly expanding addressable market. Each ground optical terminal serving a LEO FSO link requires atmospheric turbulence compensation for reliable high-data-rate (10-200 Gbps) optical link performance.

Adaptive optics wavefront correction systems provide this compensation at correction bandwidths matched to atmospheric temporal coherence scales. This technical requirement is non-negotiable for commercial optical link performance without wavefront correction; data-rate reliability and availability targets cannot be met in real-world atmospheric conditions.

This market is moving from research prototype to production procurement status simultaneously with the satellite constellation build-out timelines of SpaceX, Amazon, and Telesat. First-mover suppliers capable of delivering production-qualified optical terminal wavefront correction subsystems are positioned to capture long-term supply agreements across multiple constellation programs.

Category-wise Analysis

Component Insights

Wavefront modulators, deformable mirrors, and spatial light modulators lead the component segment with approximately 38% market share in 2026. They are both the most technically complex and the highest unit-cost component in any adaptive optics system, determining the system’s ultimate wavefront correction bandwidth and actuator stroke range.

Piezoelectric and MEMS deformable mirrors with actuator counts ranging from 37 to over 2,000 are fabricated by a small number of specialized manufacturers, including Boston Micromachines Corporation, Alpao SAS, and Imagine Optics. This concentration of specialized production capability sustains component pricing power despite growing demand from multiple application verticals.

End-user Insights

Military & Defence leads the end-use segment with approximately 35% market share in 2026, anchored by sustained U.S. and allied nation Defence investment in directed energy weapons, high-power laser beam control, and ground-to-space optical communications. Each of these applications requires precision wavefront correction at performance specifications representing the most technically demanding and highest-value adaptive optics procurement events in the market.

Defence procurement contracts for HEL and DEW adaptive optics systems generate per-system revenues of USD 1-10 million+, sustaining the segment’s revenue leadership despite lower unit volume than ophthalmology and laser application segments. The non-discretionary nature of Defence program funding further insulates this segment from economic cycle volatility.

Regional Analysis

North America Adaptive Optics Market Trends & Analysis

North America is the world’s largest adaptive optics market by revenue. It is anchored by the United States’ unmatched Defence directed energy program investment, with the U.S. Air Force Research Laboratory (AFRL), U.S. Army Research Laboratory (ARL), and DARPA collectively operating the world’s most well-funded adaptive optics research and procurement programs.

The concentration of world-class astronomy observatories, photonics research universities, and ophthalmic research centres further drives scientific application demand. The National Science Foundation (NSF) and DOE Office of Science jointly fund major ground-based telescope adaptive optics upgrades that sustain premium scientific instrument procurement.

U.S. Adaptive Optics Market Size

The United States commands approximately 84% of the North American adaptive optics market, as the world’s dominant government and commercial adaptive optics buyer and technology developer. The U.S. market grows at approximately 23.8% CAGR through 2033, reflecting exceptional growth driven by DoD directed energy program scaling and DARPA free-space optical communications investment.

Europe Adaptive Optics Market Trends, Drivers, & Insights

Europe is the world’s most scientifically established adaptive optics market, where the technology was originally developed and first deployed at major ground-based astronomical observatories including the Very Large Telescope (VLT) operated by the European Southern Observatory (ESO). This research heritage has seeded a dense European adaptive optics component manufacturing and system integration ecosystem.

The European Space Agency (ESA) is actively developing optical inter-satellite link technology for its future satellite communication infrastructure. The European Defence Fund (EDF) is funding directed energy weapon programs across EU member states, adding a growing Defence procurement layer to the region’s historically science-dominated demand profile.

Germany Adaptive Optics Market Size

Germany holds approximately 22% of the European adaptive optics market. Its position is anchored by a world-class precision optics manufacturing industry including Carl Zeiss AG, Jenoptik AG, and TOPTICA Photonics and significant contributions to European laser and photonics research through institutions including the Max Planck Institute and Fraunhofer Institute for Laser Technology (ILT).

UK Adaptive Optics Market Size

The United Kingdom represents approximately 17% of the European adaptive optics market. Demand is driven by its world-leading Defence photonics sector including BAE Systems directed energy programs and QinetiQ adaptive optics research and the UK’s significant astronomy heritage. The UK's Defence Science and Technology Laboratory (DSTL) is a major adaptive optics research funder. The UK market grows at approximately 24.5% CAGR through 2033.

France Adaptive Optics Market Size

France accounts for approximately 15% of the European adaptive optics market and is home to world-leading adaptive optics companies, including Alpao SAS (deformable mirrors) and Imagine Optic (wavefront sensors and correction systems). The Office national d’études et de recherches aérospatiales (ONERA) is France’s leading adaptive optics research institute. France's market grows at approximately 24.2% CAGR through 2033.

Asia Pacific Adaptive Optics Market Drivers & Analysis

Asia Pacific is the fastest-growing regional adaptive optics market. Growth is propelled by China’s rapidly expanding Defence photonics and free-space optical communications programs, Japan’s world-class astronomical instrumentation industry, and the region’s progressive investment in ophthalmic diagnostic technology driven by its large and aging population demographic.

China is the region’s dominant adaptive optics buyer. The Chinese Academy of Sciences (CAS) and People’s Liberation Army (PLA) research institutes operate significant adaptive optics programs spanning astronomy, directed energy, and satellite optical communications, contributing to China’s rapidly growing domestic demand for both indigenous and imported components.

China Adaptive Optics Market Size

China holds approximately 40% of the Asia Pacific adaptive optics market. Significant Defence and national security program investment in directed energy and free-space optical satellite communications drives this position, combined with China’s active large-aperture telescope programs at facilities including the Chinese Large Solar Telescope (CLST).

India Adaptive Optics Market Size

India accounts for approximately 12% of the Asia Pacific adaptive optics market and is among the region’s fastest growing at approximately 26.8% CAGR through 2033. India’s Defence Research and Development Organisation (DRDO) operates directed energy research programs, and ISRO is developing satellite optical communications capabilities.

Japan Adaptive Optics Market Size

Japan represents approximately 20% of the Asia Pacific adaptive optics market. World-class adaptive optics astronomy programs at the Subaru Telescope on Mauna Kea, where the National Astronomical Observatory of Japan (NAOJ) has deployed advanced laser guide star adaptive optics systems, establish Japan’s scientific credentials. Japan's segment grows at approximately 24.1% CAGR through 2033.

Competitive Landscape

The global adaptive optics market is highly fragmented at the component level, with deformable mirror, wavefront sensor, and control system manufacturing dispersed among dozens of specialist companies globally. However, it consolidates significantly at the system integration level, where a small number of Defence prime contractors and precision optics system integrators command the highest-value procurement contracts.

Northrop Grumman, L3Harris Technologies, and Raytheon (RTX) dominate U.S. Defence system integration for high-energy laser and directed energy applications. European companies, including CILAS (France), Alpao (France), and Imagine Optic (France) lead wavefront correction component supply, reflecting Europe’s deep scientific heritage in adaptive optics technology development.

Key Developments

- In June 2025, the European Southern Observatory procures adaptive optics wavefront sensing cameras for the Extremely Large Telescope, representing multi-million-dollar contracts for suppliers capable of producing advanced optical systems essential for next-generation astronomical observations.

- In May 2025, MKS Instruments reported Q1 2025 revenue of USD 936 million, driven by semiconductor and electronics packaging market growth, with the company's World Class Optics initiative addressing complex chip architectures requiring sub-nanometre precision adaptive optics solutions.

Adaptive Optics Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.6 Bn |

| Current Market Value (2026) | US$ 2.4 Bn |

| Projected Market Value (2033) | US$ 11.4 Bn |

| CAGR (2026 - 2033) | 24.9% |

| Leading Region | North America, 45% share |

| Dominant Application | Wavefront Modulators, 38% share |

| Top-ranking Product | Military & Défense, 35% |

| Incremental Opportunity | US$ 8.9 Bn |

Companies Covered in Adaptive Optics Market

- Northrop Grumman Corporation

- L3Harris Technologies

- Raytheon Technologies (RTX)

- Alpao SAS

- Imagine Optic

- Boston Micromachines Corporation

- CILAS (ArianeGroup)

- Thorlabs Inc.

- II-VI Incorporated (Coherent Corp.)

- Iris AO Inc.

- Xinetics Inc.

- Active Optical Systems

- UFI Filters

Frequently Asked Questions

The global adaptive optics market is valued at approximately US$ 2.4 billion in 2026. It is projected to reach US$ 11.4 billion by 2033, expanding at a CAGR of 24.9% one of the highest forecast growth rates in the photonics sector.

The primary demand drivers are U.S. DoD directed energy weapon program investment exceeding USD 1 billion annually, and SpaceX Starlink and Amazon Project Kuiper free-space optical inter-satellite link deployment creating new adaptive optics procurement demand at satellite constellation scale. NIH/NEI funding accelerating AO-OCT ophthalmology clinical diagnostic technology toward FDA 510(k) clearance is a third structural driver.

Wavefront Modulators (deformable mirrors and spatial light modulators) lead the component segment with approximately 38% market share in 2025. Their dominance reflects their position as the most complex and highest-unit-value component in any adaptive optics system.

North America leads the global adaptive optics market with approximately 44% revenue share in 2025. The United States commands approximately 84% of the North American market, underpinned by AFRL, ARL, and DARPA adaptive optics research programs and DoD directed energy weapon procurement.