- Display Technologies

- Broadcast Equipment Market

Broadcast Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Broadcast Equipment Market by Product Type (Dish Antennas, Switches, Video Servers, Encoders, Transmitters and Repeaters, Others), Technology (Analog Broadcasting, Digital Broadcasting), Application (Television, Radio), and Regional Analysis for 2026 - 2033

Broadcast Equipment Market Size and Trend Analysis

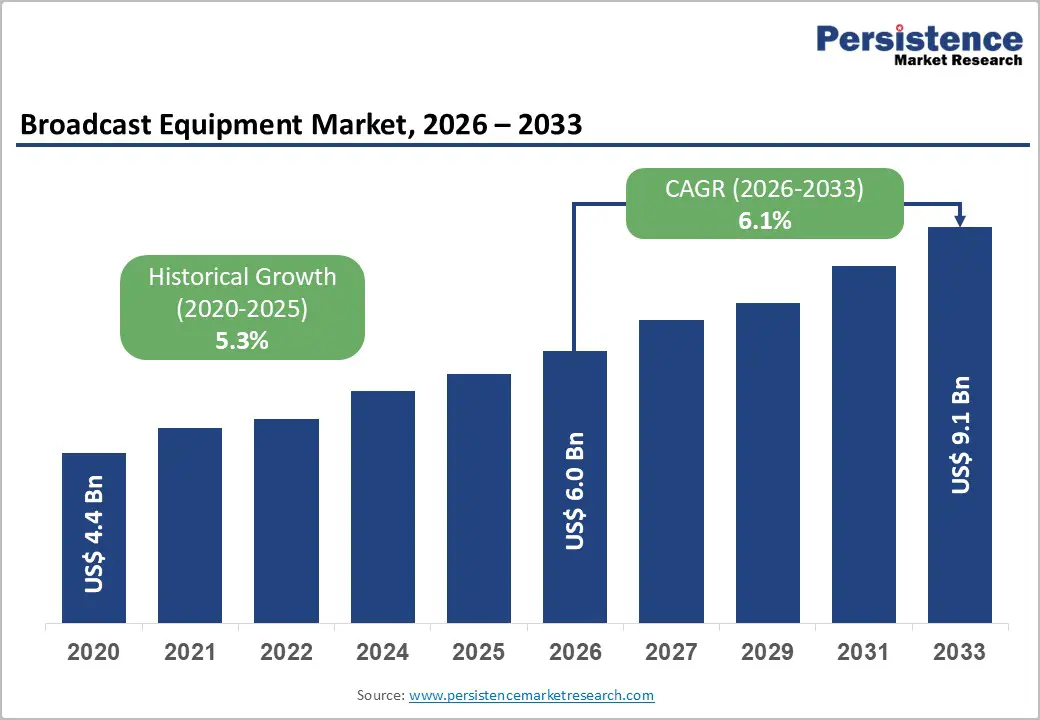

The global broadcast equipment market size is expected to be valued at US$ 6.0 billion in 2026 and is projected to reach US$ 9.1 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

The global transition from analog to digital broadcasting infrastructure, rapid adoption of IP-based broadcast workflows and cloud production technologies, and sustained government investment in digital broadcast switchover programs across Asia Pacific, Africa, and Latin America enables broader growth. The market grew from US$ 4.4 billion in 2020 at a historical CAGR of 5.3%, supported by 4K/8K UHD broadcast infrastructure investment by major broadcasters.

Key Industry Highlights:

- Leading Region - North America leads the global broadcast equipment market, driven by active ATSC 3.0 NextGen TV transmitter deployments across 60+ U.S. markets, FCC-coordinated spectrum transition programs, and major U.S. broadcaster capital expenditure cycles for IP studio and cloud production infrastructure upgrades.

- Fastest Growing Region - Asia Pacific is the fastest growing region through 2026 - 2033, with India at 8.4% CAGR driven by Prasar Bharati's 1,400+ transmitter network, China's NRTA-coordinated 4K UHD broadcast programs, and active DSO completions across Southeast Asia funded by ITU and AfDB programs.

- Dominant Segment - Digital broadcasting holds 74% technology market share in 2025, dominating through DVB-T2 availability in 90+ countries per DVB Project data, ATSC 3.0 NextGen TV rollout in 60+ U.S. markets, and spectrum efficiency enabling 6-10 digital channels per analog channel bandwidth.

- Fastest Growing Segment - IP-based broadcast equipment under SMPTE ST 2110 standard is the fastest growing product innovation, driven by BBC, NBC Universal, and Sky IP studio transitions, software-defined switching replacing dedicated hardware, and cloud-native video server and encoder platforms from Harmonic and Ericsson.

- Key Opportunity - ATSC 3.0 NextGen TV deployments across U.S. markets and DVB-T2 transitions in Italy, Sweden, and Germany create policy-mandated, multi-year transmitter and encoder equipment procurement waves for broadcast equipment manufacturers through 2033.

DRO Analysis

Drivers - Global Analog-to-Digital Broadcast Switchover Programs Driving Equipment Replacement Cycles

The worldwide transition from analog to digital broadcast infrastructure represents the single most significant structural investment catalyst in the broadcast equipment market, generating substantial transmitter, encoder, and antenna equipment replacement demand globally. The International Telecommunication Union (ITU) coordinated the Digital Switchover (DSO) process globally, with the Geneva 2006 Agreement (GE06) mandating completion of UHF/VHF analog switch-off across 120+ ITU member states.

Many African, Asian, and Latin American nations have ongoing DSO implementation programs requiring substantial broadcast transmitter and tower infrastructure investment. In the U.S., the ATSC 3.0 (NextGen TV) rollout coordinated by the Consumer Technology Association (CTA)is driving new-generation transmitter and encoder equipment deployments across commercial broadcast stations nationwide, creating a multi-year replacement upgrade cycle for U.S. broadcaster capital expenditure programs.

IP-Based Broadcast Workflows and Cloud Production Adoption Expanding Equipment Addressable Market

The broadcast industry's accelerating transition from traditional SDI-based (Serial Digital Interface) infrastructure to IP-based broadcast workflows governed by SMPTE ST 2110 standards and cloud production environments is fundamentally expanding the broadcast equipment addressable market by introducing new categories of software-defined and virtualized broadcast infrastructure.

The Society of Motion Picture and Television Engineers (SMPTE) reports that SMPTE ST 2110 adoption has grown significantly among major broadcasters globally, enabling flexible, scalable IP video production. Major broadcasters including BBC, NBC Universal, and Sky have deployed IP-based broadcast facilities that require new-generation IP encoders, software-defined switches, and cloud-connected video servers expanding total equipment procurement budgets while shifting the technology mix toward higher-value, software-enabled hardware platforms.

Restraints - High Capital Expenditure and Long Replacement Cycles in Broadcast Infrastructure

Broadcast equipment particularly transmitters, satellite dish antennas, and broadcast video servers represent substantial capital investment with typical operational lifetimes of 10-20 years. This long replacement cycle and high upfront capital requirement constrains annual procurement volumes and limits market growth in periods between technology generation transitions.

For emerging market broadcasters with constrained public budgets and limited access to equipment financing, the capital intensity of digital broadcast infrastructure investment represents a persistent adoption barrier that slows DSO completion timelines.

Intensifying Competition from OTT Streaming Platforms Pressuring Traditional Broadcaster Revenue

The rapid global growth of OTT (Over-the-Top) streaming platforms including Netflix, Amazon Prime Video, Disney+, and YouTube is diverting advertising revenue and viewership from traditional linear broadcast networks, constraining broadcaster profitability and reducing capital available for broadcast equipment investment.

The Reuters Institute Digital News Report documents consistent multi-year declines in linear TV viewership across mature markets, with OTT platform audiences growing inversely. This revenue pressure directly reduces broadcaster capital expenditure flexibility, creating procurement headwinds for high-value broadcast equipment refresh cycles in North America and Western Europe.

Opportunities - ATSC 3.0 NextGen TV and DVB-T2 Deployment Creating Multi-Year Equipment Upgrade Cycles

The commercial rollout of next-generation broadcast standards particularly ATSC 3.0 (NextGen TV) in the United States and DVB-T2 in Europe, Asia, and Latin Americas creating structured, multi-year equipment procurement cycles for advanced transmitters, encoders, and broadcast servers that support 4K HDR, immersive audio, and interactive services. The CTA's NextGen TV tracker documents over 60 U.S. markets with active ATSC 3.0 broadcasts, with continued station-by-station rollouts requiring transmitter and encoding infrastructure upgrades.

In Europe, DVB-T2 adoption across Italy, Sweden, and Germany is driving digital transmitter replacement programs. The combination of technology generation transition demand with regulatory digital switchover mandates across emerging markets creates a highly predictable, policy-driven equipment upgrade demand wave that equipment manufacturers can plan capacity and R&D investments around through 2033.

Developing Market Digital Broadcast Infrastructure Investment: Structural Greenfield Opportunity

Sub-Saharan Africa, South and Southeast Asia, and Latin America represent the largest untapped greenfield opportunity for broadcast equipment manufacturers, as dozens of nations complete their analog switch-off programs requiring full digital transmitter and infrastructure deployment. The ITU's Digital Broadcasting Transition Fund and development organization support programs are channelling funding into DSO infrastructure investment across the world's least-connected broadcast markets.

India's Prasar Bharati national broadcaster has been expanding DTT (Direct-to-Home Terrestrial) coverage under Door darshan Free Dish using MPEG-4/DVB-S2 infrastructure requiring ongoing equipment investment. Africa's ECOWAS and SADC regional DSO coordination programs, supported by the African Development Bank (AfDB), are funding transmitter and broadcast station equipment procurement across multiple countries simultaneously, creating concentrated demand opportunities for broadcast equipment suppliers with regional distribution capabilities.

Category-wise Analysis

Product Type Insights

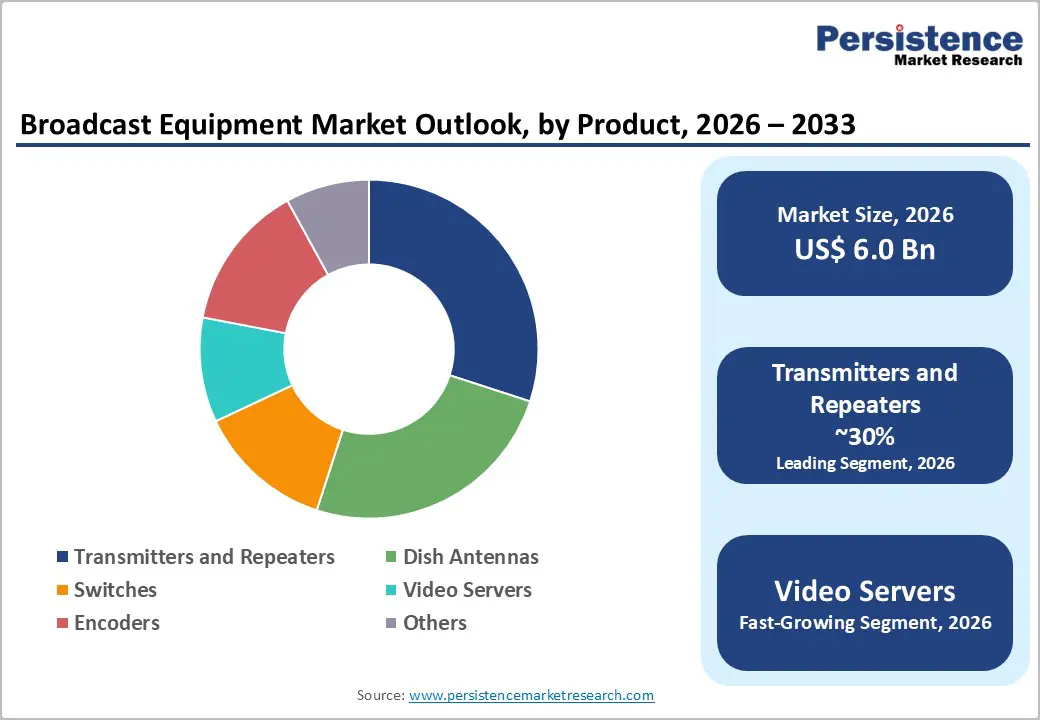

Transmitters and Repeaters represent the leading product type segment in the broadcast equipment market, accounting for approximately 28% market share in 2025. Transmitters are the core infrastructure component of every broadcast network converting electrical broadcast signals into radio frequency signals for over-the-air transmission and their replacement is mandatory in every analog-to-digital switchover program globally.

The ITU digitization agenda has driven consistent demand for solid-state digital TV transmitters compliant with DVB-T2, ATSC 3.0, and ISDB-T standards. Repeater networks extend broadcast coverage into mountainous terrain, urban canyons, and low-density rural areas where direct transmitter coverage is insufficient. Leading transmitter manufacturers including Rohde & Schwarz, Nautel, and GatesAir serve broadcast networks across all major markets with both primary transmitter and gap-filler repeater product lines for full digital coverage deployment.

Technology Insights

Digital Broadcasting is the dominant technology segment, accounting for approximately 74% market share in 2025 and continuing to gain share from analog as DSO programs complete globally. Digital broadcast standards including DVB-T2, ATSC 3.0, ISDB-T, and DAB+ (for digital radio) deliver significantly greater spectrum efficiency enabling 6-10 TV channels in the same bandwidth occupied by a single analog channel and support advanced services including 4K UHD, HDR, interactive data services, and mobile reception.

The European Broadcasting Union (EBU) and DVB Project have documented consistent growth in DVB-T2 deployments globally, with the standard now live in over 90 countries. As remaining analog markets complete switchover programs particularly across Sub-Saharan Africa and parts of Asia the digital technology segment will approach near-universal market share, sustaining new equipment procurement at high levels through the forecast period.

Application Insights

Television broadcast applications represent the dominant Application segment, accounting for approximately 68% share in 2026. Television broadcasting requires the broadest and most capital-intensive equipment portfolio encompassing transmitters, video servers, encoders, satellite uplinks, dish antennas, and signal distribution switching infrastructure generating per-network equipment value significantly higher than radio broadcast networks.

The International Telecommunication Union (ITU) estimates that global television penetration reaches over 1.8 billion households, representing the world's most widely distributed broadcast medium. Major broadcast equipment procurement programs are concentrated in television infrastructure from public service broadcaster (BBC, NHK, ARD) capital projects to commercial network digital upgrades and emerging market DSO infrastructure collectively sustaining television's commanding application dominance.

Regional Analysis

North America Broadcast Equipment Market Trends & Analysis

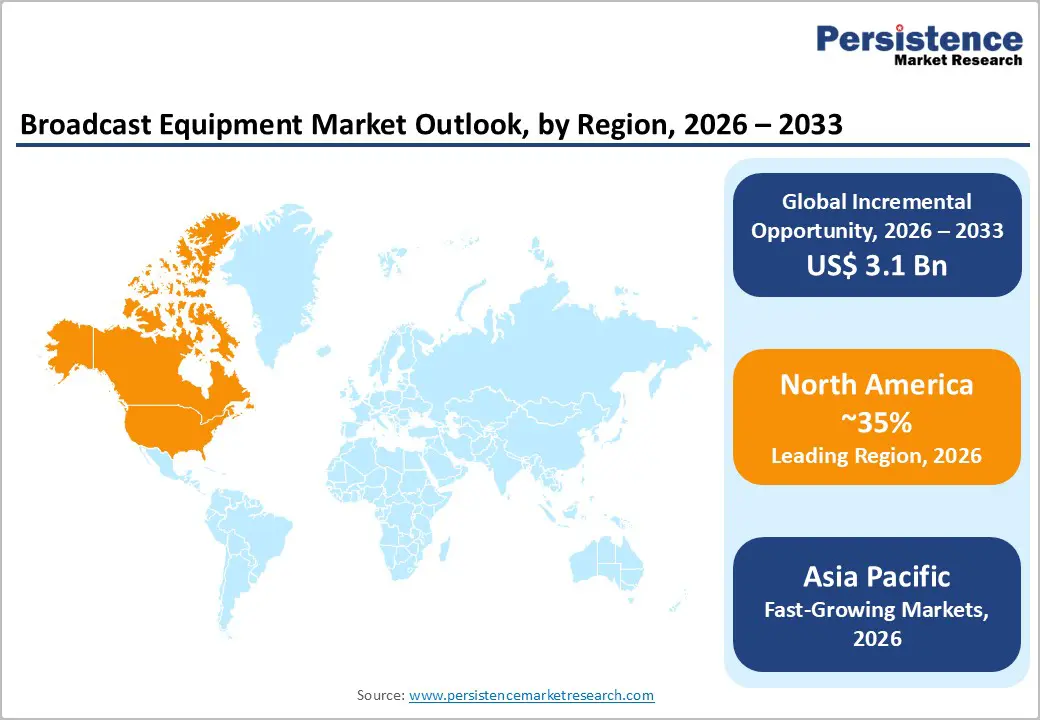

North America is the most technically advanced broadcast equipment market globally, characterized by active ATSC 3.0 NextGen TV rollout across 60+ U.S. markets, growing IP-based studio infrastructure transitions, and OTT platform investment in broadcast-quality production equipment. The FCC's spectrum reallocation processes and ATSC 3.0 transition framework are driving multi-year broadcast transmitter and encoder investment cycles across U.S. commercial broadcasters, while Canada and Mexico continue their respective digital switchover infrastructure programs.

U.S. Broadcast Equipment Market Size

The United States accounts for approximately 82% of North American broadcast equipment market revenue in 2025. The U.S. market is anchored by active ATSC 3.0 transmitter deployments, with the Consumer Technology Association (CTA) documenting over 60 markets broadcasting NextGen TV signals. Major U.S. broadcast groups including Nexstar, Sinclair Broadcast Group, and Gray Television are active ATSC 3.0 equipment buyers.

Europe Broadcast Equipment Market Trends, Drivers & Insights

Europe is a mature broadcast equipment market shaped by progressive DVB-T2 adoption, DAB+ digital radio rollout, and public broadcaster capital investment programs in UHD production infrastructure. The European Broadcasting Union (EBU) actively coordinates technical standards and best practices across European public broadcasters, creating aligned equipment procurement decisions.

Germany Broadcast Equipment Market Size

Germany holds approximately 22% of the European broadcast equipment market in 2025. Germany's complex broadcast landscape with public broadcasters ARD and ZDF plus extensive private channel networks sustains significant equipment procurement. Germany completed DVB-T2 switchover, with ongoing UHD upgrade and IP studio transition programs driving investment.

U.K. Broadcast Equipment Market Size

The United Kingdom represents approximately 19% of the European broadcast equipment market in 2025. The BBC and ITV are among the most technologically advanced broadcasters globally, with BBC's ongoing IP studio and cloud production infrastructure programs generating consistent premium equipment procurement. The UK's active DAB+ digital radio network and Freeview DVB-T2 platform sustain terrestrial broadcast transmitter network investment. UK CAGR is projected at approximately 5.9% through 2033.

France Broadcast Equipment Market Size

France accounts for approximately 14% of European broadcast equipment market revenue in 2025. France Televisions and Radio France represent major public broadcaster equipment buyers, with DVB-T2 infrastructure and UHD production equipment upgrades as primary investment categories. France's TNT platform operates an extensive DVB-T2 transmitter network requiring ongoing maintenance and upgrade investment.

Asia Pacific Broadcast Equipment Market Drivers & Analysis

Asia Pacific is the fastest growing broadcast equipment market, driven by ongoing digital switchover programs across India, Southeast Asia, and Oceania, China's continued broadcast infrastructure investment including 4K UHD upgrades, and Japan's advanced ISDB-T and ISDB-S broadcast infrastructure modernization. China accounts for approximately 35% of Asia Pacific broadcast equipment demand, with domestic broadcasters including CCTV/CMG and provincial TV networks investing in UHD and IP-based production infrastructure.

China Broadcast Equipment Market Size

China holds approximately 35% of Asia Pacific broadcast equipment revenue in 2025. China's SARFT/NRTA (National Radio and Television Administration) coordinates large-scale broadcast infrastructure investment programs, including DTMB (Digital Terrestrial Multimedia Broadcast) network expansion and 4K UHD satellite broadcast infrastructure for the CMG national broadcaster.

India Broadcast Equipment Market Size

India represents approximately 16% of Asia Pacific broadcast equipment revenue in 2025. Prasar Bharati's Doordarshan national broadcast network expansion covering MPEG-4/DVB-S2 satellite infrastructure and terrestrial transmitter networks across 1,400+ transmitters generate substantial equipment procurement. India's growing private broadcast sector with hundreds of licensed TV channels additionally sustains encoder and satellite uplink equipment demand.

Japan Broadcast Equipment Market Size

Japan contributes approximately 13% of Asia Pacific broadcast equipment revenue in 2025. Japan maintains one of the world's most advanced digital broadcast infrastructures, with NHK pioneering 8K Super Hi-Vision broadcast technology through its BS8K/CS8K satellite platform. Japan's ongoing 8K infrastructure rollout and ISDB-T next-generation upgrade programs generate consistent premium equipment procurement. Japan's broadcast technology export capabilities through Sony, Panasonic, and NEC reinforce its position as both a key demand and supply market.

Competitive Landscape

The global broadcast equipment market exhibits a moderately consolidated competitive structure, with a small number of technology-intensive multinationals including Harmonic Inc., Ericsson, Grass Valley, and Cisco Systems competing alongside specialized equipment manufacturers serving specific product niches. Key competitive differentiators include standards compliance breadth (ATSC 3.0, DVB-T2, ISDB-T), IP workflow integration, cloud production platform capabilities, and R&D investment in next-generation compression codecs (HEVC/H.265, VVC/H.266).

Emerging trends include software-defined broadcast infrastructure replacing dedicated hardware, cloud-native broadcast playout and production services, and AI-powered broadcast automation.

Key Market Developments

- In September 2025, Sony Group Corporation allocated USD 200 million to build next-generation AI broadcast production systems that combine machine-learning-based content creation with live quality optimization, helping operators cut costs while sustaining premium output across every platform.

- In August 2025, Cisco Systems finalized its USD 75 million purchase of cloud-native specialist Stream Labs Technologies, adding edge computing and AI-enhanced video processing to reinforce its leadership in IP-centric broadcast infrastructure.

Companies Covered in Broadcast Equipment Market

- Harmonic Inc.

- Telefonaktiebolaget LM Ericsson

- Grass Valley

- Cisco Systems Inc.

- Datum Systems

- OMB Broadcast

- EVS Broadcast Equipment SA

- Clyde Broadcast

- Global Invacom Group Limited

- Sencore

- Rohde & Schwarz

- GatesAir

- Nautel Ltd.

- Sony Corporation

- Panasonic Holdings

Frequently Asked Questions

The global broadcast equipment market is projected to reach US$ 9.1 billion by 2033, growing from an estimated US$ 6.0 billion in 2026 at a CAGR of 6.1%. Growth is driven by global analog-to-digital broadcast switchover programs, ATSC 3.0 NextGen TV deployment in the U.S., DVB-T2 rollout in Europe and Asia, and IP-based broadcast workflow transitions at major broadcasters globally.

Primary drivers include the ITU-coordinated Digital Switchover program mandating analog switch-off across 120+ member states, with active programs in Africa, Asia, and Latin America requiring full digital transmitter deployment. The ATSC 3.0 NextGen TV rollout in over 60 U.S. markets per CTA data, and DVB-T2 adoption in 90+ countries per DVB Project data, are driving structured multi-year equipment procurement cycles.

Digital broadcasting leads with approximately 74% market share in 2025, driven by DVB-T2 deployment in 90+ countries, ATSC 3.0 NextGen TV rollout across 60+ U.S. markets, and ISDB-T adoption across Brazil, Japan, and Southeast Asia. Digital standards' spectrum efficiency enabling 6-10 channels per analog channel bandwidth combined with support for 4K HDR and interactive services makes digital broadcasting the mandated upgrade path for virtually all remaining analog markets completing switchover programs through 2033.

North America leads, with the U.S. accounting for approximately 82% of regional revenue in 2025 through active ATSC 3.0 transmitter and encoder deployments, major broadcaster IP studio transitions, and FCC-coordinated spectrum management programs.

Key companies include Harmonic Inc., Telefonaktiebolaget LM Ericsson, Grass Valley, Cisco Systems Inc., EVS Broadcast Equipment SA, Rohde & Schwarz, GatesAir, Nautel Ltd., Sony Corporation, Global Invacom Group, Sencore, and Datum Systems.