- Chipsets & Processors

- 802.15.4 Chipset Market

802.15.4 Chipset Market Size, Share, and Growth Forecast, 2026 – 2033

802.15.4 Chipset Market by Product Type (Single-Protocol Chipsets, Multi-Protocol Chipsets), Application (Smart Home & Building, Industrial Automation, Smart Meeting, Smart City, Medical, Automotive, Smart Lighting, Others), End-User (Industrial Manufacturers, Oil & Gas, Retail Services Provider, Telecom Services Provider, Others), and Regional Analysis for 2026-2033

802.15.4 Chipset Market Share and Trends Analysis

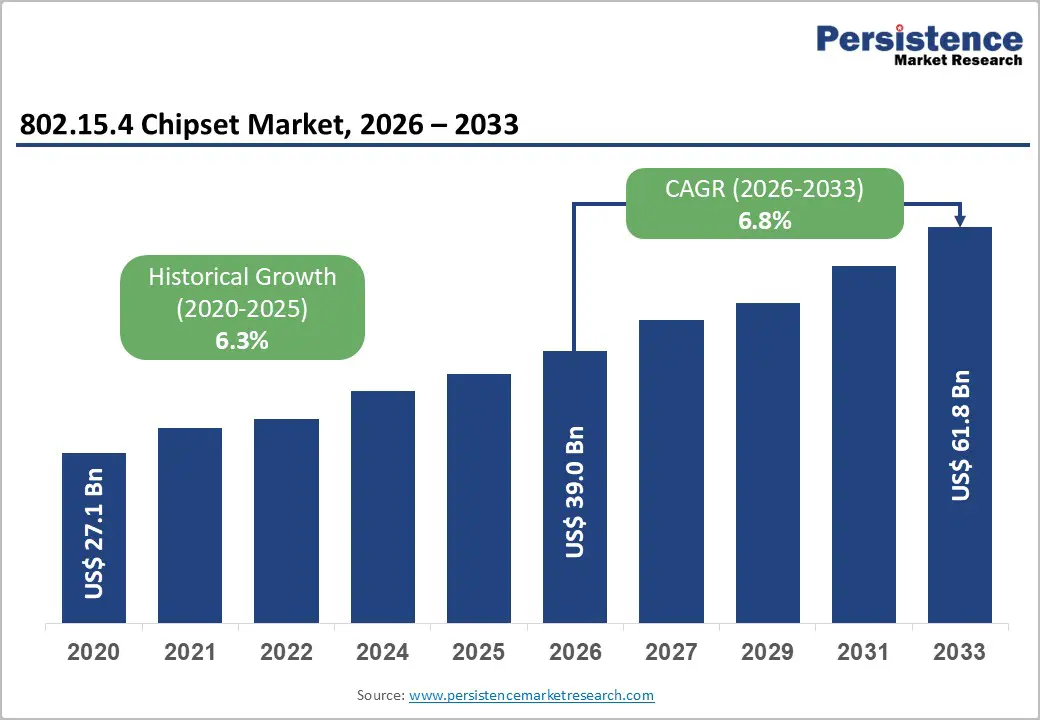

The global 802.15.4 chipset market size is likely to be valued at US$ 39.0 billion in 2026, and is projected to reach US$ 61.8 billion by 2033, growing at a CAGR of 6.8% during the forecast period 2026−2033. The market is expanding as embedded connectivity becomes foundational for Internet of Things (IoT) infrastructures across consumer and industrial domains.

Demand for low-power, mesh-network-capable wireless chipsets is increasing as smart devices proliferate, enabling dependable wireless communications without excessive power consumption. Smart home adoption, a primary use case, consistently drives unit deployments, with mesh protocols such as Zigbee and Thread relying on the 802.15.4 standard to deliver energy-efficient data exchange. Industrial IoT (IIoT) frameworks emphasize real-time monitoring, predictive maintenance, and automated workflows, further promoting these chipsets as enablers of operational intelligence. Geographic technology investment patterns show robust capital inflows into networked infrastructure, creating sustained demand for components that support scalable, secure connectivity. Integration with multi-protocol solutions that combine Bluetooth, Wi-Fi, and 802.15.4 on common silicon platforms supports cross-ecosystem interoperability and strengthens the value proposition for original equipment manufacturers.

Key Industry Highlights

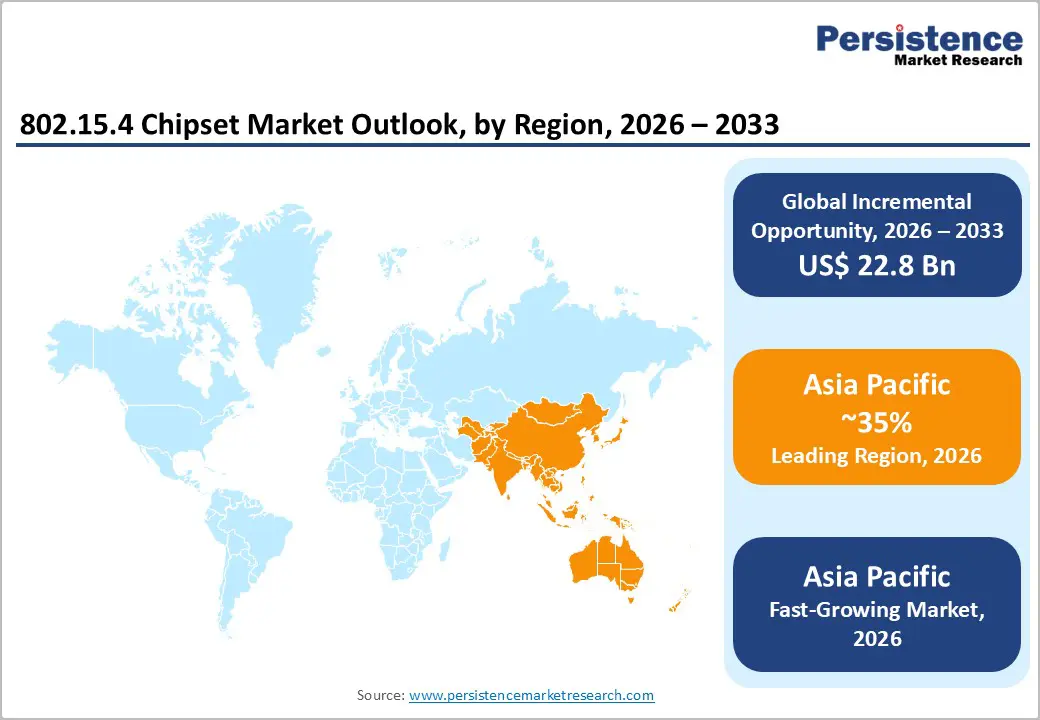

- Dominant Region: Asia Pacific is projected to hold around 35% share in 2026, supported by large-scale IoT deployment and strong local semiconductor ecosystems.

- Fastest-growing Market: Asia Pacific is expected to be the fastest-growing market from 2026 to 2033, driven by rapid IoT adoption and expanding digital infrastructure.

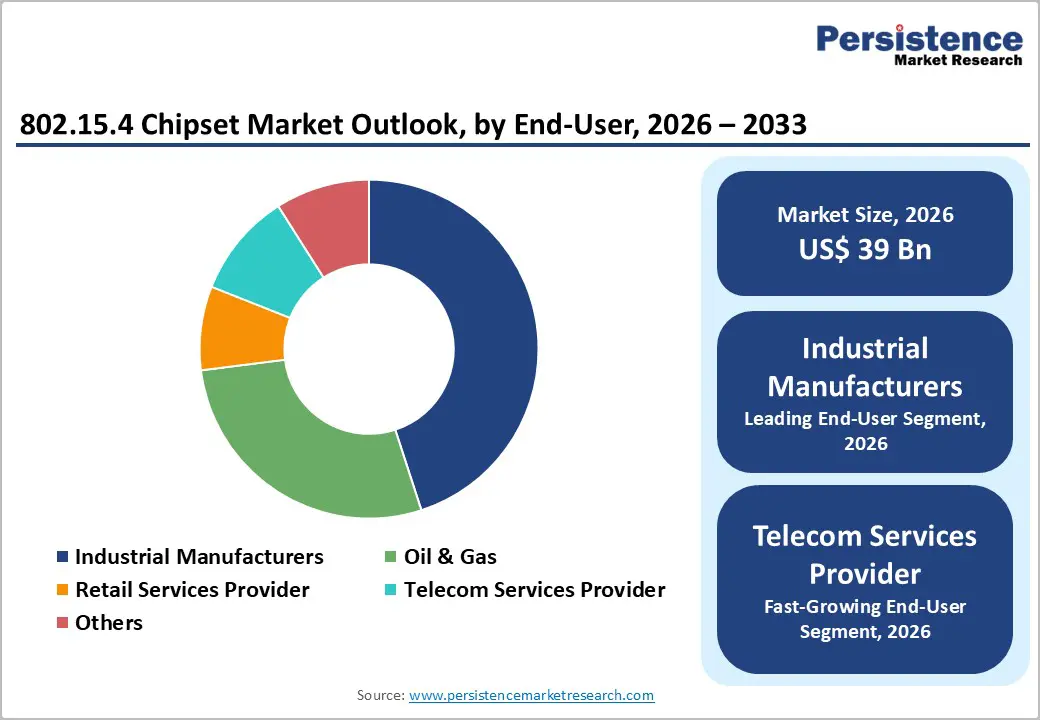

- Leading End-User: Industrial manufacturers are expected to hold about 45% market share in 2026, driven by extensive sensor deployment and predictive maintenance needs.

- Fastest-growing End-User: Telecom services providers are projected to lead growth, driven by managed IoT services, private networks, and device connectivity.

- January 2026: Broadcom launched the Wi-Fi 8 platform for access points and client devices, designed to deliver enhanced throughput, connectivity efficiency, and seamless wireless performance for next-generation networking environments.

| Key Insights | Details |

|---|---|

|

802.15.4 Chipset Market Size (2026E) |

US$ 39.0 Bn |

|

Market Value Forecast (2033F) |

US$ 61.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

IoT Device Penetration and Mesh Network Demand

The penetration of IoT devices and the rising demand for mesh networking are fundamental factors driving demand for 802.15.4 chipsets, as they align with core business needs for scalable, reliable, low-power, and cost-effective connectivity. As connected devices proliferate, the imperative for efficient communication protocols that support large numbers of endpoints with minimal power draw becomes pronounced. The adoption of IoT devices across industrial, commercial, and consumer segments is accelerating global connectivity, with data projections showing that the number of connected IoT devices is expected to grow 14% in 2025, reaching an estimated 21.1 billion globally by year-end. This expansion intensifies demand for wireless standards that can support dense node ecosystems with robust performance and extended battery life, characteristics intrinsic to 802.15.4 based solutions.

Mesh networking demand further reinforces the need for 802.15.4 chipset solutions in enterprise and distributed environments. Mesh topologies support self-healing and extended coverage without linear increases in infrastructure cost, enabling networks to scale organically as more endpoints come online. This capability addresses real business challenges in smart buildings, industrial automation, logistics tracking, and utility metering, where point-to-multipoint communication and fault-tolerant connectivity are essential. By enabling devices to relay data through neighboring nodes, mesh networks reduce dependency on centralized access points and mitigate single-point failures. This translates to lower operational expenses and improved network resilience, key performance indicators for CIOs and network architects planning long-term IoT deployments.

Competition from Alternative Wireless Technologies

The growing availability and adoption of alternative wireless communication protocols create significant challenges for chipset providers. Protocols such as Bluetooth Low Energy (BLE), Wi-Fi, Zigbee, and LoRaWAN offer overlapping functionalities, including low power consumption, reliable data transfer, and scalability for connected devices. These alternatives often benefit from widespread industry adoption, mature ecosystems, and strong interoperability with consumer electronics and industrial devices. Manufacturers may prefer these established protocols due to reduced integration costs, existing developer support, and compatibility with multiple platforms, limiting the potential uptake of newer or less prevalent chipsets. This scenario restricts revenue opportunities and slows market penetration, forcing vendors to invest heavily in differentiation and performance optimization to remain competitive.

The presence of multiple viable wireless solutions also intensifies pricing pressure and shortens the product lifecycle. Customers can choose alternatives that better align with operational requirements, network infrastructure, and total cost of ownership, reducing dependence on a single technology standard. The need to support a diverse range of protocols increases research and development expenditure and complicates product roadmaps. Strategic partnerships, certifications, and compatibility testing become essential to maintain relevance, impacting profitability. Market growth is constrained as chipset developers navigate competing options, balancing innovation with adoption challenges while striving to deliver distinctive performance, energy efficiency, and cost advantages that convince enterprises and device manufacturers to select their solutions over more established alternatives.

Multi-Protocol Integration and Unified Connectivity Platforms

Interoperability challenges in wireless networks create demand for chipsets that support multiple protocols on a single platform. Devices across the industrial, smart home, and healthcare sectors must communicate seamlessly using Zigbee, Thread, and BLE. A unified platform reduces hardware complexity and lowers production costs while enabling rapid device deployment across diverse ecosystems. Software-configurable multiprotocol capability allows adaptation to new standards without physical redesign, extending product lifecycles and improving return on investment. Manufacturers can consolidate network nodes and gateways, streamlining infrastructure requirements and improving scalability for large deployments.

Industry adoption of multiprotocol solutions is accelerating as connected ecosystems grow. Bridging low-power mesh networks with higher-bandwidth infrastructures improves device performance and network efficiency. Over 100 million multiprotocol Matter-certified devices shipped by late 2022 indicates strong market validation for integrated connectivity solutions. Unified platforms support energy efficiency, concurrent connections, and interoperability across vendor ecosystems, enabling flexible network architectures and faster integration of new technologies.

Category-wise Analysis

Product Type Insights

Multi-protocol 802.15.4 chipsets are poised to lead with a forecasted 65% market share in 2026, owing to their ability to support multiple wireless standards on a single silicon platform. This versatility allows device manufacturers to streamline hardware requirements and standardize production processes, enabling deployment across smart home, industrial, and commercial applications without additional redesign costs. Over 1 billion 802.15.4 chipsets shipped annually in 2024, illustrating broad adoption of integrated wireless solutions. It reduces time-to-market for new products and simplifies component sourcing, improving supply chain efficiency. Engineering teams can focus on software and feature innovation rather than hardware adaptation, enhancing overall product development speed and operational efficiency.

Single-protocol chipsets are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by cost-sensitive applications where dedicated functionality suffices without multi-protocol overhead. These chipsets offer a streamlined design, reducing engineering effort and lowering manufacturing costs, making them ideal for devices that require only one connectivity standard. Optimized power efficiency and simplified integration benefit industrial sensors, smart meters, and basic home automation devices, ensuring reliable operation in resource-constrained environments. Focused innovation on low-power modes further extends battery life for remote monitoring, while predictable performance and minimal complexity drive adoption in sectors prioritizing stability and operational simplicity.

Application Insights

Smart home and building automation are likely to be the leading application segment, accounting for 45% of the 802.15.4 chipset market revenue share in 2026, driven by the widespread deployment of connected devices that require robust, mesh-capable wireless communication. Devices such as smart lighting, thermostats, and security sensors increasingly rely on 802.15.4 based protocols to maintain reliable, low-power connectivity across residential and commercial environments. Integration of these devices into unified control platforms allows for seamless energy management, automated scheduling, and enhanced user convenience. Growing interoperability between products ensures broader ecosystem adoption, while energy-efficient mesh networking reduces operational cost and extends device longevity, strengthening the value proposition for both consumers and facility managers.

Industrial automation is expected to grow at the fastest pace between 2026 and 2033, driven by extensive IoT deployments across manufacturing floors, logistics hubs, and facility management systems. Low-latency, reliable wireless connectivity enables real-time asset tracking, predictive maintenance, and process optimization, improving operational efficiency and reducing downtime. 802.15.4 mesh networks provide the scalability and robustness required for dense industrial environments with high interference. Deployment of automated sensors, robotic systems, and environmental monitors accelerates adoption, while integrated connectivity platforms simplify network management. Strong demand for digital transformation across industries reinforces investment in chipsets that deliver performance, energy efficiency, and future-proofed scalability.

End-User Analysis

Industrial manufacturers are slated to hold a dominant position, with an anticipated 45% market share in 2026, driven by rising automation investments and the proliferation of smart manufacturing technologies. Wireless connectivity solutions that reduce operational downtime and enable real-time process insights are key priorities, and standardized chipsets provide consistent performance in demanding environments. Extensive deployment of sensors, actuators, and monitoring devices across production lines allows manufacturers to optimize workflows and implement predictive maintenance. Integration with cloud platforms and industrial control systems further enhances visibility, efficiency, and safety, reinforcing the strategic importance of reliable 802.15.4-based connectivity in industrial operations.

Telecom service providers are forecast to be the fastest-growing end-user segment between 2026 and 2033, driven by expansions in managed IoT services, private network offerings, and device connectivity portfolios. Integration of low-power wireless solutions into telecom service frameworks enables operators to extend network coverage, improve service reliability, and provide end-to-end connectivity for enterprises and smart city deployments. Revenue growth emerges from subscription-based device management, analytics services, and value-added applications leveraging deployed chipsets. Strong demand for connected services, combined with investments in scalable network infrastructure, positions telecom providers as key adopters of 802.15.4 chipsets in evolving IoT ecosystems.

Regional Insights

North America 802.15.4 Chipset Market Trends

North America is poised to occupy a prominent market position through advanced adoption in smart buildings and industrial IoT. Advanced manufacturing facilities and automated logistics hubs rely on reliable mesh-capable connectivity for real-time monitoring, predictive maintenance, and process optimization. Smart building deployments in commercial and residential sectors emphasize energy efficiency, automated lighting, and integrated control systems, driving adoption of multi-protocol chipsets supporting Zigbee, Thread, and Bluetooth Low Energy. Strong semiconductor design and manufacturing capabilities enable rapid prototyping and scaling of chipsets optimized for high performance and low power consumption. Collaboration between device manufacturers and software integrators enhances interoperability and shortens time-to-market for connected products. Investments in digital infrastructure and intelligent building initiatives sustain demand for 802.15.4 silicon, while enterprises focus on reliability, security, and network scalability for large-scale IoT deployment.

Market activity is supported by the extensive deployment of smart industrial networks, commercial automation systems, and enterprise IoT platforms, which require reliable, low-power, mesh-capable chipsets. Telecommunications operators and utility providers implement private networks and automated monitoring solutions, generating consistent demand for integrated connectivity platforms. Multi-protocol chipsets allow seamless integration of legacy and new devices, improving operational efficiency and reducing deployment costs. Enterprise adoption of smart manufacturing, warehouse automation, and connected energy management expands use cases for 802.15.4 silicon. High technology awareness and infrastructure readiness support scalable deployment, enabling robust, interoperable networks and reinforcing investment in advanced chipset solutions.

Europe 802.15.4 Chipset Market Trends

Europe is highly relevant in the 802.15.4 chipset market landscape, driven by the structured adoption of energy-efficient connectivity across smart infrastructure, industrial automation, and utility networks. Strict regulatory emphasis on energy efficiency, sustainability, and building performance drives deployment of low-power wireless technologies in residential and commercial environments. Smart lighting, heating control, and building management systems widely adopt mesh-capable connectivity to meet carbon-reduction targets and operational-efficiency goals. Industrial facilities across Germany, France, and Northern Europe integrate sensor networks for condition monitoring, asset tracking, and process optimization, favoring standardized wireless solutions that ensure long operational lifecycles and predictable performance.

Growth momentum is reinforced by the extensive rollout of smart grid and advanced metering infrastructure across utilities and municipalities. Deployment of connected meters, grid sensors, and distributed energy management systems relies on secure, low-latency mesh communication to maintain network stability and operational visibility. Public investment in digital infrastructure and urban modernization accelerates the adoption of connected street lighting, environmental monitoring, and traffic control systems. Industrial digitalization initiatives emphasize reliability, cybersecurity, and long-term maintenance efficiency, aligning well with low-power wireless platforms. Collaboration between technology providers, utilities, and industrial operators enables scalable implementation of connectivity solutions across multiple countries.

Asia Pacific 802.15.4 Chipset Market Trends

Asia Pacific is expected to dominate, with an estimated 35% share of the 802.15.4 chipset market in 2026, reflecting the scale and intensity of IoT deployment across industrial, commercial, and urban applications. Large-scale adoption of smart manufacturing systems, automated logistics networks, and connected infrastructure drives sustained demand for low-power, mesh-capable chipsets. Manufacturing hubs in China and industrial clusters in India have implemented extensive sensor networks, leveraging 802.15.4-based connectivity to enable real-time monitoring, predictive maintenance, and energy optimization. Government-led smart city programs and urban automation initiatives have accelerated large-scale sensor deployment, requiring chipsets capable of multi-protocol integration and reliable mesh networking. Localized semiconductor production further supports rapid prototyping and deployment, lowering cost and time-to-market for original equipment manufacturers (OEMs).

Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, stimulated by the accelerating adoption of IoT devices and the expansion of digital infrastructure across enterprise, industrial, and urban ecosystems. Deployment of sensors for traffic management, environmental monitoring, and utility control relies on robust, low-latency mesh networks to ensure reliability and scalability. Private industrial networks and large-scale commercial IoT implementations drive repeated orders of multi-protocol chipsets, supporting ecosystem development and encouraging innovation in power optimization, security, and interoperability. Strategic partnerships between chipset manufacturers and system integrators facilitate large-scale deployments, while government-backed automation programs incentivize connected device adoption.

Competitive Landscape

The global 802.15.4 chipset market exhibits a moderately consolidated structure, shaped by a limited number of global semiconductor companies that command strong design capabilities, manufacturing scale, and long-standing customer relationships. Key players such as ON Semiconductor Corporation, STMicroelectronics NV, NXP Semiconductors NV, Panasonic Corporation, and Qualcomm Inc. capture a significant portion of total revenue through diversified product portfolios addressing industrial, commercial, and consumer connectivity needs. Competitive strength is closely linked to the ability to deliver reliable, low-power wireless solutions that meet stringent performance, security, and longevity requirements. These vendors benefit from deep expertise in mixed-signal design, embedded processing, and radio frequency integration, enabling differentiated offerings across both single-protocol and multi-protocol platforms.

Competitive positioning increasingly emphasizes platform breadth, software enablement, and ecosystem alignment rather than standalone silicon performance. Vendors invest heavily in development kits, protocol stacks, and reference designs to simplify integration and shorten deployment timelines for device manufacturers. Collaboration with standards bodies, cloud service providers, and system integrators enhances interoperability across heterogeneous networks, reducing friction during large-scale rollouts. Strategic focus on integrated connectivity solutions allows suppliers to address evolving application requirements in smart infrastructure, industrial automation, and connected devices without frequent hardware redesign. Differentiation also emerges through support services, long-term product availability, and robust security features aligned with enterprise and industrial expectations.

Key Industry Developments

- In November 2025, Zigbee 4.0 introduced with the Suzi feature, enabling Sub-GHz mesh connectivity along with enhanced security and interoperability to support longer-range and more resilient IoT deployments.

- In November 2025, IntelPro licensed Ceva’s Wi-Fi 6 and Bluetooth 5 connectivity IP to power its new IPRO7AI system-on-chip, integrating multi-mode wireless, security, and AI processing to support Matter-ready smart home, industrial, and consumer IoT devices.

- In March 2025, Synaptics unveiled its ultra-low-power SYN461x SoC family combining Wi-Fi, Bluetooth/BLE, and 802.15.4 (Zigbee/Thread) connectivity to support embedded Edge AI and IoT devices with optimized power, integration, and interoperability.

Companies Covered in 802.15.4 Chipset Market

- ON Semiconductor Corporation

- STMicroelectronics NV

- NXP Semiconductors NV

- Panasonic Corporation

- Qualcomm Inc.

- Qorvo Inc.

- Marvell International Ltd

- Nordic Semiconductors ASA

- Microchip Technology Inc.

- Silicon Laboratories Inc.

- Texas Instruments Inc.

Frequently Asked Questions

The global 802.15.4 chipset market is projected to reach US$ 39.0 billion in 2026.

Rising deployment of low-power, mesh-based IoT networks across smart buildings, industrial automation, utilities, and connected infrastructure are driving the market.

The market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Expansion of multi-protocol, energy-efficient connectivity platforms that enable interoperable, scalable IoT deployments across industrial, commercial, and smart infrastructure applications represent the key market opportunity.

Some of the key market players include ON Semiconductor Corporation, STMicroelectronics NV, NXP Semiconductors NV, and Panasonic Corporation.