- Specialty & Fine Chemicals

- 1,3-Diphenyl Guanidine Market

1,3-Diphenyl Guanidine Market Size, Share, and Growth Forecast, 2025 - 2032

1,3-Diphenyl Guanidine Market by Grade Type (Industrial Grade DPG, Pharmaceutical Grade DPG, Specialty Grade DPG), Application (Automotive, Rubber and Plastics, Pharmaceuticals, Agriculture, Others), Form (Powder, Granular, Liquid), and Regional Analysis for 2025 - 2032

1,3-Diphenyl Guanidine Market Size and Trends Analysis

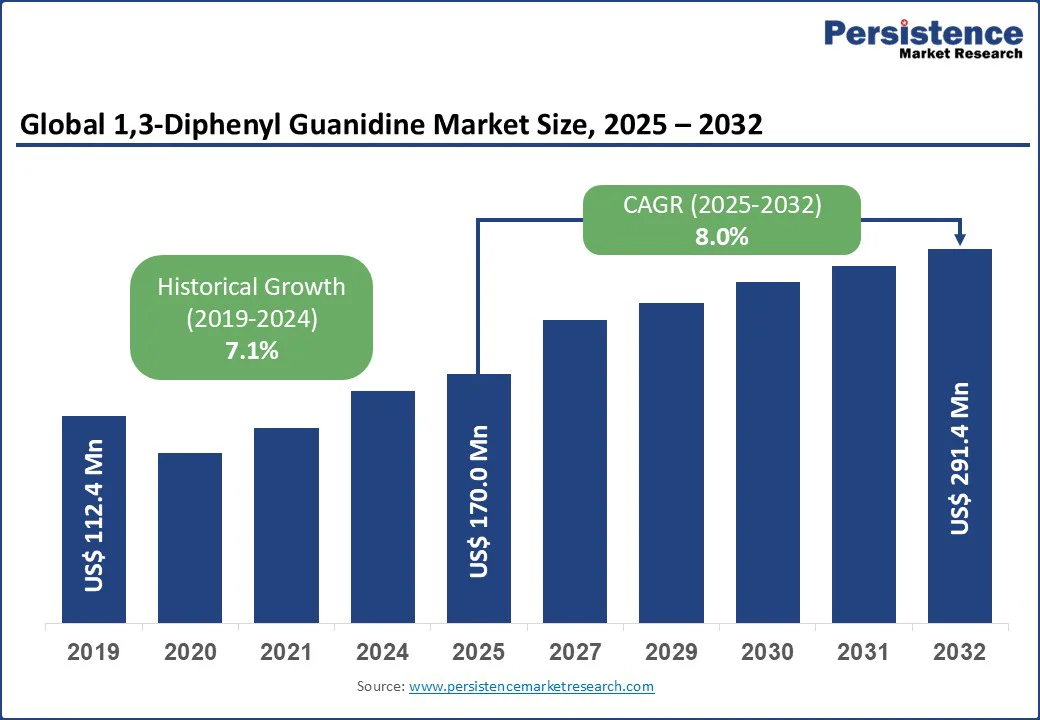

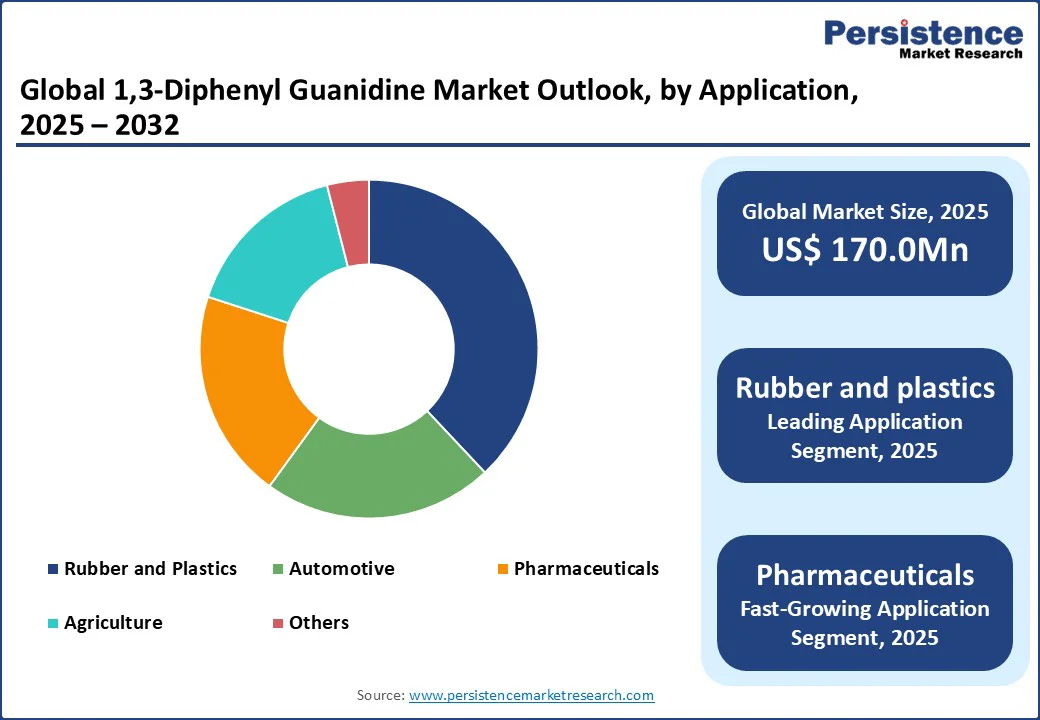

The global 1,3-diphenyl guanidine market size is likely to value at US$170.0 Mn in 2025 to US$291.4 Mn by 2032, registering a CAGR of 8.0% during the forecast period from 2025 to 2032.

Key Industry Highlights:

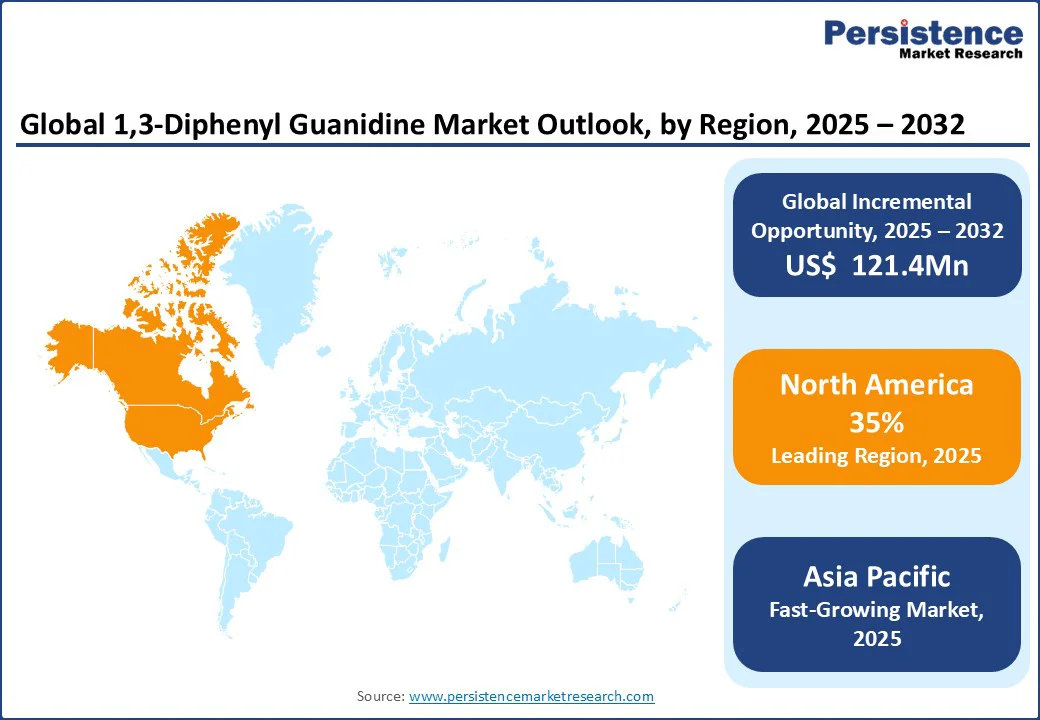

- Leading Region: North America holds a 35% market share in 2025, driven by advanced industrial infrastructure, high chemical consumption, and widespread adoption of innovative synthesis methods.

- Fastest-growing Region: Asia Pacific, propelled by increasing manufacturing investments, a high burden of industrial growth, and expanding facilities in countries such as China and India.

- Dominant Grade Type: Industrial Grade DPG accounts for approximately 35.50% of the 1,3-diphenyl guanidine market share in 2025, driven by its critical role in rubber vulcanization.

- Leading Application: Rubber and Plastics leads with a 38% share, reflecting its widespread use in tire production and polymer processing.

- Leading Form: Powder dominates with a 40% share in 2025, due to its ease of handling and stability.

| Global Market Attribute | Key Insights |

|---|---|

| 1,3-Diphenyl Guanidine Market Size (2025E) | US$170.0 Mn |

| Market Value Forecast (2032F) | US$291.4 Mn |

| Projected Growth (CAGR 2025 to 2032) | 8.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.1% |

The 1,3-diphenyl guanidine market is witnessing strong growth, propelled by rising demand for rubber accelerators in automotive and industrial sectors. Advancements in chemical synthesis, coupled with innovations in manufacturing processes, are enhancing efficiency and quality.

Expanding applications across diverse industries, along with supportive global initiatives in developing regions, further strengthen market opportunities and long-term growth prospects.

Market Factors - Trends, Growth, and Barriers Analysis

Rising Demand for Rubber Products and Technological Advancements Push Demand

The global surge in demand for rubber products is a primary driver of the 1,3-diphenyl guanidine market. According to the International Rubber Study Group, global natural rubber consumption reached 14.5 Mn tons in 2023, with synthetic rubber adding another 16 Mn tons, driven by the automotive and tire industries.

This rising consumption, particularly in emerging economies with expanding manufacturing sectors, underscores the urgent need for effective accelerators such as DPG that enhance vulcanization processes and improve rubber durability.

In recent years, the U.S. Tire Manufacturers Association reported hundreds of Mns of tires produced in North America, highlighting the demand for DPG in compounding, where efficiency improves significantly with optimal accelerators.

Technological advancements in chemical synthesis are significantly boosting market growth. Modern platforms, such as Arkema’s advanced reactors, offer high purity and yield, reducing impurities and enabling faster production through real-time monitoring.

Innovative synthesis methods can cut production costs by nearly one-third compared to traditional approaches, with purity rates exceeding very high levels for industrial-grade DPG. Innovations such as green chemistry processes and catalyst optimization further enhance adoption, particularly in resource-limited settings where conventional methods are inefficient.

Restraint - High Costs and Skilled Personnel Requirements Restrict Adoption

The high cost of 1,3-diphenyl guanidine production remains a significant barrier to widespread adoption, particularly in low- and middle-income countries. Advanced synthesis methods, equipped with features such as high-purity distillation and contamination control, require substantial upfront investment.

Additionally, ongoing costs for raw materials, quality testing, and regulatory compliance add to the total cost of ownership. In regions such as Sub-Saharan Africa and rural parts of South Asia, where industrial budgets are constrained, these financial burdens limit access to DPG, even amidst rising rubber demand.

The World Trade Organization has noted that “the cost of specialty chemicals may be a disincentive,” highlighting high production costs as a barrier to widespread adoption of innovative compounds in many countries. The requirement for skilled personnel to handle and apply DPG also hinders market growth.

Formulating and testing DPG in rubber compounds demands specialized training in chemical engineering. A shortage of certified experts in polymer chemistry in developing regions exacerbates this challenge. This skills gap, combined with high training costs, restricts the adoption of advanced grades in emerging markets, slowing market expansion.

Opportunity - Innovation in Eco-Friendly Formulations and Emerging Applications Boosts Consumption

The development of eco-friendly and sustainable DPG formulations presents significant growth opportunities, enabling deployment in green manufacturing scenarios, regulatory-compliant industries, and environmentally sensitive applications. These formulations overcome the limitations of traditional compounds, making them ideal for sustainable settings.

For example, LANXESS’s low-emission DPG offers reduced environmental impact with maintained performance, supporting use in eco-tires and green polymers. As industries prioritize sustainability, demand for such solutions is rising, particularly in regions with strict environmental regulations.

The growing popularity of DPG in pharmaceuticals and agriculture provides another avenue for market expansion. These applications require high-purity grades and deliver specialized benefits, making them suitable for niche environments. DPG derivatives can significantly enhance drug synthesis efficiency compared to alternatives, driving demand for innovative uses in high-growth sectors such as biotech.

The integration of digital platforms for supply chain monitoring and quality control further enhances market potential. Companies such as Sumitomo Chemical Co., Ltd are incorporating IoT-enabled systems, allowing real-time tracking and proactive management. This trend improves accessibility and operational efficiency, supporting market growth in both developed and emerging regions.

Category-wise Analysis

Grade Type Insights

The 1,3-diphenyl guanidine market is segmented into industrial grade DPG, pharmaceutical grade DPG, and specialty grade DPG. Industrial-grade DPG dominates, holding approximately 35.5% of the 1,3-diphenyl guanidine market share in 2025, due to its critical role in large-scale rubber processing. Advanced industrial-grade products, such as those from Arkema are widely adopted for their cost-effectiveness and reliability, making them essential in manufacturing settings.

Specialty grade DPG is the fastest-growing segment, driven by increasing demand for customized solutions in advanced applications. Innovations in specialty formulations, such as those from Sigma-Aldrich Corporation, offer superior performance and purity, boosting adoption in high-volume specialized centers.

Application Insights

The 1,3-diphenyl guanidine market is divided into automotive, rubber and plastics, pharmaceuticals, agriculture, others. Rubber and plastics lead with a 38% share in 2025, driven by its widespread use in vulcanization processes. These applications, which enhance material strength, are critical for industrial production, with millions of tons processed annually worldwide for tires and polymers.

Pharmaceuticals are the fastest-growing segment, fueled by advancements in chemical intermediates and the rising prevalence of drug synthesis needs. Its ability to act as a catalyst with high precision drives its adoption in advanced facilities, particularly post-global health focus.

Form Insights

The global 1,3-diphenyl guanidine market is segmented into powder, granular, and liquid. Powder dominates with a 40% share in 2025, driven by its high stability and ease of storage. This form relies on simple handling methods to ensure consistency, making it essential for routine compounding in factories and labs.

Liquid is the fastest-growing segment, propelled by an increasing focus on versatile formulations for complex applications. These forms allow for easy mixing, cater to the growing demand for high-throughput processing, and innovative uses.

Regional Insights

North America 1,3-Diphenyl Guanidine Market Trends

North America dominates the 1,3-diphenyl guanidine market, expected to account for a 35% share in 2025. This dominance is driven by high industrial activity, advanced chemical infrastructure, and increasing demand in the rubber sector.

The U.S. Census Bureau reports substantial growth in chemical exports annually, underscoring the urgent need for robust accelerator solutions. To address this demand, leading brands such as Sigma-Aldrich Corporation and Alfa Aesar are developing innovative platforms designed to support manufacturing teams with purity, efficiency, and scalable methods.

Consumer preferences are shifting toward high-purity, sustainable formulations with integrated quality controls, such as LANXESS’s compounds, which enhance process accuracy and compliance. Stringent EPA regulations prioritize chemical safety, encouraging the adoption of reliable, high-performance components. Favorable policies for industrial incentives further incentivize manufacturers and suppliers to invest in advanced supplies, supporting market growth.

Europe 1,3-Diphenyl Guanidine Market Trends

Europe’s market is led by Germany, the U.K., and France, driven by regulatory support and high industrial volumes. Germany holds the largest share, supported by strong sales from companies such as Arkema and LANXESS. The EU’s Chemical Strategy fosters innovation and compliance, promoting the adoption of advanced industrial and specialty grades in major facilities.

In the U.K., market growth is driven by the rising demand for rubber applications, with products such as Sumitomo Chemical Co., Ltd’s formulations gaining popularity for their precision and sustainability. France is witnessing increased demand for pharmaceutical uses, with Haihang Industry Co., Ltd offering specialized solutions. Regulatory support for green chemistry across Europe further enhances market prospects.

Asia Pacific 1,3-Diphenyl Guanidine Market Trends

Asia Pacific represents the fastest-growing market for 1,3-diphenyl guanidine, driven by expanding industrial infrastructure, increasing chemical awareness, and rising investments in manufacturing technologies.

India remains a key growth engine, where rising industrial trends and government programs such as the Production Linked Incentive scheme are boosting demand for affordable, versatile solutions. Domestic manufacturers such as Xiamen Aeco Chemical Industrial and TCI AMERICA cater to local needs with cost-effective kits designed for both urban and rural settings.

In China, rapid market expansion is supported by large-scale upgrades, growing adoption of automated systems, and the presence of leading players such as Sumitomo Chemical Co., Ltd. Japan’s market is characterized by demand for high-precision tools used in automotive and pharmaceuticals, with companies such as Arkema gaining market share.

Across the region, increased spending, digital platforms, and the emphasis on efficient production are collectively accelerating adoption, making the Asia Pacific a critical hub for future market growth.

Competitive Landscape

The global 1,3-diphenyl guanidine market is highly competitive, with global and regional players striving for dominance through innovation, cost efficiency, and strong supply reliability. The increasing demand for sustainable and high-purity formulations adds pressure, as compliance with strict regulatory frameworks becomes essential.

To gain a competitive edge, companies are actively pursuing strategic partnerships, mergers, and acquisitions, positioning themselves strongly in this evolving and regulation-driven landscape.

Key Developments:

- February 2025: LANXESS introduced Vulkanox HS Scopeblue, a sustainable antioxidant designed as a drop-in replacement for conventional TMQ. Manufactured at its ISCC PLUS-certified German plant using biocircular acetone and renewable energy, it lowers carbon footprint significantly while enhancing tire longevity.

- March 2025: LANXESS showcased its innovative and sustainable rubber additives at Tire Technology Expo 2025 in Hannover, Germany. The portfolio enabled tire manufacturers to enhance process efficiency, cut environmental impact, and produce high-performance tires. These solutions aligned with global sustainability goals, advancing eco-friendly mobility in the tire industry.

Companies Covered in 1,3-Diphenyl Guanidine Market

- Alfa Aesar

- Arkema

- Haihang Industry Co., Ltd.

- Sigma-Aldrich Corporation

- Sumitomo Chemical Co., Ltd

- TCI AMERICA

- Xiamen Aeco Chemical Industrial

- LANXESS

Frequently Asked Questions

The 1,3-diphenyl guanidine market is projected to reach US$170.0 Mn in 2025.

Rising demand for rubber products, technological advancements in synthesis, and government initiatives for industrial chemicals are the key market drivers.

The 1,3-diphenyl guanidine market is poised to witness a CAGR of 8.0% from 2025 to 2032.

Innovations in eco-friendly formulations and emerging applications in pharmaceuticals present significant growth opportunities.

Arkema, LANXESS, and Sumitomo Chemical Co., Ltd are among the leading market players.