- Pharmaceuticals

- Softgel Capsules Market

Softgel Capsules Market Size, Share, and Growth Forecast, 2025 - 2032

Softgel Capsules Market By Material (Gelatin-based, Non-Animal-based), Source (Porcine, Bovine, Piscine, Pullulan-based, Carrageenan-based, Others), Application (Pharmaceuticals, Nutraceutical & Dietary Supplements, Cosmetics & Personal Care, Others), and Regional Analysis for 2025 - 2032

Softgel Capsules Market Share and Trends Analysis

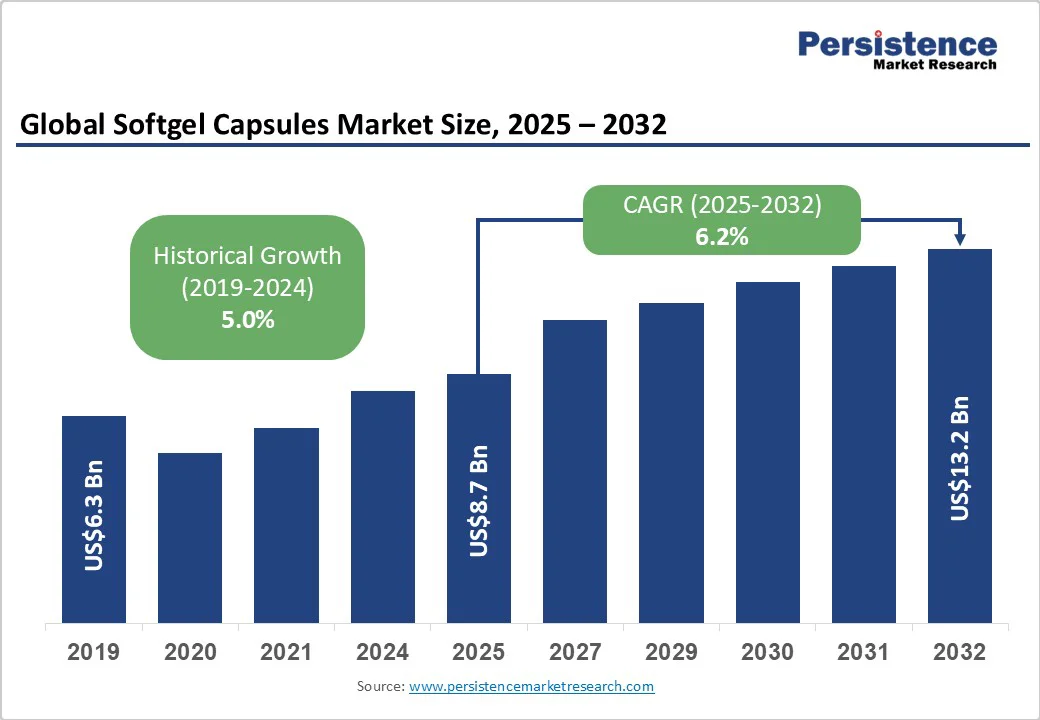

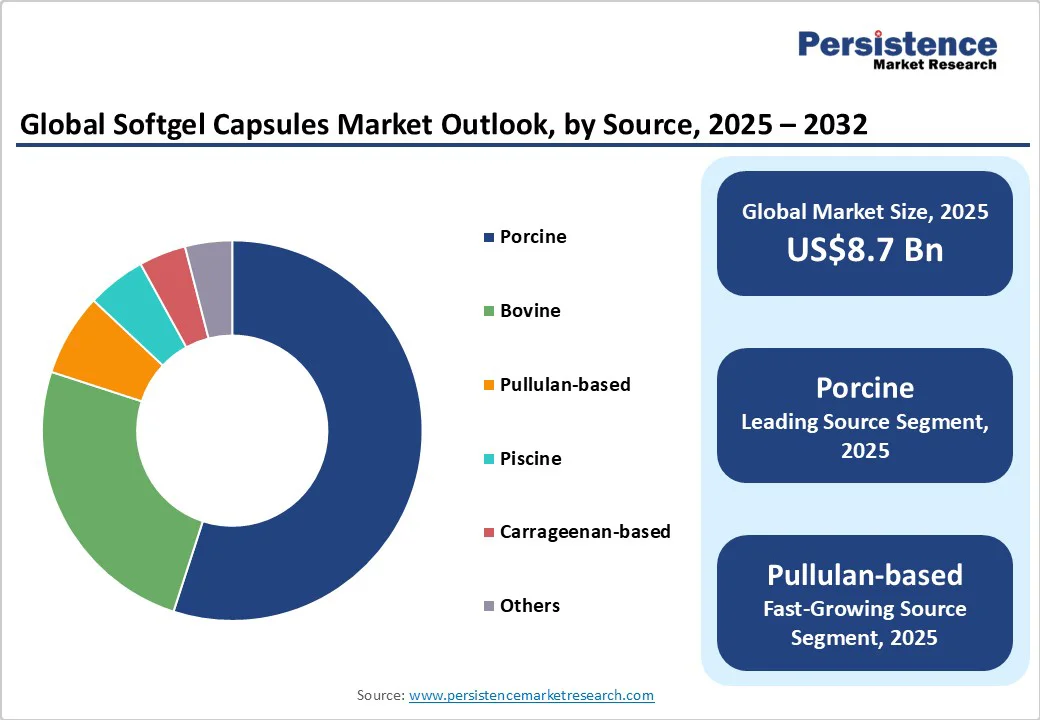

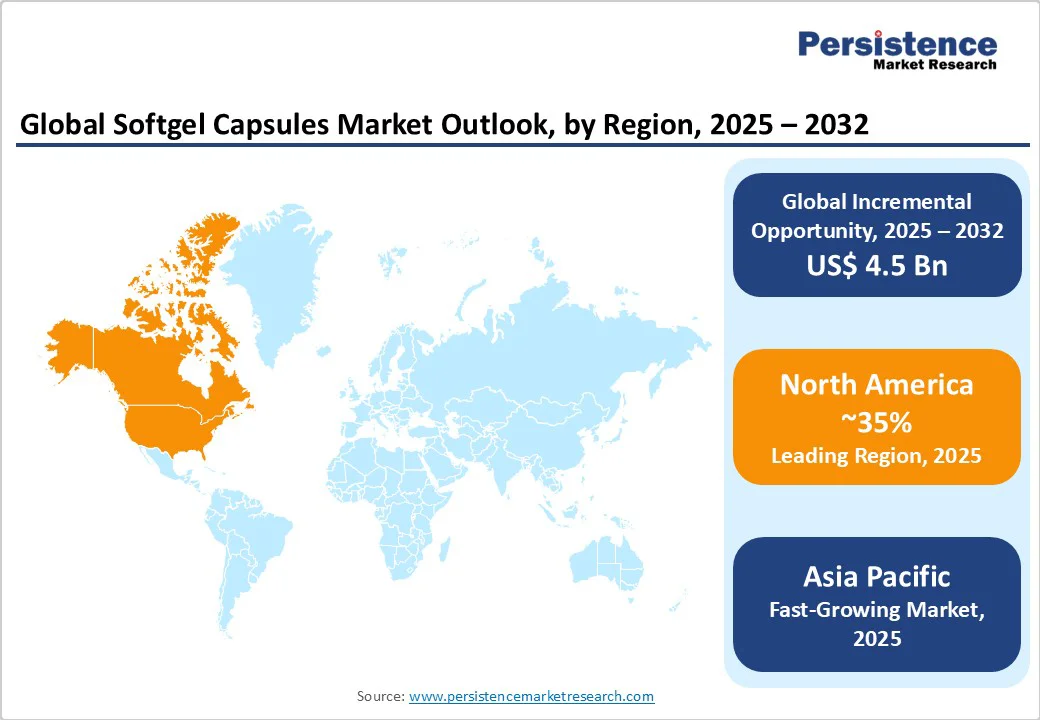

The global softgel capsules market size is likely to be valued at US$8.7 Billion in 2025, and is estimated to reach US$13.2 Billion by 2032, growing at a CAGR of 6.2% during the forecast period 2025−2032, driven by an escalating demand for nutraceutical and pharmaceutical products, supported by rising health awareness and advancements in encapsulation technology.

Market growth trajectory is underpinned by evolving consumer preferences toward convenient dosage forms, sophisticated formulation capabilities for poorly soluble drugs, and an increasing shift toward plant-based capsule materials responding to dietary and regulatory requirements.

Key Industry Highlights

- Leading Region: North America is poised to lead with around 35% market share in 2025, supported by a mature innovation ecosystem promoting pharmaceutical and nutraceutical R&D.

- Fastest-growing Regional Market: Asia Pacific is set to be the fastest-growing regional market through 2032, due to expanding middle classes and improving supply chains.

- Dominant & Fastest-growing Sources: Porcine gelatin is likely to be the leading source segment at approximately 55% market share, while pullulan-based capsules are anticipated to exhibit the fastest CAGR during 2025-2032.

- Leading and Fastest-growing Material Types: The gelatin-based capsule segment holds roughly 80% market share in 2025, but non-animal-based capsules are expected to expand at a high CAGR.

- Dominant Application Type: Nutraceuticals account for about 60% of applications in 2025, fueled by the global shift toward preventive healthcare and tailored nutrition.

- Strategic Initiatives: Acquisitions, capacity expansions, and technology partnerships focused on alternative capsule materials and oxygen-impermeable formulations to expand market access and differentiation.

| Key Insights | Details |

|---|---|

|

Softgel Capsules Market Size (2025E) |

US$8.7 Bn |

|

Market Value Forecast (2032F) |

US$13.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Adoption of Vegan Lifestyles and Religious Dietary Restrictions

The global rise in veganism, along with stricter adherence to religious dietary laws, such as Halal and Kosher requirements, is creating a growing niche demand for plant-based softgel capsules. According to the Vegan Society, the global vegan population is growing at a compound annual rate of approximately 6-8%, particularly pronounced in North America and Europe. Regulatory authorities such as the U.S. FDA and the European Food Safety Authority (EFSA) are emphasizing transparency in capsule ingredient sourcing, driving manufacturers to innovate with non-animal gelatin alternatives. This demand diverges from traditional gelatin-based sourcing, which faces supply fluctuations due to livestock disease outbreaks and environmental concerns.

Companies are investing in research and development for starch, cellulose, pullulan, and carrageenan-based capsules that meet both ethical consumer demands and regulatory compliance. Manufacturer differentiation through plant-based offerings is becoming a key competitive advantage, tapping into markets previously inaccessible due to dietary restrictions.

Cost Stability Fueled by Supply Chain Disruptions and Raw Material Availability

The market growth is constrained by its dependence on animal-derived gelatin, primarily sourced from porcine and bovine origins. The prevalence of livestock diseases such as African Swine Fever (ASF) has periodically disrupted porcine gelatin supply chains, causing volatility in raw material prices. Data from the Food and Agriculture Organization (FAO) indicates that ASF outbreaks led to a 15-20% contraction in global pig populations during 2018-2020, subsequently inflating gelatin costs by up to 18% regionally.

Environmental and ethical concerns are also pressuring supply chain transparency and sustainability practices. These supply chain risks impose cost premium burdens on softgel manufacturers, which are passed to end consumers and may limit market penetration, especially in price-sensitive regions. Furthermore, regulatory requirements around traceability and hygienic sourcing impose compliance costs estimated to add 5-7% to operational expenses. This restraint creates barriers for smaller players and novel entrants, fostering a competitive advantage for vertically integrated companies with secured gelatin sourcing.

Steady Rise in Nutraceutical Demand in Emerging Economies

Asia Pacific is presenting lucrative growth avenues for the softgel capsules market players, boosted by increasing health awareness, expanding middle-class demographics, and growing disposable incomes. Nutraceutical consumption in high-value markets such as India and China, especially omega-3 fatty acids, vitamins, and herbal supplements, is witnessing strong uptake, driven by preventive healthcare trends and government health initiatives.

Key enablers include improvements in supply chain infrastructure, increasing quality standards led by regulatory harmonization in ASEAN, and foreign direct investments boosting local manufacturing capabilities. This opportunity invites strategic partnership considerations for global players aiming to localize production, co-develop formulations tailored to regional preferences, and optimize distribution networks. Investors and companies that align with evolving regulations and cultural preferences are well-positioned to capitalize on this opportunity.

Category-wise Analysis

Material Insights

Gelatin-based softgel capsules remain the cornerstone of the material segment, commanding an estimated 80% share of the market in 2025. Their dominance stems from well-established manufacturing processes, cost efficiencies, and excellent physicochemical properties such as gel strength and flexibility, which ensure reliable encapsulation and controlled release profiles. Pharmaceutical companies and nutraceutical manufacturers extensively rely on gelatin capsules due to regulatory familiarity and established quality standards. Globally, the supply chain for animal-derived gelatin, although challenged by fluctuations, still provides scalable volume for mass-market applications.

Non-animal-based softgel capsules are experiencing the fastest adoption due to increasing consumer preference for vegan, vegetarian, and halal-compliant products, spurred by global ethical concerns and regulatory transparency requirements. These capsules offer compatibility with plant-based formulations and appeal to niche markets emphasizing clean-label products. Suppliers are continuously innovating to improve mechanical properties, shelf-life, and masking of unpleasant tastes to match gelatin’s performance. Expansion of plant-based softgel offerings unlocks new market segments and geographic territories, particularly in Asia Pacific and Europe, where the demand for sustainable and ethical products is accelerating.

Source Insights

Porcine gelatin is set to maintain its position as the largest source segment, constituting roughly 55% of the softgel capsules market revenue share in 2025. Its preferred use is driven by superior functional properties such as gel strength and thermoreversibility, which facilitate efficient encapsulation and stability. Although regional religious restrictions limit its acceptance in certain markets, porcine gelatin remains the primary choice in Western countries and East Asia. Supply chain disruptions stemming from disease outbreaks, however, have increased the cost marginally and made supply diversification a point of emphasis for manufacturers.

Pullulan-based capsules are gaining traction with an anticipated high CAGR from 2025 to 2032, reflecting their growth as an oxygen-impermeable and biodegradable solution suitable for sensitive nutraceuticals. Their natural origin from starch fermentation aligns with sustainability goals and the rising demand for clean-label products. The growing availability of pullulan at a commercial scale and advancements in manufacturing technology have reduced production costs, making it viable for premium formulations. The segment growth is further propelled by increasing conversion among pharmaceutical and nutraceutical companies aiming to address consumer demands and regulatory pressures related to ingredient transparency and environmental impact.

Application Insights

Nutraceuticals are expected to lead applications with about 60% share in 2025, driven by a global trend towards preventive healthcare and personalized nutrition. Softgel capsules maximize the bioavailability of fat-soluble vitamins, omega-3 fatty acids, and botanical extracts, meeting consumer preference for convenient dosage forms. The segment growth is supported by rising chronic disease prevalence, aging populations, and expanding fitness-conscious demographics worldwide. Regulatory clarity on health claims and supplement safety further fosters trust and market adoption.

Pharmaceutical applications in softgel capsules are likely to progress at a healthy CAGR through 2032. Their demand is bolstered by technological advances enabling encapsulation of poorly soluble APIs, controlling drug release profiles, and enhancing patient compliance. Innovations in softgel design target encapsulation of biologics and parenteral formulations, broadening therapeutic applicability. Regulatory approvals facilitating accelerated drug development cycles also stimulate pharmaceutical softgel adoption, especially in specialty and orphan drug segments.

Regional Insights

North America Softgel Capsules Market Trends

North America is poised to sustain market leadership with an approximate 35% of the softgel capsules market share by 2025, owing to the mature pharmaceutical and nutraceutical sectors of the U.S. Its regulatory environment, led by the FDA, maintains high product standards, which stimulate continuous R&D efforts in softgel formulation enhancements and plant-based alternatives. Innovation ecosystems across the U.S. foster collaboration between manufacturers, academia, and biotech firms, accelerating new capsule technology development. Investment trends focus on green manufacturing initiatives and supply chain digitalization to improve efficiency and transparency.

Key growth drivers include high consumer health awareness, increasing geriatric population demanding customized nutrition, and a preference for convenient dosage forms aligned with active lifestyles. The competitive landscape features a blend of large multinational players and nimble startups pioneering non-animal-based capsules and advanced softgel formats.

Asia Pacific Softgel Capsules Market Trends

Asia Pacific is forecast to command nearly 30% of the market by 2025, positioning it as the fastest expanding regional market with a high CAGR over the 2025-2032 period. Strong growth in prime economies of China, India, Japan, and ASEAN is propelled by rapid urbanization, expanding middle-class populations, and intensifying public and private sector focus on preventive healthcare. Government initiatives to strengthen regulatory systems and enhance product quality standards are harmonizing markets, improving trade and investment landscapes.

Manufacturing cost advantages and strategic investment inflows are enabling regional players to expand production capacity and scale export capabilities. Consumer demand for high-quality nutraceutical softgels and plant-based capsules is rising rapidly, supported by increasing health expenditures and wellness consciousness.

Europe Softgel Capsules Market Trends

Europe is predicted to hold an estimated 25% share in 2025, with Germany, the U.K., France, and Spain leading regional growth. The European Medicines Agency (EMA) provides a harmonized regulatory framework, which enhances market stability and accelerates product approvals. Sustainability and transparency are major themes, with strict guidelines on raw material sourcing and environmental impact influencing formulation choices and supply chains.

An aging population and increasing chronic disease prevalence are significant market drivers, complemented by a cultural propensity towards dietary supplements and natural health solutions. The emergence of regional manufacturing clusters focusing on plant-based softgels and specialty nutraceuticals further bolsters the competitive environment. Investment opportunities are currently concentrated on sustainable sourcing and technological innovation to meet increasingly stringent regulatory mandates.

Competitive Landscape

The global softgel capsules market structure is moderately concentrated, with leading players commanding approximately 60% combined market share. Key industry giants such as Catalent Pharma Solutions, Aenova Group, and Suheung Co. Ltd. maintain dominant positions through technological leadership, global manufacturing footprint, and robust supply chain capabilities.

A growing number of regional and niche manufacturers are intensifying competition, particularly in plant-based capsule technologies. The market reflects a balance between consolidated large-scale operations and agile niche innovators responding rapidly to evolving consumer demands.

Key Industry Developments

- In May 2025, Robinson Pharma added 10 softgel machines, becoming the largest U.S. softgel producer with a capacity of 23 billion annual. Expanded tablet, capsule, liquid, and gummy output enhances efficiency, reinforcing its global leadership in custom nutraceutical manufacturing.

- In March 2025, Jupiter Neurosciences partnered with Catalent Pharma to manufacture JOTROL softgel capsules for a Phase 2a Parkinson’s trial, focusing on safety, tolerability, and PK/PD over three months, leveraging Catalent’s expertise for efficient, timely production.

- In February 2025, Icaritin (ICA), a natural extract from Epimedium, was approved as a Class 1.2 TCM innovative drug for advanced hepatocellular carcinoma, showcasing anti-cancer, anti-inflammatory, immune-modulating, and antioxidant properties derived from a single natural source.

Companies Covered in Softgel Capsules Market

- Catalent Pharma Solutions, Inc.

- Aenova Group

- Suheung Co., Ltd.

- Lonza Group AG

- Capsugel (a Lonza business)

- Softgel Technologies Ltd.

- Patheon (Thermo Fisher Scientific Inc.)

- R. P. Scherer Corporation

- Evonik Industries AG

- Martinswerk GmbH

- Oval International Ltd.

- Pharmax Ltd.

- Xcelience Ltd.

- CPL Aromas

- Nitta Gelatin Inc.

Frequently Asked Questions

The softgel capsules market is projected to reach US$8.7 Billion in 2025.

Huge demand for nutraceutical and pharmaceutical products, rising health awareness, and advancements in encapsulation technology are driving the softgel capsules market.

The softgel capsules market is poised to witness a CAGR of 6.2% from 2025 to 2032.

Evolving consumer preferences toward convenient dosage forms, sophisticated formulation capabilities for poorly soluble drugs, and an increasing shift toward plant-based capsule materials responding to dietary and regulatory demands are key market opportunities.

Catalent Pharma Solutions, Inc., Aenova Group, and Suheung Co., Ltd. are some of the key players in this market.