- Telecommunications

- SD-WAN Market

SD-WAN Market Size, Share, and Growth Forecast, 2026 – 2033

SD-WAN Market by Component (Solution, Services), Deployment (Cloud-based, On-premises, Hybrid), Enterprise Size (Small & Medium Enterprises, Large Enterprises), End User (Service Provider, Vertical [BFSI, Healthcare, Government, Retail & CPG, Energy & Utilities, Manufacturing, Others], and Regional Analysis for 2026 – 2033

SD-WAN Market Size and Trend Analysis

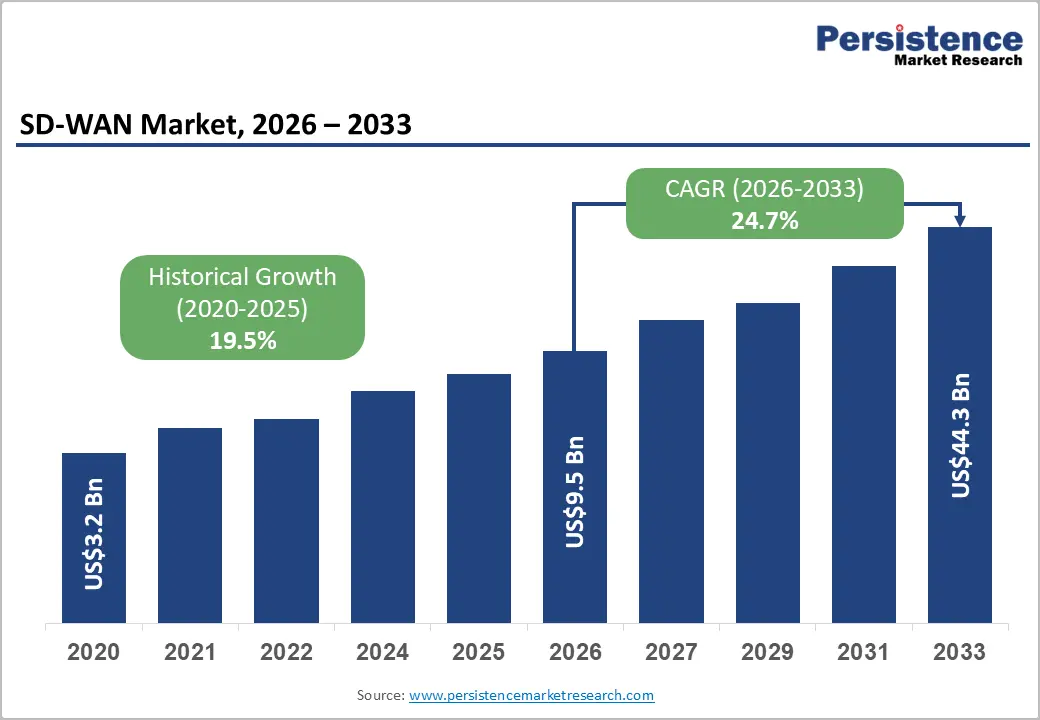

The global SD-WAN (Software-Defined Wide Area Network) Market size is projected to rise from US$9.5 Bn in 2026 to US$44.3 Bn by 2033. It is anticipated to witness a CAGR of 24.7% during the forecast period from 2026 to 2033. This growth reflects the shift in enterprise networking driven by cloud-native transformation, hybrid workforce adoption, and the need for cost-optimized, secure, high-performance connectivity. SD-WAN serves as a foundational technology enabling zero-trust security, AI-driven network intelligence, and distributed application optimization, making it an essential infrastructure component.

Key Industry Highlights:

- Leading Component: Solutions dominate the market with over 67% share in 2026, driven by enterprises’ need for centralized network control, application-aware routing, and cost-efficient connectivity across hybrid and multi-cloud environments. Services are the fastest-growing segment, supported by managed services and professional support for deployment, optimization, and continuous monitoring of complex WAN architectures.

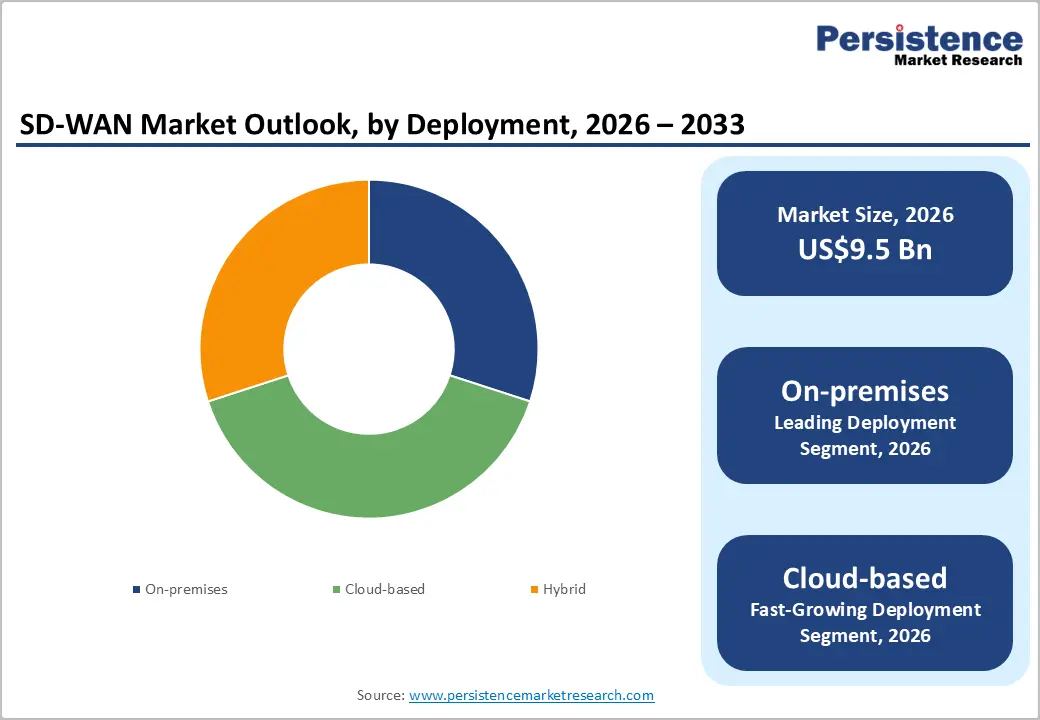

- Leading Deployment: On-premises holds over 30% market share in 2026, preferred for latency-sensitive and mission-critical applications, regulatory compliance, and tighter integration with legacy security stacks. Cloud-based deployments are the fastest-growing, fueled by scalable, flexible, and cost-effective WAN solutions, simplified management, and support for remote work and multi-cloud connectivity.

- Leading Enterprise Size: Large enterprises lead with more than 62% share in 2026, driven by the need for advanced WAN transformation, centralized control, and guaranteed performance for mission-critical workloads. SMEs are the fastest-growing segment, adopting subscription-based and managed SD-WAN services for cost-efficient, scalable, and easy-to-manage networking solutions.

- Leading Vertical: BFSI commands the largest share at over 26% in 2026, due to high demand for secure, low-latency, and resilient connectivity, regulatory compliance, and real-time transaction support. Retail & CPG is the fastest-growing sector with a CAGR of 28.9%, driven by omnichannel operations, cloud application adoption, and secure high-speed connectivity across multiple locations.

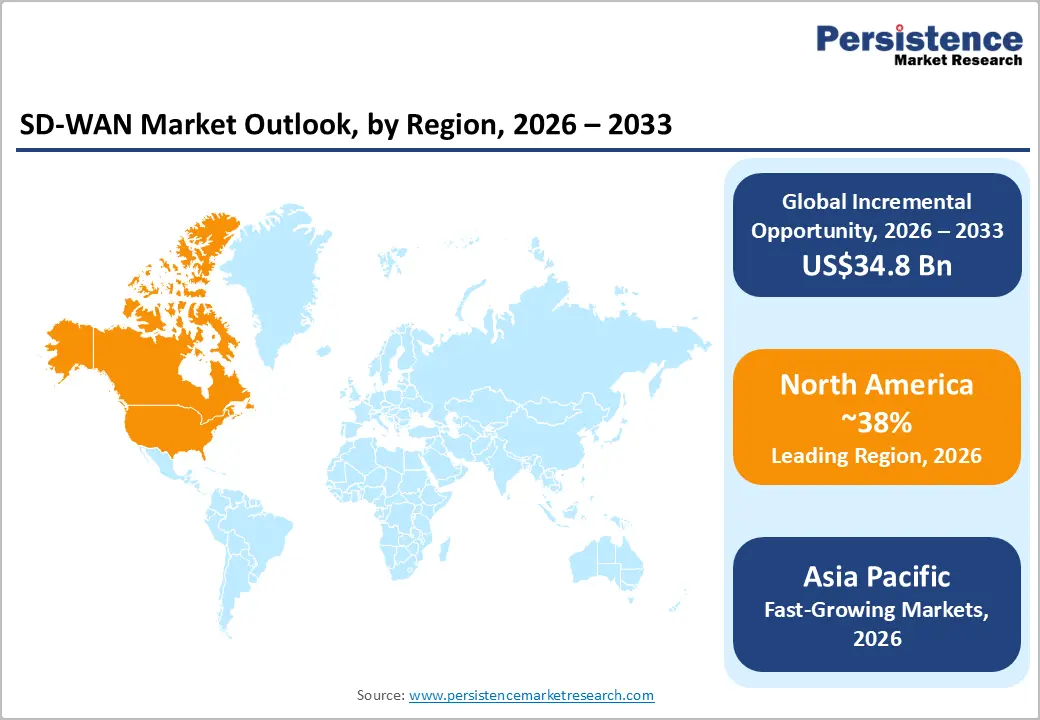

- Leading Region: North America leads with over 38% market share in 2026, valued at US$ 3.6 Bn, supported by mature cloud infrastructure, managed service ecosystems, and regulatory mandates driving zero-trust adoption. Asia Pacific is the fastest-growing region at a CAGR of 30.1%, fueled by digitalization, enterprise cloud adoption, 5G rollout, and government modernization initiatives. Europe holds more than 26% share, driven by GDPR, DORA regulations, and regional managed service adoption.

|

Global Market Attribute |

Key Insights |

|

SD-WAN Market Size (2026E) |

US$9.5 Bn |

|

Market Value Forecast (2033F) |

US$44.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

24.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

19.5% |

Market Dynamics

Driver

Zero-Trust Security Architecture and Regulatory Compliance Requirements

The shift from traditional perimeter-based security to zero-trust frameworks driven by regulatory standards such as NIST, PCI-DSS, and emerging healthcare and financial compliance mandates requires granular visibility, dynamic policy enforcement, and encrypted traffic inspection. SD-WAN platforms with integrated security simplify network architecture by consolidating security functions, enabling microsegmentation, context-aware access, and centralized control. This ensures consistent policy enforcement, detailed audit logging, and traffic visibility across distributed sites, helping organizations meet regulatory compliance in BFSI, healthcare, and government sectors. By combining zero-trust principles with SD-WAN, enterprises can modernize networks, optimize performance, reduce complexity, and streamline compliance management.

Hybrid Workforce Expansion and Remote Work Infrastructure Mandates

The shift toward hybrid and distributed work models is reshaping WAN requirements, as enterprises with 40–60% of their workforce working remotely need secure, high-performance connectivity. SD-WAN enables zero-trust access, integrated security, and centralized policy management, reducing IT complexity in managing dispersed endpoints. Cloud-based deployments simplify branch onboarding and remote connectivity without extensive on-premises infrastructure. SD-WAN’s application-aware routing ensures optimized performance for critical workloads like voice and video collaboration, maintaining service quality across geographically distributed locations.

Restraint

Internal Skill Gaps and Service Delivery Complexity

Internal skill gaps in design, deployment, and optimization hinder SD-WAN adoption, with over 70% of enterprises reporting limited expertise as a key challenge. Centralized orchestration, application performance optimization, and policy management remain concentrated among vendors and managed service providers, increasing implementation risks and extending deployment timelines. The complexity of SD-WAN, including cloud connectivity, edge integration, zero-trust enforcement, and multi-vendor interoperability often exceeds traditional WAN skills, forcing organizations to allocate 20–40% of total implementation costs to professional services, particularly affecting SMEs and mid-market IT budgets.

Legacy Infrastructure Interdependencies and Migration Risk

Legacy WAN infrastructure, multi-year MPLS contracts, and entrenched security solutions create significant barriers to SD-WAN adoption. Organizations with 100+ branch locations face 18–36 month transition periods due to application dependencies on specific network characteristics, risking disruption during migration. Maintaining parallel WAN connectivity further increases total cost of ownership and can extend break-even timelines by 12–18 months. Substantial investments in existing security platforms add integration complexity and organizational resistance, especially when current solutions perform adequately in non-cloud environments.

Opportunity

AI-Driven Network Intelligence and Autonomous Network Operations

The convergence of SD-WAN platforms with AI-driven network monitoring and autonomous operations presents a key technology differentiation and market expansion opportunity. AI-enabled SD-WAN solutions detect anomalies, optimize policies automatically, and support self-healing operations, addressing skill gaps and improving overall network performance. This integration opens new use cases in network security, capacity planning, and application performance optimization, providing organizations with stronger operational efficiency and faster incident resolution, which supports faster adoption and a broader market potential.

?Security Convergence Through SD?WAN & SASE

Enterprises are increasingly seeking simplified management, improved threat protection, and consistent policy enforcement across distributed locations and remote users. This integration enables secure direct-to-cloud access, reducing reliance on backhauling traffic through data centers and improving application performance. Vendors offering SD?WAN with built-in SASE (Secure Access Service Edge) capabilities capture new customers, expand services to SMEs, and differentiate in a competitive market. The also drives demand for subscription-based and managed SD?WAN services, accelerating adoption across industries.

Category-wise Analysis

Component Analysis,

Solution dominates the global market, capturing more than 67% of the market share in 2026, due to enterprises increasingly needing centralized network control, improved application performance, and cost-efficient connectivity across hybrid and multi-cloud environments. Organizations prioritize better security integration, simplified management, and real-time traffic optimization, all of which full SD-WAN solutions deliver. The emphasis on scalability and support for remote work further drives the adoption of complete solutions over standalone components.

Services are expected to grow at a significant rate driven by organizations increasingly rely on managed services and professional support to deploy, configure, and optimize SD-WAN solutions. Businesses often lack in-house expertise to handle complex WAN architectures, security integration, and cloud connectivity requirements. Managed services offer predictable costs, faster deployment, and continuous monitoring, addressing performance and reliability needs. Ongoing support and consulting help enterprises adapt to changing network demands, making services more critical than standalone hardware or software solutions.

Deployment Analysis,

On-premises hold over 30% market share in 2026, as organizations need direct control over network performance, security, and data locality, especially for latency-sensitive and mission-critical applications. Many organizations still rely on legacy infrastructure, private data centers, and MPLS networks, making on-prem deployment the least disruptive option. Regulatory and compliance requirements in sectors like BFSI, government, and healthcare also favor keeping traffic and policies within enterprise-controlled environments. On-prem SD-WAN supports customized routing, deep visibility, and tighter integration with existing security stacks, which cloud-only models cannot fully meet yet.

Cloud-based is expected to grow at the highest rate due to organizations increasingly needing scalable, flexible, and cost-effective network solutions to support remote work, multi-cloud environments, and branch connectivity. Cloud deployment reduces the need for heavy on-premises infrastructure, simplifies management through centralized control, and allows faster provisioning of new sites. It also provides real-time monitoring, automated policy enforcement, and improved security integration, which align with enterprises’ needs for agility, performance, and simplified IT operations.

Enterprise Size Analysis,

Large enterprises are expected to hold more than 62% in 2026, as their scale and complexity of their network needs demand advanced WAN transformation. They operate hundreds to thousands of distributed sites, requiring centralized control, application-aware routing, and guaranteed performance for mission-critical workloads. High adoption of cloud, SaaS, and hybrid IT architectures increases the need for intelligent traffic optimization and resilient connectivity. Large enterprises prioritize integrated security, compliance, and SLA-driven performance, making SD-WAN a strategic investment in infrastructure rather than a cost-saving tool.

Small & Medium Enterprises (SMEs) are expected to grow at the highest rate as they increasingly need cost-effective, scalable, and easy-to-manage networking solutions. SMEs often lack dedicated IT teams and prefer subscription-based or managed SD-WAN services that reduce complexity and upfront investment. The growing adoption of cloud applications, remote work, and SaaS platforms drives their need for reliable, secure, and high-performance WAN connectivity. Telecom providers and cloud marketplaces now offer SME-friendly SD-WAN solutions, accelerating adoption.

End User Analysis,

BFSI commands the largest market share at over 26% in 2026, due to its critical need for secure, low-latency, and highly resilient connectivity across branches, data centers, and cloud platforms. Banks and financial institutions rely on SD-WAN to support real-time transactions, digital payments, and core banking applications with guaranteed performance. The sector’s strict regulatory and compliance requirements drive demand for centralized visibility, traffic segmentation, and integrated security. Rapid expansion of digital banking, fintech partnerships, and omnichannel customer services increases network complexity, making SD-WAN essential for scalability and operational control.

Retail & CPG is expected to grow at a CAGR of 28.9% as these sectors increasingly rely on real-time data, cloud applications, and omnichannel operations to manage stores, supply chains, and customer experiences. SD-WAN enables secure, high-speed connectivity across multiple locations, supporting inventory management, digital payments, and personalized marketing. The need for seamless integration between physical stores and e-commerce platforms, along with cost-efficient network management, drives rapid adoption. SD-WAN improves network reliability for POS systems and IoT devices, which are critical for retail operations.

Regional Insights

North America SD-WAN Market Trends

North America holds over 38% share in 2026, reaching US$ 3.6 Bn value, driven by early vendor concentration, advanced cloud and broadband infrastructure, and enterprises’ capital availability for network modernization. The United States dominates regional adoption, accounting for over 78% of market value, supported by cloud hyperscaler infrastructure and enterprise cloud-first strategies. The region’s robust 4G/5G broadband enables enterprises to replace MPLS with cost-optimized alternatives. Regulatory frameworks, including PCI-DSS, HIPAA, and sector-specific compliance mandates, drive zero-trust security adoption, necessitating SD-WAN integration. Additionally, an established managed services ecosystem, with MSPs offering specialized SD-WAN expertise, accelerates adoption among mid-market organizations lacking internal capabilities.

Asia Pacific SD-WAN Market Trends

Asia Pacific is expected to grow at the highest rate with a CAGR of 30.1%, reflecting rapid digitalization and accelerating enterprise cloud adoption. China leads the region, driven by a robust digital economy, major cloud infrastructure investments, and government mandates promoting enterprise modernization. The country’s accelerated 5G deployment further enables enterprises to leverage high-bandwidth, low-latency connectivity for cloud applications. India shows growing adoption, supported by government digitization initiatives, a rapidly expanding IT services sector, and increasing enterprise reliance on hybrid cloud models. Japan and South Korea are advanced technology adopters, with high SD-WAN penetration in manufacturing and technology sectors, driven by robotics and IoT requirements demanding reliable, low-latency connectivity.

Europe SD-WAN Market Trends

Europe is expected to hold more than 26% share by 2026, driven by GDPR and DORA regulatory mandates that emphasize data sovereignty, network visibility, and operational transparency. Germany leads adoption, propelled by manufacturing sector digitalization and Industry 4.0 initiatives that require robust WAN infrastructure. France shows accelerating adoption supported by hybrid cloud strategies and application performance optimization, while the United Kingdom maintains stable growth with a focus on managed services. Overall, European enterprises demonstrate a strong preference for regional vendors and managed service providers, reflecting regulatory alignment and data sovereignty priorities.

Competitive Landscape

The SD-WAN market exhibits moderate-to-high consolidation. This concentration reflects substantial technology differentiation, switching costs inherent in enterprise deployments, and vendor investments in ecosystem development. The market includes specialist vendors with focused technology positions and major IT infrastructure vendors leveraging existing enterprise relationships. Companies are focusing on differentiation through advanced features like zero-trust security, AI-driven analytics, and multi-cloud optimization to stand out.

Key Industry Developments

- In June 2025, Cisco’s new network architecture includes SD-WAN and SASE-enabled secure routers, delivering high-throughput, low-latency connectivity and integrated security to support AI workloads across campus, branch, and industrial networks.

- In September 2024, Airtel Business, in partnership with Cisco, launched Airtel SD-Branch, a cloud-based, end-to-end managed network solution for enterprises. Powered by Cisco Meraki, it enables unified management of LAN, WAN, security, and connectivity across multiple branches, simplifying network operations and enhancing application performance.

Companies Covered in SD-WAN Market

- Cisco Systems, Inc.

- Palo Alto Networks

- Fortinet, Inc.

- Aryaka Networks, Inc.

- Barracuda Networks

- HPE

- VMware, Inc.

- Juniper Networks

- Cato Networks

- Citrix Systems, Inc.

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- Oracle Corporation

- CenturyLink, Inc.

- IBM Corporation

- Others

Frequently Asked Questions

The global market is projected to be valued at US$9.5 Bn in 2026.

The need for secure, reliable, and high-performance connectivity across multiple locations, along with simplified network management and optimized cloud application access, is a key driver of the market.

The market is expected to witness a CAGR of 24.7% from 2026 to 2033.

Increasing hybrid work models and the integration of AI-driven network management for enhanced performance and security are creating strong growth opportunities.

Cisco Systems, Inc., Palo Alto Networks, Fortinet, Inc., Aryaka Networks, Inc., Barracuda Networks, and HPE are among the leading key players.