- Medical Devices

- Nitrile Gloves Market

Nitrile Gloves Market Size, Share, and Growth Forecast, 2026 - 2033

Nitrile Gloves Market by Gloves Type (Powdered Nitrile Gloves, Powder-Free Nitrile Gloves), Grade (Medical Grade, Industrial Grade, Food Grade), End-user (Medical & Healthcare, Food Processing, Automotive, Chemical & Industrial, Others), and Regional Analysis for 2026 - 2033

Nitrile Gloves Market Share and Trends Analysis

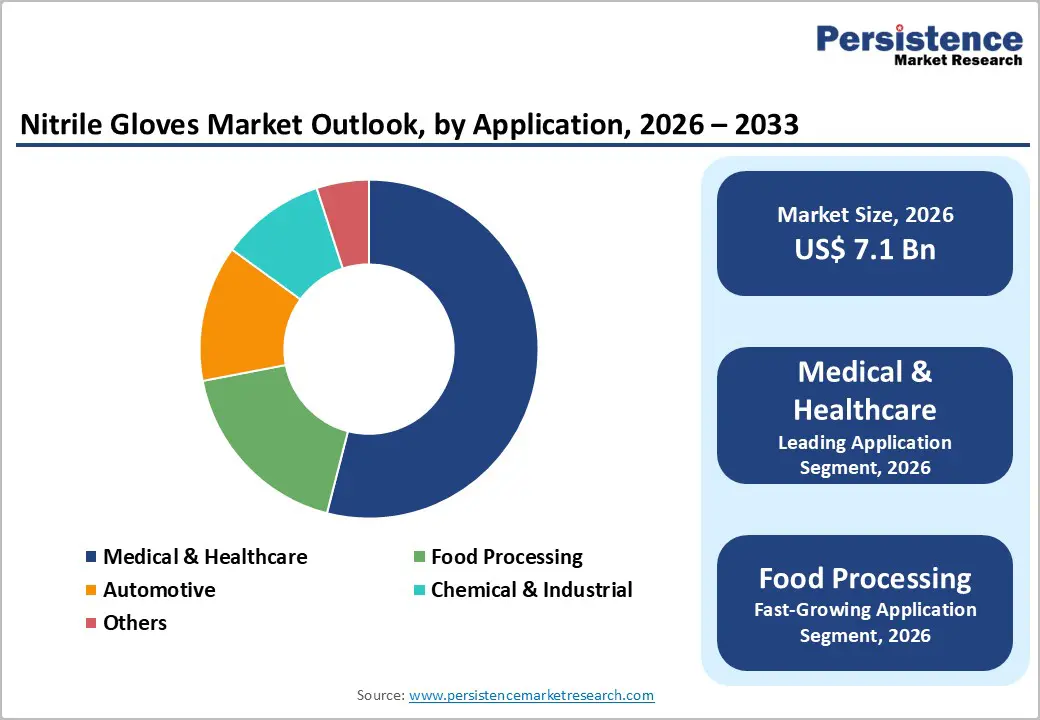

The global nitrile gloves market size is likely to be valued at US$7.1 billion in 2026 and is estimated to reach US$13.4 billion by 2033, growing at a CAGR of 9.5% during the forecast period from 2026 to 2033, driven by rising demand across healthcare, food processing, and industrial sectors.

An aging global population and the expansion of chronic disease management programs create sustained demand for examination and procedural gloves in clinical environments. Technological advancements in thin-wall nitrile formulation improve tactile sensitivity while retaining chemical resistance, broadening applicability across laboratory and surgical settings.

Key Industry Highlights:

- Leading Gloves Type: Powder-free nitrile gloves are set to hold around 72% revenue share in 2026, driven by universal FDA and EU regulatory enforcement of powder-free mandates across medical procurement channels.

- Fastest-growing Gloves Type: Powdered nitrile gloves are projected as the fastest-growing sub-segment, supported by residual industrial and food processing demand in cost-sensitive emerging market procurement environments.

- Leading Application: Medical and healthcare is estimated to hold roughly 54% revenue share in 2026, due to non-substitutable infection control mandates and high per-day glove consumption protocols across institutional care environments.

- Fastest-growing Application: Food processing is forecast to record the fastest growth, driven by tightening food hygiene standards globally.

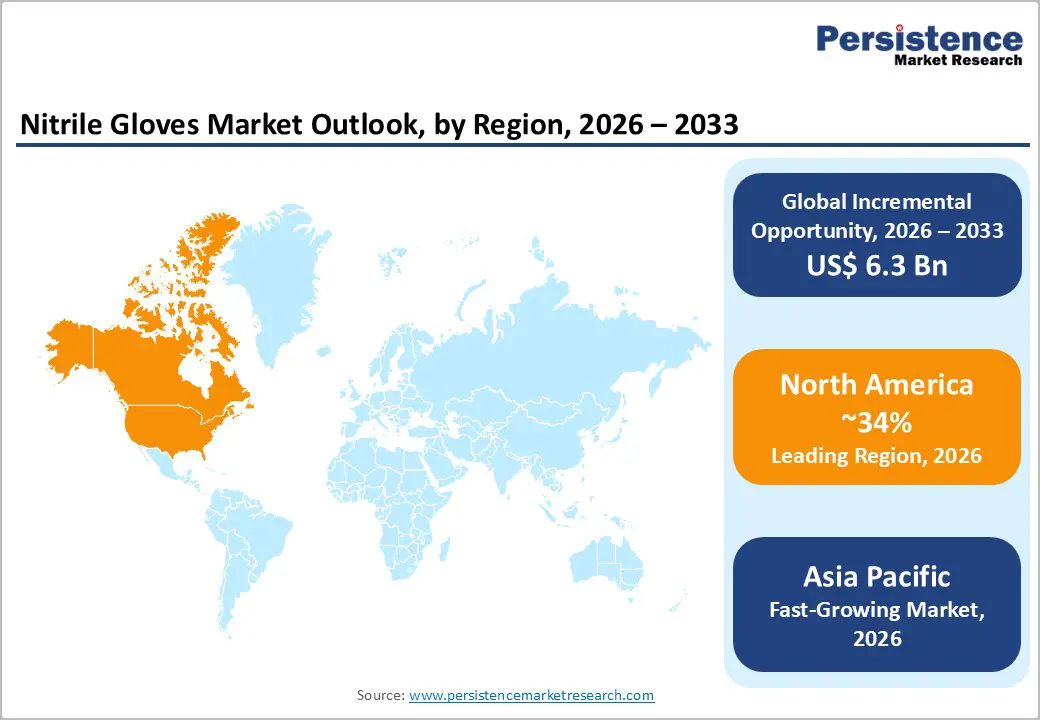

- Regional Leadership: North America is projected to capture approximately 34% of market share in 2026, while Europe is forecast to record the fastest regional growth due to full MDR enforcement and sustainable procurement mandates.

- Competitive Environment: The market reflects a moderately consolidated structure, with key players such as Top Glove, Hartalega, Kossan Rubber, Supermax, and Sri Trang Gloves leveraging scale, automation, and regulatory certification to maintain competitive positioning across global distribution channels.

DRO Analysis

Driver - Rising Incidence of Bloodborne Pathogen Exposure and Infection Control Protocols

Healthcare-associated infections (HAIs) represent a primary concern for hospital administrators and infection control committees globally. The U.S. Centers for Disease Control and Prevention (CDC) estimated in 2025 that approximately 1 in 31 U.S. hospital patients contracts at least one HAI on any given day, generating direct pressure on procurement teams to enforce single-use glove policies at every point of patient contact. This statistical burden translates into policy mandates that preclude reuse, thereby creating continuous replacement demand for nitrile examination gloves.

Bloodborne pathogen standards enforced by Occupational Safety and Health Administration (OSHA) under 29 CFR 1910.1030 require employers to provide appropriate barrier protection to workers exposed to blood or other potentially infectious materials. Compliance documentation requirements necessitate trackable, certified glove inventories, reinforcing the preference for nitrile over latex due to consistent allergy-free performance. The intersection of infection control science and occupational health regulation creates a demand structure that is resilient to economic cycles, as glove consumption in clinical settings is not discretionary.

Restraint - Volatility in Butadiene and Acrylonitrile Raw Material Prices

Nitrile Butadiene Rubber (NBR) synthesis depends on butadiene and acrylonitrile, both derived from petroleum and natural gas processing. Price volatility in crude oil markets introduces unpredictable cost structures for glove manufacturers, compressing operating margins during feedstock price spikes. Manufacturers operating on thin contract-pricing arrangements with government health agencies face particular difficulty in passing input cost increases downstream, reducing profitability and limiting capital available for capacity expansion.

Supply chain disruptions affecting petrochemical feedstock logistics, as observed during the 2021-2023 energy market dislocations, demonstrated the structural vulnerability of NBR-dependent industries. Manufacturers unable to hedge feedstock costs through long-term procurement agreements experience margin erosion that can delay planned capacity additions. This restraint disproportionately affects mid-tier producers in emerging markets, limiting their ability to scale in response to growing regional demand.

Opportunity - Technological Innovation in Sustainable and High-Performance Nitrile Formulations

Environmental sustainability regulations governing single-use plastics and synthetic polymers are creating a policy-driven incentive for manufacturers to develop biodegradable nitrile formulations. The European Union's Green Deal and Single-Use Plastics Directive are prompting procurement officers at healthcare institutions to evaluate lifecycle environmental impact alongside functional performance metrics. Manufacturers that successfully develop and certify bio-based or accelerated-degradation nitrile gloves stand to capture first-mover advantage in a regulatory environment that will increasingly differentiate between standard and sustainable product lines.

Demand from semiconductor manufacturing, pharmaceutical compounding, and biotechnology sectors for ultra-thin, chemically resistant gloves with enhanced tactile sensitivity creates a premium product opportunity. These applications command significantly higher average selling prices than standard examination gloves, providing margin diversification for manufacturers currently exposed to commodity pricing cycles. Investment in polymer chemistry R&D and cleanroom-compatible manufacturing certifications enables producers to address high-value industrial niches that are less susceptible to oversupply dynamics affecting the commodity segment.

Category-wise Analysis

Gloves Type Insights

Powder-free nitrile gloves are anticipated to secure around 72% of the nitrile gloves market share in 2026. Major hospital systems, such as Mayo Clinic, have codified powder-free procurement policies into all supply contracts, reinforcing this segment dominance. Regulatory compliance requirements eliminate powder-based alternatives from most institutional procurement processes.

Powdered nitrile gloves are expected to be the fastest-growing segment, propelled by residual demand in specific industrial and food-handling applications where doffing convenience and lower per-unit cost remain procurement priorities. Food processing facilities in Southeast Asia, such as large-scale seafood processing plants in Vietnam, continue to specify powdered variants for assembly-line workflows.

Grade Insights

Medical-grade nitrile gloves are poised to dominate with a forecast market share of over 61% in 2026, powered by universal adoption across surgical, examination, and diagnostic laboratory environments where FDA 510(k) or CE marking certification is a non-negotiable procurement requirement. Becton Dickinson and Cardinal Health have structured dedicated medical-grade supply agreements with major U.S. health systems, demonstrating the entrenched commercial relationships that sustain segment leadership.

Food-grade nitrile gloves are estimated to be the fastest-growing segment, fueled by the global expansion of processed food manufacturing and increasingly stringent food safety standards under frameworks such as the FDA Food Safety Modernization Act (FSMA) and the EU General Food Law Regulation 178/2002. Meat processing facilities in Brazil and poultry operations in Thailand represent high-volume procurement centers driving this growth. Consumer demand for certified food-safe packaging and preparation environments intensifies buyer pressure on food manufacturers to enforce certified glove usage throughout production lines.

End-User Insights

Medical and healthcare are likely to be the leading segment with a projected 54% of the nitrile gloves market share in 2026 due to the non-negotiable requirement for infection prevention across modern healthcare networks. Dental professionals utilize these hypoallergenic barriers during routine cleanings to isolate fluid transmission pathways safely. The continuous volume requirements of modern medicine maintain this high segment valuation.

Food processing is anticipated to be the fastest-growing segment, fueled by expanding food safety laws and globalized supply chain audits aiming to eliminate batch contamination. Commercial meat packaging facilities require workers to use color-coded nitrile barriers to prevent cross-contamination between raw processing zones. Heightened corporate liability standards accelerate adoption across commercial food operations.

Regional Insights

North America Nitrile Gloves Market Trends

North America is expected to lead with an estimated 34% of the nitrile gloves market share in 2026, supported by the largest concentration of accredited healthcare facilities globally, rigorous OSHA and FDA enforcement regimes, and a deep group purchasing organization (GPO) infrastructure that drives standardized nitrile glove adoption across thousands of institutional buyers.

U.S. Nitrile Gloves Market Insights

The U.S. is projected to expand through domestic manufacturing capacity additions and strict enforcement of federal worker protection codes. Federal supply chain initiatives encourage domestic production facilities to insulate local supply lines from international logistics bottlenecks. Advanced medical centers utilize high-tactility synthetic barriers to optimize outcomes during delicate surgical interventions.

Canada Nitrile Gloves Market Insights

Canada is forecast to see rising demand across pharmaceutical laboratories and research centers operating under strict contamination control standards. Provincial healthcare networks enforce uniform safety guidelines, accelerating the transition toward premium synthetic options over older natural rubber alternatives. Growing public investments in biotechnology infrastructure support this regional consumption path.

Europe Nitrile Gloves Market Trends

Europe is expected to hold a significant market share, driven by uniform occupational safety directives and comprehensive environmental protection frameworks across member states. Regional procurement policies prioritize manufacturing entities that comply with strict chemical registration, evaluation, and authorization codes. European automotive and chemical manufacturing sectors demand specialized, long-cuff protective variants.

Germany Nitrile Gloves Market Insights

Germany is likely to be the primary revenue contributor within Europe, driven by its extensive network of advanced acute care hospitals and specialized automobile assembly centers. High industrial safety standards require automated manufacturing facilities to supply certified hand protection for workers managing caustic cleaning agents. Advanced chemical distribution networks sustain steady industrial consumption.

U.K. Nitrile Gloves Market Insights

The U.K. is expected to experience steady consumption growth within outpatient healthcare facilities and decentralized community nursing programs. National healthcare sourcing frameworks emphasize supply chain visibility and product compliance certifications, stabilizing market parameters for authorized suppliers. Growing investments in specialized clinical research facilities further expand usage options.

Asia Pacific Nitrile Gloves Market Trends

Asia Pacific is projected to capture roughly 38% of global production capacity in 2026, with Malaysia and Thailand representing the dominant manufacturing centers supplying approximately 60% of world nitrile glove output. Domestic demand within the region is growing simultaneously, as expanding middle-income populations in Indonesia, India, and Vietnam support healthcare system investment that drives institutional glove procurement.

Malaysia Nitrile Gloves Market Insights

Malaysia is projected to maintain its role as a global production hub while expanding domestic automation to counter rising regional labor costs. Local manufacturing organizations integrate advanced dipping technologies to optimize export capabilities toward Western consumer markets. Strategic investments in infrastructure ensure consistent supply outputs.

China Nitrile Gloves Market Insights

China is forecast to see rapid internal demand generation due to expanding pharmaceutical manufacturing lines and strict new food hygiene standards implemented across urban centers. Massive chemical manufacturing complexes require industrial-strength hand barriers to minimize chemical burns and occupational health liabilities. Expanding provincial clinical networks increases overall healthcare consumption volumes.

Competitive Landscape

The global nitrile gloves market is moderately consolidated, with a small number of large-scale Malaysian and Thai manufacturers, including Top Glove Corporation, Hartalega Holdings, Kossan Rubber Industries, Supermax Corporation, and Sri Trang Gloves Thailand, collectively commanding a majority of global production and export volume.

Competitive differentiation is increasingly driven by product specialization, sustainability credentials, and geographic distribution reach rather than price alone. Mid-tier producers are pursuing niche positioning in chemically resistant industrial gloves, ultra-thin cleanroom variants, and accelerated-biodegradation formulations to escape commodity pricing dynamics.

Key Industry Developments:

- In May 2025, Wadi Surgicals launched India’s first accelerator-free nitrile gloves under the Enliva brand, strengthening skin-safe and allergy-free protection across healthcare, food processing, and industrial applications.

- In May 2025, Enliva announced the launch of accelerator-free nitrile gloves designed to improve skin safety and allergy protection for healthcare workers and industrial users.

- In March 2025, Top Glove launched ElastiCore accelerator-free nitrile examination gloves to enhance user comfort and reduce allergy risks across healthcare and laboratory applications.

Companies Covered in Nitrile Gloves Market

- Top Glove Corporation Berhad

- Hartalega Holdings Berhad

- Kossan Rubber Industries Berhad

- Supermax Corporation Berhad

- Sri Trang Gloves (Thailand) Public Company Limited

- Ansell Limited

- Medline Industries LP

- Cardinal Health Inc.

- Kimberly-Clark Corporation

- Mölnlycke Health Care AB

- O&M Halyard Inc.

- Protective Industrial Products Inc.

- Rubberex (M) Sdn Bhd

- Paul Hartmann AG

- Riverstone Holdings Limited

Frequently Asked Questions

The global nitrile gloves market is projected to reach US$7.1 billion in 2026.

Rising infection control requirements, expanding healthcare infrastructure, stricter industrial safety regulations, and increasing adoption of latex-free protective equipment drive the nitrile gloves market.

The nitrile gloves market is poised to witness a CAGR of 9.5% from 2026 to 2033.

Expansion in food processing, chemical manufacturing, and healthcare procurement programs, along with innovation in accelerator-free and sustainable nitrile gloves, creates key market opportunities.

Some of the key market players include Top Glove Corporation, Hartalega Holdings, Kossan Rubber Industries, Supermax Corporation, and Sri Trang Gloves Thailand.