- Metals & Minerals

- Refractories Market

Refractories Market Size, Share, and Growth Forecast, 2025 - 2032

Refractories Market By Form (Bricks and Shaped Refractories, Monolithic/Unshaped), Material Type (Clay-Based Refractories, Non-Clay Refractories), Alkalinity, End-user, and Regional Analysis for 2025 - 2032

Refractories Market Size and Trends Analysis

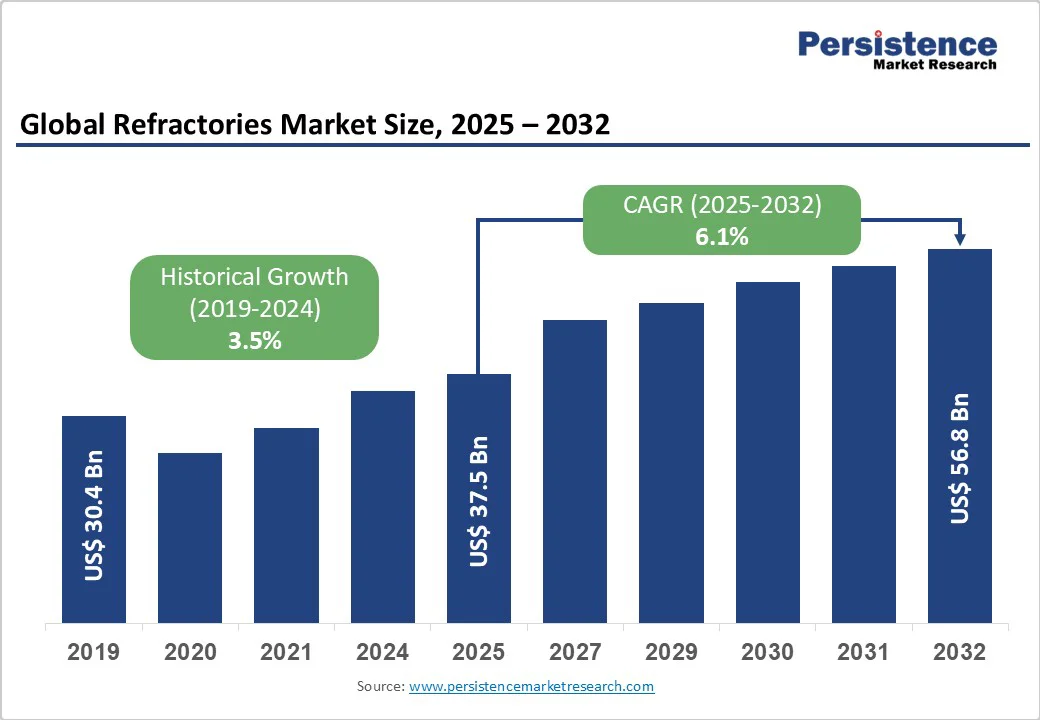

The global refractories market size is likely to be valued at US$37.5 Bn in 2025 and is expected to reach US$56.8 Bn by 2032, growing at a CAGR of 6.1% during the forecast period from 2025 to 2032, driven by the steady expansion of the steel, cement, glass, and non-ferrous metals industries, which rely heavily on refractory linings for thermal insulation and mechanical resistance in extreme temperature operations.

The market also benefits from ongoing modernization in steel manufacturing, the emergence of electric arc furnaces (EAFs), and the adoption of circular-economy initiatives that promote recycling of used refractories.

Key Industry Highlights

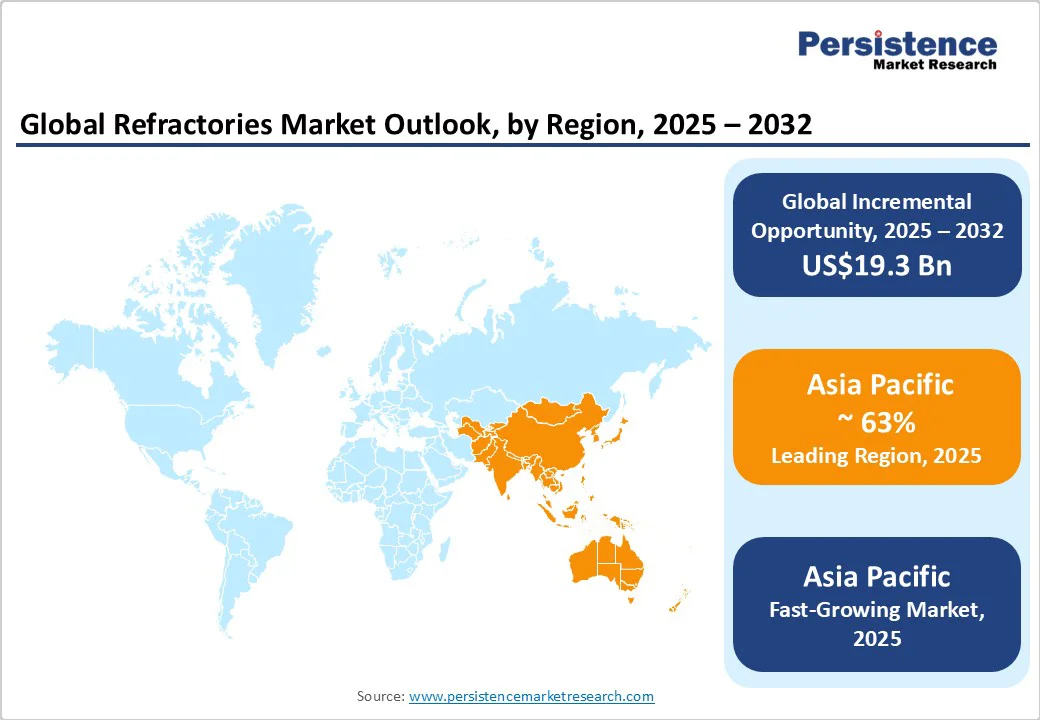

- Leading Region: Asia Pacific, accounting for approximately 63% of the global revenue in 2025, driven by China, India, and Japan.

- Fastest-Growing Region: Asia Pacific, fueled by industrial expansion, infrastructure development, and green-steel initiatives.

- Investment Plans: Strategic expansions by RHI Magnesita, Calderys, and POSCO Chemical, including new plants in China’s Liaoning Province (2023), India (Calderys-Krosaki JV), and the POSCO Pohang expansion (2024), targeting high-performance refractory production and low-carbon solutions.

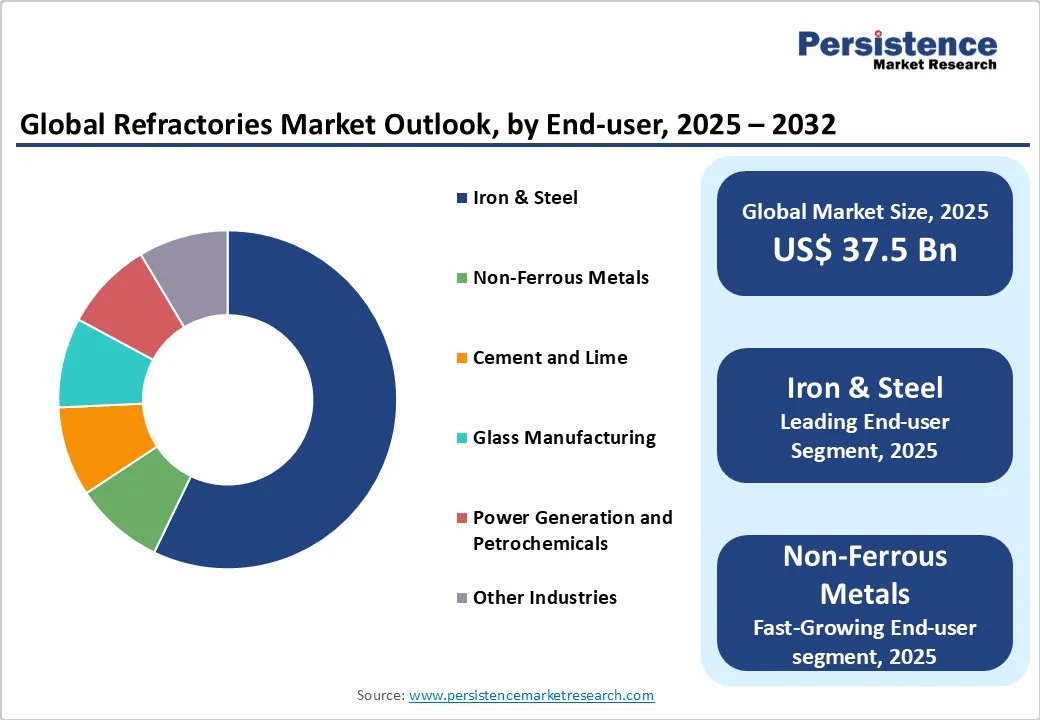

- Dominant Product Type: Clay-based Refractories, with approximately 55.1% of global market volume in 2025, preferred for moderate-temperature applications in cement, glass, and power-generation industries.

- Leading End-user: Iron & Steel, representing over 60.4% of global refractory demand, supported by high-temperature furnace operations and ongoing replacement cycles in Asia and the Middle East.

| Key Insights | Details |

|---|---|

|

Refractories Market Size (2025E) |

US$37.5 Bn |

|

Market Value Forecast (2032F) |

US$56.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Steel Sector Demand and Transformation

The iron and steel industry remains the largest consumer of refractories, accounting for nearly 60–65% of the global demand. Rising global steel production and the growing use of EAF-based steelmaking are fueling continuous refractory replacement cycles. EAFs, which require higher heat-resistant materials, demand frequent lining replacements due to the dynamic thermal environment. This shift enhances the consumption of basic refractories such as magnesia and dolomite, alongside advanced alumina-based monolithics. The expansion of steel capacity across Asia, Europe, and North America under sustainability mandates ensures consistent medium-term growth for refractory suppliers.

Industrialization in Asia Pacific

Asia Pacific represents approximately two-thirds of global refractory consumption, led by China, India, and Southeast Asian nations. China’s large-scale metallurgical infrastructure and India’s increasing investment in infrastructure and manufacturing underpin the region’s leading position. Robust growth in cement production, base-metal smelting, and non-ferrous metallurgy supports demand for both shaped and unshaped refractory forms. Government initiatives encouraging domestic production and capacity upgrades provide long-term growth opportunities for local manufacturers, while global companies are expanding their manufacturing footprint locally to serve these rapidly industrializing markets.

Sustainability and Refractory Recycling

Sustainability has become a structural driver in the refractory industry. Companies are now investing in recycling programs that recover used refractory materials, lowering waste generation and dependence on virgin minerals. Increasing pressure from environmental regulations, especially in Europe and North America, is accelerating this transition. Recycling can reduce raw-material costs by up to 20–25% and enhances corporate ESG performance. The evolution of refractory circular-economy systems, integrating collection, processing, and remanufacturing, is emerging as one of the most significant innovation avenues within the industry.

Barrier Analysis - Raw-Material Price Volatility

The refractory industry relies on alumina, magnesia, and specialty minerals that are sourced from limited global suppliers. Price fluctuations in these minerals, combined with energy cost volatility, directly impact production economics. Any disruption in mining or transportation leads to supply shortages and affects delivery schedules for downstream customers. Smaller manufacturers often struggle to hedge raw-material risks, compressing profit margins and discouraging long-term investment in product development.

Cyclical End-Market Exposure

Refractories are highly dependent on the performance of heavy industries such as steel, cement, and glass. During downturns in construction or industrial output, replacement cycles are delayed, leading to revenue contraction. Market fluctuations in steel production, for instance, directly reduce refractory consumption. This cyclical exposure increases working capital requirements and complicates production planning for suppliers, especially those with limited geographic diversification.

Opportunity Analysis - Premium Engineered Refractories and Services

As industries modernize, there is increasing demand for engineered refractories offering superior chemical resistance, longer life, and predictive-maintenance features. The integration of digital monitoring, remote temperature sensing, and predictive maintenance contracts transforms refractories from one-time consumables into service-based offerings. Premium engineered products could capture an incremental 7–10% share of total market revenue over the next decade. Companies investing in R&D and technical-service divisions are best positioned to benefit from this high-margin opportunity.

Recycled and Circular Refractory Solutions

Recycling represents a substantial untapped revenue stream. Capturing even 10–15% of refractory waste for reprocessing and resale could create a multi-billion-dollar submarket by 2030. European regulatory frameworks, corporate ESG mandates, and waste-management incentives are already driving significant investment in refractory reclamation plants. Companies establishing closed-loop recycling and supply agreements with large steel and cement producers will secure cost advantages and long-term customer retention.

Category-wise Analysis

Product Type Insights

Clay-based refractories such as fireclay bricks, insulating firebricks, and silica-alumina blends account for around 55.1% of global refractory volume in 2025. Preferred for applications between 1,200°C and 1,700°C, they are used in cement kilns, lime shafts, glass tanks, and thermal plants. Their cost-effectiveness, easy production, and versatility make them ideal for mid-scale industries. India and China lead in production due to abundant clay reserves, while companies such as TRL Krosaki and IFGL serve key sectors locally. In the U.S., HarbisonWalker International employs clay-based bricks for boilers and kilns, valued for their durability, thermal shock resistance, and dependable performance.

Non-clay or high-performance refractories, made from alumina, magnesia, zirconia, chromite, silicon carbide, and spinel, are seeing strong demand growth due to their superior resistance to corrosion, abrasion, and temperatures above 1,800°C. High-alumina bricks are widely used in electric arc furnaces and steel ladles for their long life and reliability. Magnesia-carbon bricks offer excellent slag resistance and reduced maintenance in steelmaking. Zirconia-based refractories are favored in glass and petrochemical industries for their durability against molten glass corrosion. Saint-Gobain SEFPRO’s fused-cast zirconia products enhance float glass furnace performance, ensuring consistent quality and improved operational efficiency.

End-user Insights

The iron and steel industry remains the largest end-user, accounting for over 60.4% of global refractory demand in 2025. Refractories are essential across every stage of steelmaking, from blast and basic oxygen furnaces to electric arc furnaces (EAFs), ladles, and tundishes, where they withstand temperatures beyond 1,600°C. Continuous wear from molten metal and slag necessitates frequent relining, driving steady demand for both shaped and unshaped refractories. In Asia, Baowu Steel Group and JSW Steel together consume millions of tons annually, using magnesia-carbon, alumina-magnesia, and dolomite-based products to maintain thermal integrity and minimize downtime. In Europe, ArcelorMittal’s collaboration with Vesuvius plc focuses on advanced linings to enhance steel purity and reduce energy use.

The non-ferrous metals sector is the fastest-growing consumer, driven by infrastructure growth, decarbonization, and recycling initiatives. Refractories are vital for smelting and refining aluminum, copper, nickel, and zinc, with alumina-spinel and silica-based materials used in electrolytic cells and rotary furnaces. Companies such as Hindalco Industries and Rio Tinto are adopting high-performance refractories to improve smelter efficiency and extend furnace life, reflecting the shift toward cleaner, more energy-efficient industrial operations.

Regional Insights

Asia Pacific Refractories Market Trends- High-Volume Demand, Green Steel Drive, and Innovation Leadership

Asia Pacific dominates the global refractory market, contributing 63% of total revenue in 2025. Growth is driven by China, India, Japan, South Korea, and ASEAN nations, which lead in steel, cement, and non-ferrous metal production. Asia Pacific is also the fastest-growing region. China alone accounts for over half of global refractory demand, supported by robust steel output and infrastructure expansion. Under its 14th Five-Year Plan, China is replacing outdated linings with energy-efficient, low-carbon solutions. Domestic firms such as Lier Refractory and Puyang Refractories partner with Baowu Group and HBIS to develop advanced magnesia-carbon and alumina-spinel products for green-steel applications.

India, the world’s second-largest steel producer, is witnessing rising refractory demand driven by expansions at Tata Steel, JSW Steel, and SAIL. Initiatives such as “Make in India” and the National Infrastructure Pipeline (NIP) are fueling growth across cement, power, and metals, boosting refractory use. Cement leaders such as UltraTech, Shree Cement, and ACC are adopting phosphate-bonded and spinel-reinforced castables for improved kiln durability. Japan and South Korea emphasize innovation, with Krosaki Harima, Shinagawa Refractories, and Posco Chemical producing advanced alumina-spinel bricks and corrosion-resistant linings. In 2024, POSCO Chemical expanded its Pohang plant for low-carbon steel materials.

North America Refractories Market Trends- EAF Expansion, and Eco-Efficient Refractories

North America holds a moderate but steadily expanding share of the global refractory market. The U.S. dominates regional demand, driven by the resurgence of electric-arc-furnace (EAF) steelmaking, growing emphasis on sustainable industrial operations, and renewed infrastructure investments. Legislative measures such as the Infrastructure Investment and Jobs Act (IIJA) and the Inflation Reduction Act (IRA) are catalyzing upgrades across cement, power, and metallurgical plants, resulting in significant refractory replacement cycles. U.S. steelmakers, including Cleveland-Cliffs and Nucor Corporation, are expanding EAF operations to reduce carbon intensity, which has increased demand for high-performance magnesia-carbon and alumina-spinel refractories capable of withstanding dynamic heat loads.

The cement and lime industries also contribute to growth, with aging kilns in states such as Texas, Missouri, and Alabama undergoing modernization using low-cement castables and high-alumina bricks to improve energy efficiency and extend service life. In addition, regional acquisitions, such as RHI Magnesita’s 2023 purchase of Resco Products, have strengthened supply chains and secured domestic raw-material sources, aligning with industry initiatives favoring near-sourcing to reduce logistics costs and carbon emissions. The ongoing transition toward eco-efficient refractories positions North America as a center for technological adoption and process innovation.

Europe Refractories Market Trends - Green Steel, Circular Economy, and Refractory Recycling

Europe represents a technologically advanced and sustainability-focused refractory market shaped by strict EU environmental norms and circular-economy principles. Key markets—Germany, France, Italy, Spain, and the U.K.—are investing in furnace upgrades and low-carbon technologies. Germany leads demand through its steel, automotive, and glass industries, with projects such as thyssenkrupp’s hydrogen-based “tkH2Steel” and Salzgitter’s SALCOS driving the need for high-purity magnesia and spinel refractories. France and Italy, under CEMBUREAU’s Carbon Neutrality Roadmap, are modernizing cement production, boosting demand for alkali-resistant castables and durable monolithic linings.

Regulatory alignment under the EU Green Deal and Circular Economy Directive has accelerated the adoption of refractory recycling and secondary raw material utilization. Companies such as Imerys Refractory Minerals and Calderys (Saint-Gobain Group) have scaled operations for spent-refractory collection and reprocessing, thereby reducing landfill waste and CO? emissions. Recent developments include RHI Magnesita’s 2024 inauguration of a low-carbon magnesia plant in Hochfilzen, Austria, the 2023 launch by Vesuvius plc of data-driven furnace monitoring systems in partnership with Tenaris, and Refratechnik Holding GmbH’s 2024 collaboration with CEMEX Europe to co-develop low-NO? kiln linings.

Competitive Landscape

The global refractory market displays moderate concentration, with a few integrated players dominating high-end engineered products and a fragmented base of smaller regional producers serving commodity applications. Major companies such as RHI Magnesita, Vesuvius, Saint-Gobain (Calderys/SEFPRO), Krosaki Harima, Shinagawa, and Imerys collectively control over 40% of global revenue. Integration of raw-material sourcing, service networks, and recycling facilities enhances competitive positioning.

Leading companies are focusing on product-service bundling, digital monitoring of furnace linings, and closed-loop recycling partnerships with end users. Strategies emphasize innovation, cost optimization, and regional diversification, ensuring resilience against raw-material volatility and cyclical downturns.

Key Industry Developments

- In March 2025, RHI Magnesita inaugurated a new low-carbon magnesia production plant in Hochfilzen, Austria, integrating renewable energy in sintering operations to enhance sustainability and reduce carbon emissions in Europe’s steel and cement sectors.

- In January 2025, Vesuvius plc launched advanced data-driven furnace monitoring systems in collaboration with Tenaris, aimed at optimizing refractory lifecycle management and improving operational efficiency in EAF steelmaking facilities globally.

Companies Covered in Refractories Market

- RHI Magnesita

- Vesuvius plc

- Saint-Gobain

- Calderys

- HarbisonWalker International

- Plibrico Company LLC

- Krosaki Harima Corporation

- Shinagawa Refractories

- Imerys Refractory Minerals

- Refratechnik Holding GmbH

- Lier Refractory

- Puyang Refractories Group

- Luoyang Institute of Refractories Research Co. Ltd.

- TRL Krosaki Refractories

- IFGL Refractories

- Posco Chemical

- Fives Stein

- Morgan Advanced Materials

- Magnesita Refratários S.A.

- CoorsTek Inc.

Frequently Asked Questions

The market size is estimated at US$37.5 Bn in 2025.

The market is projected to reach US$56.8 Bn by 2032, reflecting sustained demand across steel, cement, and non-ferrous industries.

Key trends include increasing adoption of high-performance, non-clay refractories in the steel and glass industries and the growth of electric-arc-furnace (EAF) steelmaking and green-steel initiatives.

The iron & steel industry is the leading end-user segment, accounting for over 60.4% of global demand. Among product types, clay-based refractories dominate, with approximately 55.1% of the global volume.

The refractories market is expected to grow at a CAGR of 6.1% between 2025 and 2032.

Major companies include RHI Magnesita, Vesuvius plc, Saint-Gobain/Calderys, and HarbisonWalker International.