- Medical Devices

- Gamma Knife Market

Gamma Knife Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Gamma Knife Market by Device Range (High-End Gamma Knife, Medium Gamma Knife, Low Gamma Knife), Disease Indication (Brain Metastasis, Arteriovenous Malformation (AVM), Malignant & Benign Tumors, Trigeminal Neuralgia, Vascular Disorders, Ocular Diseases, Others), End-User (Hospitals, Ambulatory Service Centers, Specialty Clinics), and Regional Analysis for 2025 - 2032

Gamma Knife Market Share and Trends Analysis

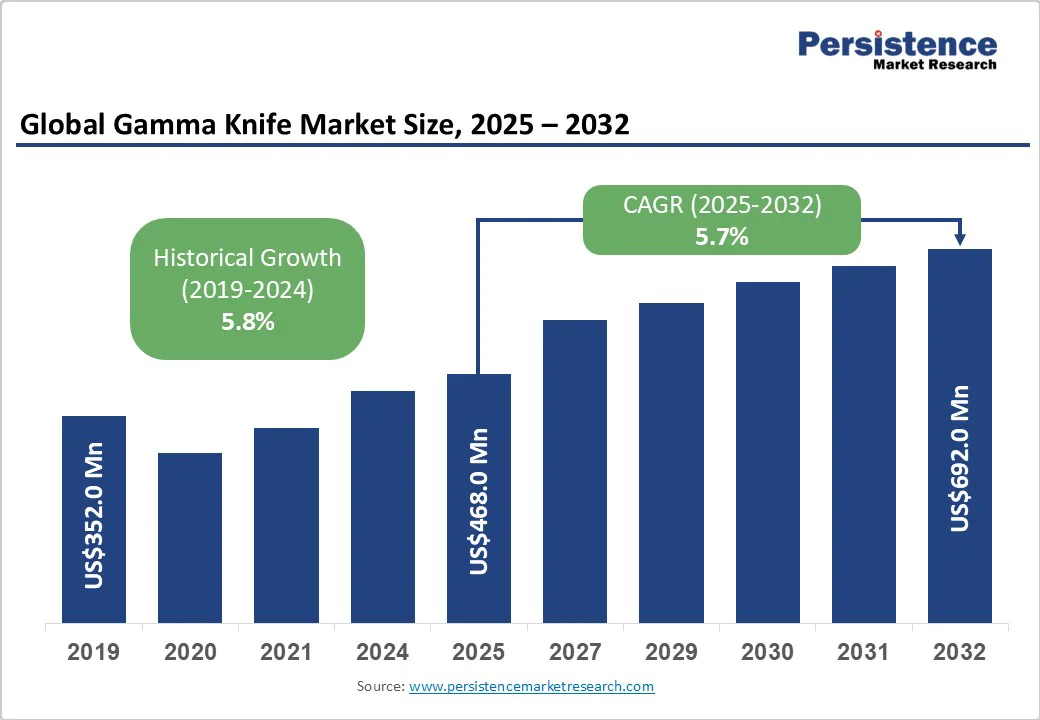

The global gamma knife market size is likely to be valued at US$468.0 Mn in 2025. It is estimated to reach US$692.0 million by 2032, growing at a CAGR of 5.7% during the forecast period of 2025 -2032, fueled by the convergence of rising neurological disease incidence, increased adoption of minimally invasive radiosurgery, and an expanding aging population requiring advanced therapies.

Key Industry Highlights

- Leading Region: North America maintains a substantial 2025 share of 31.0%, benefiting from insurance reimbursement and public health investment.

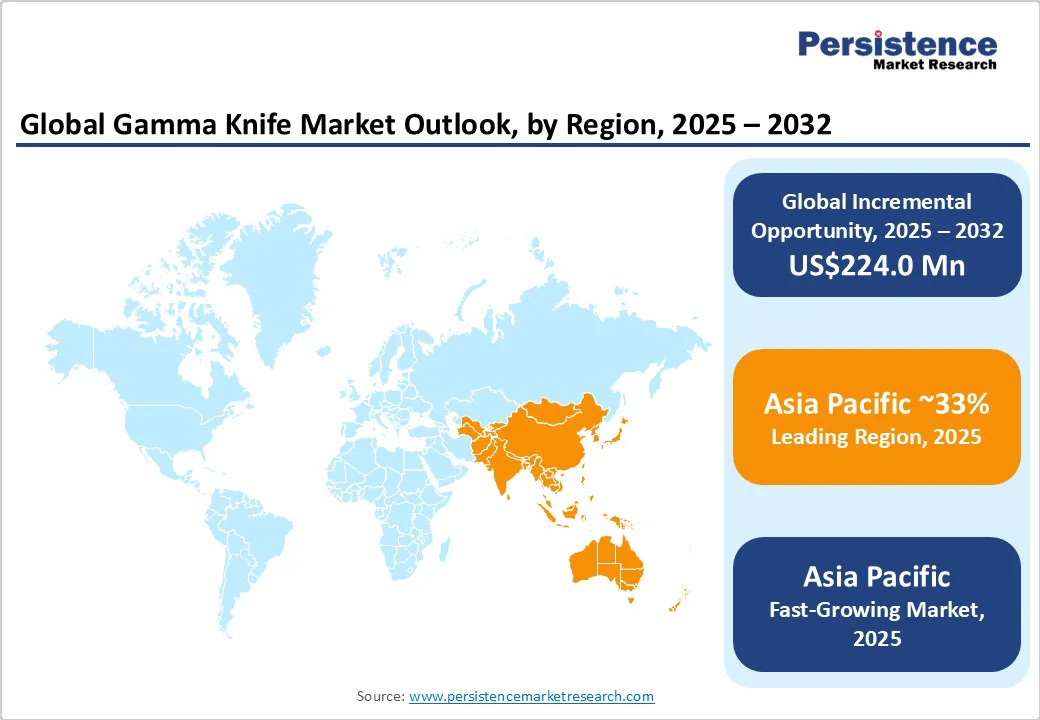

- Fast-Growing Region: Asia Pacific is set to become the largest regional market with a 33.0% share in 2025 and is likely to register the highest CAGR of 9.6% through 2032, fueled by rapid hospital construction and device installation.

- Market Innovation: Elekta, Varian Medical, and Huiheng Medical are the industry leaders, with innovations in imaging and AI positioning them for continued growth.

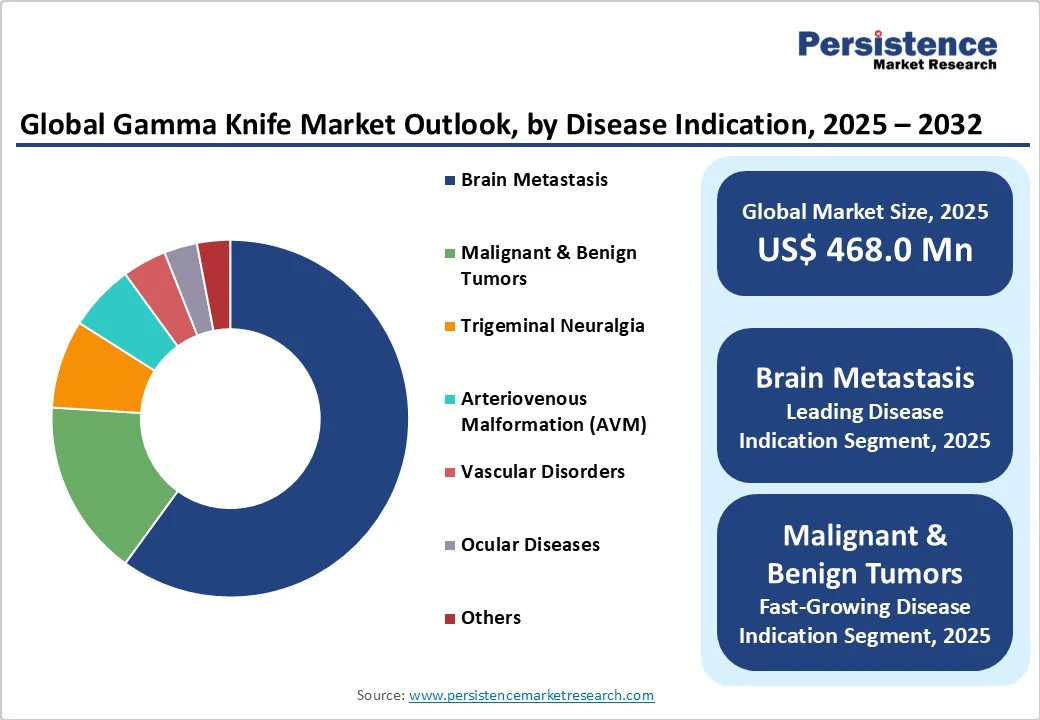

- Leading Disease Indication: Brain metastasis leads with more than 60.0% market share in 2025 and is expected to grow at a CAGR of 6.5% between 2025 and 2032 as cancer prevalence rises globally.

- Dominant Device Range: High-end gamma knife systems account for nearly 55.0% of the revenue share in 2025, driven by large hospitals embracing technological innovation.

| Key Insights | Details |

|---|---|

| Gamma Knife Market Size (2025E) | US$ 468.0 Mn |

| Market Value Forecast (2032F) | US$ 692.0 Mn |

| Projected Growth (CAGR 2025 to 2032) | 5.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.8% |

Market Dynamics

Market Drivers - Technological Advancements and Procedure Preference

Continuous innovation in gamma knife systems is enhancing treatment precision, patient safety, and clinical outcomes. The non-invasive nature and micro-precision of stereotactic radiosurgery significantly reduce hospital stay lengths compared to conventional neurosurgical approaches. The introduction of Leksell Gamma Knife models, which feature integrated MRI and advanced dose-planning software, is projected to further accelerate adoption.

Industry experts from the American Society for Radiation Oncology report that over 88,000 annual Gamma Knife surgeries are performed globally, indicating robust clinical demand. As procedures shift from inpatient neurosurgery to outpatient radiosurgery, payers and hospitals report up to 15% cost savings per patient, improving operating margins and reinforcing the transition towards advanced radiosurgical modalities.

Rising Prevalence of Brain Tumors and Neurological Disorders

According to the International Agency for Research on Cancer (IARC) of the World Health Organization (WHO), in 2022, 20 million new cancer cases were diagnosed, and 9.7 million people died from cancer worldwide. The National Brain Tumor Society notes over 700,000 cases of primary brain tumors in the United States in 2024, with a predicted annual increase of 87,000 new diagnoses.

Aging demographics and higher rates of neurological conditions, such as trigeminal neuralgia and vascular malformations, continue to boost market demand. Actionable insights from Frost & Sullivan indicate that more than 60% of gamma knife procedures in 2025 will target brain metastases, resulting in high-volume demand across tertiary care centers.

Market value-added analysis suggests this clinical focus will represent nearly 55% of global market revenues through 2032, underpinning growth.

Regulatory Support and Healthcare Infrastructure Enhancement

National regulatory bodies, including the FDA and the European Medicines Agency (EMA), are fast-tracking the approval of minimally invasive radiosurgical devices to address urgent clinical needs, particularly in neuro-oncology. This policy momentum aligns with OECD and World Bank reports that highlight strong public and private investments in medical device innovations, particularly in the Asia Pacific and North America.

Data aggregation from various market analyses suggests that favorable reimbursement and expanded insurance coverage for stereotactic radiosurgery are increasing accessibility, particularly in high-income economies. Strategic industry positioning in countries such as Japan and South Korea is leveraging robust healthcare spending, exceeding US$500 billion annually, which offers new market penetration avenues and accelerates the adoption cycle of gamma knife technologies.

Market Restraints

High Capital Costs and Cost Recovery

Gamma knife systems represent a substantial capital investment, with each unit costing upwards of US$4 million, including acquisition, installation, and certification. According to Deloitte and KPMG analyses, facility retrofitting and staff training entail additional costs, typically extending the return-on-investment period to five to seven years.

Despite favorable reimbursement frameworks in North America and Western Europe, several secondary and tertiary care hospitals in emerging geographies face barriers in securing financing for equipment procurement, thereby constraining market penetration and widening equity gaps in access to advanced care.

Regulatory and Skill Shortages

Stringent regulatory standards imposed by the FDA, EMA, and equivalent agencies in China and India require exhaustive clinical trial evidence for approval, which can slow the time-to-market by up to three years for new gamma knife models.

In addition, the World Bank and the American Hospital Association report critical shortages in skilled neurosurgeons and radiation oncologists trained in stereotactic radiosurgery, especially in Latin America, Africa, and the ASEAN region, leading to underutilization of installed capacity and operational inefficiencies. Risk quantification from BCG indicates up to 30% of gamma knife devices in some areas remain underutilized due to regulatory and talent bottlenecks.

Market Opportunities

Emerging Markets and Infrastructure Development

Frost & Sullivan and the World Health Organization underscore robust opportunities across the Asia Pacific, where expanding public sector investments into oncology and neurosurgical infrastructure are increasing market accessibility.

China, India, and ASEAN nations are expected to represent over 42% of the incremental global market revenue from 2025 to 2032, driven by hospital network expansion, affordable financing, and government-backed technology adoption programs. Market sizing estimates suggest an additional US$120 million in revenue potential by 2032, with installed base growth rates of over 15% CAGR in Tier-1 cities across Asia.

Integration with Advanced Imaging and Treatment Modalities

The integration of MRI-guided gamma knife and AI-powered dose-planning is expected to revolutionize therapeutic approaches, improving lesion targeting and patient outcomes.

Technology convergence with platforms such as robotic positioning and real-time imaging will drive a 12% CAGR in hybrid device sales from 2025 to 2032. Hospitals that leverage these new modalities can expect a 20% acceleration in procedure volumes and a 17% improvement in long-term patient outcomes, supporting the development of a business case for capital investments.

Unmet Needs in Pediatric and Rare Neurological Disorders

The European Society for Pediatric Neurosurgery reports significant gaps in access to stereotactic radiosurgery for children with rare vascular malformations and genetic neurodisorders.

Policy alignment and targeted investment in specialized gamma knife centers could unlock market value exceeding US$65 million through 2032, according to a PwC model. Strategic expansion into these specialty therapeutic areas will be driven by government research grants, non-profit collaborations, and evolving reimbursement policy, supporting sustainable margin growth.

Category-wise Analysis

Disease Indication Insights

In 2025, the brain metastasis segment is holding the largest share, accounting for more than 60.0% of the total market revenue, supported by the increasing prevalence and high clinical need in neuro-oncology worldwide. The aging population and rising cancer incidence are sustaining segment dominance, with North America performing particularly well in tertiary care.

Fastest growth is appearing in the malignant and benign tumor sub-segments, posting a CAGR of around 6.5% over 2025 - 2032, as newer indications for functional disorders and vascular malformations continue to emerge and broaden access for previously underserved patient groups.

Device Range Insights

The high-end gamma knife systems segment is leading with nearly 55.0% market share in 2025, underpinned by premium adoption in academic medical centers, oncology specialty hospitals, and large neurosurgical networks.

These systems, equipped with integrated MRI and AI-powered dose planning, support precision treatment and higher patient throughput, resulting in up to a 20% improvement in operational margins compared to standard devices. The medium-range segment is forecasted to be the fastest growing, posting a CAGR of 7.1% between 2025 and 2032, as mid-tier hospitals in the Asia Pacific and Europe invest in affordable, scalable technology platforms.

End-user Insights

Hospitals remain the dominant end-user segment, commanding a close to 70.0% share in 2025, as they continue to invest in centralized radiology and outpatient centers. This is reinforced by favorable reimbursement frameworks and the expansion of hospital networks in key growth markets.

Ambulatory service centers and specialty clinics demonstrate the most rapid expansion, achieving a CAGR of 8.1% across the forecast period 2025 - 2032, as procedural outsourcing and non-inpatient care models proliferate due to evolving consumer preferences and regulatory flexibility.

Regional Market Insights

North America Gamma Knife Market Trends

North America is set to maintain its strong position with approximately 31.0% gamma knife market share in 2025, valued at nearly US$145 million. The United States, in particular, is driving growth through investments in academic medical centers, cutting-edge research, and the presence of established device manufacturers such as Elekta and Varian.

The supportive regulatory framework established by the FDA, combined with Medicare and Medicaid reimbursements for radiosurgical procedures, results in robust device sales and high clinical adoption rates. The competitive landscape is highly consolidated, with top-tier hospitals controlling over 65% of device installations.

Investment trends further reflect private equity inflows and hospital system consolidations, creating opportunities for expansion in suburban and rural networks. Canada is also seeing moderate growth due to provincial public health system support.

Europe Gamma Knife Market Trends

Europe is expected to hold a substantial share of approximately 29.0% in 2025, with the regional market size reaching about US$136 million. Germany, the U.K., France, and Spain account for the majority of regional deployments, driven by high insurance penetration and robust public healthcare funding. Market growth is propelled by regulatory harmonization efforts among the EMA and national agencies, supporting the timely approval and adoption of new devices.

Fragmented competitive dynamics allow for local specialty clinics and regional hospital chains to play a significant role, while merger & acquisition (M&A) activities are focused on cross-border expansion and technology sharing. Europe gamma knife market also benefits from both domestic manufacturing and favorable cost structures, supporting sustained investment and device uptake.

Asia Pacific Gamma Knife Market Trends

Asia Pacific is emerging as the largest and fastest-growing regional market, representing a nearly 33.0% share in 2025. China, Japan, and India are leading with high volumes of installed base expansion, robust public infrastructure investment, and strong momentum in medical device manufacturing.

The competitive landscape is characterized by regional players, such as Huiheng Medical and Masep Infini Global, as well as global leaders entering the market through joint ventures and technology licensing. Regulatory frameworks in countries such as Japan and Singapore are streamlining device approval timelines, accelerating market entry for new products.

Investment opportunities abound in private hospital networks and tertiary care centers across Tier 2 and Tier 3 cities, supported by rising patient awareness, policy incentives, and improved access to advanced technologies.

Competitive Landscape

The global gamma knife market is moderately consolidated, with the top six players, Elekta, Varian Medical Systems, Nordion Inc., Huiheng Medical, ET Medical Group, Masep Infini Global, controlling nearly 70.0% of the total revenue in 2025.

Global companies focus on innovation, clinical partnerships, and product portfolio diversification to maintain market leadership. Mid-size and emerging manufacturers are capturing niche segment growth, particularly in APAC and Latin America, by offering differentiated, value-driven products. Competitive positioning is being shaped by technology advancements, intellectual property portfolios, and regional expansion strategies.

Business Strategies

Leading firms are leveraging innovation-driven product development, cost leadership in manufacturing, and aggressive geographic expansion as the dominant strategic themes driving market success.

Market leaders prioritize technology integration, such as AI integration, advanced imaging, and integrated workflow solutions, to differentiate product offerings. Emerging trends include bundled services (training, consulting, device servicing), cross-industry partnerships, and digital health platform extensions, optimizing clinical value and operational efficiency.

Strategic Developments

- In July 2025, Elekta’s Leksell Gamma Knife radiosurgery system has received U.S. FDA 510(k) clearance for treating adults with refractory, drug-resistant mesial temporal lobe epilepsy (MTLE). This treatment works by precisely focusing 192 beams of gamma radiation on the seizure focus in the brain, offering a non-invasive alternative to open-skull surgery. The Gamma Knife system, developed in 1968, has been already used globally for other functional brain disorders such as essential tremor and trigeminal neuralgia; this clearance broadens its usage by allowing precision radiosurgery in MTLE cases in the U.S.

- In May 2025, KIMS Hospital in Hyderabad launched a new Gamma Knife Centre, offering advanced non-invasive radiosurgery technology to treat complex brain disorders with high precision and minimal recovery time. The facility is expected to benefit patients from Telangana, Andhra Pradesh, and neighbouring regions who are not ideal candidates for open surgery, providing outpatient treatment for conditions such as brain metastases, arteriovenous malformations (AVMs), acoustic neuromas, pituitary tumors, epilepsy and trigeminal neuralgia.

- In May 2025, AIIMS Delhi, for the first time in India, used Gamma Knife radiosurgery to treat retinoblastoma, a rare eye cancer in young children, applying it to two patients aged 6-7 whose tumors did not respond to standard treatments such as chemotherapy. The procedure, done in one day, is less invasive and aims to preserve vision and the eye, with the cost (? 75,000) covered under the Ayushman Bharat scheme for eligible cases.

Companies Covered in Gamma Knife Market

- Elekta AB

- Varian Medical Systems

- Nordion Inc.

- Huiheng Medical, Inc.

- ET Medical Group

- American Shared Hospital Services

- Masep Infini Global, Inc.

- Hokai Medical Technology

- Cyber Medical Corporation Ltd.

- Accuray Incorporated

- Brainlab AG

- Elekta Korea Ltd.

- ZAP Surgical Systems Inc.

- IntraOp Medical Corporation

- Stryker Corporation

Frequently Asked Questions

The global gamma knife market is projected to reach US$ 468.0 million in 2025.

Rising neurological disease incidence, increased adoption of minimally invasive radiosurgery, and an expanding aging population requiring advanced therapies are driving the market.

The gamma knife market is poised to witness a CAGR of 5.7% from 2025 to 2032.

Increased investments in advanced gamma knife technologies, mounting government support, and innovation targeting unmet clinical needs in neuro-oncology and functional disorders are key market opportunities.

Elekta AB, Varian Medical Systems, and Nordion Inc. are some of the key players.