- Automotive

- Wireline Trucks Market

Wireline Trucks Market Size, Share, and Growth Forecast, 2026 - 2033

Wireline Trucks Market by Product Type (Fiber Optic Construction Trucks, Cable Plowing Trucks, Bucket Trucks, Derrick Trucks, Reel Trailers), Vehicle Size (Light-Duty Trucks, Medium-Duty Trucks, Heavy-Duty Trucks), Application (Underground Cable Installation, Aerial Cable Installation, Fiber Splicing and Testing, Cable Maintenance and Repair, Emergency Response), and Regional Analysis for 2026-2033

Wireline Trucks Market Share and Trends Analysis

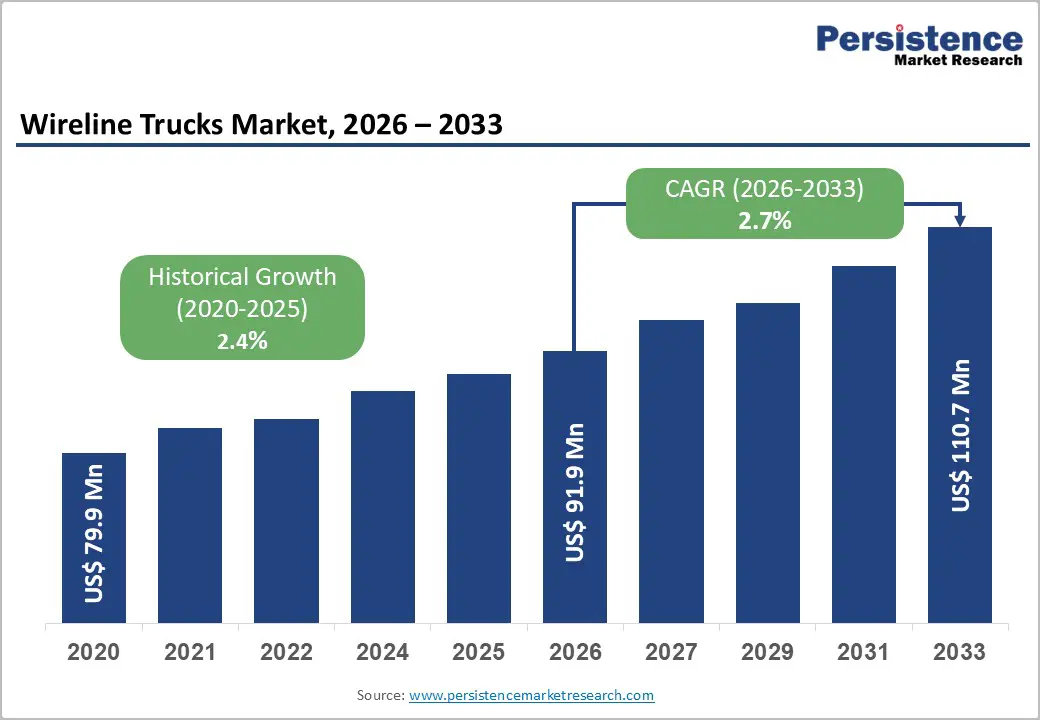

The global wireline trucks market size is likely to be valued at US$ 91.9 million in 2026, and is projected to reach US$ 110.7 million by 2033, growing at a CAGR of 2.7% during the forecast period 2026−2033.

Growth is primarily driven by increasing deployment of fiber optic networks, rising demand for underground and aerial cable installations, and technological integration in utility and telecommunication infrastructure. Digitalization of power grids and telecom systems enhances operational efficiency and drives fleet modernization. Adoption of advanced truck configurations enables faster fiber splicing, testing, and maintenance, reducing downtime and operational costs. Expanding urbanization and industrialization, particularly in emerging economies, increase the demand for reliable cable infrastructure, boosting wireline truck utilization. Investment in smart city projects and renewable energy distribution networks supports market expansion. Infrastructure policy reforms and regulatory frameworks encouraging utility and telecom service improvement further create market pull.

Key Industry Highlights

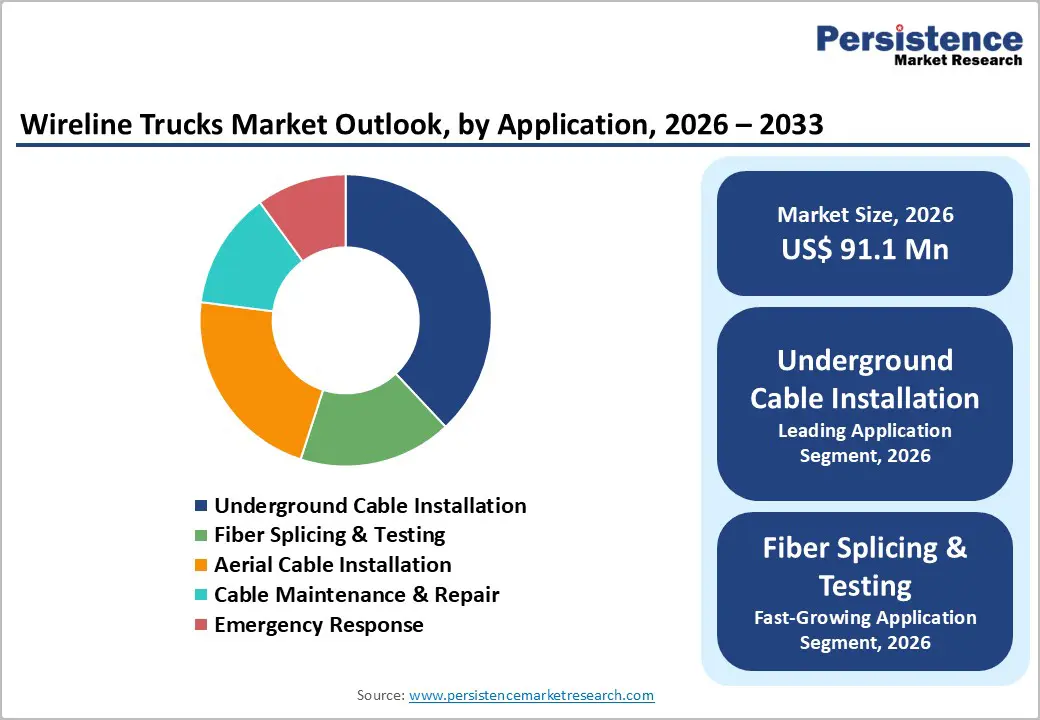

- Leading Application: Underground cable installation is projected to lead the market with a 38% share in 2026, driven by utility and telecommunication infrastructure expansion.

- Fastest-growing Application: Fiber splicing and testing is expected to be the fastest-growing segment from 2026 to 2033, supported by high-speed connectivity demand and network reliability.

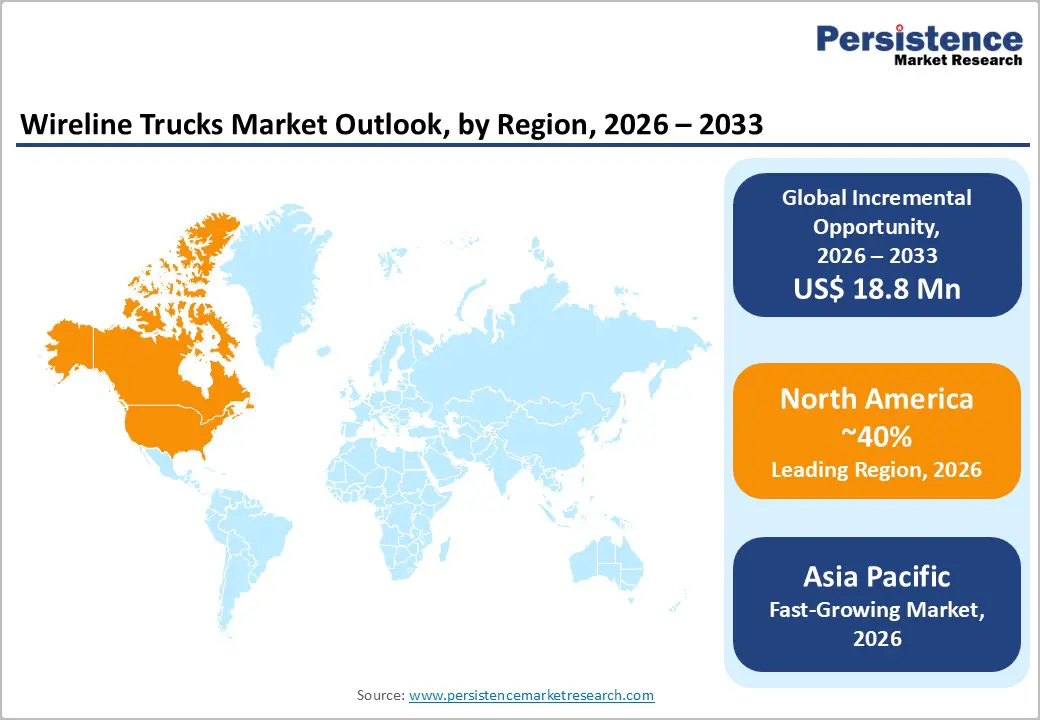

- Dominant Region: North America is projected to hold approximately 40% market share in 2026, owing to extensive fiber optic network expansion and advanced fleet technology adoption.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market from 2026 to 2033, stimulated by accelerated urbanization and large-scale telecommunication infrastructure development.

| Key Insights | Details |

|---|---|

| Wireline Trucks Market Size (2026E) | US$ 91.9 Mn |

| Market Value Forecast (2033F) | US$ 110.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 2.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Infrastructure Modernization and Fiber Network Expansion

Rising demand for high-speed connectivity across urban and semi-urban regions is fueling investment in upgraded communication networks. Deployment of advanced fiber-optic cables and replacement of legacy copper systems require specialized vehicles capable of transporting heavy equipment, spools of fiber, and tools to remote installation sites. These trucks support efficient network rollout, ensuring timely completion of large-scale projects. Expansion of broadband services to underserved areas drives consistent utilization, creating steady demand for vehicles optimized for wireline operations. Fleet operators prioritize reliability, payload capacity, and maneuverability, which directly aligns with ongoing network expansion initiatives.

Telecommunication providers are restructuring network frameworks to accommodate increasing data traffic and future-proof digital infrastructure. Specialized vehicles enable installation, maintenance, and rapid troubleshooting of complex fiber layouts, reducing operational downtime. Network densification and urban connectivity projects increase the need for flexible transportation solutions that can navigate congested areas while supporting heavy loads. This integration of advanced logistics with network construction accelerates service delivery and enhances operational efficiency.

Technological Advancements in Vehicle Design and Automation

Integration of advanced vehicle design and automation has transformed operational efficiency within the sector. Modern wireline operations demand precision, safety, and speed, which are significantly enhanced through automated systems. Smart vehicle controls, real-time monitoring, and predictive maintenance technologies reduce downtime and optimize resource allocation. Ergonomic design improvements and modular equipment layouts enhance on-site adaptability, allowing crews to complete complex tasks with higher accuracy. The shift toward electric and hybrid powertrains also improves energy efficiency and lowers operational costs, supporting sustainable practices in intensive field operations. These innovations directly influence operational throughput and cost-effectiveness, aligning with strategic objectives of service providers.

Automation facilitates data-driven decision-making, enabling remote operation and advanced analytics for performance evaluation. Onboard sensors and integrated control systems allow continuous monitoring of load, tension, and environmental conditions, mitigating risks and improving safety compliance. Enhanced connectivity and digital interfaces streamline coordination between field teams and control centers, reducing response times and operational errors. Investment in intelligent vehicle platforms accelerates adoption of advanced applications, such as high-speed deployment and complex logging operations in challenging terrains. This technological evolution establishes a competitive edge, driving market adoption as service providers prioritize vehicles capable of delivering reliable performance under demanding conditions while maintaining operational efficiency and safety standards.

Volatility in Oil and Gas Prices

Fluctuations in crude oil and natural gas prices directly influence capital expenditure decisions within exploration and production operations. Wireline services are heavily reliant on drilling and well intervention activities, which are scaled up or down according to revenue expectations from hydrocarbon extraction. When energy prices experience significant swings, operators tend to delay or reduce non-essential field operations, impacting demand for service fleets. This financial sensitivity limits long-term investment in fleet expansion, advanced equipment, and technological upgrades, constraining growth opportunities for service providers. Budgetary uncertainties further affect contract negotiations, leading to shorter-term agreements and reduced utilization of high-capacity units.

Price instability also affects project planning and operational risk management. Energy companies prioritize cost optimization and risk mitigation under volatile conditions, often opting for minimal intervention strategies over full-scale well completions or maintenance programs. Seasonal fluctuations and global supply-demand imbalances amplify this cautious approach, resulting in underutilization of specialized trucks and workforce. Capital allocation toward exploration ventures becomes contingent on forecast stability, which in turn limits market penetration in emerging basins. The indirect consequence is slower adoption of high-efficiency wireline technologies, restricting revenue growth and reducing the incentive for service innovation. Investment cycles align closely with predictable pricing environments, making market expansion sensitive to external macroeconomic and geopolitical factors.

Technological Integration Challenges

Integration of advanced digital systems with existing equipment often faces significant obstacles, as legacy infrastructure frequently lacks compatibility with modern software, automation modules, and real-time monitoring tools. Operational workflows must coordinate across multiple platforms, and inconsistencies in communication protocols can result in delayed or inaccurate data transfer. Employees are required to develop new technical competencies while maintaining operational efficiency, placing additional pressure on human resources and training programs. High upfront costs associated with hardware upgrades, software licenses, and system integration services constrain deployment and limit scalability across operational units. These factors reduce the pace at which organizations can adopt emerging digital solutions and advanced analytics for enhanced operational management.

Maintenance and reliability challenges arise when hardware and software components operate under differing technical standards. Equipment downtime increases as integration issues require specialized support for troubleshooting, configuration, and updates. Vendors and service providers encounter difficulties standardizing processes across diverse equipment models, field conditions, and operational environments, complicating project timelines and resource allocation. Regulatory and safety compliance introduces further complexity, as technological modifications must undergo extensive validation and certification to meet industry standards, slowing implementation. Data security and system interoperability concerns also contribute to integration barriers, as connected systems must maintain secure and consistent information flow without compromising operational integrity.

Automation and Digital Monitoring Improve Efficiency

Integration of automation systems and digital monitoring tools has transformed operational workflows in field services. Real-time data collection from sensors and telemetry allows operators to monitor truck performance, equipment status, and operational metrics without manual intervention. This leads to precise scheduling of maintenance, reduced downtime, and optimized resource allocation. Remote diagnostics enable predictive identification of potential failures, minimizing interruptions and enhancing reliability. Streamlined workflows reduce labor-intensive tasks and errors associated with manual monitoring, translating into faster job completion and lower operational expenditure. The ability to access performance analytics instantly supports informed decision-making and resource planning, which is critical in time-sensitive operations.

Digital control systems facilitate seamless coordination between multiple units on-site, improving task sequencing and operational synchronization. Performance dashboards provide actionable insights for efficiency optimization, helping teams allocate resources where they generate maximum value. Enhanced monitoring ensures compliance with safety and operational standards, reducing risk exposure. Data-driven performance assessment encourages continuous improvement and operational standardization across fleets, supporting consistent service delivery. The combination of automated processes and real-time monitoring reduces human dependency, accelerates task execution, and strengthens overall operational efficiency, positioning this capability as a strategic growth driver in service-oriented fleet operations.

Electric and Eco-Friendly Trucks Support Sustainable Operations.

The adoption of electric and eco-friendly trucks drives a significant shift in operational efficiency and cost management within the sector. Transitioning to low-emission vehicles reduces fuel expenditures and maintenance costs while mitigating exposure to volatile fossil fuel prices. These trucks integrate advanced energy management systems that optimize route planning and load distribution, enhancing overall operational productivity. Emission reductions achieved through electric powertrains contribute to compliance with increasingly stringent environmental regulations, supporting corporate sustainability goals and strengthening brand reputation in an environmentally conscious market. Investors and clients increasingly favor partners demonstrating measurable progress toward reducing carbon footprints, making clean vehicle integration a strategic advantage.

Infrastructure improvements and technological innovation accelerate the adoption of electric and eco-friendly trucks. Investment in charging networks, regenerative braking systems, and energy storage solutions enables extended operational ranges and minimizes downtime during fleet operations. These vehicles support the transition to renewable energy sources, aligning operations with global decarbonization targets. Deployment of electric and hybrid fleets fosters a resilient logistics framework capable of adapting to regulatory changes and market pressures. Operational data collected from smart vehicle systems facilitates predictive maintenance, resource optimization, and cost forecasting, improving decision-making efficiency.

Category-wise Analysis

Product Type Insights

Fiber optic construction trucks are anticipated to secure around 35% of the wireline trucks market share in 2026, reflecting high demand from telecom network expansion and smart grid deployment. These specialized vehicles enable precise and efficient cable splicing, aerial installation, and underground deployment, reducing operational delays and improving project timelines. Their robust design ensures reliability across diverse terrains, including urban, suburban, and industrial environments. High-capacity reel transport and integrated storage solutions allow operators to carry larger volumes of fiber optic cable, reducing trips and operational costs. Safety systems and ergonomic configurations further support workforce productivity, making these vehicles a preferred choice for strategic network expansions and infrastructure modernization projects.

Bucket trucks are expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by adoption in aerial cable installation and emergency response applications. Advanced hydraulic lifts and reinforced safety cages allow technicians to reach elevated work sites efficiently, improving task completion speed and operational reliability. Telematics and monitoring systems enable real-time fleet management, reducing downtime and enhancing maintenance planning. Modular design configurations support multiple service requirements, allowing operators to deploy a single vehicle across various tasks, from infrastructure maintenance to emergency interventions. Focus on workplace safety, rapid maintenance response, and uninterrupted service drives continued investment and adoption in urban and remote operational contexts.

Application Insights

Underground cable installation is likely to be the leading segment with a projected 38% of the wireline trucks market revenue share in 2026 due to widespread utility and telecommunication infrastructure expansion. These specialized vehicles support deep trenching, cable plowing, and reel deployment while minimizing operational disruption to urban and industrial areas. Advanced designs enhance reliability under varying soil and environmental conditions, ensuring uninterrupted project execution. Integration of digital monitoring, automated cable handling, and real-time data collection improves installation accuracy, reduces labor requirements, and shortens project timelines. Cost efficiency, operational precision, and adaptability to diverse infrastructure environments drive fleet procurement preference and long-term adoption.

Fiber splicing and testing are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by increasing demand for high-speed connectivity, network reliability, and service-level adherence. Wireline trucks equipped with automated splicing units, diagnostic instruments, and testing devices streamline deployment, reducing manual intervention and error rates. Expansion of smart city initiatives, broadband networks, and industrial fiber installations drives consistent growth across multiple regions. Integration of digital monitoring and predictive analytics enhances operational oversight, resource allocation, and maintenance scheduling. The combination of advanced technology, workflow efficiency, and scalable deployment positions the segment for sustained market expansion.

Regional Insights

North America Wireline Trucks Market Trends

North America is anticipated to secure approximately 40% of the wireline trucks market share in 2026, reflecting strong infrastructure development, technological adoption, and established industrial networks. High demand for fiber optic network expansion and utility modernization drives procurement of specialized vehicles designed for cable deployment, splicing, and maintenance. Operational efficiency is enhanced through advanced digital monitoring systems, automated reel handling, and telematics integration, allowing fleet operators to optimize routes, reduce downtime, and minimize labor costs. Regulatory frameworks mandating safety compliance, emission standards, and infrastructure reliability further incentivize adoption of modern wireline vehicles. High concentration of urban centers and industrial hubs increases the need for versatile trucks capable of addressing diverse deployment scenarios, including deep trenching, aerial installation, and emergency maintenance operations.

Dominance is also supported by strong private-sector investments and public-private partnerships in telecommunications and energy infrastructure projects. The prevalence of large-scale broadband initiatives, smart grid implementation, and high-speed network upgrades drives demand for trucks with high-capacity reel transport, hydraulic lifts, and integrated testing equipment. Fleet operators prioritize reliability, safety features, and modular vehicle configurations to meet complex project requirements efficiently. Integration of predictive maintenance systems and real-time diagnostics enhances asset utilization and reduces operational risk. Advanced logistics and supply chain networks enable timely deployment and consistent service delivery across urban, suburban, and industrial zones.

Europe Wireline Trucks Market Trends

The market for wireline trucks in Europe is predicted to exhibit steady growth throughout the 2026-2033 forecast period, underpinned by ongoing modernization of telecommunication and utility infrastructure. Expansion of fiber optic networks, deployment of smart grids, and upgrades to industrial connectivity systems drive demand for specialized vehicles designed for underground and aerial cable installation. Emphasis on operational safety and regulatory compliance encourages procurement of trucks with advanced hydraulic lifts, integrated testing units, and digital monitoring systems. Urban centers with high population density require vehicles capable of navigating constrained environments while transporting large-capacity reels efficiently.

Adoption is further strengthened by sustainability initiatives and energy efficiency targets. Fleet operators prioritize electric and low-emission trucks to align with emission reduction mandates and environmental standards. Modular vehicle configurations allow operators to handle multiple tasks, from fiber splicing to network testing, within a single deployment cycle. Integration of smart diagnostics and automated handling systems enhances installation accuracy, reduces operational risk, and accelerates project timelines. Focused government incentives for infrastructure modernization, coupled with robust transport and logistics networks, support seamless deployment across diverse terrains.

Asia Pacific Wireline Trucks Market Trends

Asia Pacific is expected to register the fastest growth in the market for wireline trucks between 2026 and 2033, driven by accelerated urbanization, industrial expansion, and large-scale telecommunication infrastructure projects. Rapid adoption of high-speed broadband networks, smart city initiatives, and industrial fiber deployments creates strong demand for specialized vehicles capable of efficient cable installation, splicing, and maintenance. Investments in underground and aerial network expansion necessitate trucks with advanced reel handling, hydraulic lifts, and digital monitoring systems, enabling operators to manage complex projects with minimal downtime. Increasing focus on operational efficiency, network reliability, and service-level compliance further fuels procurement of technologically advanced fleets. Expanding energy and utility networks require vehicles that can adapt to diverse terrains and urban congestion, supporting timely deployment and reducing operational risk.

Growth is reinforced by government initiatives and private-sector investments aimed at improving connectivity and reducing digital divides. Strategic deployment of wireline trucks in tier-2 and tier-3 cities accelerates network coverage, while modular vehicle configurations allow operators to manage multiple tasks across industrial, urban, and remote sites efficiently. Adoption of automated splicing units, integrated testing equipment, and smart diagnostics improves accuracy, reduces labor requirements, and shortens project timelines. Supportive policies, combined with improved transport infrastructure and logistics capabilities, facilitate seamless fleet operations across expanding service areas.

Competitive Landscape

The global wireline trucks market landscape is a highly vibrant one, shaped by the presence of global oilfield service leaders alongside specialized equipment manufacturers. Key players such as Baker Hughes, Schlumberger Limited, Weatherford International plc, National Oilwell Varco, Inc., and Halliburton Company maintain substantial market influence through extensive fleets and comprehensive service offerings. These companies leverage digital integration, advanced telemetry systems, and predictive maintenance technologies to enhance operational efficiency, reduce downtime, and improve project accuracy. Their global reach and established client relationships enable large-scale deployment across complex infrastructure projects, including underground cable installation, fiber splicing, and emergency network maintenance.

At the same time, a wide range of regional and niche manufacturers contribute to market dynamism by focusing on customization, localized support, and cost-effective solutions. These firms cater to specific operational requirements, such as urban deployment, modular configurations, and terrain-specific vehicle adaptations, allowing operators to optimize efficiency and reduce project-specific costs. Flexibility in service models, rapid response times, and adaptability to regulatory variations provide these players with a competitive edge in certain segments.

Key Industry Developments

- In January 2026, SLB advanced its platform-based oilfield software strategy by integrating real-time data streams from wireline trucks into its cloud- and AI-driven digital ecosystem, enabling unified subsurface insights, operational optimization, and faster decision-making across wireline logging and intervention workflows.

- In December 2025, Autocar Trucks introduced a smart battery cable system designed to reduce fire risks in refuse trucks by automatically disconnecting power under hazardous conditions, enhancing vehicle safety and uptime in waste collection operations. The solution addresses a common source of electric system–related fires and supports fleet reliability.

Companies Covered in Wireline Trucks Market

- Baker Hughes

- Schlumberger Limited

- Weatherford International plc

- National Oilwell Varco, Inc.

- Halliburton Company

- Pioneer Energy Services Corp.

- Expro Group

- Superior Energy Services, Inc.

- C&J Energy Services, Inc.

- Archer Well Company AS

Frequently Asked Questions

The global wireline trucks market is projected to reach US$ 91.9 million in 2026.

Rapid expansion of telecommunication and utility infrastructure, coupled with demand for efficient cable installation, splicing, and maintenance, is driving the market.

The market is poised to witness a CAGR of 2.7% from 2026 to 2033.

Adoption of electric and eco-friendly trucks, fleet modernization, and smart city infrastructure projects present key market opportunities.

Some of the key market players include Baker Hughes, Schlumberger Limited, Weatherford International plc, National Oilwell Varco, Inc., and Halliburton Company.