- Industrial Goods & Service

- Wire & Cable Lubricant Market

Wire & Cable Lubricant Market Size, Share, and Growth Forecast 2026 - 2033

Wire & Cable Lubricant Market by Product Type (Gel, Wax, Spray, Liquid), Base Oil (Mineral Oil, Synthetic Oil, Bio-Based Oil), Application (Wire Drawing, Cable Pulling, Cable Manufacturing, Mill Machinery, Others), End-Use Industry (Construction, Electronics, Telecommunications, Energy, Industrial Manufacturing), by Regional Analysis, 2026 - 2033

Wire & Cable Lubricant Market Size and Trend Analysis

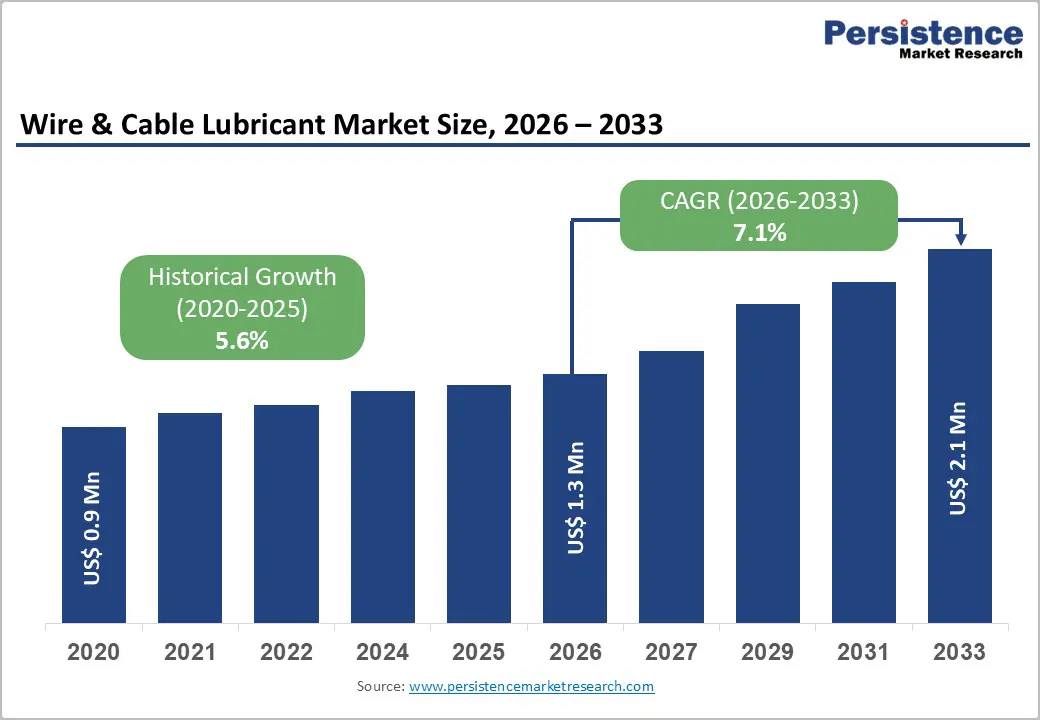

The global wire & cable lubricant market size is expected to be valued at US$ 1.3 Billion in 2026 and projected to reach US$ 2.1 Billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

Accelerating global expansion of telecommunications and power infrastructure, rising adoption of high-performance synthetic lubricants, and stringent regulatory standards governing cable installation safety are the core forces propelling market growth. The proliferation of 5G network rollouts and smart grid modernization programs across developed and emerging economies is generating surging demand for specialized cable pulling and drawing lubricants that ensure installation integrity and reduce conductor damage. Simultaneously, growing environmental consciousness is shifting end users toward bio-based and low-VOC lubricant formulations, supported by tightening chemical regulations in the European Union and North America, reinforcing innovation pipelines across leading lubricant manufacturers.

Key Industry Highlights

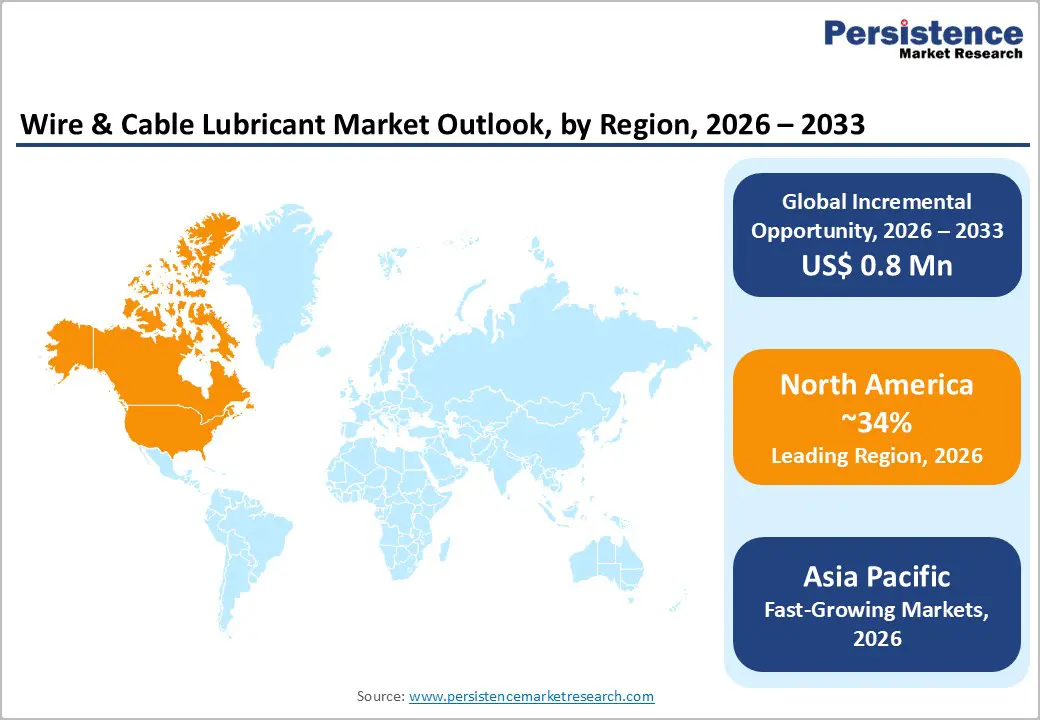

- Leading Region: North America commands approximately 34% of global Wire & Cable Lubricant market revenue in 2025, underpinned by the U.S. Infrastructure Investment and Jobs Act's US$ 65 billion broadband and grid investment and high regulatory compliance standards.

- Fastest Growing Region: Asia Pacific is projected to grow at a CAGR of 8.2% during 2026 - 2033, driven by China's dominance in copper wire rod production, India's BharatNet Phase III broadband rollout, and expanding ASEAN electronics manufacturing hubs.

- Dominant Segment: Gel lubricants lead the market with approximately 38% share in 2025, preferred for cable pulling applications due to superior thixotropic properties, high film strength, and universal compatibility with PVC, LSZH, and polyethylene cable jacket materials.

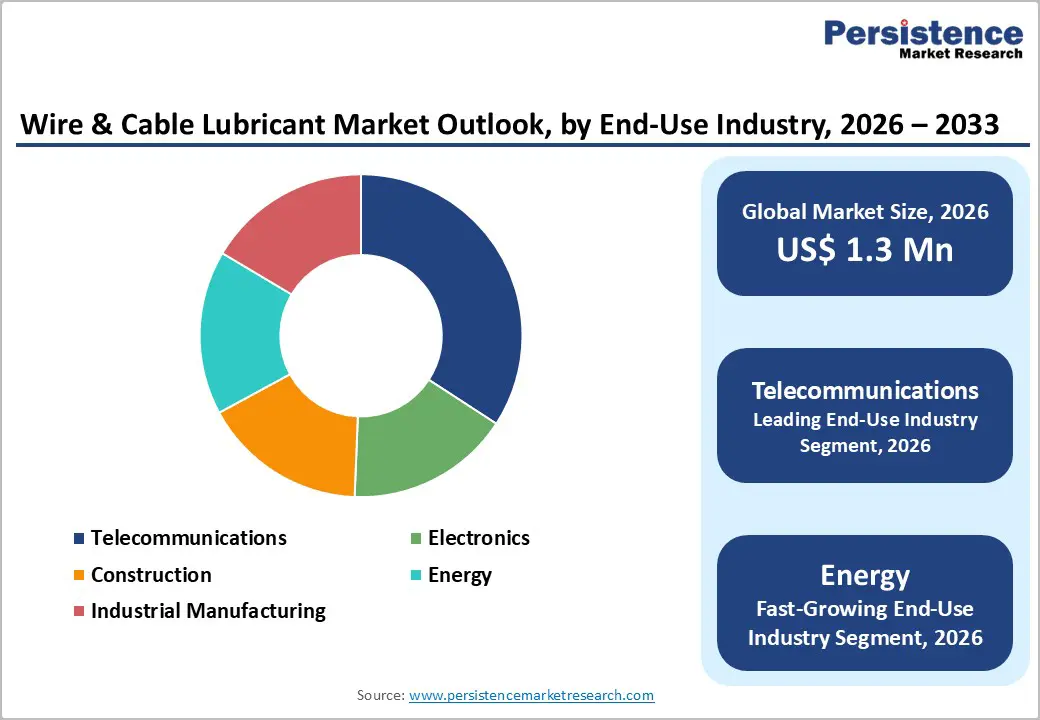

- Fastest Growing Segment: The Energy sector is the fastest growing end-use segment, driven by global renewable energy capacity additions, offshore wind cable projects, and high-voltage underground cable installations connecting solar and wind farms to national grids.

- Key Market Opportunity: Rising EU REACH restrictions and EPA guidelines are creating strong demand for bio-based and synthetic ester wire lubricants, with European bio-lubricant adoption growing 12% in 2023; NSF H1 and USDA BioPreferred-certified products offer significant revenue upside.

| Key Insights | Details |

|---|---|

| Wire & Cable Lubricant Market Size (2026E) | US$ 1.3 Billion |

| Market Value Forecast (2033F) | US$ 2.1 Billion |

| Projected Growth CAGR (2026 - 2033) | 7.1% |

| Historical Market Growth (2020 - 2025) | 5.6% |

Market Dynamics

Market Growth Drivers

Surging Global Investments in Telecommunications and Power Grid Infrastructure

Massive public and private investment in telecommunications and electrical grid infrastructure is a primary catalyst for wire and cable lubricant demand. According to the International Energy Agency (IEA), global electricity grid investment reached a record US$ 400 billion in 2023, with grid expansion and modernization projects in Asia Pacific, North America, and Europe driving large-scale conduit cabling activity. The U.S. Infrastructure Investment and Jobs Act allocated US$ 65 billion toward broadband and grid infrastructure, directly stimulating demand for cable pulling lubricants during conduit installation. Each kilometer of underground cable installation typically requires substantial volumes of pulling compound to reduce friction and prevent insulation damage, making lubricants an indispensable consumable across all cable laying operations.

Growth of the Global Wire Drawing Industry and Metal Processing Sector

Wire drawing is a foundational metalworking process in which lubricants play a critical functional role, reducing die friction, extending tool life, and improving finished wire surface quality. Global crude steel production reached 1,888 million tonnes in 2023 according to the World Steel Association, and the downstream wire rod market, which feeds directly into wire drawing operations, continues to expand steadily. China alone produced approximately 128 million tonnes of wire rod in 2023, representing a significant demand anchor for wire drawing lubricants. Rising production of copper conductors for electric vehicle wiring harnesses, solar panel connectors, and high-voltage transmission cables further amplifies lubricant consumption, as copper wire drawing demands precisely formulated emulsions and soaps to achieve the tight dimensional tolerances required by the electronics and energy industries.

Market Restraints

Volatile Raw Material Prices and Petroleum Feedstock Dependency

The majority of wire and cable lubricants are formulated using mineral or synthetic base oils derived from petroleum feedstocks, making the market highly sensitive to crude oil price fluctuations. Brent crude prices oscillated between US$ 72 and US$ 97 per barrel during 2023-2024, creating unpredictable input cost environments for lubricant manufacturers. These cost pressures compress profit margins, particularly for small and mid-sized formulators who lack the purchasing scale to negotiate fixed-price raw material contracts. Price volatility also disrupts long-term formulation planning and can force reformulation compromises that may affect product performance consistency.

Stringent Environmental Regulations Restricting Conventional Lubricant Formulations

Tightening chemical safety and environmental regulations, particularly the EU REACH regulation and U.S. EPA Toxic Substances Control Act (TSCA) requirements, impose significant compliance costs on lubricant manufacturers. Restrictions on high-viscosity aromatic oils, chlorinated paraffins, and certain biocide additives commonly used in metalworking lubricants are forcing reformulation across product lines. Companies must invest in extensive toxicological testing, regulatory documentation, and alternative ingredient sourcing, increasing time-to-market for new products and raising the barrier to innovation for smaller market participants.

Market Opportunities

Rising Demand for Bio-Based and Environmentally Compliant Lubricant Formulations

The global transition toward sustainable industrial chemicals presents a compelling growth opportunity for bio-based wire and cable lubricant manufacturers. The European Chemicals Agency (ECHA) and U.S. Environmental Protection Agency (EPA) are progressively restricting petroleum-derived lubricant additives, creating regulatory tailwinds for plant-based and synthetic ester-based lubricant alternatives. Bio-based lubricants derived from vegetable oils and biosynthetic esters offer comparable or superior lubricity, higher flash points, and significantly improved biodegradability compared to mineral oil counterparts. The European Lubricants Industry (ELGI) reports that bio-lubricant adoption in industrial applications grew by 12% in 2023 across the EU. Manufacturers that invest in NSF H1-certified and USDA BioPreferred-classified lubricant lines will be strongly positioned to capture procurement preferences across environmentally regulated end-use industries including construction, energy, and telecommunications.

Expanding 5G Infrastructure Rollout and Subsea Cable Network Development

The accelerating global deployment of 5G telecommunications networks and subsea fiber optic cable systems is generating sustained incremental demand for high-performance cable pulling lubricants. The International Telecommunication Union (ITU) estimates that global 5G connections will surpass 5 billion by 2030, necessitating extensive underground and in-building fiber and coaxial cable installation, each requiring appropriate pulling compounds for friction reduction and cable jacket protection. Subsea cable installations, which are expanding rapidly to support cross-border data traffic growth, demand ultra-specialized lubricants capable of performing under high-pressure, salt-water-adjacent conditions. In 2024, Google and Meta jointly announced the Arachnid subsea cable project connecting Asia, Africa, and Europe, exemplifying the scale of cable infrastructure investment that directly translates into demand for specialized installation lubricants.

Category-wise Insights

Product Type Analysis

Gel-based lubricants represent the leading product type in the wire and cable lubricant market, commanding approximately 38% of total market share in 2025. Gels are the preferred formulation for cable pulling applications due to their superior thixotropic properties, they flow under shear stress during cable installation and revert to a semi-solid state at rest, preventing drip and minimizing waste in vertical conduit runs. Their high film strength ensures effective lubrication throughout extended cable pulls exceeding 300 meters in a single run, a critical performance requirement for underground utility and data center cabling projects. Gel lubricants also adhere well to diverse cable jacket materials, including PVC, LSZH (Low Smoke Zero Halogen), and polyethylene, making them a universal solution across construction and telecommunications end-use segments. Spray lubricants are the fastest growing product type, driven by growing preference for ease of application in industrial and field maintenance settings.

Base Oil Analysis

Mineral oil remains the dominant base oil category in the global wire and cable lubricant market, accounting for approximately 52% of total market share in 2025. Mineral oil-based lubricants are widely preferred due to their cost-effectiveness, availability through established petroleum distribution networks, and compatibility with a broad range of metallic and polymer substrates encountered in wire drawing and cable manufacturing processes. Standard mineral oil formulations in ISO VG 15 to ISO VG 68 viscosity grades are extensively used in wet wire drawing of copper and aluminum conductors, forming the operational backbone of the global wire and cable manufacturing industry. However, Synthetic Oil is the fastest growing base oil segment, expanding at an above-average CAGR as manufacturers seek higher-temperature stability, reduced consumption rates, and lower toxicity profiles to meet evolving environmental and operational requirements.

Application Analysis

Cable Pulling is the leading application segment in the global wire and cable lubricant market, representing approximately 35% of total revenue share in 2025. Cable pulling lubricants, commonly known as pulling compounds, are used to reduce the coefficient of friction between the cable jacket and conduit wall during installation, enabling longer pulls, reducing installation labor time, and preventing jacket damage that could compromise cable performance and longevity. The National Electrical Code (NEC) in the United States mandates the use of approved lubricants during electrical conduit cable installation, establishing a regulatory demand foundation for this segment. Infrastructure investment booms in broadband, power distribution, and smart city projects globally are sustaining strong volume growth for pulling compounds. Wire Drawing is the fastest growing application, driven by rising copper and aluminum conductor production for EVs and renewable energy systems.

End-Use Industry Analysis

The Telecommunications end-use industry is the dominant segment in the wire and cable lubricant market, accounting for approximately 30% of total market share in 2025. Telecommunications networks require extensive fiber optic and coaxial cable installations both above-ground and underground, with cable pulling lubricants serving as an essential consumable at every installation point. The global push toward universal broadband access, as articulated in the UN Broadband Commission's 2025 targets, and the concurrent rollout of 5G infrastructure across Asia Pacific, North America, and Europe are generating consistent demand for gel and liquid pulling compounds. The Energy sector is the fastest growing end-use segment, propelled by global renewable energy capacity additions and high-voltage underground cable projects connecting offshore wind and solar installations to national grids.

Regional Insights

North America Wire & Cable Lubricant Market Trends and Insights

North America is the leading regional market for wire and cable lubricants, commanding approximately 34% of global market share in 2025, driven by large-scale broadband expansion under the U.S. Infrastructure Investment and Jobs Act's US$ 65 billion broadband allocation and ongoing smart grid modernization programs. The National Electrical Manufacturers Association (NEMA) reports sustained growth in U.S. wire and cable production, underpinning consistent lubricant consumption. Regulatory compliance under EPA TSCA and UL standards is actively shaping product formulation, favoring low-VOC, water-based pulling compounds.

The U.S. leads regional innovation with companies like American Polywater Corporation and Greenlee (Emerson Electric Co.) developing environmentally compliant, high-performance pulling compounds specifically designed for fiber optic and LSZH cable jacket compatibility. Canada's accelerating fibre-to-the-home (FTTH) buildout under the CRTC's universal broadband fund is also driving incremental lubricant demand across remote and rural installation projects, contributing to steady regional volume growth.

Europe Wire & Cable Lubricant Market Trends and Insights

Europe represents the second largest regional market, characterized by rigorous environmental compliance frameworks and a strong shift toward bio-based and synthetic lubricant formulations. EU REACH and the European Green Deal mandates are compelling manufacturers in Germany, France, and the United Kingdom to reformulate conventional mineral oil-based lubricants, favoring synthetic ester and vegetable oil alternatives. Germany, as Europe's largest wire and cable producer, drives significant lubricant demand through its automotive wiring harness, industrial automation, and renewable energy cable manufacturing sectors.

The United Kingdom's Project Gigabit, a £5 billion initiative targeting nationwide full-fibre broadband coverage, is generating sustained fiber optic cable installation activity, boosting pulling compound consumption. Spain's accelerating offshore wind development under its National Energy and Climate Plan (NECP) is driving demand for high-specification cable lubricants used in marine and subsea energy cable manufacturing and installation, with the Spanish offshore wind pipeline expected to reach 3 GW by 2030.

Asia Pacific Wire & Cable Lubricant Market Trends and Insights

Asia Pacific is the fastest growing regional market for wire and cable lubricants, projected to register a CAGR of 8.2% during 2026-2033, propelled by massive wire rod and conductor manufacturing capacity in China, accelerating telecommunications infrastructure buildout in India, and expanding electronics manufacturing ecosystems across Vietnam and South Korea. China dominates regional production, accounting for over 50% of global copper wire rod output, sustaining substantial wire drawing lubricant consumption in its extensive conductor manufacturing base.

India's BharatNet Phase III project, targeting optical fiber connectivity to 600,000 villages, is driving significant cable installation activity and demand for cable pulling lubricants in rural broadband infrastructure programs. Japan remains a technology leader in specialized lubricant formulations for precision electronics and fine wire drawing applications, with companies like Klüber Lubrication maintaining strong regional market presence. The ASEAN region's growing FDI inflows into electronics manufacturing, particularly in Vietnam and Malaysia, are creating new demand pockets for high-purity wire drawing lubricants.

Competitive Landscape

The global wire and cable lubricant market is moderately fragmented, with a mix of multinational chemical companies and specialized lubricant formulators competing across distinct application niches. Market leaders including 3M Company, American Polywater Corporation, and Klüber Lubrication differentiate through proprietary formulation technologies, application-specific product portfolios, and regulatory compliance capabilities. Key competitive strategies include investment in bio-based product development, expansion into high-growth Asia Pacific markets, and the adoption of e-commerce and digital distribution channels to improve market accessibility. Emerging business models include lubricant-as-a-service offerings with technical application support and custom formulation services for large cable manufacturers, enabling deeper customer relationships and switching cost barriers.

Key Developments

- August, 2025: Metalube Group Ltd. launched Lubricool 955, a next-generation semi-synthetic copper wire drawing lubricant designed for high-speed multi-wire machines, offering extended sump life, improved emulsion stability, and reduced downtime to enhance efficiency in modern wire manufacturing operations.

- May, 2024: Klüber Lubrication announced an INR 142 crore investment to expand its specialty lubricant manufacturing facility in Mysore, India, aiming to increase domestic production capacity, strengthen R&D infrastructure, and support new product development as part of its “Make in India” strategy.

Companies Covered in Wire & Cable Lubricant Market

- 3M Company

- CRC Industries

- American Polywater Corporation

- Synco Chemical Corporation (Super Lube)

- IDEAL Industries, Inc.

- Lubrication Engineers, Inc.

- Klein Tools, Inc.

- Klüber Lubrication (Freudenberg Group)

- Greenlee (Emerson Electric Co.)

- Aerolube Corporation

- Interlub Group

- Techspan Industries Inc.

- Accurate Lubrication

- Polywater Europe

- Rectorseal Corporation

- WD-40 Company

- Molykote (DuPont de Nemours)

Frequently Asked Questions

The global Wire & Cable Lubricant market is expected to reach US$ 1.3 Billion in 2026 and is projected to grow to US$ 2.1 Billion by 2033 at a CAGR of 7.1%.

Rising investments in telecom and power grid infrastructure, expansion of 5G networks, increasing wire and cable manufacturing, and growing adoption of environmentally compliant lubricant formulations are the primary demand drivers.

North America leads the global Wire & Cable Lubricant market with around 34% revenue share, supported by strong broadband infrastructure investment and expanding wire and cable manufacturing activities.

The key opportunity lies in the development of bio-based and synthetic ester lubricants that meet tightening environmental regulations and sustainability requirements.

Key players include American Polywater Corporation, 3M Company, CRC Industries, Klüber Lubrication, Greenlee, IDEAL Industries Inc., Synco Chemical Corporation, Klein Tools Inc., and Interlub Group.