- Pharmaceuticals

- Wart Remover Market

Wart Remover Market Size, Share, and Growth Forecast, 2026 – 2033

Wart Remover Market by Treatment Type (Salicylic Acid, Cryotherapy Devices, Laser Therapy, Immunotherapy), End-User (Online Pharmacies, Retail Pharmacies, Hospital Pharmacies, Others), Distribution Channel (Pharmacies, Supermarkets, Online Retail), and Regional Analysis for 2026-2033

Wart Remover Market Share and Trends Analysis

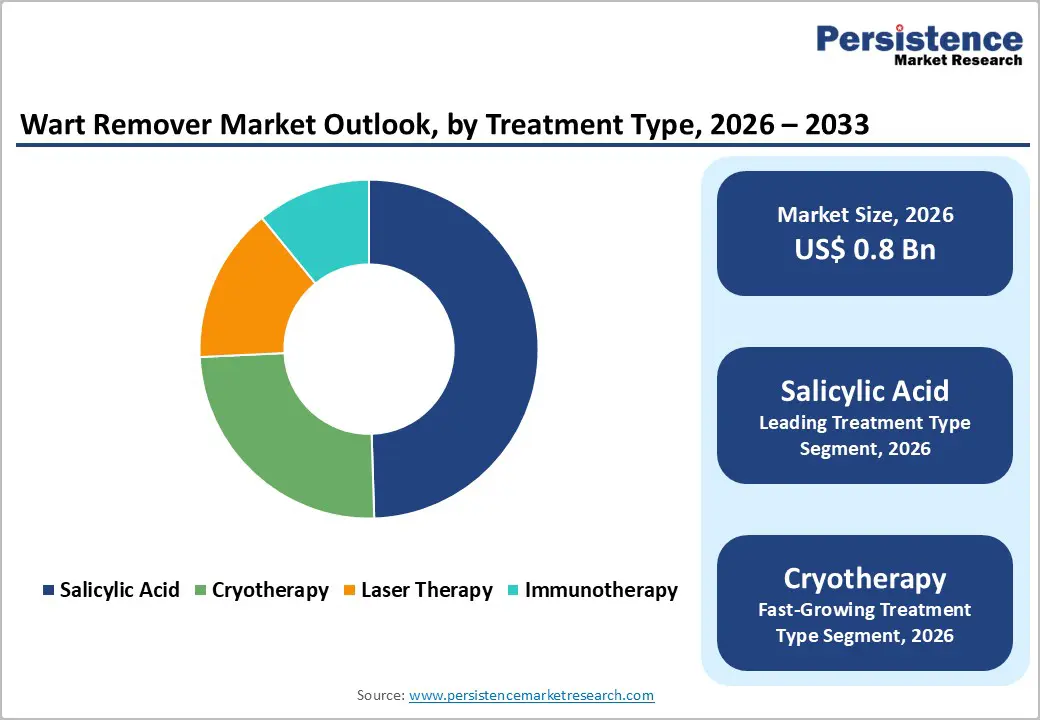

The global wart remover market size is likely to be valued at US$ 0.8 billion in 2026, and is projected to reach US$ 1.2 billion by 2033, growing at a CAGR of 3.5% during the forecast period 2026−2033. Rising global prevalence of human papillomavirus (HPV) infections, which affects an estimated 11-12% of the world population at any given time according to the World Health Organization (WHO), continues to generate robust demand for efficacious wart removal solutions. Concurrently, growing consumer awareness regarding dermatological health and increasing self-medication tendencies, particularly in developed economies, are expanding the over-the-counter (OTC) segment. Technological advancements in cryotherapy devices and the proliferation of e-commerce distribution channels are further accelerating market accessibility and volume growth across geographies.

Key Industry Highlights

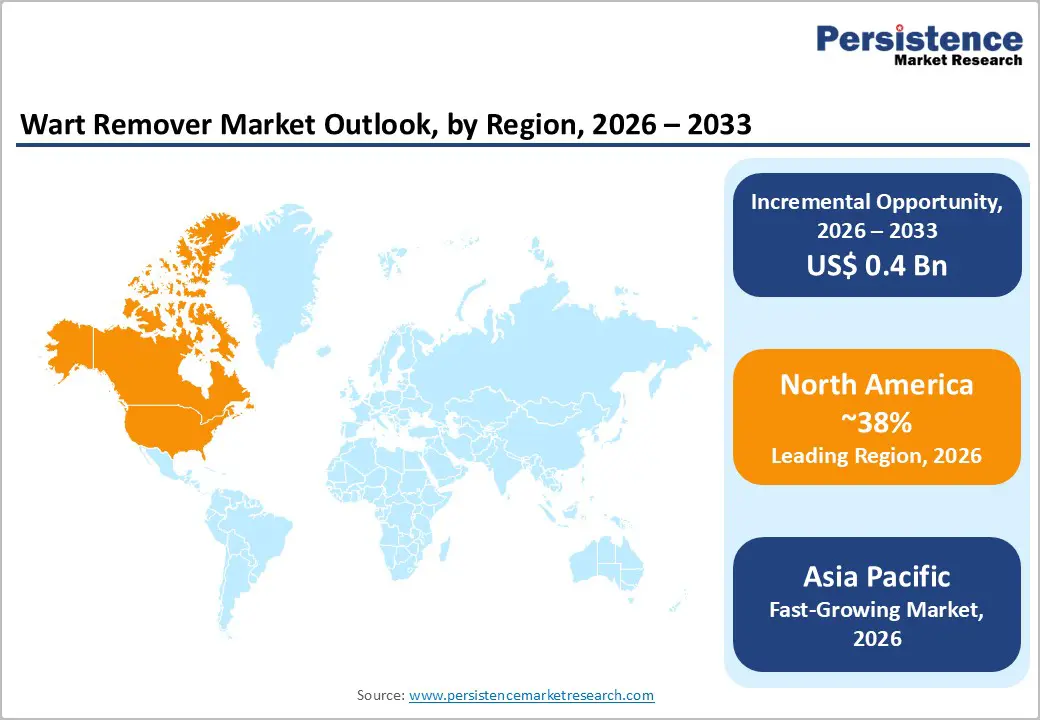

- Dominant Region: North America is expected to command a share of about 38% in 2026, supported by widespread consumer knowledge of skin care and extensive pharmacy networks.

- Fastest-growing Market: The Asia Pacific market is poised to be the fastest-growing through 2033, due to expanding healthcare access and consumer awareness.

- Leading & Fastest-growing Treatment Type: Salicylic acid is set to capture nearly 50% revenue share in 2026, while cryotherapy devices are likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing End-User: Retail pharmacies are slated to lead with an estimated revenue share of 75% in 2026, with online pharmacies growing the fastest from 2026 to 2033.

| Key Insights | Details |

|---|---|

| Wart Remover Market Size (2026E) | US$ 0.8 Bn |

| Market Value Forecast (2033F) | US$ 1.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Global HPV Prevalence and Expanding Patient Pool

HPV infection remains one of the most prevalent sexually transmitted diseases (STDs) and skin-contact infections globally. According to the WHO, HPV affects nearly 630 million individuals worldwide. The U.S. Centers for Disease Control and Prevention (CDC) notes that common warts affect a significant portion of the general population. Children and young adults face higher rates of these infections, which will sustain a large group of potential users in the coming years. Healthcare providers and consumers increasingly turn to accessible treatments, such as topical salicylic acid products, cryotherapy kits, and medicated patches, to address this ongoing need.

Pharmaceutical companies are responding to changing healthcare needs by improving product formulations and expanding distribution channels across retail pharmacies, hospital networks, and digital commerce platforms. Manufacturers are increasingly focusing on accessibility and convenience, ensuring that treatments are readily available through both physical outlets and online purchasing systems. This approach is strengthening the relationship between rising infection incidence and consumer purchasing behavior because patients are seeking faster access to over-the-counter and prescribed solutions. Awareness initiatives led by healthcare providers and public health organizations are educating families about early symptom recognition and timely intervention, which is supporting higher treatment adoption rates.

Technological Innovation in Treatment Modalities

Companies are continuously investing in research & development (R&D) to advance wart removal technologies, with a focus on improving treatment effectiveness, safety profiles, and patient comfort. Next-generation cryotherapy devices such as single-use disposable applicators and precision dosing delivery systems are entering the market with strong clinical validation, offering faster wart clearance compared with traditional salicylic acid formulations. Pharmaceutical manufacturers are developing these solutions to address increasing consumer demand for reliable at-home treatments that reduce dependence on clinical procedures. Healthcare professionals are endorsing these innovations because they are lowering the need for in-office interventions while improving therapeutic outcomes and patient satisfaction. As innovation progresses, manufacturers are introducing devices that balance high efficacy with minimal adverse effects, which is strengthening consumer confidence and encouraging broader adoption across age groups.

Regulatory agencies such as the U.S. Food and Drug Administration (FDA) are approving advanced OTC products that combine multiple therapeutic mechanisms, including imiquimod-based immunomodulatory agents and multi-action topical formulations. Peer-reviewed publications such as the Journal of Dermatological Treatment are providing clinical evidence that supports the effectiveness of these newer approaches, enabling companies to position premium-priced offerings within the category. Advanced treatment options are resolving warts more quickly than conventional methods, which is expanding overall market value and attracting investor interest. Consumers, on the other hand, are benefiting from convenient solutions that align with busy lifestyles, while companies are strengthening brand loyalty through clinically proven performance and regulatory credibility, is supporting wart remover market growth.

High Cost of Advanced Treatment Options

The elevated cost structure of advanced cryotherapy devices and prescription-grade formulations is creating a structural access constraint, particularly across price-sensitive emerging economies. Professional cryotherapy treatment courses in the U.S. range between US$ 200 and US$ 600, which is discouraging households from pursuing clinically supervised interventions. Healthcare providers are observing that affordability concerns are delaying care-seeking behavior, even when treatment is medically appropriate. Companies are attempting geographic expansion into lower-income markets, yet purchasing decisions are continuing to prioritize essential healthcare expenditures over elective procedures. Insurance reimbursement gaps are compounding this challenge because many health systems are classifying wart removal as a cosmetic procedure rather than a medical necessity. This reimbursement stance is shifting the financial burden directly onto patients, thereby constraining utilization across middle-income populations and reducing procedural volumes.

The affordability gap is narrowing the total addressable market and moderating revenue scalability for premium brands. Industry participants are responding by developing tiered portfolios that include entry-level solutions alongside technologically advanced platforms, which is enabling broader segmentation coverage. Policymakers are supporting the adoption of generic formulations to reduce fiscal pressure on public healthcare systems, and this trend is improving baseline accessibility. Commercial opportunities are also emerging through collaborations with retail pharmacies and e-commerce distributors that are bundling cost-efficient treatment kits with educational outreach initiatives to improve consumer confidence and adherence. Future innovation pipelines will have prioritized cost-efficient engineering approaches such as reusable applicators, optimized refrigerant utilization, and simplified device architectures to enhance affordability without compromising efficacy.

Availability of Alternative Remedies and Treatment Substitutes

The wart remover market is experiencing sustained pressure from a broad spectrum of therapeutic substitutes that are addressing similar clinical needs through different value propositions. Alternatives are spanning OTC salicylic acid formulations, consumer freezing kits, and physician-administered procedures such as cryotherapy, laser ablation, and immunotherapy. Interest in herbal and plant-derived remedies is also increasing as consumers are prioritizing perceived safety and natural positioning for dermatological care. Dermatology clinics are continuing to offer in-office interventions, including laser therapy and minor surgical excision, which are attracting patients with recurrent or treatment-resistant lesions. This competitive intensity is reducing differentiation for branded wart removal products and is complicating new product adoption cycles.

Market expansion is also moderating due to the self-limiting nature of viral warts, as many cases are resolving spontaneously without therapeutic intervention over time. This clinical characteristic is discouraging repeat purchases and is constraining predictable revenue streams for manufacturers. Concurrently, rising consumer inclination toward organic skincare routines is intensifying substitution risk, particularly among health-conscious demographics that are favoring botanical regimens. Industry participants are countering this shift by developing hybrid formulations that are integrating evidence-based active compounds with naturally derived supportive ingredients to strengthen perceived safety and efficacy. Educational initiatives are emphasizing the advantages of clinically validated therapies, including shorter treatment duration and reduced recurrence probability. Retail channels are promoting bundled solutions that combine OTC kits with behavioral guidance and preventive education to enhance user engagement and trust.

Combination Therapy and Prescription-to-OTC Switches

Regulatory authorities are advancing structured initiatives to transition selected prescription dermatology therapies to OTC status, which is creating a meaningful growth catalyst for the wart treatment category. The U.S. FDA is advancing its Drug Efficacy Study Implementation (DESI) program, while the European Medicines Agency (EMA) is applying comparable scientific review frameworks to reassess legacy prescription products. Regulators are evaluating active agents such as imiquimod 5% cream and podophyllotoxin formulations that still require physician authorization across multiple jurisdictions despite established efficacy profiles. Pharmaceutical manufacturers are preparing for potential reclassification by upgrading production processes, labeling standards, and pharmacovigilance systems to align with OTC compliance requirements. Clinicians are generally supporting these regulatory transitions as expanded non-prescription availability is improving patient access to validated therapies and is reducing delays associated with appointment scheduling.

Prescription to OTC conversion is enabling consumers to initiate therapy earlier through self-managed care, which is reducing clinical workload for routine cases and is improving treatment adherence timelines. Manufacturers are benefiting from broader commercial reach as products are entering retail pharmacy chains, e-commerce platforms, and mass merchandising outlets, thereby expanding revenue opportunities and strengthening brand recognition. Retail stakeholders are diversifying product formats to address heterogeneous user preferences, including topical solutions, applicator-based systems, and combination kits. Consumers are adopting these convenient options as part of routine self-care practices, while healthcare providers are concentrating clinical resources on complex or refractory presentations.

Shift toward Advanced Formulations and Delivery Systems

Companies are actively pursuing growth by engineering advanced formulations and novel delivery platforms that are moving beyond conventional liquids and gels toward higher-precision therapeutic systems. Product development teams are prioritizing improvements such as optimized cryotherapy applicators, medicated adhesive patches, and controlled-release topical matrices that are enhancing dosing accuracy and treatment consistency. These innovations are aligning with consumer demand for home-based interventions that approximate outcomes achieved in clinical settings, thereby strengthening adoption among convenience-oriented users. Healthcare professionals are recognizing the value of these advancements since they are enabling patients to manage uncomplicated cases independently while maintaining clinical effectiveness.

Innovation trajectories are also responding to lifestyle-driven expectations for precision, efficiency, and integration into daily routines. Companies are incorporating ergonomic applicator structures, metered dosing controls, and skin-protective adjunct ingredients to improve adherence and therapeutic outcomes. Research efforts are exploring synergistic combinations of active compounds that accelerate lesion resolution while preserving surrounding tissue integrity. Retail channels are emphasizing these differentiated features through merchandising strategies that facilitate informed decision-making at the point of sale. Consumers are gaining confidence when products provide transparent instructions, predictable timelines, and observable progress indicators. Firms are further differentiating through educational packaging and digital guidance resources that are reinforcing correct usage and strengthening long-term trust. Healthcare providers are benefiting from reduced patient visits for minor dermatological concerns, which allows clinical capacity to focus on complex cases.

Category-wise Analysis

Treatment Type Insights

Salicylic acid is slated to lead in 2026 by holding approximately 50% of the wart remover market revenue share due to its well-established therapeutic profile and strong consumer acceptance. Its dominance is supported by proven keratolytic efficacy, widespread OTC accessibility, cost efficiency, and long-standing familiarity among both patients and healthcare providers. Decades of accumulated safety and performance evidence, combined with consistent physician endorsement, are reinforcing consumer confidence and repeat utilization. The U.S. FDA and the EMA are positively recognizing salicylic acid as a safe and effective ingredient under established OTC monograph frameworks. Prominent retail shelf positioning and inclusion in pharmacist-recommended treatment pathways are further strengthening its commercial leadership and sustaining volume-driven growth across global markets.

Cryotherapy devices are likely to be the fastest expanding segment through 2033, fueled by shifting consumer preferences toward home-use technologies that replicate clinic-grade outcomes. Increasing availability of user-friendly disposable applicators at accessible price points is accelerating adoption across developed and emerging regions. Established brands such as Compound W Freeze Off and Wartner Cryotherapy are maintaining strong market presence in North America and Europe, supported by brand recognition and perceived clinical credibility. Continuous innovation in applicator engineering, including improved temperature regulation and targeted delivery mechanisms, is reducing the probability of collateral skin injury while improving treatment precision. These technological refinements are expanding the eligible user base to include older adults and individuals with sensitive skin profiles.

End-User Insights

Retail pharmacies are poised to command approximately 75% of the wart remover market share in 2026, attributable to their extensive geographic reach and strong consumer trust. Community pharmacists are actively assisting customers in selecting appropriate therapies such as salicylic acid patches and cryotherapy kits, which is increasing purchase certainty among households seeking rapid and practical solutions. Large pharmacy chains such as Walgreens and CVS Health Corporation are reinforcing category visibility through in-store merchandising, promotional campaigns, and private-label offerings that are strengthening OTC product dominance. This channel also benefits from sustained foot traffic, rising self-care awareness, and growing recognition of minor dermatological conditions that can be managed without physician intervention.

Online pharmacies are projected to register the highest 2026-2033 CAGR, as digital health commerce adoption is accelerating across multiple demographic groups. E-commerce platforms such as Amazon Pharmacy and Flipkart Health Plus are extending product availability beyond metropolitan centers, which is improving access for rural populations and digitally engaged younger consumers. Features including price comparisons, user-generated reviews, automated refill programs, and subscription-based purchasing models are strengthening consumer engagement and improving adherence to treatment regimens. Online distribution is also enabling manufacturers to reach previously underserved segments while reducing dependence on physical retail infrastructure.

Regional Insights

North America Wart Remover Market Trends

North America is projected to account for an estimated 38% of the wart remover market value in 2026, boosted by a mature OTC healthcare ecosystem, high consumer awareness of dermatological care, and dense pharmacy distribution networks. Regulatory efficiency is playing a central role, as the U.S. FDA OTC Monograph framework is streamlining product approvals, formulation updates, and rapid commercialization timelines. Canada is maintaining comparable regulatory alignment through Health Canada’s Natural Health Products Directorate (NHPD), which is ensuring consistent product availability and safety standards across the region. Consumers are demonstrating strong trust in established brands and are prioritizing accessible self-treatment solutions for minor skin conditions, ensuring demand stability.

Regional market expansion is further accelerating due to educational initiatives led by professional organizations such as the American Academy of Dermatology (AAD), alongside the proliferation of premium cryotherapy solutions and teledermatology services. Major industry participants including Prestige Consumer Healthcare, Reckitt Benckiser Group, and 3M Health Care are influencing the market through continuous innovation, strong retail partnerships, and diversified product pipelines. Digital commerce platforms such as Amazon Prime Health are increasing repeat purchase frequency by offering rapid fulfillment, subscription options, and algorithm-driven product recommendations. Companies are allocating significant resources to R&D to advance immunomodulatory OTC therapies and digital engagement tools that support treatment adherence. Healthcare providers are integrating virtual consultation models to guide home-based care in a bid to reduce in-clinic demand for routine cases.

Europe Wart Remover Market Trends

Europe stands out as the second-largest regional market for wart removal products, with Germany, the U.K., and France serving as primary revenue contributors. National authorities such as Germany’s Federal Institute for Drugs and Medical Devices (BfArM) and the U.K.’s Medicines and Healthcare products Regulatory Agency (MHRA) are enforcing rigorous quality and safety standards, strengthening trust in OTC dermatology solutions. At the supranational level, the EMA is harmonizing evaluation pathways and OTC switch frameworks, which are facilitating broader cross-border access to approved therapies and accelerating product availability. Pharmaceutical and consumer healthcare companies are benefiting from this structured environment as predictable compliance requirements are enabling efficient market entry for innovative formulations.

In Spain and France, the market is experiencing strong growth momentum due to rising discretionary spending on personal care and dense retail pharmacy infrastructure. Even though regulatory adjustments following the U.K.’s exit from the European Union (EU) have worsened procedural complexities for cross-border product launches, underlying demand fundamentals remain resilient. The competitive environment includes multinational corporations alongside regional brands such as Wartner by Omega Pharma, Bazuka by Dendron Pharmaceuticals Ltd., and Scholl, which are maintaining shelf prominence through established consumer recognition and clinically validated formulations. Manufacturers are increasingly reformulating products to reduce solvent content and incorporate environmentally responsible packaging materials to appeal to sustainability-focused consumers. Retailers are reinforcing these initiatives through point-of-sale education and pharmacist engagement, fostering brand loyalty.

Asia Pacific Wart Remover Market Trends

Asia Pacific is expected to register the fastest growth in the market for wart removers, driven by expanding healthcare infrastructure, rising disposable income, and increasing consumer awareness of self-managed dermatological care. China, Japan, India, and the ASEAN bloc are contributing substantially through policy support and market accessibility improvements. China’s National Medical Products Administration (NMPA) is streamlining OTC product registration pathways, which is facilitating faster entry for multinational brands and accelerating portfolio expansion. Japan is maintaining demand for premium, clinically validated formulations that emphasize safety assurance and product reliability, reflecting strong consumer preference for high-quality healthcare solutions. India is generating significant volume growth through cost-effective product offerings distributed via extensive pharmacy networks and rapidly expanding digital commerce channels. Domestic manufacturers are leveraging lower production costs and localized supply chains to provide competitively priced alternatives, enabling tiered product segmentation that addresses heterogeneous income groups across the region.

Indonesia, Thailand, and Vietnam are rife with substantial untapped opportunities due to young demographics, urbanization trends, and increasing expenditure on personal wellness products. Cross-border e-commerce ecosystems including Shopee, Lazada, and JD Health are accelerating product penetration among urban consumers who prioritize convenience, product variety, and digital purchasing experiences. International companies are forming joint ventures, licensing agreements, and distribution partnerships with regional stakeholders to navigate diverse regulatory requirements and shorten commercialization timelines. These collaborative approaches are ensuring regulatory compliance while enabling product customization to local preferences, including the incorporation of botanical ingredients and culturally relevant formulations.

Competitive Landscape

The global wart remover market exhibits a moderately consolidated structure, with Prestige Consumer, Reckitt Benckiser, Omega Pharma, and 3M Health Care heavily influencing market dynamics. These companies are prioritizing continuous product innovation, particularly through the development of user-centric delivery formats such as medicated adhesive pads, precision applicators, and cryogenic freeze sprays that improve application accuracy and therapeutic outcomes. Strategic investments in digital marketing infrastructure and e-commerce integration are enabling firms to engage digitally oriented consumers who are increasingly relying on online channels for healthcare purchases. Organizations are also diversifying product portfolios to address heterogeneous clinical needs, including formulations for sensitive skin, rapid-action treatment systems, and solutions tailored to different wart subtypes.

The combination of technological advancement and targeted commercialization is reinforcing brand leadership and sustaining customer loyalty across global markets. Companies are focusing on solving practical user challenges such as minimizing application complexity, reducing treatment discomfort, and shortening resolution timelines, which is improving user satisfaction and repeat purchase behavior. Digital engagement campaigns are providing educational content that clarifies correct product usage and sets realistic expectations, thereby enhancing consumer confidence and trust. Portfolio expansion strategies are capturing niche segments, including pediatric-friendly options and products incorporating naturally derived adjunct ingredients, while cross-border e-commerce platforms are extending geographic reach and improving market penetration.

Key Industry Developments

- In January 2026, Verrica Pharmaceuticals announced that the first patient was dosed in its global Phase 3 clinical program evaluating YCANTH® (VP-102) for common warts, marking a key milestone toward potential label expansion into a large unmet dermatology market with no approved prescription therapies.

- In October 2025, Nielsen BioSciences expanded its licensing agreement with Maruho Co., Ltd., granting exclusive rights to develop and commercialize CANDIN® for common warts across China, South Korea, Taiwan, and several ASEAN members.

- In March 2025, the U.S. FDA cleared CryoSurgery Inc.'s CryoFreeze Wart and Skin Tag Remover via 510(k) #K243487. This over-the-counter device treats common and plantar warts in adults and children aged 4+, as well as skin tags in adults aged 22+, demonstrating substantial equivalence to a predicate device.

Companies Covered in Wart Remover Market

- Prestige Consumer Healthcare Inc.

- Reckitt Benckiser Group plc

- Omega Pharma

- 3M Healthcare

- Church & Dwight Co., Inc.

- Dr. Scholl's

- Medline Industries LP

- Medigene AG

- Nuvo Pharmaceuticals Inc.

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

- CIPLA Limited

- Haleon plc

- Blairex Laboratories

Frequently Asked Questions

The global wart remover market is projected to reach US$ 0.8 billion in 2026.

Rising HPV prevalence and advancements in OTC formulations are fueling the market.

The market is poised to witness a CAGR of 3.5% from 2026 to 2033.

Prescription-to-OTC switches and emerging market penetration via e-commerce offer high growth potential to market players.

Prestige Consumer Healthcare, Reckitt Benckiser, Omega Pharma, and 3M Healthcare are some of the key players in the market.