- Pharmaceuticals

- Veterinary Vaccines Market

Veterinary Vaccines Market Size, Share, and Growth Forecast 2026 - 2033

Veterinary Vaccines Market by Vaccine Type (Live Vaccines, Inactivated Vaccines, Recombinant Vaccines, Others), Animal Type (Livestock Animals, Companion Animals, Aquaculture Animals), Disease Type (Rabies, Foot & Mouth Disease, Newcastle Disease, Swine Fever, Others), Route of Administration (Injectable, Oral, Nasal), Distribution Channel (Veterinary Hospitals & Clinics, Veterinary Pharmacies, Online Sales), and Regional Analysis, 2026 - 2033

Veterinary Vaccines Market Share and Trends Analysis

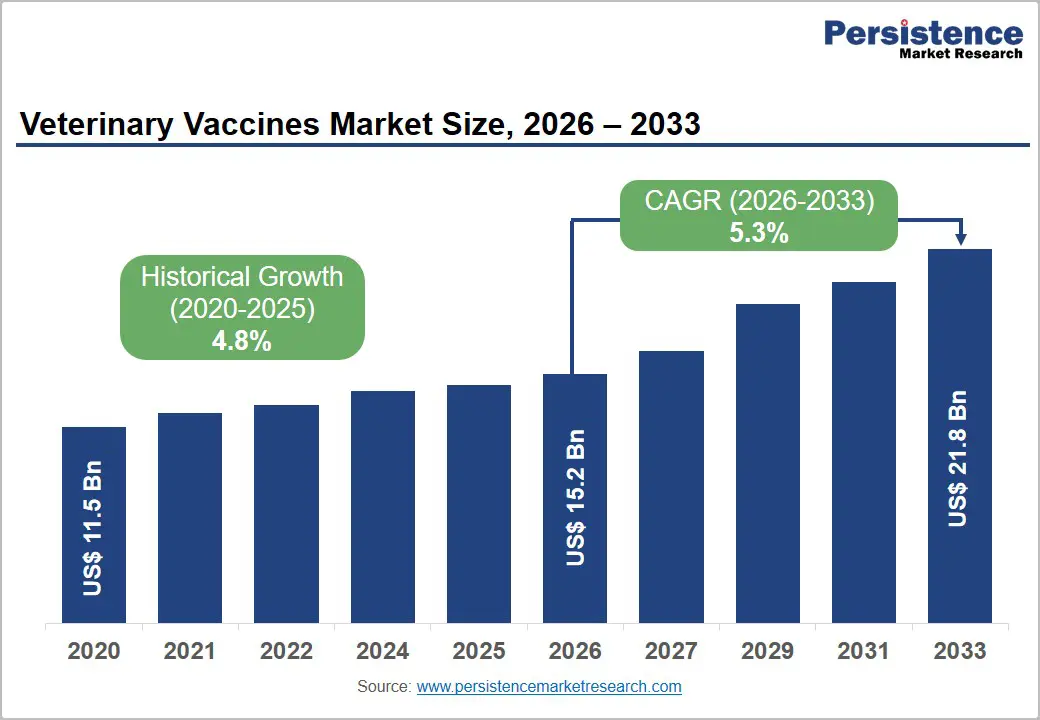

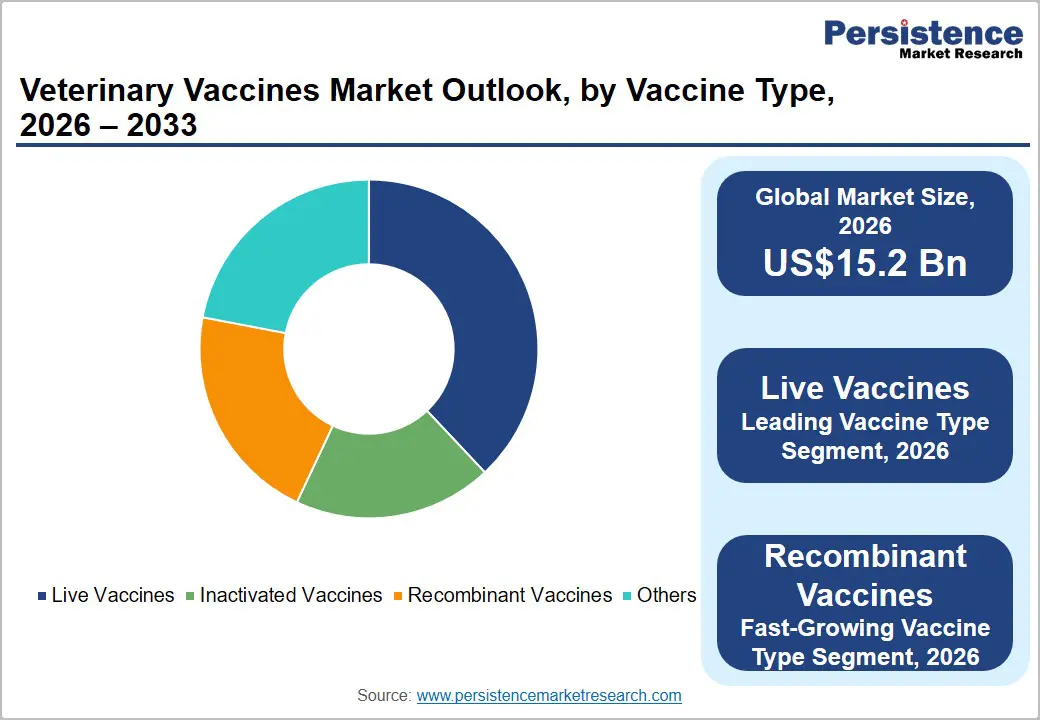

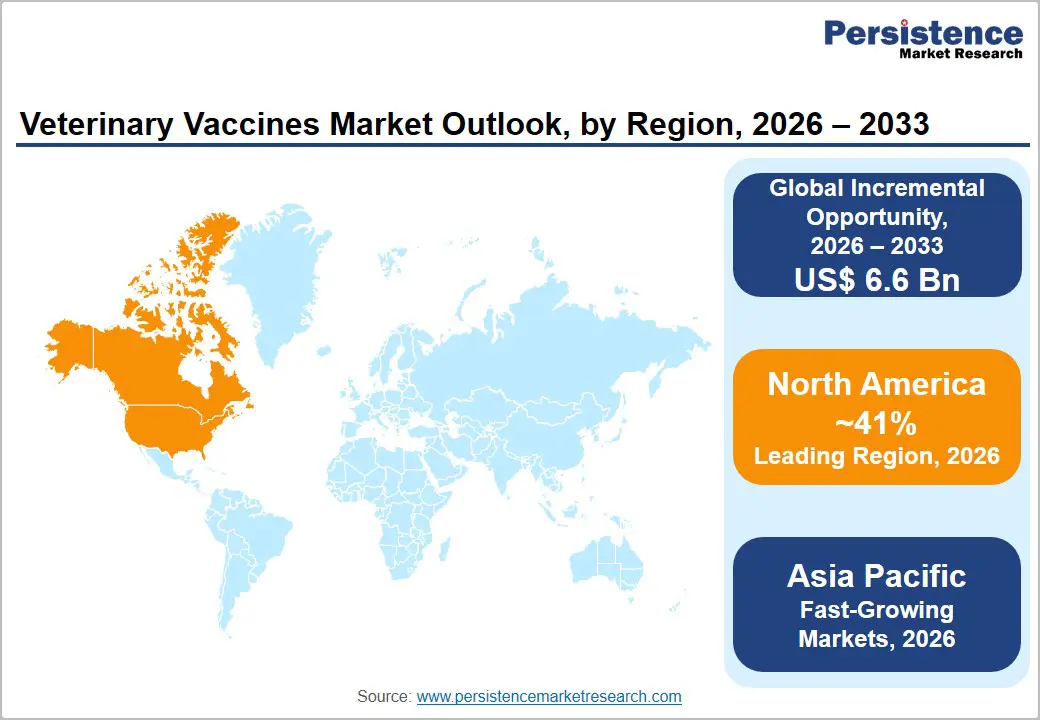

The global veterinary vaccines market size is expected to be valued at US$ 15.2 billion in 2026 and projected to reach US$ 21.8 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

The veterinary vaccines market is experiencing steady growth driven by rising global demand for animal protein, expanding livestock populations, and increasing focus on zoonotic disease prevention. Government-led vaccination programs for diseases such as foot-and-mouth disease, brucellosis, and avian influenza are further strengthening institutional procurement of vaccines across both developed and emerging economies.

Technological advancements, including recombinant, DNA, and vector-based vaccines, are improving efficacy and safety profiles, supporting wider adoption. Companion animal vaccination is also growing due to higher pet ownership and rising expenditure on preventive healthcare.

Key Industry Highlights:

- Leading Region - North America commands approximately 41% of global veterinary vaccine revenues in 2025, driven by 67% U.S. pet ownership (APPA), mandatory rabies vaccination laws across all 50 states, and the highest per-animal veterinary healthcare spending globally, anchored by Zoetis and Merck Animal Health.

- Fast-Growing Market - Asia Pacific is the fast-growing veterinary vaccines market, propelled by China's compulsory FMD/HPAI vaccination programs, India's NADCP targeting 500 million livestock, and rapidly expanding companion animal ownership across urban Southeast Asia and South Korea.

- Dominant Vaccine Type - Live vaccines lead the vaccine type segment with approximately 38% market share in 2025, dominant in poultry disease prevention (Newcastle Disease, IB) via mass water/spray delivery, and core companion animal vaccine protocols (DAPP, FVRCP) globally across leading brands from Zoetis and Boehringer Ingelheim.

- Fast-Growing Segment - Recombinant veterinary vaccines are the fast-growing type, propelled by superior DIVA capability for livestock disease eradication certification, mRNA platform entry via Zoetis' canine influenza vaccine, and expanding aquaculture and swine applications from Boehringer Ingelheim and Ceva.

Market Dynamics

Drivers - Rising Zoonotic Disease Threat and One Health Policy Framework Driving Vaccination Demand

The intensifying global threat of zoonotic disease pathogens transmitted between animals and humans is a critical demand driver for veterinary vaccines under the One Health framework promoted by the World Health Organization (WHO), FAO, and World Organization for Animal Health (WOAH). The WHO estimates that approximately 60% of known infectious diseases and 75% of new or emerging diseases in humans are of animal origin. Rabies alone causes approximately 59,000 human deaths annually per WHO data, with dogs serving as the vector in 99% of cases.

Mass rabies vaccination of animal reservoirs, particularly dogs and livestock in Asia and Africa, is now a formal WHO-FAO-WOAH target to achieve zero human rabies deaths by 2030, creating sustained institutional and government procurement demand.

Companion Animal Population Growth and Premium Preventive Healthcare Spending

The rapid global growth of companion animal ownership, accelerated by the COVID-19 pandemic pet adoption surge, is creating a large and growing premium veterinary vaccine demand segment. The American Pet Products Association (APPA) reported that approximately 67% of U.S. households own a pet, with annual U.S. pet industry spending exceeding US$ 147 billion in 2023.

In Europe, the European Pet Food Industry Federation (FEDIAF) estimates over 340 million pets across member states. Core vaccine schedules for dogs and cats covering rabies, distemper, parvovirus, and feline herpesvirus represent a large, recurring preventive care revenue stream. The trend toward pet humanization is driving companion animal owners to adopt comprehensive preventive healthcare protocols, including vaccines for Leptospirosis, Bordetella, and Lyme disease, significantly expanding the per-animal vaccine revenue opportunity.

Restraints - Cold-Chain Infrastructure Deficiencies in High-Burden Emerging Markets

The vast majority of veterinary vaccines, whether live attenuated or inactivated, require uninterrupted cold-chain maintenance between 2°C and 8°C from production to the point of administration. In several countries with the highest livestock disease and rabies burden across Sub-Saharan Africa, South Asia, and parts of Latin America, unreliable power infrastructure and limited refrigeration access create critical cold-chain gaps. The WOAH has identified vaccine cold-chain breakdown as a leading cause of field vaccination failure, undermining herd immunity targets and constraining the effective market penetration of veterinary vaccines in high-burden geographies.

Opportunities - Recombinant Vaccines: The Fastest-Growing Platform with Superior Safety and Efficacy Profile

Recombinant veterinary vaccines represent the fastest-growing vaccine type segment, offering transformative advantages over conventional live and inactivated platforms in terms of safety, targeted immune response, and DIVA (Differentiating Infected from Vaccinated Animals) capability which is critical for livestock disease surveillance and export market certification. The USDA APHIS and WOAH have endorsed DIVA-compatible recombinant vaccines as a priority tool for FMD and classical swine fever (CSF) eradication programs in endemic countries.

Boehringer Ingelheim's recombinant swine fever vaccine and Ceva's recombinant Newcastle Disease platform exemplify the commercial traction of this modality. The growing pipeline of recombinant vaccines for aquaculture, particularly for salmon and shrimp diseases, represents a further high-growth frontier where conventional vaccines have historically underperformed.

Aquaculture Vaccines: Addressing Rapidly Expanding Disease Control Demand in Fish Farming

Aquaculture is the fastest-growing food production sector globally, with the FAO reporting that aquaculture now supplies over 50% of global fish for human consumption, creating a rapidly expanding demand for aquaculture vaccines to protect fish and shrimp farms from catastrophic disease losses. Infectious Salmon Anemia (ISA), Pancreas Disease (PD), and Infectious Pancreatic Necrosis (IPN) cause multi-billion-dollar losses in salmon aquaculture annually. Norway, the world's largest salmon producer, has virtually eliminated antibiotic use through systematic vaccination, demonstrating the commercial viability of aquaculture vaccines.

Companies including Merck Animal Health, Zoetis, and Vaxxinova are actively expanding their aquaculture vaccine portfolios, representing a high-growth commercial frontier for veterinary vaccine manufacturers through 2033.

Category-wise Analysis

Vaccine Type Insights

Live vaccines represent the leading vaccine type segment in the veterinary vaccines market, commanding approximately 38% of global revenues in 2026. Live attenuated vaccines offer robust, long-lasting immunity with typically a single or two-dose immunization protocol, minimizing labor and administration costs in large-scale livestock operations.

For poultry diseases such as Newcastle Disease and Infectious Bronchitis, live attenuated vaccines are the global standard of care delivered via drinking water or spray, enabling mass administration in commercial flocks of thousands. For companion animals, modified-live virus (MLV) vaccines for canine distemper, parvovirus, and adenovirus (DAPP protocols) represent the backbone of core preventive veterinary care globally. Leading products from Zoetis, Merck Animal Health, and Boehringer Ingelheim dominate the live vaccine revenue base.

Animal Type Insights

Livestock animals represent the leading animal type segment in the veterinary vaccines market, accounting for approximately 55% of global revenues in 2026. The sheer scale of the global livestock population, approximately one billion cattle, one billion pigs, and over 30 billion poultry per FAO estimates, creates an immense and recurring vaccine demand base that dwarfs the companion animal sector by volume. Government-mandated vaccination programs for FMD, Newcastle Disease, Classical Swine Fever, and Brucellosis create institutionalized livestock vaccine procurement across over 100 countries under WOAH frameworks. The economic cost of livestock disease outbreaks, including the US$ 21 billion annual global FMD impact (FAO/WOAH) reinforces the financial imperative for comprehensive livestock vaccination programs globally.

Disease Type Insights

Foot-and-Mouth Disease (FMD) is the leading disease type segment in the veterinary vaccines market, accounting for approximately 24% of global revenues in 2025. FMD is the most economically significant livestock disease globally, highly contagious, infecting all cloven-hoofed species, and capable of decimating trade access for affected countries. The WOAH coordinates the Global FMD Control Strategy (GF-TADs), mandating systematic vaccination in endemic countries across Asia, Africa, and Latin America. Government-funded FMD vaccination campaigns consuming billions of doses annually sustain the segment's revenue leadership with major producers including Indian Immunologicals Ltd., Biogenesis Bagó, and multinational animal health companies supplying these high-volume institutional markets.

Route of Administration Insights

Injectable vaccines represent the leading route of administration in the veterinary vaccines market, accounting for approximately 62% of revenues in 2025. Injectable delivery subcutaneous, intramuscular, or intradermal ensures precise dosing, reliable immunogenicity, and predictable immune response outcomes, making it the preferred route for livestock production vaccines and companion animal core immunization protocols. The WOAH and USDA APHIS vaccination guidelines for FMD, BRD, and reproductive disease management specify injectable administration as the standard protocol for most large animal species.

For companion animals, injectable multi-valent combination vaccines administered by licensed veterinarians represent the clinical gold standard for core vaccine schedules under WSAVA (World Small Animal Veterinary Association) vaccination guidelines.

Distribution Channel Insights

Veterinary hospitals and clinics represent the leading distribution channel for veterinary vaccines, accounting for approximately 52% of revenues in 2025. Veterinary hospitals and clinics are the primary administration sites for companion animal vaccines and the most trusted point-of-care channel for pet owners seeking preventive health services. In the United States, the American Veterinary Medical Association (AVMA) reports over 45,000 practicing veterinarians operating across private practice settings.

Clinic-administered vaccine protocols aligned with WSAVA and AAHA guidelines drive consistent, recurring immunization visits and generate stable consumable revenue. The growth of corporate veterinary practice networks (VCA, Banfield) is consolidating purchasing power and driving volume-based vaccine procurement agreements with manufacturers.

Regional Insights

North America Veterinary Vaccines Market Trends and Insights

North America leads the global veterinary vaccines market with approximately 41% revenue share in 2025, driven by the highest companion animal ownership rates globally, comprehensive regulatory frameworks under USDA CVB, and the world's highest per-animal veterinary healthcare spending. The region benefits from a 6trong companion animal vaccine compliance culture and robust mandatory rabies vaccination statutes across all U.S. states, sustaining high-volume preventive care purchasing.

U.S. Veterinary Vaccines Market Size

The United States accounts for approximately 86% of North American veterinary vaccine revenues in 2025. With over 90 million dogs and 94 million cats (APPA), mandatory rabies vaccination laws in all 50 states, and annual core vaccine protocol adoption reinforced by AAHA guidelines, the U.S. is the world's largest single national veterinary vaccine market. Zoetis and Merck Animal Health dominate commercial revenues.

Europe Veterinary Vaccines Market Trends and Insights

Europe is the second-largest veterinary vaccines market, characterized by a strong regulatory framework under EMA's Committee for Medicinal Products for Veterinary Use (CVMP), high companion animal ownership, and active EU livestock disease surveillance programs. The region's focus on antimicrobial resistance (AMR) reduction under the European Green Deal is driving the substitution of antibiotics with prophylactic veterinary vaccines across cattle and poultry farming.

Germany Veterinary Vaccines Market Size

Germany is the largest European veterinary vaccines market, contributing approximately 18% of regional revenues in 2026. Germany's 3.8 million dairy cattle (Destatis), high companion animal density, and Boehringer Ingelheim Animal Health headquarters drive strong domestic vaccine production and utilization. German farmers' high compliance with BVD, BHV-1, and respiratory vaccine protocols reinforces premium vaccine adoption.

U.K. Veterinary Vaccines Market Size

The U.K. accounts for approximately 13% of European veterinary vaccine revenues in 2025. Strong companion animal ownership, with over 13 million dogs and 12 million cats per PFMA data and post-Brexit VMD regulatory pathways, sustains market activity. The ongoing bovine tuberculosis (bTB) crisis drives government investment in cattle bTB vaccine development, with APHA field trials representing a potential new market segment.

France Veterinary Vaccines Market Size

France represents approximately 14% of European veterinary vaccine revenues in 2025, supported by large cattle and poultry sectors and a strong domestic veterinary pharmaceutical industry anchored by Ceva Santé Animale and Virbac. France's active national FMD, Bluetongue, and avian influenza contingency vaccination programs sustain government-funded institutional vaccine demand across multiple disease indications.

Asia Pacific Veterinary Vaccines Market Trends and Insights

Asia Pacific is the fastest-growing veterinary vaccines market, driven by the world's largest livestock populations in China and India, compulsory FMD and Newcastle Disease vaccination programs, and a rapidly expanding companion animal sector. China enforces mandatory FMD, Classical Swine Fever, and Highly Pathogenic Avian Influenza (HPAI) vaccination under national animal disease control programs, creating vast institutional procurement volumes for government-subsidized vaccines through provincial health agencies.

India Veterinary Vaccines Market Size

India's veterinary vaccines market is valued at approximately US$ 380 million in 2025, growing rapidly, driven by the government's National Animal Disease Control Programme (NADCP) targeting 500 million livestock for FMD and brucellosis vaccination. Domestic manufacturers Indian Immunologicals Ltd. and Hester Biosciences supply the bulk of institutional vaccine volumes, with strong export competitiveness across Southeast Asia and Africa.

Competitive Landscape

The veterinary vaccines market is highly competitive and characterized by continuous innovation in vaccine technologies, including live attenuated, inactivated, and recombinant platforms. Market players are focusing on expanding product portfolios to address a wide range of livestock, companion animal, and aquaculture diseases. Increasing demand for preventive animal healthcare, rising zoonotic disease concerns, and growing pet ownership are intensifying competition across regions. Companies are investing in R&D for next-generation vaccines with improved safety, efficacy, and longer protection duration.

Key Developments:

- In March 2026, the Bhubaneswar Municipal Corporation (BMC) had launched a citywide mass anti-rabies vaccination drive targeting around 52,000 stray dogs across the city as part of its public health initiative to control rabies and reduce dog bite risks.

- In April 2026, a first-of-its-kind combination vaccine was launched in Kenya to enhance protection against small ruminant diseases such as Peste des Petits Ruminants (PPR), Contagious Caprine Pleuropneumonia (CCPP), and Sheep and Goat Pox.

- In November 2025, Zoetis announced the U.S. launch of Vanguard® Recombishield™, a new injectable recombinant vaccine for dogs designed to protect against Bordetella bronchiseptica, the bacterium responsible for kennel cough.

Companies Covered in Veterinary Vaccines Market

- Zoetis Inc.

- Merck Animal Health

- Boehringer Ingelheim Animal Health

- Elanco Animal Health

- Ceva Santé Animale

- Virbac

- HIPRA

- Phibro Animal Health Corporation

- Indian Immunologicals Ltd.

- Vetoquinol

- Biogénesis Bagó

- Vaxxinova International

- Hester Biosciences Limited

Frequently Asked Questions

The global veterinary vaccines market size is projected to be valued at US$ 15.2 billion in 2026.

The primary drivers are the global zoonotic disease threat under the One Health framework, with 75% of emerging human diseases of animal origin (WHO) and rabies, causing 59,000 annual human deaths, and the companion animal ownership surge, with over 340 million pets in Europe (FEDIAF) and US$ 147 billion in annual U.S. pet spending (APPA), driving premium preventive healthcare demand.

North America leads with approximately 41% market share in 2025. The United States accounts for ~86% of regional revenues, supported by mandatory rabies vaccination laws in all 50 states, over 90 million dogs and 94 million cats (APPA), comprehensive USDA CVB regulatory frameworks, and commercial dominance of Zoetis, Merck Animal Health, and Boehringer Ingelheim.

Use of recombinant and mRNA veterinary vaccines, exemplified by Zoetis' canine influenza mRNA vaccine launch in 2025 and the rapidly growing aquaculture vaccines segment, where the FAO reports aquaculture supplying over 50% of global fish consumption and Norway has demonstrated the transformative potential of systematic fish vaccination in eliminating antibiotic dependence in salmon farming.

The leading companies include Zoetis Inc. (largest global animal health company by revenue), Merck Animal Health, Boehringer Ingelheim Animal Health, Elanco Animal Health, Ceva Santé Animale, Virbac, HIPRA, Indian Immunologicals Ltd., Hester Biosciences, and Vaxxinova International.