- Healthcare Services

- Urgent Care Market

Urgent Care Market Size, Share, and Growth Forecast for 2025 - 2032

Urgent Care Market by Service (Trauma/Injury Treatment, Acute Illness Treatment, Diagnostic Services, Immunization & Vaccination, Others), Ownership (Corporate Owned, Hospital Owned/Joint Venture Centers, Physician Owned), Payment Source (Commercial / Managed Care Payor, Government Payor), and Regional Analysis

Urgent Care Market Outlook (2025-2032)

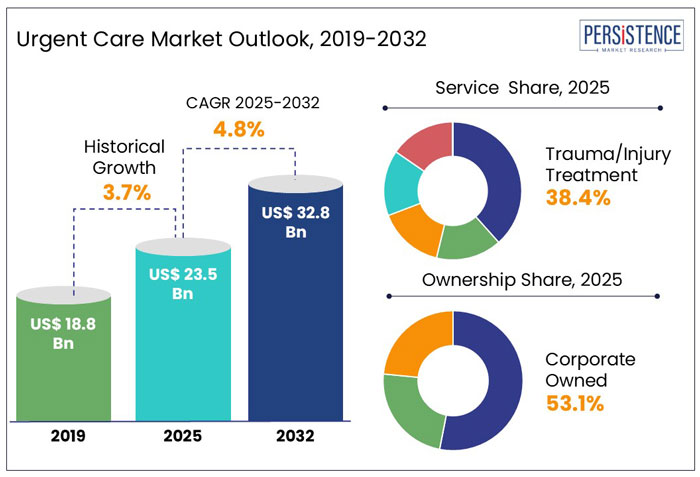

Globally, the market for Urgent Care is forecasted to expand at a CAGR of 4.8% between 2025 and 2032. The global market is expected to reach a valuation of US$ 32.8 Bn in 2032 from US$ 23.5 Bn in 2025.

|

Global Market Attributes |

Key Insights |

|

Urgent Care Market Size (2025E) |

US$ 23.5 Bn |

|

Market Value Forecast (2032F) |

US$ 32.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.7% |

Historical Growth and Course Ahead

Urgent Care Market is a specialized healthcare service that bridges the divide between emergency room and primary care by providing immediate medical attention for non-life-threatening injuries and illnesses. These establishments provide timely access to medical specialists without requiring appointments, generally functioning outside of standard business hours.

The global urgent care market expanded at a CAGR of 3.7% from 2019 to 2024.

Historically, the market was driven by the increasing demand for accessible and affordable healthcare options. Urgent care centers prioritize the provision of medical attention that is both prompt and economical, attending to ailments such as minor fractures, infections, and symptoms of the virus. By adopting a patient-centric approach, they ensure accessibility and convenience, thereby alleviating the strain on emergency rooms caused by non-emergency situations.

The worldwide urgent care industry is experiencing substantial expansion because of a multitude of propelling factors. Factors including growing incidence of chronic illnesses, rising need for alternative treatment options for economical substitutes to emergency rooms visits and rising healthcare costs contribute to the market's expansion.

Market expansion is further propelled by technological advancements, such as the integration of telemedicine in urgent care, which contribute to the healthcare industry's dynamic and ever-changing environment. All these factors are presumed to boost the global market to reach a valuation of US$ 32.8 Bn by 2032.

Urgent Care Market Growth Drivers

“Rising Need for Accessible and Economical Healthcare Solutions”

Growing demand for accessible and economical healthcare solutions is one of the key factors driving the global market for urgent care services. Rising healthcare costs makes patient turn to urgent care centers to seek timely medical attention for non-life-threatening conditions.

Urgent care centers offer an appealing alternative to conventional healthcare settings by offering appointment-free services for minor ailments, injuries, and preventive care. Thereby offering significant savings compared to emergency room visits. Streamlined operations, decreased overheads, and an emphasis on specific, non-complex medical issues all contribute to urgent care centers becoming an essential part of the modern healthcare landscape.

Growth Restraints

“Regulatory and Licensing Obstacles”

The global urgent care market is frequently constrained by the regulatory and licensing obstacles that these facilities must contend with. The presence of regulatory complexities in various countries and regions may present challenges to the establishment and smooth functioning of urgent care facilities. Ensuring adherence to diverse regulations, licensing prerequisites, and healthcare policies poses a formidable challenge and demands substantial resources from service providers seeking to expand their operations on a global scale.

“Presence of Emergency Rooms, and Conventional Healthcare Providers”

Although urgent care centers provide a beneficial substitute for non-critical medical situations, they frequently encounter the difficulty of differentiating themselves and becoming the preferred option among patients who are accustomed to seeing primary care physicians and are inclined to feel rushed in emergency rooms.

Effective marketing strategies that inform the public about the specific advantages of urgent care-including reduced costs, shortened wait times, and easy accessibility—are necessary to surmount this obstacle. Furthermore, as conventional healthcare providers acknowledge the need for urgent healthcare services, they increase their business hours or integrate urgent care models into their operations, thereby intensifying competition.

Urgent Care Market Opportunities

“Rising Penetration of Telemedicine, and Digital Health Technologies”

An opportunistic factor propelling the expansion of the worldwide urgent care industry is the rising prevalence of telemedicine and digital health technologies. The ongoing progression of technology has sparked an increasing inclination towards the incorporation of telehealth solutions into urgent care services. This development presents fresh prospects for improved patient engagement and broader outreach.

Telemedicine in urgent care facilitates remote access for patients to healthcare professionals, enabling urgent care centers to expand their service offerings beyond physical locations and provide expeditious consultations for non-emergent matters.

Telehealth solutions further enable virtual consultations via secure messaging platforms or video calls, enhancing convenience for patients unable to visit urgent care centers. This alleviates the strain on healthcare facilities through the diversion of less complicated cases from emergency rooms. Additionally, digital health technologies in urgent care facilitates remote monitoring of chronic conditions, thereby encouraging early intervention and preventive care.

Category-wise Insights

Which are the Most Sought-after Urgent Care Services?

“Increasing Patient Demand for Timely Trauma and Injury Care in Urgent Care”

Trauma and injury treatment is the most sought-after urgent care service, accounting for 38.4% of the global revenue share. This demand is driven by the need for quick intervention without necessitating visit to emergency room, provision of timely and cost-effective alternative to traditional emergency departments for minor to moderate injuries, such as sprains, fractures, and cuts. Rising number of accidents and trauma cases positions trauma and injury treatment as a critical focus for urgent care providers.

- WHO’s 2024 data revealed 4.4 million deaths occur annually due to injuries, including both unintentional and violence-related, making up nearly 8% of all deaths. The 72nd World Health Assembly (WHA) emphasized the critical role of Emergency Care systems in achieving universal health coverage and providing timely care for the acutely ill and injured. The guidelines offer a framework for member states and WHO to collaborate on strengthening emergency trauma and care systems.

Which is the Largest Segment in Terms of Ownership?

“Operational Excellence in Corporate-Owned Urgent Care Centers Across Multiple Locations”

Corporate owned urgent care held the highest market share of around 53.1% within the global urgent care services industry. Urgent care facilities that are owned by corporations frequently possess the infrastructure and resources necessary to establish a vast network of centers, thereby serving a diverse patient population. The prominence of the organization is a result of their capacity to allocate resources towards marketing, technology, and operational efficiency. The sector that is anticipated to experience the most rapid expansion is physician-owned and joint ventures owned urgent care.

The participation of private equity and joint ventures provides urgent care services with financial support and strategic alliances, which facilitate swift growth and advancement. These entities frequently demonstrate agility in adjusting to market trends and possess the capability to exploit nascent opportunities, thereby propelling the urgent care market towards accelerated expansion. The dynamic and swift growth of urgent care services is a result of the adaptability and strategic methodology employed by private equity and joint ventures.

Country-wise Insights

Why is the North America Urgent Care Sector a Prominent Market?

Widespread Accessibility of Urgent Care Alternatives to Uphold Leadership Position of North America

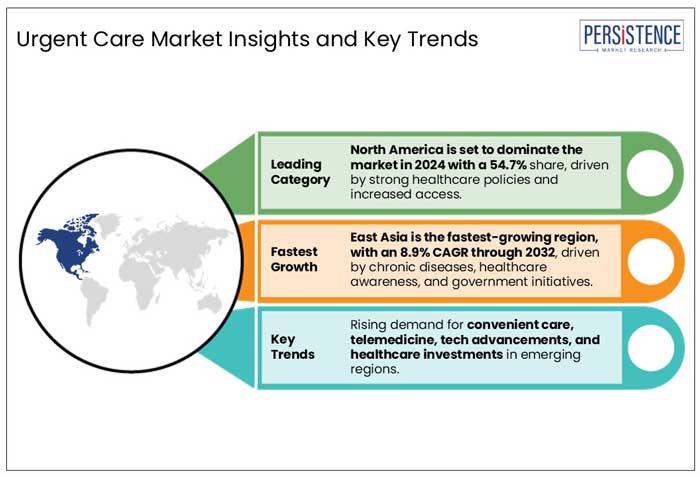

North America held the largest market share in the global urgent care service industry with the revenue share of around 54.7% in 2024. This growth can be ascribed to a multitude of factors, encompassing a firmly established healthcare infrastructure, considerable awareness of urgent care alternatives, and a cultural inclination towards promptly pursuing medical intervention for non-threatening conditions. This has led to substantial expansion in urgent care facilities to meet the demand for accessible medical care.

Additionally, widespread availability of insurance coverage substantially contributes to the market share in the region. North America's status as the preeminent market for urgent care services is further solidified by the presence of key market participants and ongoing initiatives to improve the efficacy of healthcare delivery.

- According to Urgent Care Association 2024 statistics, the number of urgent care centers in the U.S. has seen an exponential growth from over 8000 in 2016 to nearly 15000 in 2024.

- More than 200 million patients are treated in an urgent care setting yearly.

- Over 89% of the U.S. population lives within a 20-minute drive of an urgent care center, while more than 78% within a 10-minute drive.

How can Urgent Care Providers Meet Europe's Growing Healthcare Demand?

“Transforming Europe’s Healthcare Landscape with Efficient Urgent Care Services”

Europe urgent care market is poised to become a highly profitable market for urgent care service providers during the forecast period. In several European countries, accident and emergency (A&E) services are the primary point of care for both urgent and minor health issues leading to severe overcrowding in A&Es. Given this ongoing strain on A&E departments, Europe’s healthcare system presents a significant opportunity for urgent care service providers for patients seeking faster, and more accessible solutions.

Such environment further provides great opportunities for the urgent care service providers to offer specialized care services, enhancing patient satisfaction, while relieving pressure from the overburdened traditional hospital systems.

- As per the 2019 study, the number of non-urgent visits in hospital emergency departments (ED) annually grew by 8.5% in England and 5% in Belgium, significantly highlighting the growing demand for urgent care services.

Why is Asia Pacific Emerging as a Lucrative Market for Urgent Care Services?

“Asia Pacific Urgent Care Market to Benefit from Pacing Healthcare Developments in the Region”

Asia Pacific is anticipated to witness the most rapid expansion of the urgent care services market on a global scale. Increasing healthcare awareness, accelerated population growth, and economic development all contribute to the region's rising demand for immediate and cost-effective medical services.

Asian governments are investing in healthcare infrastructure, while urbanization and changes in lifestyle contribute to an increased prevalence of non-urgent health conditions. The expansion of urgent care services is also accelerated by technological advances and integration of telehealth solutions into healthcare systems. These factors position Asia at the forefront of the global urgent care market's exponential expansion, demonstrating its capacity for significant development and growth in the foreseeable future.

Competitive Landscape

- Numerous strategic initiatives are being implemented by service providers of urgent care industry. Prominent players are allocating resources towards marketing and branding endeavors to establish a unique reputation and enhance customer consciousness. Educational initiatives, community outreach programs, and targeted advertising campaigns are among these efforts to promote the advantages of urgent care services.

- In July 2025, the University of Maryland Urgent Care announced expansion of its services by opening two University of Maryland Urgent Care centers in Anne Arundel County. This initiative is designed to improve access to urgent care for local residents, offering prompt medical attention for non-life-threatening conditions.

- In September 2024, Yale New Haven Health (YNHH) unveiled a rebrand of its urgent care centers, marking a major shift in its healthcare services. This change was prominently showcased with the opening of a new facility at 340 Grasmere Ave. in Fairfield, Connecticut.

- In July 2024, Virginia Mason Franciscan Health (VMFH) formed a partnership with Intuitive Health, a company recognized for its innovative healthcare delivery approach. This collaboration seeks to improve access to healthcare services for residents in the Puget Sound region. The partnership aims to meet the increasing demand for accessible and efficient healthcare, especially in light of the challenges brought on by the COVID-19 pandemic and ongoing public health needs.

- In July 2024, CentraCare joined forces with KeyCare to offer patients virtual urgent care services accessible anytime and anywhere. This collaboration utilizes KeyCare’s Epic-based telehealth platform, aimed at improving healthcare delivery through digital solutions.

Companies Covered in Urgent Care Market

- NextCare Urgent Care

- Aurora Urgent Care

- MinuteClinic, LLC

- HealthWorks, Inc.

- MedExpress

- FastMed Urgent Care

- AFC/Doctors Express, LLC, U.S.

- Patient First

- TexasMedClinic

- CareSpot Express Healthcare

- Concentra Inc.

- CareSpot Express Healthcare LLC

- MD Now

- Bellin Health

- Hometown Urgent Care & Occupational Health

- American Family Care

- Dignity Health Care

- USA HealthWorks

Frequently Asked Questions

The market is set to reach US$ 23.5 Bn in 2025.

North America is projected to hold the largest share of the industry in 2025.

Services for trauma/injury treatment dominates the global market.

East Asia is estimated to be the most lucrative sector for the urgent care service providers.