- Biotechnology

- Transforming Growth Factor Market

Transforming Growth Factor Market Size, Share, and Growth Forecast 2026 - 2033

Transforming Growth Factor Market by Product Type (TGF-beta, Bone Morphogenetic Proteins, Activin), by Application (Oncology, Fibrosis, Cell & Stem Cell Research, Wound Healing, Autoimmune Disorders), by End User (Pharmaceutical & Biotechnology Companies, Research Institutes & Universities, CROs & CDMOs, Hospitals & Clinics), by Regional Analysis, 2026-2033

Transforming Growth Factor Market Size

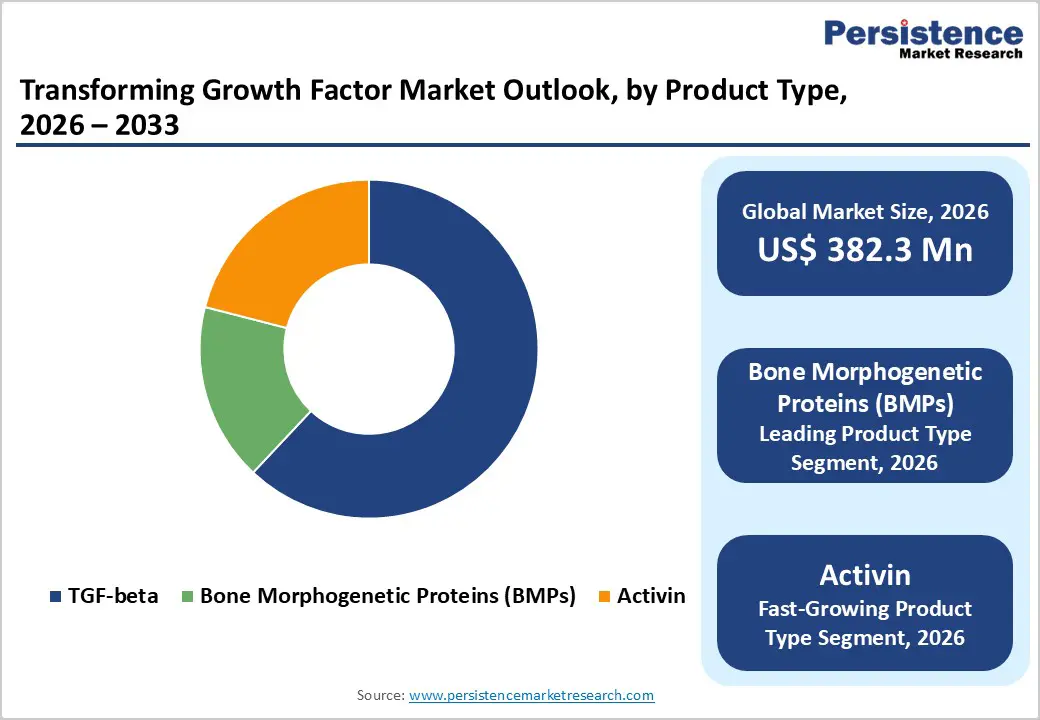

The global Transforming Growth Factor (TGF) market size is expected to be valued at US$ 382.3 million in 2026 and projected to reach US$ 627.3 million by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

The market is on a structurally positive growth path, supported by its central role in disease biology and the spread of advanced biomedical research and therapies. Growth is underpinned by rising use of TGF-related reagents and therapeutics in oncology, fibrosis, regenerative medicine, and autoimmune disease research, where TGF signaling modulates cell proliferation, differentiation, and immune responses. As more TGF-pathway–targeted molecules progress through clinical pipelines and receive regulatory support, adoption of high-value TGF products by pharmaceutical companies, academic institutes, and CROs is expected to accelerate.

Key Market Highlights

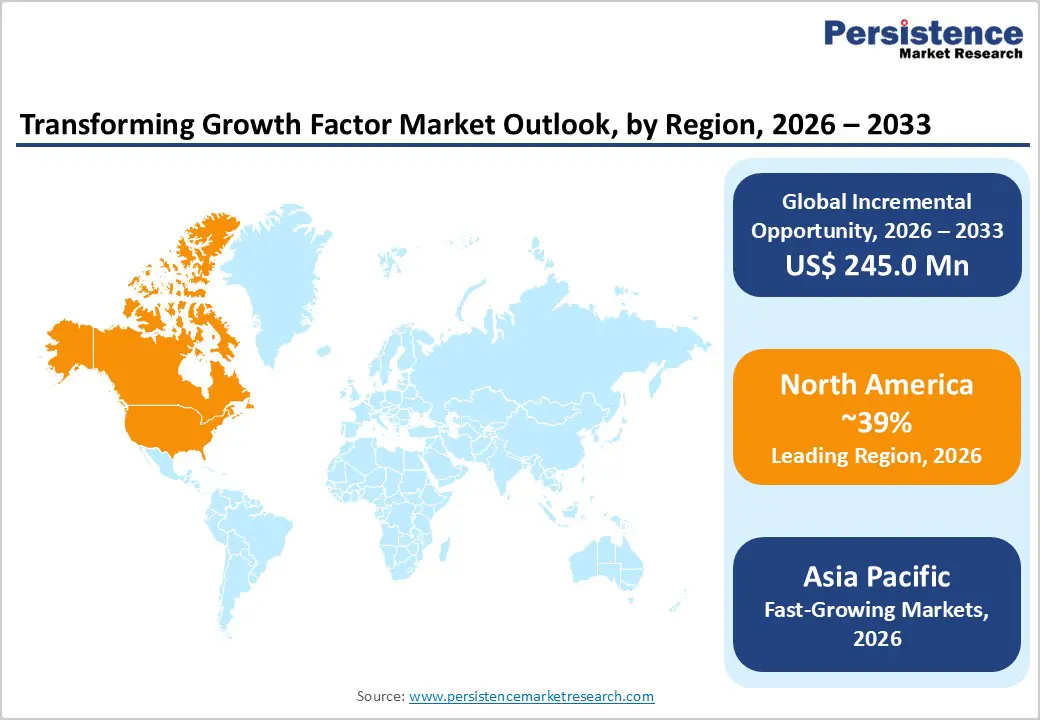

- North America remains the leading region in the Transforming Growth Factor market, contributing around 39% of global revenue in 2025, supported by high R&D spending, large biopharma presence, and favorable regulatory programs that promote innovation in TGF-targeting therapies and research tools.

- Asia Pacific is poised to be the fastest-growing regional market through 2033, as China, Japan, India, and ASEAN countries scale up biopharma manufacturing, invest heavily in clinical research, and expand adoption of TGF-family reagents across oncology, regenerative medicine, and autoimmune research.?

- Among product types, Bone Morphogenetic Proteins (BMPs) hold a leading estimated 62% share in 2025, anchored by long-standing use of recombinant BMP-2 and BMP-7 in spinal fusion, fracture repair, and craniofacial applications, along with growing interest in novel delivery systems and biomaterials.

- The Activin segment is expected to grow fastest within the TGF superfamily, catalyzed by the approval of an activin receptor–targeting fusion protein for pulmonary arterial hypertension and a growing pipeline of agents for hematologic and fibrotic diseases, creating attractive opportunities for specialized suppliers.

- Combination strategies that pair TGF-beta inhibitors with immune checkpoint inhibitors represent one of the most significant future revenue opportunities, with dozens of active trials and regulatory designations indicating strong momentum for TGF-centric approaches to overcoming immunotherapy resistance in solid tumors.

| Key Insights | Details |

|---|---|

|

Transforming Growth Factor Market Size (2026E) |

US$ 382.3 million |

|

Market Value Forecast (2033F) |

US$ 627.3 million |

|

Projected Growth CAGR (2026-2033) |

7.3% |

|

Historical Market Growth (2020-2025) |

6.8% |

Market Dynamics

Rising prevalence of chronic diseases and cancer

Growing global burden of chronic diseases, particularly cancer, fibrosis, and autoimmune disorders, is a fundamental driver for the Transforming Growth Factor market. In many solid tumors, dysregulated TGF-beta signaling contributes to epithelial–mesenchymal transition (EMT), metastasis, and immune escape, making TGF a critical focus in oncology research and drug development. Global cancer incidence exceeded 19–20 million new cases in recent years, with further increases projected due to aging populations and lifestyle risk factors, which sustains demand for TGF-focused assays, recombinant proteins, and inhibitors used in preclinical and translational research. Fibrotic diseases are estimated to account for more than 1.7 million deaths annually worldwide, and TGF is recognized as a master regulator of tissue fibrosis, encouraging development of TGF-pathway–modulating therapies and associated research tools.

Advances in regenerative medicine and cell therapy

Rapid expansion of regenerative medicine, tissue engineering, and cell therapy is significantly boosting demand for TGF-family growth factors, especially in controlled differentiation and maintenance of pluripotent stem cells. TGF-beta and related ligands regulate key processes such as stem cell fate, immune tolerance, and extracellular matrix remodeling, making them indispensable in protocols for induced pluripotent stem cell (iPSC) culture, mesenchymal stem cell (MSC) expansion, and organoid development. Global cell therapy markets have been growing at high single- to low double-digit CAGRs, and a substantial share of those workflows use TGF and other growth factors as critical reagents for process optimization and quality control. Supportive regulatory stances on advanced therapy medicinal products (ATMPs), along with increasing numbers of cell- and gene-therapy clinical trials, are translating into higher recurring consumption of TGF-based proteins and media supplements by biopharma and specialized CDMOs.

Market Restraints

Regulatory complexity and extended development timelines

The Transforming Growth Factor market faces structural headwinds from stringent regulatory demands applied to biologics, recombinant proteins, and advanced TGF-targeting therapeutics. Bringing a novel biologic from discovery to approval can require 10–15 years and investments often exceeding US$ 1–2 billion, including extensive nonclinical safety studies and multi-phase clinical programs. For TGF-pathway inhibitors and agonists, regulators such as FDA and EMA require robust characterization of pleiotropic effects, immune modulation, and long-term safety, which increases data requirements and risk of delay. Requirements around GMP manufacturing, comparability, and analytical validation can add 15–20% to development costs and make it harder for smaller biotechs to sustain long programs, limiting the breadth of commercially available TGF therapeutics.?

Market Opportunities

Expanding therapeutic applications of Activin pathway modulation

Within the TGF superfamily, the Activin pathway is emerging as a particularly attractive high-growth area as clinical validation accumulates. The approval of Sotatercept (Winrevair), an activin receptor type IIA-Fc fusion protein for pulmonary arterial hypertension (PAH) in 2024, has demonstrated that targeting the activin signaling axis can yield meaningful clinical benefit in severe cardiovascular disease. Multiple companies are now developing activin-modulating agents for hematologic conditions, anemia of chronic disease, and fibrotic indications, translating into heightened demand for activin ligands, antagonists, and analytical assays. Early-stage trials in myelodysplastic syndromes (MDS) and oncology settings further broaden the addressable opportunity, and as proof-of-concept data matures, the Activin segment is expected to outpace the overall TGF market, making it a key strategic focus for both established suppliers and innovative biotech firms.

Integration of TGF-beta inhibitors into immuno-oncology combinations

A major opportunity lies in combining TGF-beta inhibitors with immune checkpoint inhibitors (ICIs) such as anti–PD-1 or anti–PD-L1 antibodies to overcome primary or acquired resistance. TGF-beta is known to suppress antitumor immunity by promoting regulatory T cells, excluding effector T cells from tumors, and fostering an immunosuppressive microenvironment, so dual targeting of checkpoints and TGF-beta can synergistically restore immune responses. Several clinical candidates, including small-molecule inhibitors, antibodies, and oncolytic viruses encoding TGF-beta traps, are under evaluation in Phase I–III trials across solid tumors like melanoma, NSCLC, and GI cancers. A recent example is a TGF-beta–inhibiting oncolytic adenovirus that received FDA Fast Track designation in combination with ICIs for advanced soft-tissue sarcoma, underscoring regulatory and clinical enthusiasm for this strategy. If such combinations deliver durable survival gains, they could unlock a multi-billion–dollar addressable opportunity for TGF-focused platforms in oncology.

Category-wise Insights

Product Type Analysis

Bone Morphogenetic Proteins (BMPs) represent the leading product type in the Transforming Growth Factor market, accounting for about 62% share in 2025. BMPs such as BMP-2 and BMP-7 have long-standing clinical use in orthopedic and spinal indications, supported by strong mechanistic and clinical data on osteoinduction and bone regeneration. FDA-cleared products like INFUSE Bone Graft (recombinant human BMP-2) and devices using OP-1 (recombinant human BMP-7) have shown improved fusion rates and reduced need for autograft harvesting in select spinal and fracture procedures. The high procedure volume in spinal fusion and trauma surgery, along with exploration of BMPs in dental, craniofacial, and orthopedic revision contexts, has helped establish BMPs as the backbone of commercial TGF-family utilization. Continued innovation in controlled-release carriers and biomaterial scaffolds is further strengthening BMPs’ position as the dominant revenue contributor among TGF-related products.

Application Analysis

Oncology is the dominant application area for the Transforming Growth Factor market, capturing the largest share of demand due to the central role of TGF-beta signaling in tumor biology and the intensity of global oncology R&D spending. TGF-beta exerts a tumor-suppressive effect in early disease but later promotes invasion, metastasis, immune evasion, and therapy resistance, making it a high-value target from discovery through clinical development. As of the mid-2020s, dozens of TGF-pathway modulators are in clinical development, including ligand traps, receptor kinase inhibitors, antisense oligonucleotides, and viral vectors encoding TGF antagonists. These programs drive extensive use of TGF reagents in model development, biomarker assays, and combination studies with immunotherapies and targeted agents. Oncology-focused CROs and translational centers employ TGF-related tools in preclinical efficacy and safety testing, reinforcing oncology as the largest and technically most demanding segment of the market.

End User Analysis

Pharmaceutical and biotechnology companies form the leading end-user segment, accounting for the largest share of spending on TGF-related products and services. Large pharma and mid-size biotech firms run multi-indication pipelines targeting TGF-beta, activin, and BMP pathways, requiring significant volumes of recombinant proteins, neutralizing antibodies, ELISA kits, cell-based assays, and GMP-grade materials for both research and clinical supply. Suppliers such as Thermo Fisher Scientific, Merck KGaA, Lonza, and Bio-Techne cater heavily to this segment with broad product portfolios and customized production capacity. Research institutes and universities represent another important user group, producing a high volume of TGF-focused publications and early-stage discoveries that often seed later commercial programs. CROs and CDMOs are increasingly central as outsourcing partners for biopharma, providing assay development, toxicology, clinical trial management, and biologics manufacturing that incorporate TGF reagents, thereby expanding institutional participation and recurring demand.

Regional Insights

North America Transforming Growth Factor Market Trends and Insights

North America holds the leading regional position in the Transforming Growth Factor market, with an estimated 39% share in 2025, underpinned by its concentration of biopharmaceutical R&D, advanced academic centers, and strong funding ecosystems. The United States dominates regional activity, supported by substantial NIH and other federal funding streams that channel several tens of billions of US dollars annually into health research, including cancer, fibrosis, and immunology programs where TGF signaling is central. Prestigious institutions such as Harvard Medical School, Stanford University, Johns Hopkins University, and MIT host leading TGF-focused laboratories that both consume high-value reagents and generate foundational knowledge translated into industrial pipelines.

The FDA plays a key role by setting regulatory frameworks for TGF-targeting biologics, gene therapies, and advanced combination regimens, and has increasingly made use of programs such as Fast Track, Breakthrough Therapy, and Priority Review to accelerate promising candidates in oncology and rare diseases. North America also benefits from a dense cluster of major suppliers and CDMOs that provide growth factors, media, and custom proteins, many based in biotech hubs such as Boston–Cambridge and the San Francisco Bay Area. This integrated innovation ecosystem, spanning discovery through commercial manufacturing, reinforces North America’s status as the largest and most influential market for TGF-related technologies.

Asia Pacific Transforming Growth Factor Market Trends and Insights

Asia Pacific is the fastest-growing region in the Transforming Growth Factor market, with a forecast CAGR above the global average through the 2026–2033 period. China has rapidly expanded its biopharmaceutical and life sciences footprint, supported by large-scale investments in research parks, high-end manufacturing facilities, and national-level grants for precision medicine and advanced therapies. Chinese institutions and companies are active in recombinant protein production, biosimilars, and innovative biologics, and are increasingly integrating TGF-family reagents into regenerative medicine and oncology pipelines.?

Japan maintains a strong base in innovative drug development and cell therapy, with major firms and academic hospitals conducting TGF-oriented research in oncology and fibrosis. India and several ASEAN countries, including Singapore and South Korea, are emerging as key hubs for contract manufacturing and R&D services, leveraging cost advantages and skilled scientific talent. Many global suppliers partner with local manufacturers or distributors in Asia Pacific to expand access to TGF proteins, BMPs, and assay kits, while regional companies are building their own brands in recombinant growth factors. This combination of domestic demand growth, manufacturing scale-up, and integration into global value chains positions Asia Pacific as the most dynamic market for future TGF-sector expansion.

Competitive Landscape

Market Structure Analysis

The Transforming Growth Factor market is moderately consolidated at the top, with a handful of large life science and bioprocess suppliers holding significant global share, complemented by a long tail of specialized biotech companies. Players such as Thermo Fisher Scientific, Merck KGaA, Lonza, and Bio-Techne offer extensive portfolios of recombinant growth factors, cytokines, antibodies, and assay kits, together with distribution networks that reach pharma, biotech, and academic customers worldwide. Differentiation is driven by product quality, lot-to-lot consistency, regulatory support (including documentation for GMP and clinical use), and technical service, as well as integration with adjacent offerings like media, instruments, and cell therapy services. At the same time, smaller and mid-size biotechs developing TGF-targeting therapeutics contribute to innovation at the clinical frontier, while relying heavily on outsourced manufacturing and CDMO partnerships for scale-up.

Key Market Developments

- In April 2024, Shanghai Henlius Biotech, Inc. announced that the first subject had been dosed in a phase 1 clinical trial of HLX6018 (NCT06310746), a novel anti-GARP/TGF-β1 monoclonal antibody (mAb) independently developed by the company. HLX6018 became Henlius’ first innovative product in the treatment of chronic inflammatory diseases and had recently been approved by the National Medical Products Administration (NMPA) for the treatment of idiopathic pulmonary fibrosis (IPF).

Companies Covered in Transforming Growth Factor Market

- Thermo Fisher Scientific

- Merck KGaA

- Lonza Group

- Bio-Techne

- Abcam

- PeproTech

- Cell Signaling Technology

- Sartorius CellGenix

- Proteintech Group

- Sino Biological

- Akron Biotech

- Applied Biological Materials (abm)

- Medtronic

- Stryker

Frequently Asked Questions

The Transforming Growth Factor market is projected to reach about US$ 382.3 million in 2026, reflecting steady demand growth from oncology, fibrosis, and regenerative medicine research and the expanding use of TGF-pathway tools and therapeutics across leading biopharmaceutical markets.

Demand is primarily driven by rising global incidence of cancer, fibrotic diseases, and autoimmune conditions linked to dysregulated TGF signaling, as well as rapid growth of cell and gene therapies and regenerative medicine approaches that rely on TGF-family growth factors for controlled cell differentiation and immune modulation.

North America currently leads the global Transforming Growth Factor market with an estimated 39% share in 2025, supported by strong research funding, concentration of major biopharma companies, and an innovation-friendly regulatory environment that accelerates development and adoption of TGF-targeting therapies.

A major opportunity lies in developing and commercializing TGF-beta inhibitors in combination with immune checkpoint inhibitors to overcome resistance in solid tumors, a strategy backed by multiple ongoing clinical trials and recent Fast Track regulatory designations that could unlock multi-billion–dollar oncology revenues over the long term.

Key players include large life science suppliers and biopharma companies such as Thermo Fisher Scientific, Merck KGaA, Lonza, Bio-Techne, Abcam, PeproTech, Cell Signaling Technology, and Sartorius CellGenix, as well as emerging therapeutic developers like EpicentRx and Keros Therapeutics that are advancing innovative TGF-pathway–targeted drugs.