- Medical Devices

- Transseptal Access Systems Market

Transseptal Access Systems Market Size, Share, and Growth Forecast 2026 - 2033

Transseptal Access Systems Market by Product (Transseptal Access Needle, Transseptal Access Sheath), by Application (Atrial Fibrillation Ablation, Mitral Valve Repair, Left Atrial Appendage Occlusion), by End User, by Regional Analysis, 2026-2033

Transseptal Access Systems Market Size and Trend Analysis

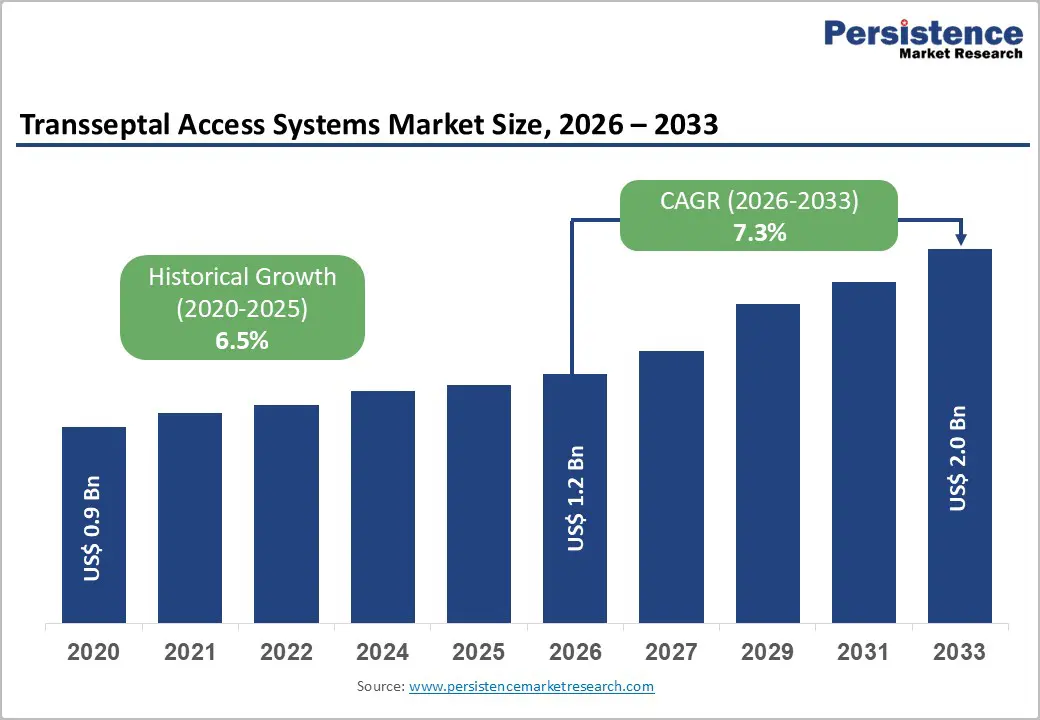

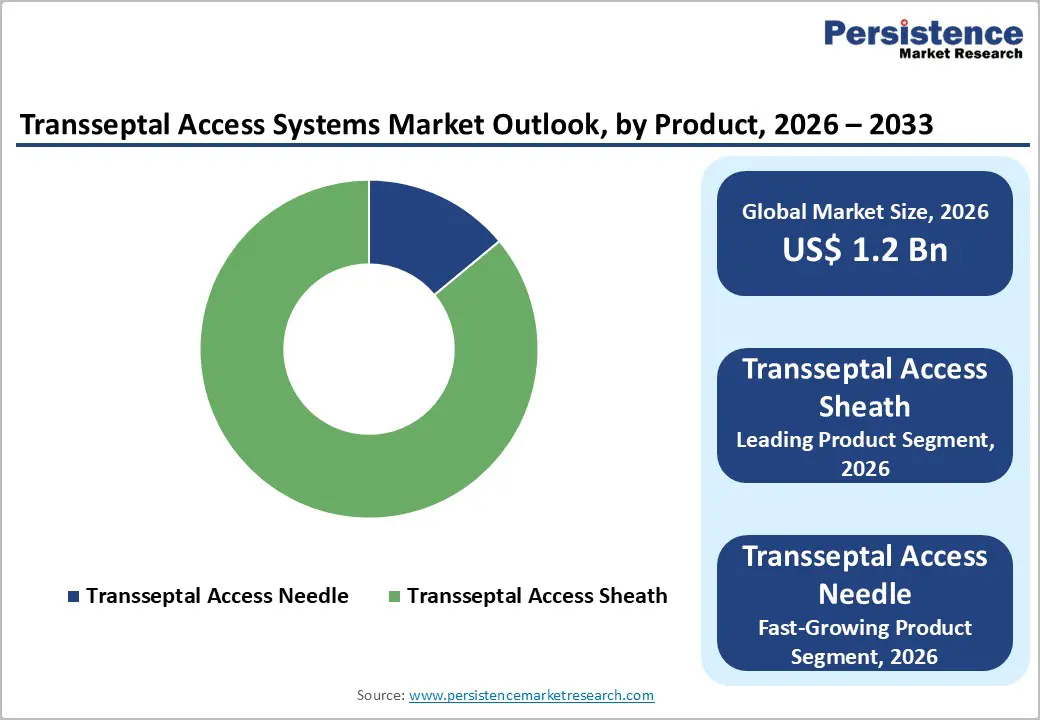

The global transseptal access systems market size is expected to be valued at US$ 1.2 billion in 2026 and projected to reach US$ 2.0 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

The transseptal access systems market is gaining momentum as left atrial catheterization becomes increasingly common for arrhythmia ablation and structural heart procedures. Rising global cardiac disease burden, driven by aging populations, hypertension prevalence, alcohol consumption, tobacco use, and sedentary lifestyles, accelerate demand. Increasing atrial fibrillation incidence in both developed and emerging economies has boosted adoption of therapies such as atrial fibrillation ablation, mitral valve interventions, and left atrial appendage occlusion procedures. These minimally invasive approaches rely heavily on precise and safe transseptal puncture systems, positioning them as essential tools in modern electrophysiology and interventional cardiology practices worldwide.

Market growth is further supported by improving healthcare infrastructure across emerging nations and expanding access to advanced cardiac care. Continuous technological innovation such as integrated imaging guidance, safer needle designs, and next-generation left atrial appendage occlusion therapies are enhancing procedural success and physician confidence. The introduction of cutting-edge devices is enabling broader patient eligibility and outpatient treatment models, supporting steady global expansion of the transseptal access systems market over the forecast period.

Key Market Highlights

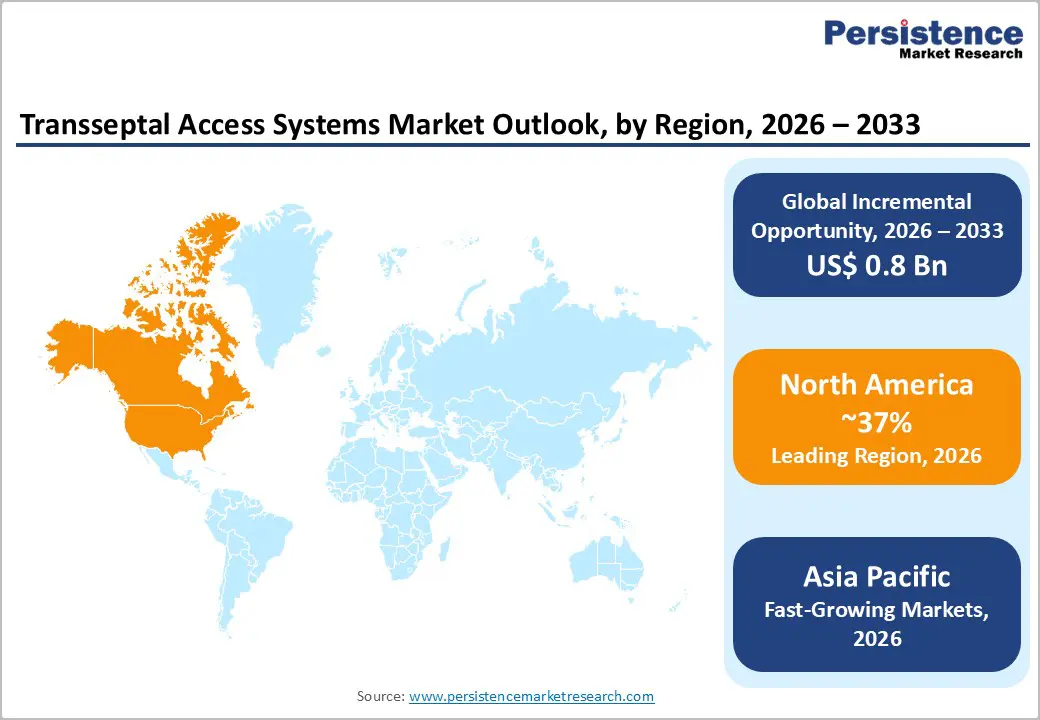

- North America dominates the transseptal access systems market, supported by high atrial fibrillation procedure volumes, advanced cardiac catheterization labs, favorable reimbursement policies, and rapid adoption of minimally invasive cardiology technologies.

- Asia Pacific is the fastest-growing region, driven by expanding healthcare infrastructure, rising cardiovascular disease prevalence, government hospital investments, and increasing local device manufacturing partnerships.

- Transseptal access sheaths hold the largest product share, owing to their essential role in left atrial catheter delivery, growing use in atrial fibrillation ablation, and rising adoption of steerable and integrated designs.

- Hospitals remain the leading end users, while ambulatory surgical centers are the fastest-growing, supported by payer shifts toward outpatient electrophysiology procedures and demand for lower-cost, same-day cardiac interventions.

| Global Market Attributes | Key Insights |

|---|---|

| Transseptal Access Systems Market Size (2026E) | US$ 1.2 billion |

| Market Value Forecast (2033F) | US$ 2.0 billion |

| Projected Growth CAGR (2026-2033) | 7.3% |

| Historical Market Growth (2020-2025) | 6.5% |

Market Dynamics

Driver: Increasing Risk Factors like Hypertension and Growing Product Penetration

Transseptal access systems' increasing technological development and rising levels of public awareness are anticipated to increase demand. Transseptal puncture methods have advanced due to the introduction of transesophageal and fluoroscopic echocardiographic pictures.

Similarly, it is anticipated that improvements in mechanical technology and the introduction of new products with improved features would drive an increase in demand for transseptal access systems. For instance, the introduction AVANCE Bi-directional steerable introducer sheaths by Abbott, which have even bendable properties in all directions, makes it easier to enter the left atrium during transseptal accessibility, improving procedure efficiency.

Leading producers of transseptal access systems are collaborating to increase product penetration in developing regions. Numerous causes, including an ageing general population and inadequate management of risk factors like hypertension, are driving up the patient population. In addition to health problems, other risk factors for atrial fibrillation include the consumption of alcohol, tobacco, and other drugs, as well as a changing culture that promotes an active lifestyle.

It is anticipated that in the projected years, the government and commercial healthcare insurance providers would support the expansion of the global market, who have made it easier to receive reimbursement for the treatment and diagnosis of diseases. Consumers' changing lifestyles because of their hectic lifestyles have led to high-risk conditions that might cause atrial fibrillation, which is projected to increase in prevalence globally and accelerate market growth in the upcoming years.

Restraint: Shortage of Skilled Professionals and Lack of Availability of Enhanced Services

Global demand for transseptal access systems increased as atrial fibrillation cases increased. However, there is a lack of qualified and skilled professions for these procedures in several middle to low-income nations, thus restraining the overall market growth. Transseptal access system usage is decreased because of other obstacles, such as supply chain problems, ineffective healthcare service management, a lack of technologically advanced equipment, etc., which restrains the market growth. Despite advancements in healthcare facilities and regional and international support, the great majority of people still have limited access to treatment options. Factors include a shortage of qualified workers, substandard service providers, a lack of knowledge of disease symptoms, poverty, problems with the supply chain, ineffective management of healthcare services, a lack of technologically advanced equipment, etc.

These factors limit the trend in product consumption despite the high demand, which restrains the market expansion of transseptal access systems.

Opportunity: Ambulatory Surgical Centers Shift

The rapid shift of electrophysiology and structural heart procedures toward ambulatory surgical centers (ASCs) presents a major growth opportunity for the transseptal access systems market. Rising healthcare cost pressures, payer preference for same-day discharge models, and patient demand for faster recovery are encouraging hospitals to decentralize selected catheter-based interventions into outpatient settings. Improvements in imaging guidance, catheter maneuverability, and safety-engineered transseptal needles are increasing procedural confidence outside traditional tertiary hospitals, enabling ASCs to adopt complex left-atrial access techniques for atrial fibrillation ablation and left atrial appendage occlusion procedures.

Manufacturers can capitalize by developing compact, easy-to-use transseptal platforms optimized for outpatient workflows, including integrated sheaths, pressure-sensing needles, and reduced fluoroscopy systems. Training programs bundled device offerings, and partnerships with fast-growing ASC networks further strengthen market entry. As outpatient cardiac care expands globally particularly in North America and Asia Pacific ASCs are poised to become a key volume driver for transseptal access system adoption over the next decade.

Category-wise Insights

Product Analysis

Transseptal access sheaths dominate the global transseptal access systems market, accounting for an estimated 86% share in 2025 due to their indispensable role in providing stable left atrial (LA) access following septal puncture. These devices are essential in atrial fibrillation ablation, which represents nearly 65% of total procedural volumes, as they enable precise catheter navigation, torque control, and sustained positioning within the left atrium. Historically, transseptal sheaths have retained leadership because of their compatibility with multiple catheter platforms and expanding availability of steerable and deflectable variants. Integrated sheath–dilator designs and pressure-monitoring capabilities are further reducing device exchanges, procedural time, and complication risks, making them especially valuable in complex electrophysiology and structural heart interventions. Continuous innovation including thinner-wall materials, enhanced radiopacity, and reduced-profile designs is strengthening physician preference. As procedural volumes grow globally and outpatient settings expand, manufacturers focusing on ergonomic handling, imaging compatibility, and safety-enhanced sheath platforms are expected to sustain category dominance through the forecast period.

End User Analysis

Hospitals remain the leading end users in the transseptal access systems market in 2025, supported by their advanced catheterization laboratories, electrophysiology suites, and ability to manage high-volume atrial fibrillation ablations and complex structural heart procedures. Large tertiary-care centers dominate adoption due to access to hybrid operating rooms, intracardiac echocardiography systems, and multidisciplinary cardiac teams that collectively enable procedural success rates approaching 98.5% in experienced facilities. Hospitals also benefit from reimbursement coverage for advanced electrophysiology procedures, robust post-procedure monitoring infrastructure, and established referral networks that funnel complex cases requiring transseptal access. Teaching hospitals and cardiac institutes further drive demand through physician training programs and early adoption of next-generation access technologies. While ambulatory surgical centers are gaining momentum for selected low-risk procedures, hospitals continue to account for the majority of cases because of their ability to handle complications, perform high-risk interventions, and conduct clinical research supporting new device approvals.

Regional Insights

North America Transseptal Access Systems Market Trends and Insights

North America led by the U.S. is projected to remain a dominant regional market, with the U.S. expected to capture around 37% of global revenue in 2026 and maintain strong growth during the forecast period. Expanding healthcare infrastructure, broad access to advanced diagnostic and interventional cardiology services, and supportive reimbursement policies are sustaining procedural volumes. Aging demographics are a key catalyst, as the proportion of individuals aged 60 years and above continues to rise globally, increasing the burden of atrial fibrillation and structural heart disease. In the U.S., atrial fibrillation remains the most frequently diagnosed arrhythmia, affecting millions of adults and projected to exceed twelve million cases by 2030, reinforcing long-term demand for left-atrial access devices. Hospitals’ early adoption of catheter-based therapies, coupled with strong regulatory frameworks and payer coverage for electrophysiology procedures, further strengthens North America’s leadership in transseptal access system utilization.

Europe Transseptal Access Systems Market Trends and Insights

Europe represents a mature yet steadily expanding market for transseptal access systems, driven by rising atrial fibrillation prevalence and increasing volumes of left atrial appendage occlusion, catheter ablation, and mitral valve interventions. Transseptal puncture remains a widely accepted technique for percutaneous left atrial access across European cardiac centers, supporting consistent device demand. Germany plays a pivotal role through its Diagnosis-Related Group reimbursement structure, where codes such as F50A, F50B, and F50C are frequently associated with cardiac ablation procedures. Ongoing policy refinements that adjust relative weights into hospital payments continue to influence adoption patterns and procedural economics. Favorable reimbursement environments in major markets, combined with well-established electrophysiology networks and academic hospitals, are encouraging continued investment in advanced transseptal technologies. Growth is further supported by pan-European initiatives to expand minimally invasive cardiac care and improve access to innovative structural heart interventions.

Asia Pacific Transseptal Access Systems Market Trends and Insights

Asia Pacific is emerging as the fastest-growing regional market for transseptal access systems, with China leading East Asia and forecast to expand at approximately 10.1% CAGR during the outlook period. Rapid modernization of healthcare infrastructure, rising cardiovascular disease prevalence, and government-backed hospital expansion programs are increasing access to advanced electrophysiology and structural heart procedures. China’s momentum is reinforced by domestic innovation and international partnerships, exemplified by Peijia Medical’s successful first-in-human case using the Highlife TSMVR system for transcatheter mitral valve replacement and its licensing agreement with France-based HighLife SAS to develop and commercialize TMVR products across Greater China. Such collaborations accelerate technology transfer and local manufacturing, reducing dependence on imports while broadening clinical adoption. Similar trends across India, South Korea, and Southeast Asia along with improving reimbursement pathways are expected to sustain Asia Pacific’s rapid uptake of transseptal access systems over the coming decade.

Competitive Landscape

Market Structure Analysis

The transseptal access systems market is moderately consolidated, with a few multinational medical device companies holding significant shares alongside emerging regional manufacturers. Leading players compete through broad electrophysiology portfolios, physician training programs, and long-term hospital contracts. Continuous product innovation such as steerable sheaths, pressure-sensing needles, and imaging-integrated platforms remains the primary differentiator. Strategic collaborations with catheter manufacturers, acquisitions of niche technology firms, and geographic expansion in Asia Pacific are shaping competitive dynamics. Barriers to entry include stringent regulatory requirements, clinical validation needs, and strong brand loyalty among interventional cardiologists.

Key Market Developments

- In February 2022, Boston Scientific Corporation completed the acquisition of Baylis Medical Company Inc., expanding its portfolio of advanced transseptal access solutions, including guidewires, sheaths, and dilators for catheter-based left-heart procedures.

- In January 2019, Abbott exercised its option to acquire the privately held company Cephea Valve Technologies, Inc., which develops minimally invasive mitral valve replacement technologies for patients with mitral valve disease.

Companies Covered in Transseptal Access Systems Market

- Boston Scientific Corporation

- Medtronic plc

- Biosense Webster, Inc. (Johnson & Johnson)

- Terumo Corporation

- St. Jude Medical LLC (Abbott Laboratories)

- Merit Medical Systems, Inc.

- Baylis Medical Company, Inc.

- Pressure Product Medical Device Manufacturing LLC

- Cook Medical LLC

- Transseptal Solutions, Inc.

- Abbott Laboratories

Frequently Asked Questions

The global transseptal access systems market is valued at US$ 1.2 billion in 2026.

Rising atrial fibrillation prevalence, growing catheter ablation procedures, structural heart interventions, aging populations, minimally invasive cardiology adoption worldwide.

North America leads with 37% share in 2025.

Developing safer needle designs, integrated imaging guidance, emerging market expansion, outpatient electrophysiology growth, partnerships with cardiac centers globally.

Leaders include Boston Scientific Corporation, Medtronic plc, Biosense Webster, Inc. (Johnson & Johnson), Terumo Corporation, and St. Jude Medical LLC (Abbott Laboratories).