- Automotive Components & Materials

- Torsional Vibration Dampers (TVD) Market

Torsional Vibration Dampers (TVD) Market Size, Share, and Growth Forecast, 2026-2033

Torsional Vibration Dampers (TVD) Market by Product Type (Elastomer Dampers, Viscous Dampers, Pendulum Dampers, Dual Mass Flywheels, Composite Material Dampers), Mechanical Configuration (Internal Combustion Engine, Turbocharged Engines, Hybrid Powertrains, Electric Vehicle (EV) Drivetrains, Others), End-Use Industry (Automotive, Industrial Machinery & Equipment, Power Generation Equipment, Marine Engines, Aerospace Systems, Others) and Regional Forecast for 2026-2033

Torsional Vibration Dampers (TVD) Market Share and Trends Analysis

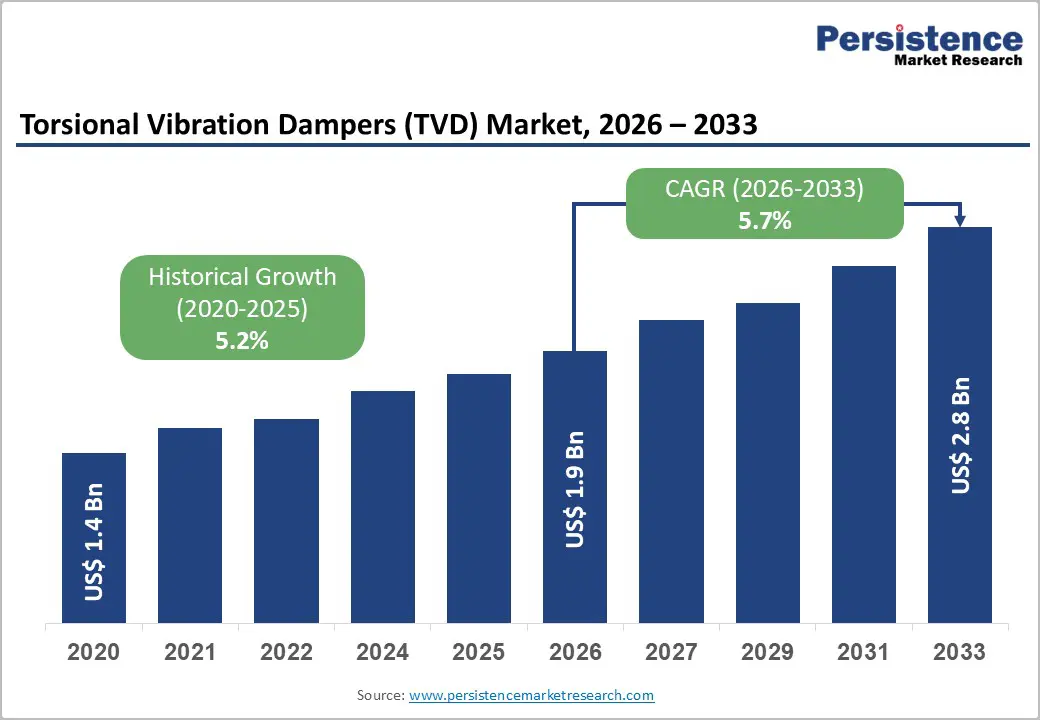

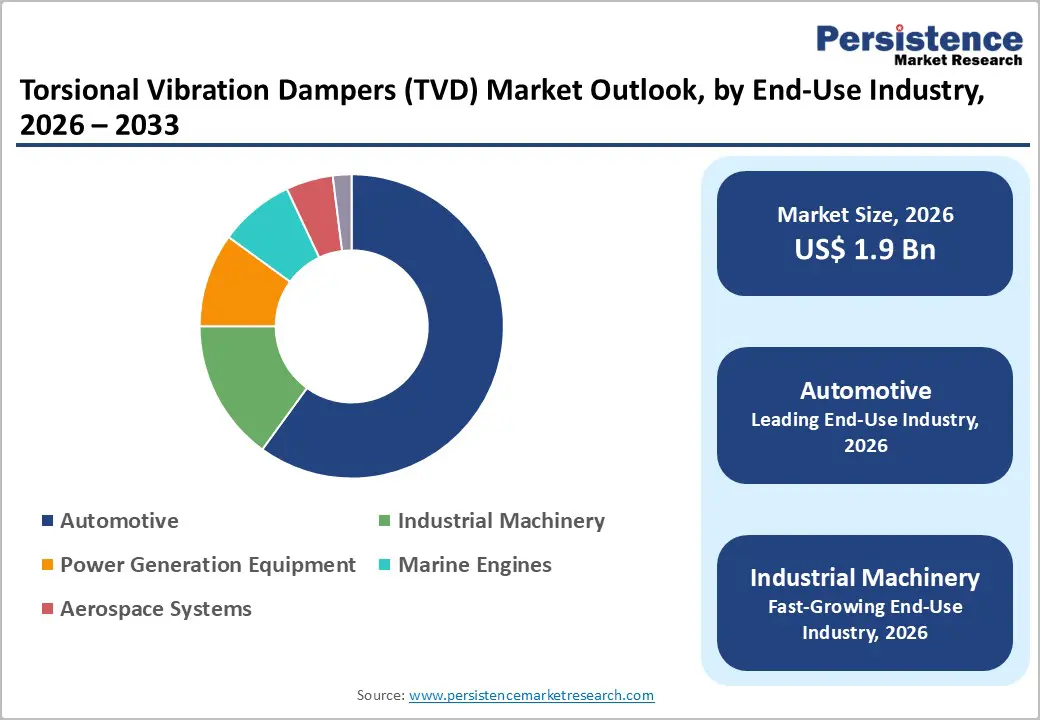

The global torsional vibration dampers (TVD) market is likely to be valued at US$ 1.9 billion in 2026, and is projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 5.7% during the forecast period 2026-2033.

Tightening global emission regulations that are requiring higher engine efficiency and smoother power transmission are supporting market expansion. Engine downsizing and turbocharging trends are increasing torsional stress within drivetrains, which is strengthening the need for effective vibration control solutions across passenger vehicles, commercial vehicles, and industrial equipment. Fueling market momentum investments by original equipment manufacturers (OEMs) in noise, vibration, & harshness (NVH) reduction technologies, particularly within hybrid powertrains and high torque engine architectures. As powertrain complexity is increasing, torsional vibration dampers are playing a critical role in protecting crankshafts, improving component longevity, and maintaining ride quality. Despite the gradual shift toward electrified propulsion systems, mechanical vibration control remains structurally essential across internal combustion, hybrid, and transitional powertrain platforms.

Key Industry Highlights

- Dominant End-Use Industry: Automotive is projected to lead with 60% market share in 2026, driven by regulatory-mandated integration of torsional vibration dampers across internal combustion engine (ICE) and hybrid vehicles.

- Leading Product Type: Elastomer dampers are expected to dominate with 38% share in 2026, while dual mass flywheels are likely to be the fastest-growing at 6.8% CAGR due to rising NVH requirements.

- Mechanical Configuration Dominance: ICE platforms are anticipated to account for 55% of demand in 2026, whereas hybrid powertrains are projected to grow the fastest at 7.5% CAGR through 2033.

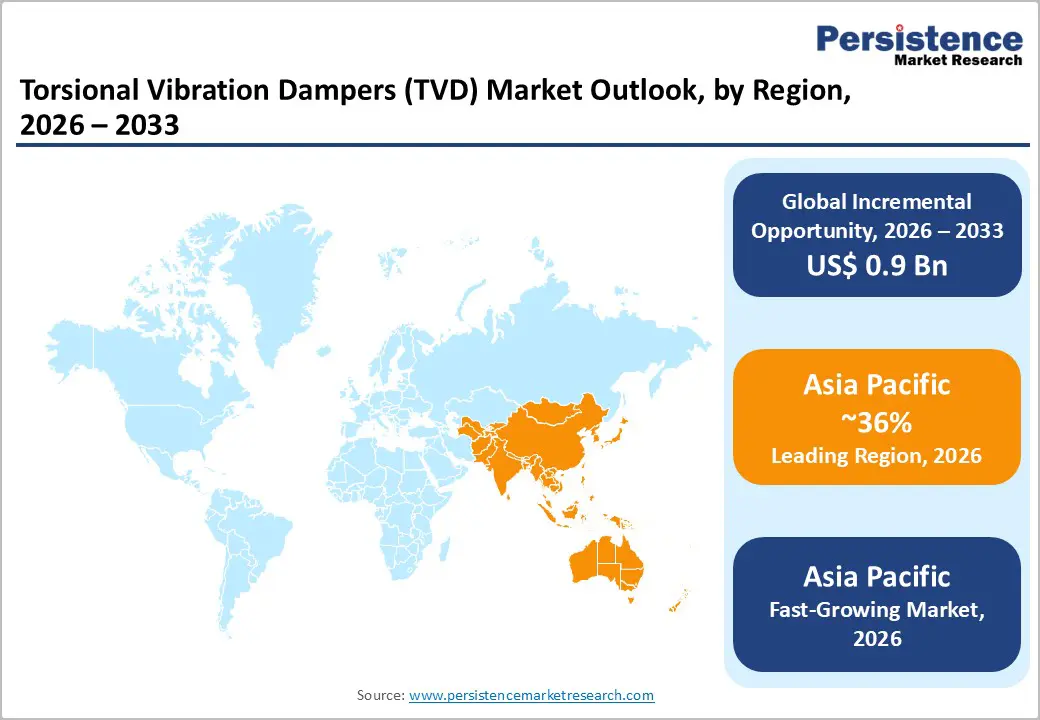

- Regional Leadership: Asia Pacific is set to hold 36% share in 2026 and register the highest growth at 7.0% CAGR, led by automotive engineering advancements in China, Japan, and India.

- Technology & Regulation Impact: Tightening emission norms and increasing focus on NVH optimization continue to sustain damper demand despite gradual EV penetration.

- Competitive & Investment Trends: Investments are being directed toward lightweight materials, advanced elastomers, and hybrid-optimized damping technologies to enhance efficiency and durability.

| Key Insights | Details |

|---|---|

| Torsional Vibration Dampers (TVD) Market Size (2026E) | US$ 1.9 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulatory-Driven Powertrain Evolution and Rising Torsional Stress

Stringent emission regulations enforced by agencies such as the U.S. Environmental Protection Agency (EPA), the European Commission (Euro 6/7), and China’s Ministry of Industry and Information Technology (MIIT) have compelled OEMs to redesign engines for higher efficiency and lower displacement. According to data from the European Automobile Manufacturers Association (ACEA) and the International Energy Agency (IEA), downsized and turbocharged engines generate higher torsional stress levels, increasing reliance on torsional vibration dampers to protect crankshafts and drivetrains. These regulations directly elevate damper integration rates per vehicle, particularly in gasoline direct injection (GDI) and diesel platforms, where combustion-induced vibration levels are structurally higher. As a result, dampers have evolved into mandatory drivetrain protection components across regulated automotive markets.

The rapid shift toward turbocharged and high-torque powertrains has further intensified torsional vibration challenges. SAE International highlights that turbocharging increases crankshaft torsional excitation by over 30% compared to naturally aspirated engines, significantly raising fatigue risks across rotating components. Similar stress patterns are observed in high-load industrial, marine, and construction engines operating under variable torque conditions. These dynamics have accelerated adoption of elastomer dampers, viscous dampers, and dual mass flywheel systems, expanding damper demand beyond passenger vehicles and reinforcing the torsional vibration dampers market across both mobility and industrial applications.

Electrification Impact and Cost Pressures on TVD Adoption

The accelerating shift toward pure electric drivetrains is reshaping powertrain architectures and reducing reliance on traditional mechanical components. Several major automotive OEMs have publicly committed to clear electrification timelines. For example, Volkswagen Group has announced plans to end internal combustion engine vehicle sales in Europe by 2035, aligning with regional regulatory targets. According to IEA transport outlooks, EV penetration continues to rise in Europe and China, structurally capping long-term demand for torsional vibration dampers in small and mid-size passenger vehicle segments. As battery electric vehicles eliminate crankshafts, the need for conventional TVDs is inherently reduced in these platforms.

Cost pressures and material price volatility continue to constrain damper adoption. Recent volatility in petrochemical markets has raised costs for engineered elastomers and silicone-based fluids, while supply disruptions in specialty materials have affected advanced composite components. These challenges are compounded by sustained OEM price-reduction programs, particularly in high-volume automotive contracts. As a result, damper manufacturers face margin compression and slower technology deployment, especially in cost-sensitive markets where balancing performance improvements with affordability remains critical.

Hybrid Powertrain Expansion, Industrial Modernization, and Advanced Damper Innovation

The opportunity is reinforced by specific OEM actions and infrastructure developments. For instance, Toyota Motor Corporation has continued to expand its hybrid powertrain portfolio across multiple vehicle segments, positioning hybrid technology as a core long-term strategy rather than a transitional offering. These hybrid systems rely on frequent engine start-stop operation and torque blending between electric motors and internal combustion engines, significantly increasing transient torsional loads. As a result, OEMs specify higher-performance torsional vibration dampers to protect crankshafts and driveline components, raising value per unit relative to conventional ICE platforms.

The government-led grid resilience and infrastructure programs are driving modernization of power generation equipment, including gensets and rotating machinery that operate under variable load conditions. These profiles intensify torsional stress, accelerating adoption of viscous and pendulum dampers, particularly in regions with expanding power capacity. At the technology level, OEM initiatives focused on lightweighting and digital monitoring have increased demand for composite dampers and condition-integrated solutions, aligning with Industry 4.0 objectives. These developments substantiate the growth opportunity for suppliers offering advanced torsional vibration dampers across automotive, industrial, and marine applications.

Category-wise Analysis

Product Type Insights

Elastomer dampers are expected to be the leading product type, holding an estimated 38% of the TVD market share in 2026 due to cost efficiency, broad OEM acceptance, and reliable performance in passenger vehicles and light commercial platforms. They are widely specified to manage torsional oscillations and improve NVH metrics without excessive complexity. Their compatibility with gasoline, diesel, and hybrid powertrains reinforces their role as the default damping solution across many OEM programs. Continued ICE production and hybrid adoption in high-volume regions sustain elastomer demand, while refinements such as higher temperature-rated elastomers support usage in turbocharged and hybrid engines. For example, at IAA Mobility 2025, Valeo showcased an expanded range of electrified powertrain solutions, including 48V systems and hybrid-compatible components designed to improve efficiency and integration across multiple vehicle platforms, reinforcing the ecosystem in which elastomer dampers operate.

Dual mass flywheels are anticipated to be the fastest-growing product segment, projected to expand at 6.8% CAGR from 2026 to 2033, driven by superior torque isolation and NVH control in turbocharged and hybrid vehicles. Their ability to absorb torsional energy and smooth drivetrain transitions makes them attractive for premium and performance applications in European and Asian passenger car markets. Technological advancements and lightweight material integration enhance performance and fuel efficiency. Suppliers focusing on this segment are well positioned to benefit from increasingly complex powertrains and higher consumer expectations for refined ride quality, while ongoing industry innovation in hybrid-compatible systems further supports dual mass flywheel adoption.

Mechanical Configuration

Internal combustion engines, including gasoline and diesel platforms, are likely to remain the dominant mechanical configuration, representing 55% of the torsional vibration dampers market share in 2026. They rely on torsional vibration dampers to manage combustion-induced torsional loads and maintain NVH standards, particularly in high-compression diesel engines. ICE dominance is supported by strong production volumes in Asia Pacific and North America, as well as ongoing industrial applications in generators, construction, and agricultural machinery. Regulatory fuel-efficiency mandates continue to shape damper specifications, ensuring durability and performance are maintained across diverse vehicle and industrial platforms.

Hybrid powertrains projected to be the fastest-growing configuration, projected to expand at 7.5% CAGR from 2026 to 2033, as start-stop cycles and torque blending introduce complex torsional loads. These dynamics require tailored damping solutions to improve drivetrain smoothness and protect components. OEMs are increasingly integrating advanced dampers to meet NVH and durability standards. For example, at VIBES experience 2025, BMW, Volvo, Hyundai, and Stellantis highlighted hybrid modular damping solutions aimed at optimizing torsional control in electrified drivetrains, demonstrating active collaboration between OEMs and suppliers.

End-Use Industry

The automotive sector is expected to lead the torsional vibration dampers market revenue share at an estimated 60% in 2026, driven by high production volumes and regulatory-driven component integration across passenger vehicles, commercial vehicles, and off-highway platforms. OEMs prioritize NVH optimization, powertrain durability, and reliability, making dampers essential across gasoline, diesel, and hybrid engines. The segment benefits from global supply chains, standardized specifications, and compliance with regional fuel economy and emissions mandates, providing suppliers with stable contracts and opportunities to innovate. For example, Stellantis expanded its hybrid powertrain strategy in Europe, planning more than 30 hybrid model launches through 2026, reinforcing integration of advanced drivetrain components that include damping solutions.

Industrial machinery are projected to be the fastest-growing end-use segment, projected to expand at 6.5% CAGR through 2033, driven by infrastructure modernization and variable load operation requirements. Heavy-duty engines, gensets, and rotating equipment experience high torsional loads under fluctuating conditions, driving demand for viscous and pendulum dampers optimized for durability and performance. Emerging markets in Asia Pacific are boosting demand through large industrial infrastructure projects, such as India’s Chennai-Bangalore Industrial Corridor, which is expected to enhance regional manufacturing, logistics, and power infrastructure capacity. This expansion stimulates greater industrial machinery deployment and associated damping needs. Meanwhile, the Middle East continues infrastructure investment in energy and industrial works, further supporting industrial segment growth and equipment utilization.

Regional Insights

North America Torsional Vibration Dampers (TVD) Market Trends

North America holds a strong position in the torsional vibration dampers market, supported by an increased adoption of advanced damping systems in passenger and commercial vehicles. The United States contributes a significant share due to its large vehicle ownership, advanced industrial base, and strict EPA emission and fuel-efficiency standards that elevate vibration control requirements, supported by increased adoption of advanced damping systems in passenger and commercial vehicles. OEMs emphasize durability, NVH optimization, and compliance with fuel-efficiency mandates. Regulatory focus indirectly strengthens demand for robust damper integration across ICE and hybrid platforms. The industrial sector also drives adoption through heavy-duty engines and power generation equipment. Technological innovation encourages localized manufacturing and aftermarket expansion.

American Axle & Manufacturing (AAM) acquiring the Dowlais Group plc, expanding its driveline capabilities across ICE, hybrid, and EV platforms is a prime example illustrating this trend in the region. This strategic move reinforces advanced damping and torque management technologies, allowing North American OEMs to meet stringent performance and durability requirements. Industrial engines and power generation applications further support steady market demand. Investments in material innovation and lightweighting enhance product performance. The region’s mature supply chains maintain consistent component availability. NVH standards and durability expectations remain central to adoption.

Europe Torsional Vibration Dampers (TVD) Market Trends

Europe is a technology-driven and regulation-intensive market for torsional vibration dampers, with Germany, the U.K., France, and Spain serving as primary demand centers. Regional market growth is driven by strict emission standards such as Euro-7, which influence damper specifications for turbocharged and hybrid powertrains. European OEMs prioritize dual mass flywheels and high-performance elastomer dampers for NVH refinement. The supplier base is consolidated and technologically advanced, emphasizing lightweighting and sustainability. Compliance with regional regulations drives integration across ICE and hybrid platforms. High vehicle sophistication supports advanced damping adoption. Innovation in materials and design strengthens competitive positioning.

Europe’s regulatory framework continues to shape market demand. The European Commission’s 2025 “Automotive Package” promotes low-emission vehicles and strengthens battery supply chains, encouraging OEM adoption of hybrid powertrains. Advanced damping systems are increasingly integrated to maintain NVH and drivetrain durability. Turbocharged engine proliferation and electrification trends support high-spec damper deployment. Lightweight and composite solutions are emphasized for sustainability. Supplier collaborations focus on performance and emission compliance. These policies reinforce Europe’s leadership in torsional vibration damper technologies.

Asia Pacific Torsional Vibration Dampers (TVD) Market Trends

Asia Pacific is expected to be the leading and fastest-growing regional market for torsional vibration dampers with a 36% share in 2026. The regional market is projected to grow at a CAGR of nearly 7% through 2033, driven by high automotive production in China, Japan, India, and ASEAN countries. China leads hybrid adoption, while India’s industrial engine demand supports steady growth across heavy-duty and power generation applications. The region benefits from manufacturing cost advantages, expansive OEM programs, and supportive government policies promoting local production and technology deployment. Adoption spans ICE, hybrid, and industrial platforms, strengthening demand for torsional vibration dampers across segments. High-volume OEM powertrain programs and infrastructure investment underpin growth. Broad industrial integration incentivizes supplier capacity expansion. Asia Pacific’s combined automotive and industrial demand positions it as the global growth leader.

Regional infrastructure developments further accelerate damper adoption. In 2025, Singapore’s Jurong Innovation District completed Bulim Square, adding over 110,000 m² of industrial space for advanced manufacturing and technology firms, supporting equipment deployment and industrial machinery growth. Expansion attracts robotics, electronics, and precision machinery companies, enhancing demand for vibration mitigation solutions. Complementary renewable energy capacity across the region supports rotating equipment deployment. Local policies encourage hybrid and high-efficiency vehicle programs, sustaining automotive demand. Suppliers are investing in facilities and advanced damper solutions. These initiatives collectively reinforce Asia Pacific’s industrial and automotive market growth.

Competitive Landscape

The global torsional vibration dampers market structure is moderately consolidated, with leading players such as Schaeffler, ZF Friedrichshafen, Continental, Vibracoustic, and Valeo collectively accounting for over half of total revenue. These companies leverage extensive OEM relationships, advanced engineering expertise, and integrated powertrain component portfolios to maintain leadership. They continue to invest heavily in R&D, focusing on high-performance elastomer solutions, dual mass flywheels, and lightweight composite dampers for hybrid and electrified powertrains. Continuous innovation in NVH optimization, durability, and temperature-resistant materials strengthens their technological edge.

Regional and niche players, including AAM, NTN Corporation, and LuK, target specialized industrial, marine, and regional automotive segments, often providing tailored damping solutions for specific torque and load profiles. Barriers such as high engineering complexity, material costs, and stringent OEM specifications limit new entrants. However, growing hybrid and industrial powertrain adoption creates opportunities for partnerships and joint development. Market consolidation is expected to continue gradually, with major players expanding via acquisitions, strategic alliances, and investments in advanced damper technologies, while smaller and regional suppliers collaborate to access global OEM programs.

Key Industry Developments

- In December 2025, Changan’s powertrain division, Harbin Dongan Auto Engine, successfully started the first run of its new 1.5-liter ICE that meets both China VII and Euro VII emission standards, developed for plug-in hybrid applications. The engine, designated M15NTH, uses advanced technologies such as the Miller cycle, cooled exhaust gas recirculation (EGR), variable valve timing (VVT), and built-in TVDs to achieve the tighter emissions targets.

- In June 2025, Baker Hughes launched GuardVibe, a new technology platform for mitigating drill-string vibration during drilling operations by combining real-time data analytics with adaptive control strategies to improve drilling efficiency and reduce mechanical wear. The system is designed to continuously monitor downhole vibration patterns and automatically adjust drilling parameters to optimize performance, enhancing bit life and operational uptime for oil and gas drilling programs.

- In June 2025, Hodek Vibration Technologies opened its third manufacturing facility in Karnataka, reflecting a deliberate expansion of production capacity and operational readiness aligned with Industry 4.0 automation standards. The new plant is designed as a lean, environmentally conscious hub for producing torsional vibration dampers for internal combustion engines, while also strengthening the company’s ability to meet growing demand from key OEMs across the automotive and industrial sectors.

Companies Covered in Torsional Vibration Dampers (TVD) Market

- Schaeffler Group

- Continental AG

- Vibracoustic

- Trelleborg AB

- BorgWarner Inc.

- ATI Performance Products

- Hasse & Wrede

- Sumitomo Riko

- Hutchinson SA

- ZF Friedrichshafen AG

- Voith GmbH

- LORD Corporation

Frequently Asked Questions

The global torsional vibration dampers (TVD) market is projected to reach US$ 1.9 billion in 2026.

The rising adoption of turbocharged and hybrid powertrains, stringent NVH and emissions regulations, and industrial engine modernization initiatives are key drivers of market growth.

The market is poised to witness a CAGR of 5.7% from 2026 to 2033.

The emerging hybrid and range-extended vehicle programs, industrial modernization, and adoption of advanced composite and smart damper technologies represent major opportunities for suppliers.

Schaeffler, ZF Friedrichshafen, Continental, Vibracoustic, Valeo, American Axle & Manufacturing, NTN Corporation, LuK are some of the key market players.